STRABAG PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and environmental regulations are reshaping STRABAG’s strategic outlook in our concise PESTLE snapshot. This analysis highlights risks and opportunities that matter to investors and planners. Buy the full PESTLE for a detailed, ready-to-use report you can download instantly.

Political factors

EU infrastructure and public procurement policy

Large portions of STRABAG’s backlog hinge on government-funded work as EU public procurement equals about 14% of GDP (~€2tn/year); changes in 2021–27 cohesion funding and NextGenerationEU/RRF (€723.8bn) plus TEN-T CEF allocations (€33.7bn) can speed or stall pipelines. Tender transparency, local-content and ESG rules materially affect win rates and margins, while political stability in core markets supports predictable award cycles.

Geopolitical tensions and regional risk

Russia's full-scale invasion of Ukraine since February 2022, widespread EU/US sanctions and recurring supply‑route disruptions have tightened material availability, raised insurance and site‑security costs across Europe; Eastern and Southeastern exposures show higher political and payment risk. With defense and critical‑infrastructure budgets rising to record levels in 2023, STRABAG must adopt risk‑adjusted pricing and robust contingency planning.

Permitting and planning regimes

Lengthy, decentralized permitting in Europe often delays project starts by 12–24 months, raising holding costs and financing charges for STRABAG on large civil and infra projects. Fast-track policies for renewables, rail, and energy-transition assets—supporting the EU renewables target of 42.5% by 2030—create bidding opportunities. Political pressure to streamline environmental approvals may shorten lead times but tighten compliance and penalties. Proactive stakeholder engagement with municipalities is critical to unlock local acceptance and reduce delays.

Subsidies and green industrial policy

National incentives for energy efficiency, heat pumps and low-carbon cement—driven by the EU Fit for 55 target (55% GHG reduction by 2030)—shift demand toward retrofits and sustainable materials; PPPs benefit from clear policy support and risk-sharing frameworks, but volatility in subsidy budgets creates stop‑start order cycles, so STRABAG’s skill in structuring subsidy‑eligible projects directly affects pipeline quality.

- Incentives steer retrofit and low‑carbon material demand

- PPPs strengthened by policy and risk‑sharing

- Subsidy volatility causes stop‑go orders

- STRABAG project structuring determines pipeline quality

Trade, labor mobility, and cross-border rules

EU freedom of movement eases STRABAG staffing across sites, with intra-EU movers comprising roughly 3–4% of the workforce (Eurostat 2023), though migration debates can trigger tighter national measures. Import tariffs or export controls on steel and machinery (EU safeguards active in 2023–24) can raise material baselines and margins. Cross-border VAT and posting-of-workers rules increase compliance costs; reshoring policies in 2024 boost demand for domestic suppliers.

- mobility: 3–4% intra-EU workforce (Eurostat 2023)

- materials: EU steel safeguards 2023–24 raise input risk

- compliance: VAT/posting rules increase overhead

- reshoring: 2024 policies favor domestic sourcing

EU procurement shifts, rising costs and permitting delays reshape infrastructure pipelines

STRABAG depends heavily on EU public procurement (~€2tn/yr) and recovery funding (NextGenerationEU/RRF €723.8bn; CEF TEN‑T €33.7bn), so shifts in allocations reshape pipelines. Russia war/sanctions since 2022 raised insurance/material costs and Eastern risk; defense budgets rose in 2023. Permitting delays (12–24 months) but fast‑track renewable targets (42.5% by 2030) create mixed opportunities.

| Metric | Value |

|---|---|

| EU procurement | ~€2tn/yr |

| RRF/NGEU | €723.8bn |

| Intra‑EU movers | 3–4% (Eurostat 2023) |

What is included in the product

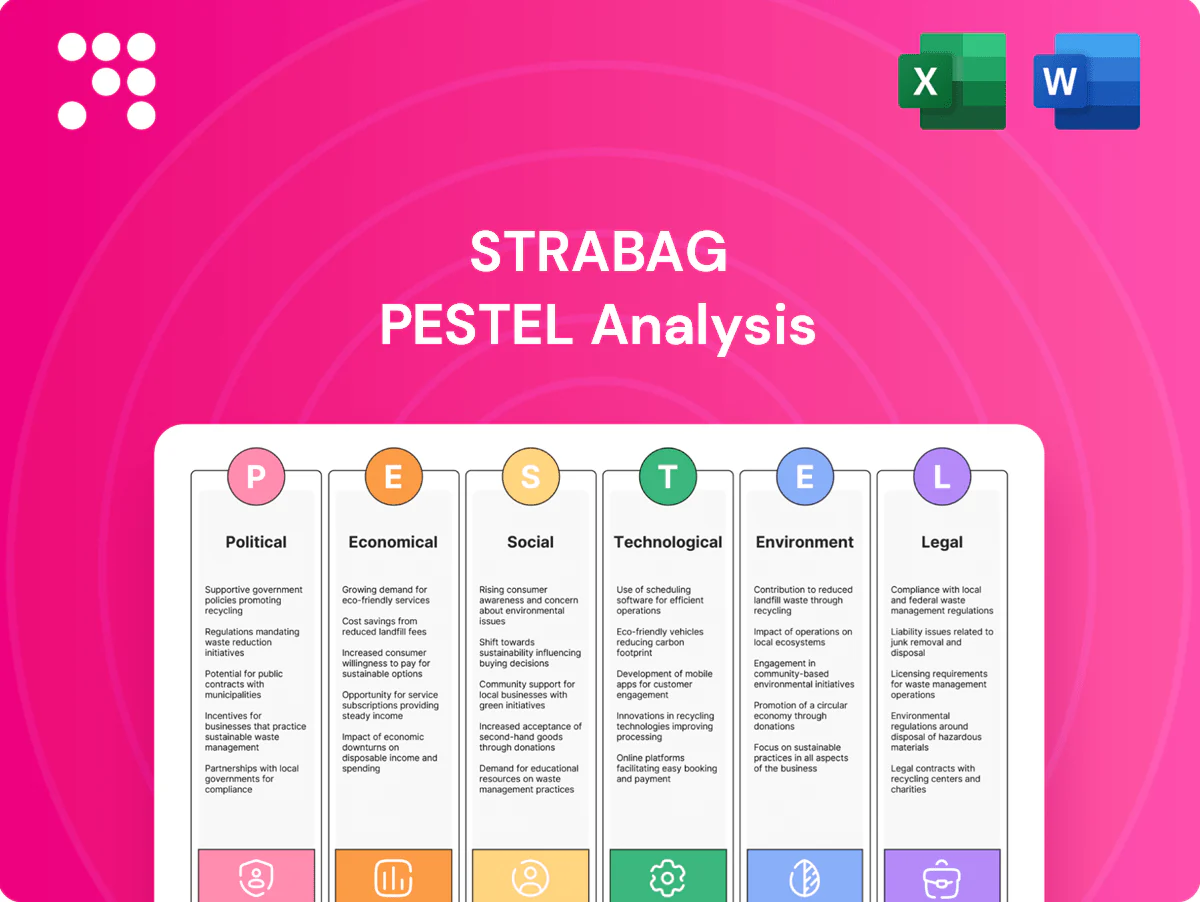

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely affect STRABAG, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it offers forward-looking insights, scenario planning support, and ready-to-use formatting for reports and pitches.

A concise, visually segmented STRABAG PESTLE summary that teams can drop into slides or share for quick alignment on external risks and market positioning; editable for region- or business-line‑specific notes to streamline planning and client reporting.

Economic factors

Construction cycle sensitivity

STRABAG’s top-line closely tracks GDP, public capex and private real estate cycles: 2024 group revenue ~€18.3bn and order backlog ~€17.8bn, reflecting sensitivity to construction demand swings.

Civil and infrastructure works (transport, utilities) historically outperformed commercial building in downturns, cushioning revenue declines.

Geographic and segment-diversified backlog plus counter-cyclical maintenance and facility services provide additional volatility mitigation.

Interest rates and financing conditions

Higher rates raise discount rates for developers and slow new project starts as German 10y bund yields traded around 2.5% in mid‑2025 and construction lending spreads have widened roughly 100bps since 2022, reducing NPV for greenfield bids. PPP and concession economics hinge on long‑term funding costs and spreads (swap‑to‑bond gaps near 150bps), while client credit stress (speculative‑grade default rates ~3.5% YTD 2025) pressures receivables, making hedging and strict working‑capital discipline margin‑critical.

Material and energy input costs

Volatility in cement, steel, bitumen and diesel materially shapes STRABAG bid pricing and execution risk, with European hot-rolled coil averaging ~900 EUR/tonne in 2024 and bitumen trading near 450 EUR/tonne. Eurostat reports EU diesel pump prices averaged ~1.72 EUR/L in 2024, squeezing asphalt and batching economics during energy-price shocks. Indexation clauses and long-term supplier frameworks help pass through inflation. Strategic procurement and inventory timing protect gross margins.

Labor availability and wage inflation

Skilled trades shortages are elevating wage pressures and subcontractor rates for STRABAG, with EU unemployment ~6.1% in 2024 tightening supply; productivity initiatives and modularization are used to offset unit labor cost increases. Training pipelines and cross-border crews ease peak-season gaps but tight markets raise schedule risk and penalty exposure.

- Skilled shortages → higher subcontractor rates

- Modularization → productivity gains

- Training/cross-border crews for peaks

- Tight labor markets → increased schedule/penalty risk

Currency and emerging market exposure

Multi-country STRABAG operations face EUR versus CEE currency swings that affect local costs and euro revenues, requiring active FX management; equipment purchases and imported materials create mismatches that must be hedged. Macro stress in non-core markets often delays receivables, while a shift toward euro-denominated contracts reduces earnings volatility.

- FX exposure: hedging needed

- Receivables risk: delayed payments in stressed markets

- Mitigation: euro contracts lower volatility

EU procurement shifts, rising costs and permitting delays reshape infrastructure pipelines

STRABAG revenue ~€18.3bn (2024) and backlog ~€17.8bn show GDP and capex sensitivity; civil works cushion downturns. Rising funding costs (German 10y ~2.5% mid‑2025) and wider lending spreads (~+100bps since 2022) pressure new starts and PPP economics. Input-price volatility (HRC ~€900/t, bitumen ~€450/t, diesel €1.72/L in 2024) and tight EU labor (6.1% 2024) elevate margin and schedule risk.

| Metric | Value |

|---|---|

| 2024 Revenue | €18.3bn |

| Order backlog | €17.8bn |

| German 10y | ~2.5% (mid‑2025) |

| HRC | ~€900/t (2024) |

| Diesel EU | €1.72/L (2024) |

| EU unemployment | 6.1% (2024) |

Preview Before You Purchase

STRABAG PESTLE Analysis

The preview shown here is the exact STRABAG PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible in this sample are identical to the downloadable file delivered immediately after payment. No placeholders or teasers—this is the final, professionally structured report.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and environmental regulations are reshaping STRABAG’s strategic outlook in our concise PESTLE snapshot. This analysis highlights risks and opportunities that matter to investors and planners. Buy the full PESTLE for a detailed, ready-to-use report you can download instantly.

Political factors

EU infrastructure and public procurement policy

Large portions of STRABAG’s backlog hinge on government-funded work as EU public procurement equals about 14% of GDP (~€2tn/year); changes in 2021–27 cohesion funding and NextGenerationEU/RRF (€723.8bn) plus TEN-T CEF allocations (€33.7bn) can speed or stall pipelines. Tender transparency, local-content and ESG rules materially affect win rates and margins, while political stability in core markets supports predictable award cycles.

Geopolitical tensions and regional risk

Russia's full-scale invasion of Ukraine since February 2022, widespread EU/US sanctions and recurring supply‑route disruptions have tightened material availability, raised insurance and site‑security costs across Europe; Eastern and Southeastern exposures show higher political and payment risk. With defense and critical‑infrastructure budgets rising to record levels in 2023, STRABAG must adopt risk‑adjusted pricing and robust contingency planning.

Permitting and planning regimes

Lengthy, decentralized permitting in Europe often delays project starts by 12–24 months, raising holding costs and financing charges for STRABAG on large civil and infra projects. Fast-track policies for renewables, rail, and energy-transition assets—supporting the EU renewables target of 42.5% by 2030—create bidding opportunities. Political pressure to streamline environmental approvals may shorten lead times but tighten compliance and penalties. Proactive stakeholder engagement with municipalities is critical to unlock local acceptance and reduce delays.

Subsidies and green industrial policy

National incentives for energy efficiency, heat pumps and low-carbon cement—driven by the EU Fit for 55 target (55% GHG reduction by 2030)—shift demand toward retrofits and sustainable materials; PPPs benefit from clear policy support and risk-sharing frameworks, but volatility in subsidy budgets creates stop‑start order cycles, so STRABAG’s skill in structuring subsidy‑eligible projects directly affects pipeline quality.

- Incentives steer retrofit and low‑carbon material demand

- PPPs strengthened by policy and risk‑sharing

- Subsidy volatility causes stop‑go orders

- STRABAG project structuring determines pipeline quality

Trade, labor mobility, and cross-border rules

EU freedom of movement eases STRABAG staffing across sites, with intra-EU movers comprising roughly 3–4% of the workforce (Eurostat 2023), though migration debates can trigger tighter national measures. Import tariffs or export controls on steel and machinery (EU safeguards active in 2023–24) can raise material baselines and margins. Cross-border VAT and posting-of-workers rules increase compliance costs; reshoring policies in 2024 boost demand for domestic suppliers.

- mobility: 3–4% intra-EU workforce (Eurostat 2023)

- materials: EU steel safeguards 2023–24 raise input risk

- compliance: VAT/posting rules increase overhead

- reshoring: 2024 policies favor domestic sourcing

EU procurement shifts, rising costs and permitting delays reshape infrastructure pipelines

STRABAG depends heavily on EU public procurement (~€2tn/yr) and recovery funding (NextGenerationEU/RRF €723.8bn; CEF TEN‑T €33.7bn), so shifts in allocations reshape pipelines. Russia war/sanctions since 2022 raised insurance/material costs and Eastern risk; defense budgets rose in 2023. Permitting delays (12–24 months) but fast‑track renewable targets (42.5% by 2030) create mixed opportunities.

| Metric | Value |

|---|---|

| EU procurement | ~€2tn/yr |

| RRF/NGEU | €723.8bn |

| Intra‑EU movers | 3–4% (Eurostat 2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely affect STRABAG, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it offers forward-looking insights, scenario planning support, and ready-to-use formatting for reports and pitches.

A concise, visually segmented STRABAG PESTLE summary that teams can drop into slides or share for quick alignment on external risks and market positioning; editable for region- or business-line‑specific notes to streamline planning and client reporting.

Economic factors

Construction cycle sensitivity

STRABAG’s top-line closely tracks GDP, public capex and private real estate cycles: 2024 group revenue ~€18.3bn and order backlog ~€17.8bn, reflecting sensitivity to construction demand swings.

Civil and infrastructure works (transport, utilities) historically outperformed commercial building in downturns, cushioning revenue declines.

Geographic and segment-diversified backlog plus counter-cyclical maintenance and facility services provide additional volatility mitigation.

Interest rates and financing conditions

Higher rates raise discount rates for developers and slow new project starts as German 10y bund yields traded around 2.5% in mid‑2025 and construction lending spreads have widened roughly 100bps since 2022, reducing NPV for greenfield bids. PPP and concession economics hinge on long‑term funding costs and spreads (swap‑to‑bond gaps near 150bps), while client credit stress (speculative‑grade default rates ~3.5% YTD 2025) pressures receivables, making hedging and strict working‑capital discipline margin‑critical.

Material and energy input costs

Volatility in cement, steel, bitumen and diesel materially shapes STRABAG bid pricing and execution risk, with European hot-rolled coil averaging ~900 EUR/tonne in 2024 and bitumen trading near 450 EUR/tonne. Eurostat reports EU diesel pump prices averaged ~1.72 EUR/L in 2024, squeezing asphalt and batching economics during energy-price shocks. Indexation clauses and long-term supplier frameworks help pass through inflation. Strategic procurement and inventory timing protect gross margins.

Labor availability and wage inflation

Skilled trades shortages are elevating wage pressures and subcontractor rates for STRABAG, with EU unemployment ~6.1% in 2024 tightening supply; productivity initiatives and modularization are used to offset unit labor cost increases. Training pipelines and cross-border crews ease peak-season gaps but tight markets raise schedule risk and penalty exposure.

- Skilled shortages → higher subcontractor rates

- Modularization → productivity gains

- Training/cross-border crews for peaks

- Tight labor markets → increased schedule/penalty risk

Currency and emerging market exposure

Multi-country STRABAG operations face EUR versus CEE currency swings that affect local costs and euro revenues, requiring active FX management; equipment purchases and imported materials create mismatches that must be hedged. Macro stress in non-core markets often delays receivables, while a shift toward euro-denominated contracts reduces earnings volatility.

- FX exposure: hedging needed

- Receivables risk: delayed payments in stressed markets

- Mitigation: euro contracts lower volatility

EU procurement shifts, rising costs and permitting delays reshape infrastructure pipelines

STRABAG revenue ~€18.3bn (2024) and backlog ~€17.8bn show GDP and capex sensitivity; civil works cushion downturns. Rising funding costs (German 10y ~2.5% mid‑2025) and wider lending spreads (~+100bps since 2022) pressure new starts and PPP economics. Input-price volatility (HRC ~€900/t, bitumen ~€450/t, diesel €1.72/L in 2024) and tight EU labor (6.1% 2024) elevate margin and schedule risk.

| Metric | Value |

|---|---|

| 2024 Revenue | €18.3bn |

| Order backlog | €17.8bn |

| German 10y | ~2.5% (mid‑2025) |

| HRC | ~€900/t (2024) |

| Diesel EU | €1.72/L (2024) |

| EU unemployment | 6.1% (2024) |

Preview Before You Purchase

STRABAG PESTLE Analysis

The preview shown here is the exact STRABAG PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible in this sample are identical to the downloadable file delivered immediately after payment. No placeholders or teasers—this is the final, professionally structured report.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and environmental regulations are reshaping STRABAG’s strategic outlook in our concise PESTLE snapshot. This analysis highlights risks and opportunities that matter to investors and planners. Buy the full PESTLE for a detailed, ready-to-use report you can download instantly.

Political factors

EU infrastructure and public procurement policy

Large portions of STRABAG’s backlog hinge on government-funded work as EU public procurement equals about 14% of GDP (~€2tn/year); changes in 2021–27 cohesion funding and NextGenerationEU/RRF (€723.8bn) plus TEN-T CEF allocations (€33.7bn) can speed or stall pipelines. Tender transparency, local-content and ESG rules materially affect win rates and margins, while political stability in core markets supports predictable award cycles.

Geopolitical tensions and regional risk

Russia's full-scale invasion of Ukraine since February 2022, widespread EU/US sanctions and recurring supply‑route disruptions have tightened material availability, raised insurance and site‑security costs across Europe; Eastern and Southeastern exposures show higher political and payment risk. With defense and critical‑infrastructure budgets rising to record levels in 2023, STRABAG must adopt risk‑adjusted pricing and robust contingency planning.

Permitting and planning regimes

Lengthy, decentralized permitting in Europe often delays project starts by 12–24 months, raising holding costs and financing charges for STRABAG on large civil and infra projects. Fast-track policies for renewables, rail, and energy-transition assets—supporting the EU renewables target of 42.5% by 2030—create bidding opportunities. Political pressure to streamline environmental approvals may shorten lead times but tighten compliance and penalties. Proactive stakeholder engagement with municipalities is critical to unlock local acceptance and reduce delays.

Subsidies and green industrial policy

National incentives for energy efficiency, heat pumps and low-carbon cement—driven by the EU Fit for 55 target (55% GHG reduction by 2030)—shift demand toward retrofits and sustainable materials; PPPs benefit from clear policy support and risk-sharing frameworks, but volatility in subsidy budgets creates stop‑start order cycles, so STRABAG’s skill in structuring subsidy‑eligible projects directly affects pipeline quality.

- Incentives steer retrofit and low‑carbon material demand

- PPPs strengthened by policy and risk‑sharing

- Subsidy volatility causes stop‑go orders

- STRABAG project structuring determines pipeline quality

Trade, labor mobility, and cross-border rules

EU freedom of movement eases STRABAG staffing across sites, with intra-EU movers comprising roughly 3–4% of the workforce (Eurostat 2023), though migration debates can trigger tighter national measures. Import tariffs or export controls on steel and machinery (EU safeguards active in 2023–24) can raise material baselines and margins. Cross-border VAT and posting-of-workers rules increase compliance costs; reshoring policies in 2024 boost demand for domestic suppliers.

- mobility: 3–4% intra-EU workforce (Eurostat 2023)

- materials: EU steel safeguards 2023–24 raise input risk

- compliance: VAT/posting rules increase overhead

- reshoring: 2024 policies favor domestic sourcing

EU procurement shifts, rising costs and permitting delays reshape infrastructure pipelines

STRABAG depends heavily on EU public procurement (~€2tn/yr) and recovery funding (NextGenerationEU/RRF €723.8bn; CEF TEN‑T €33.7bn), so shifts in allocations reshape pipelines. Russia war/sanctions since 2022 raised insurance/material costs and Eastern risk; defense budgets rose in 2023. Permitting delays (12–24 months) but fast‑track renewable targets (42.5% by 2030) create mixed opportunities.

| Metric | Value |

|---|---|

| EU procurement | ~€2tn/yr |

| RRF/NGEU | €723.8bn |

| Intra‑EU movers | 3–4% (Eurostat 2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely affect STRABAG, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it offers forward-looking insights, scenario planning support, and ready-to-use formatting for reports and pitches.

A concise, visually segmented STRABAG PESTLE summary that teams can drop into slides or share for quick alignment on external risks and market positioning; editable for region- or business-line‑specific notes to streamline planning and client reporting.

Economic factors

Construction cycle sensitivity

STRABAG’s top-line closely tracks GDP, public capex and private real estate cycles: 2024 group revenue ~€18.3bn and order backlog ~€17.8bn, reflecting sensitivity to construction demand swings.

Civil and infrastructure works (transport, utilities) historically outperformed commercial building in downturns, cushioning revenue declines.

Geographic and segment-diversified backlog plus counter-cyclical maintenance and facility services provide additional volatility mitigation.

Interest rates and financing conditions

Higher rates raise discount rates for developers and slow new project starts as German 10y bund yields traded around 2.5% in mid‑2025 and construction lending spreads have widened roughly 100bps since 2022, reducing NPV for greenfield bids. PPP and concession economics hinge on long‑term funding costs and spreads (swap‑to‑bond gaps near 150bps), while client credit stress (speculative‑grade default rates ~3.5% YTD 2025) pressures receivables, making hedging and strict working‑capital discipline margin‑critical.

Material and energy input costs

Volatility in cement, steel, bitumen and diesel materially shapes STRABAG bid pricing and execution risk, with European hot-rolled coil averaging ~900 EUR/tonne in 2024 and bitumen trading near 450 EUR/tonne. Eurostat reports EU diesel pump prices averaged ~1.72 EUR/L in 2024, squeezing asphalt and batching economics during energy-price shocks. Indexation clauses and long-term supplier frameworks help pass through inflation. Strategic procurement and inventory timing protect gross margins.

Labor availability and wage inflation

Skilled trades shortages are elevating wage pressures and subcontractor rates for STRABAG, with EU unemployment ~6.1% in 2024 tightening supply; productivity initiatives and modularization are used to offset unit labor cost increases. Training pipelines and cross-border crews ease peak-season gaps but tight markets raise schedule risk and penalty exposure.

- Skilled shortages → higher subcontractor rates

- Modularization → productivity gains

- Training/cross-border crews for peaks

- Tight labor markets → increased schedule/penalty risk

Currency and emerging market exposure

Multi-country STRABAG operations face EUR versus CEE currency swings that affect local costs and euro revenues, requiring active FX management; equipment purchases and imported materials create mismatches that must be hedged. Macro stress in non-core markets often delays receivables, while a shift toward euro-denominated contracts reduces earnings volatility.

- FX exposure: hedging needed

- Receivables risk: delayed payments in stressed markets

- Mitigation: euro contracts lower volatility

EU procurement shifts, rising costs and permitting delays reshape infrastructure pipelines

STRABAG revenue ~€18.3bn (2024) and backlog ~€17.8bn show GDP and capex sensitivity; civil works cushion downturns. Rising funding costs (German 10y ~2.5% mid‑2025) and wider lending spreads (~+100bps since 2022) pressure new starts and PPP economics. Input-price volatility (HRC ~€900/t, bitumen ~€450/t, diesel €1.72/L in 2024) and tight EU labor (6.1% 2024) elevate margin and schedule risk.

| Metric | Value |

|---|---|

| 2024 Revenue | €18.3bn |

| Order backlog | €17.8bn |

| German 10y | ~2.5% (mid‑2025) |

| HRC | ~€900/t (2024) |

| Diesel EU | €1.72/L (2024) |

| EU unemployment | 6.1% (2024) |

Preview Before You Purchase

STRABAG PESTLE Analysis

The preview shown here is the exact STRABAG PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible in this sample are identical to the downloadable file delivered immediately after payment. No placeholders or teasers—this is the final, professionally structured report.