STRATEC Porter's Five Forces Analysis

From Overview to Strategy Blueprint

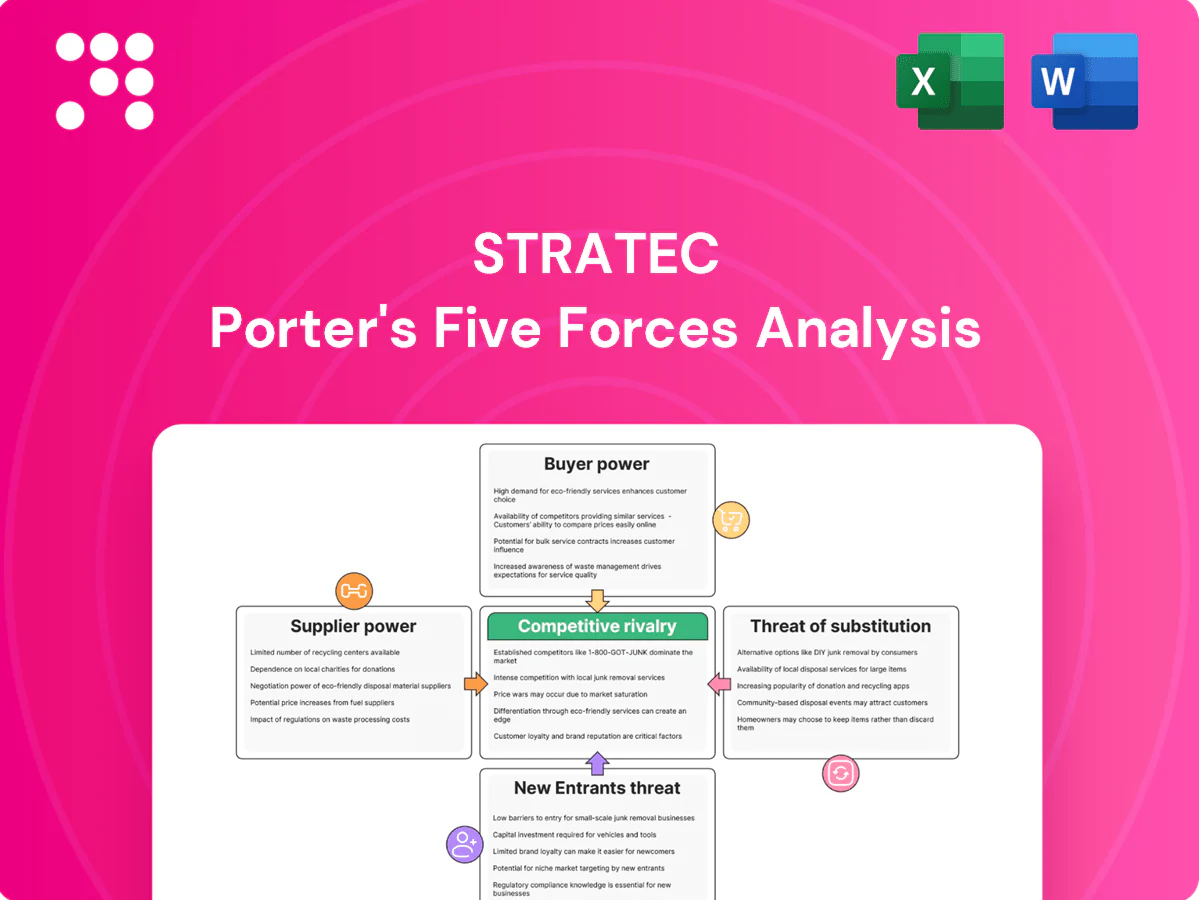

STRATEC’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer power, substitute threats, and barriers to entry shaping its med-tech niche. These forces reveal strategic risks and growth levers that inform investment and corporate strategy. This preview only scratches the surface—unlock the full analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized component dependence

STRATEC depends on niche optics, sensors, precision mechatronics and microfluidics where qualified vendors are often scarce, giving suppliers pricing and scheduling leverage. Lead times for critical modules commonly run 12–24 weeks and ISO 13485 qualification cycles typically take 6–12 months, making rapid supplier switches impractical. This concentration elevates supplier power over uptime and margins.

Regulatory-locked supply base

As of 2024, STRATEC faces a regulatory-locked supply base where medical device QMS (ISO 13485), biocompatibility requirements (ISO 10993) and validated processes limit supplier substitution. Any supplier change typically triggers revalidation, design control documentation and potential FDA/Notified Body notifications (21 CFR 820/MD regulations), raising switching costs and strengthening supplier bargaining power; long-term approved vendor lists further entrench incumbents.

Dual-sourcing mitigations

For commoditized parts and plastics STRATEC can materially reduce supplier risk via dual-sourcing and framework agreements, supported by typical industry safety stocks of 30–90 days to cushion volatility. True redundancy for bespoke diagnostic assemblies is often infeasible, concentrating bargaining power for those critical items. Net effect: mixed supplier power that varies by part criticality and supply-chain complexity.

Scale and long-term volumes

Multi-year OEM programs (commonly 3–7 years in diagnostics) give STRATEC suppliers predictable demand and volume visibility, enabling better pricing and prioritized capacity allocation; aggregated purchasing across STRATEC platforms further strengthens negotiating leverage and partly offsets supplier power on price and service.

- Long-term contracts: predictable demand

- Volume visibility: improved terms/capacity

- Aggregated purchasing: reduced supplier leverage

Upstream tech roadmaps

Suppliers drive innovation in optics, chips and embedded software stacks, and STRATEC's dependence on those roadmaps can swing BOM costs and time-to-market; industry-wide semiconductor sales approached roughly 600 billion USD in 2024, reinforcing supplier leverage. Early co-development aligns incentives but can lock STRATEC into supplier designs; timing and exclusivity clauses materially shape bargaining power.

- Supplier-led R&D increases BOM volatility

- 2024 semiconductors ~600B USD elevates supplier leverage

- Co-development reduces mismatch but risks lock-in

- Timing/exclusivity clauses determine negotiation leverage

Niche optics lead times and supplier power raise switching costs; $600B chip market shifts leverage

STRATEC faces strong supplier power for niche optics, sensors and microfluidics (12–24 wk lead times; ISO 13485 requal 6–12 mo), raising switching costs. Commodities use dual-sourcing (30–90 days stock); semiconductor market ~$600B (2024) increases chip leverage; 3–7 yr OEM contracts partly offset power.

| Metric | Value |

|---|---|

| Lead times | 12–24 wk |

| Requalification | 6–12 mo |

| Safety stock | 30–90 days |

| Semiconductor market | $600B (2024) |

What is included in the product

Tailored Porter's Five Forces for STRATEC, detailing competitive rivalry, supplier and buyer power, substitute threats, and barriers to entry while highlighting disruptive technologies and strategic levers for protecting market position.

Clear one-sheet Porter's Five Forces for STRATEC—instantly visualise competitive pressure with a radar chart, customise force levels and notes for changing market conditions, and drop the clean layout straight into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Concentrated OEM customers

Concentrated OEM customers—large diagnostics firms with professional procurement—dominate demand, using their scale to enforce tough pricing, SLA and warranty terms; the global IVD market was about $95 billion in 2024, amplifying their leverage. For STRATEC, reliance on a few OEMs means losing one account can shave off mid-single to double-digit percent of annual revenues, elevating buyer bargaining power.

High switching costs

Design-in cycles, regulatory filings and workflow integration create strong lock-in for STRATEC OEM customers; switching partners risks delays and revalidation часто taking 6–12 months and costing up to €200k–€300k, so buyers tolerate price pressure post-launch and switching propensity remains low, softening buyer power.

Customization and co-development

Bespoke platforms increase buyer dependency on STRATEC expertise, with co-funded development commonly trading up to 10% margin for multi-year volume commitments; STRATEC reported roughly €280m revenue in 2024, highlighting scale benefits. Milestone gates and IP ownership terms serve as key negotiation levers, shifting risk and pricing. Buyers wield strongest influence during development but lose leverage after scale-up and volume ramp.

Total cost of ownership focus

Buyers now evaluate uptime, consumables, service and lifecycle costs, pushing STRATEC discussions toward total cost of ownership; strong field reliability supports premium pricing and reduces churn. Performance-linked KPIs in 2024 increasingly dictate margin allocation and risk-sharing, shifting negotiations from unit price to measurable outcomes.

- Uptime-focused procurement

- Service-heavy TCO

- KPI-linked margins

Global service expectations

Tier-1 diagnostics customers demand global service coverage and parts availability, forcing STRATEC to maintain expanded spare-part inventories and regional service teams, which elevates its cost base and compresses margins. Buyers increasingly include service-level penalties and credit clauses in contracts, shifting risk to suppliers and strengthening their negotiating position. This service leverage makes buyers more price- and terms-sensitive, amplifying their bargaining power in 2024.

OEM concentration in $95B IVD market risks mid-single to double-digit% of a €280m supplier

Concentrated OEMs (~95B USD IVD market in 2024) exert strong price and SLA pressure; losing one OEM can cut mid-single to double-digit percent of STRATEC revenue (STRATEC ~€280m in 2024). Design-in and regulatory lock-in (6–12 months, €200k–€300k) reduce switching. Service/SLA demands raise OPEX and shift risk, increasing buyer bargaining power.

| Metric | 2024 value |

|---|---|

| Global IVD market | $95B |

| STRATEC revenue | €280m |

| Switch cost/time | €200k–€300k / 6–12m |

Preview Before You Purchase

STRATEC Porter's Five Forces Analysis

This preview shows the exact STRATEC Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy. You're looking at the actual deliverable with all findings, data and recommendations included.

From Overview to Strategy Blueprint

STRATEC’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer power, substitute threats, and barriers to entry shaping its med-tech niche. These forces reveal strategic risks and growth levers that inform investment and corporate strategy. This preview only scratches the surface—unlock the full analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized component dependence

STRATEC depends on niche optics, sensors, precision mechatronics and microfluidics where qualified vendors are often scarce, giving suppliers pricing and scheduling leverage. Lead times for critical modules commonly run 12–24 weeks and ISO 13485 qualification cycles typically take 6–12 months, making rapid supplier switches impractical. This concentration elevates supplier power over uptime and margins.

Regulatory-locked supply base

As of 2024, STRATEC faces a regulatory-locked supply base where medical device QMS (ISO 13485), biocompatibility requirements (ISO 10993) and validated processes limit supplier substitution. Any supplier change typically triggers revalidation, design control documentation and potential FDA/Notified Body notifications (21 CFR 820/MD regulations), raising switching costs and strengthening supplier bargaining power; long-term approved vendor lists further entrench incumbents.

Dual-sourcing mitigations

For commoditized parts and plastics STRATEC can materially reduce supplier risk via dual-sourcing and framework agreements, supported by typical industry safety stocks of 30–90 days to cushion volatility. True redundancy for bespoke diagnostic assemblies is often infeasible, concentrating bargaining power for those critical items. Net effect: mixed supplier power that varies by part criticality and supply-chain complexity.

Scale and long-term volumes

Multi-year OEM programs (commonly 3–7 years in diagnostics) give STRATEC suppliers predictable demand and volume visibility, enabling better pricing and prioritized capacity allocation; aggregated purchasing across STRATEC platforms further strengthens negotiating leverage and partly offsets supplier power on price and service.

- Long-term contracts: predictable demand

- Volume visibility: improved terms/capacity

- Aggregated purchasing: reduced supplier leverage

Upstream tech roadmaps

Suppliers drive innovation in optics, chips and embedded software stacks, and STRATEC's dependence on those roadmaps can swing BOM costs and time-to-market; industry-wide semiconductor sales approached roughly 600 billion USD in 2024, reinforcing supplier leverage. Early co-development aligns incentives but can lock STRATEC into supplier designs; timing and exclusivity clauses materially shape bargaining power.

- Supplier-led R&D increases BOM volatility

- 2024 semiconductors ~600B USD elevates supplier leverage

- Co-development reduces mismatch but risks lock-in

- Timing/exclusivity clauses determine negotiation leverage

Niche optics lead times and supplier power raise switching costs; $600B chip market shifts leverage

STRATEC faces strong supplier power for niche optics, sensors and microfluidics (12–24 wk lead times; ISO 13485 requal 6–12 mo), raising switching costs. Commodities use dual-sourcing (30–90 days stock); semiconductor market ~$600B (2024) increases chip leverage; 3–7 yr OEM contracts partly offset power.

| Metric | Value |

|---|---|

| Lead times | 12–24 wk |

| Requalification | 6–12 mo |

| Safety stock | 30–90 days |

| Semiconductor market | $600B (2024) |

What is included in the product

Tailored Porter's Five Forces for STRATEC, detailing competitive rivalry, supplier and buyer power, substitute threats, and barriers to entry while highlighting disruptive technologies and strategic levers for protecting market position.

Clear one-sheet Porter's Five Forces for STRATEC—instantly visualise competitive pressure with a radar chart, customise force levels and notes for changing market conditions, and drop the clean layout straight into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Concentrated OEM customers

Concentrated OEM customers—large diagnostics firms with professional procurement—dominate demand, using their scale to enforce tough pricing, SLA and warranty terms; the global IVD market was about $95 billion in 2024, amplifying their leverage. For STRATEC, reliance on a few OEMs means losing one account can shave off mid-single to double-digit percent of annual revenues, elevating buyer bargaining power.

High switching costs

Design-in cycles, regulatory filings and workflow integration create strong lock-in for STRATEC OEM customers; switching partners risks delays and revalidation часто taking 6–12 months and costing up to €200k–€300k, so buyers tolerate price pressure post-launch and switching propensity remains low, softening buyer power.

Customization and co-development

Bespoke platforms increase buyer dependency on STRATEC expertise, with co-funded development commonly trading up to 10% margin for multi-year volume commitments; STRATEC reported roughly €280m revenue in 2024, highlighting scale benefits. Milestone gates and IP ownership terms serve as key negotiation levers, shifting risk and pricing. Buyers wield strongest influence during development but lose leverage after scale-up and volume ramp.

Total cost of ownership focus

Buyers now evaluate uptime, consumables, service and lifecycle costs, pushing STRATEC discussions toward total cost of ownership; strong field reliability supports premium pricing and reduces churn. Performance-linked KPIs in 2024 increasingly dictate margin allocation and risk-sharing, shifting negotiations from unit price to measurable outcomes.

- Uptime-focused procurement

- Service-heavy TCO

- KPI-linked margins

Global service expectations

Tier-1 diagnostics customers demand global service coverage and parts availability, forcing STRATEC to maintain expanded spare-part inventories and regional service teams, which elevates its cost base and compresses margins. Buyers increasingly include service-level penalties and credit clauses in contracts, shifting risk to suppliers and strengthening their negotiating position. This service leverage makes buyers more price- and terms-sensitive, amplifying their bargaining power in 2024.

OEM concentration in $95B IVD market risks mid-single to double-digit% of a €280m supplier

Concentrated OEMs (~95B USD IVD market in 2024) exert strong price and SLA pressure; losing one OEM can cut mid-single to double-digit percent of STRATEC revenue (STRATEC ~€280m in 2024). Design-in and regulatory lock-in (6–12 months, €200k–€300k) reduce switching. Service/SLA demands raise OPEX and shift risk, increasing buyer bargaining power.

| Metric | 2024 value |

|---|---|

| Global IVD market | $95B |

| STRATEC revenue | €280m |

| Switch cost/time | €200k–€300k / 6–12m |

Preview Before You Purchase

STRATEC Porter's Five Forces Analysis

This preview shows the exact STRATEC Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy. You're looking at the actual deliverable with all findings, data and recommendations included.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

STRATEC’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer power, substitute threats, and barriers to entry shaping its med-tech niche. These forces reveal strategic risks and growth levers that inform investment and corporate strategy. This preview only scratches the surface—unlock the full analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized component dependence

STRATEC depends on niche optics, sensors, precision mechatronics and microfluidics where qualified vendors are often scarce, giving suppliers pricing and scheduling leverage. Lead times for critical modules commonly run 12–24 weeks and ISO 13485 qualification cycles typically take 6–12 months, making rapid supplier switches impractical. This concentration elevates supplier power over uptime and margins.

Regulatory-locked supply base

As of 2024, STRATEC faces a regulatory-locked supply base where medical device QMS (ISO 13485), biocompatibility requirements (ISO 10993) and validated processes limit supplier substitution. Any supplier change typically triggers revalidation, design control documentation and potential FDA/Notified Body notifications (21 CFR 820/MD regulations), raising switching costs and strengthening supplier bargaining power; long-term approved vendor lists further entrench incumbents.

Dual-sourcing mitigations

For commoditized parts and plastics STRATEC can materially reduce supplier risk via dual-sourcing and framework agreements, supported by typical industry safety stocks of 30–90 days to cushion volatility. True redundancy for bespoke diagnostic assemblies is often infeasible, concentrating bargaining power for those critical items. Net effect: mixed supplier power that varies by part criticality and supply-chain complexity.

Scale and long-term volumes

Multi-year OEM programs (commonly 3–7 years in diagnostics) give STRATEC suppliers predictable demand and volume visibility, enabling better pricing and prioritized capacity allocation; aggregated purchasing across STRATEC platforms further strengthens negotiating leverage and partly offsets supplier power on price and service.

- Long-term contracts: predictable demand

- Volume visibility: improved terms/capacity

- Aggregated purchasing: reduced supplier leverage

Upstream tech roadmaps

Suppliers drive innovation in optics, chips and embedded software stacks, and STRATEC's dependence on those roadmaps can swing BOM costs and time-to-market; industry-wide semiconductor sales approached roughly 600 billion USD in 2024, reinforcing supplier leverage. Early co-development aligns incentives but can lock STRATEC into supplier designs; timing and exclusivity clauses materially shape bargaining power.

- Supplier-led R&D increases BOM volatility

- 2024 semiconductors ~600B USD elevates supplier leverage

- Co-development reduces mismatch but risks lock-in

- Timing/exclusivity clauses determine negotiation leverage

Niche optics lead times and supplier power raise switching costs; $600B chip market shifts leverage

STRATEC faces strong supplier power for niche optics, sensors and microfluidics (12–24 wk lead times; ISO 13485 requal 6–12 mo), raising switching costs. Commodities use dual-sourcing (30–90 days stock); semiconductor market ~$600B (2024) increases chip leverage; 3–7 yr OEM contracts partly offset power.

| Metric | Value |

|---|---|

| Lead times | 12–24 wk |

| Requalification | 6–12 mo |

| Safety stock | 30–90 days |

| Semiconductor market | $600B (2024) |

What is included in the product

Tailored Porter's Five Forces for STRATEC, detailing competitive rivalry, supplier and buyer power, substitute threats, and barriers to entry while highlighting disruptive technologies and strategic levers for protecting market position.

Clear one-sheet Porter's Five Forces for STRATEC—instantly visualise competitive pressure with a radar chart, customise force levels and notes for changing market conditions, and drop the clean layout straight into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Concentrated OEM customers

Concentrated OEM customers—large diagnostics firms with professional procurement—dominate demand, using their scale to enforce tough pricing, SLA and warranty terms; the global IVD market was about $95 billion in 2024, amplifying their leverage. For STRATEC, reliance on a few OEMs means losing one account can shave off mid-single to double-digit percent of annual revenues, elevating buyer bargaining power.

High switching costs

Design-in cycles, regulatory filings and workflow integration create strong lock-in for STRATEC OEM customers; switching partners risks delays and revalidation часто taking 6–12 months and costing up to €200k–€300k, so buyers tolerate price pressure post-launch and switching propensity remains low, softening buyer power.

Customization and co-development

Bespoke platforms increase buyer dependency on STRATEC expertise, with co-funded development commonly trading up to 10% margin for multi-year volume commitments; STRATEC reported roughly €280m revenue in 2024, highlighting scale benefits. Milestone gates and IP ownership terms serve as key negotiation levers, shifting risk and pricing. Buyers wield strongest influence during development but lose leverage after scale-up and volume ramp.

Total cost of ownership focus

Buyers now evaluate uptime, consumables, service and lifecycle costs, pushing STRATEC discussions toward total cost of ownership; strong field reliability supports premium pricing and reduces churn. Performance-linked KPIs in 2024 increasingly dictate margin allocation and risk-sharing, shifting negotiations from unit price to measurable outcomes.

- Uptime-focused procurement

- Service-heavy TCO

- KPI-linked margins

Global service expectations

Tier-1 diagnostics customers demand global service coverage and parts availability, forcing STRATEC to maintain expanded spare-part inventories and regional service teams, which elevates its cost base and compresses margins. Buyers increasingly include service-level penalties and credit clauses in contracts, shifting risk to suppliers and strengthening their negotiating position. This service leverage makes buyers more price- and terms-sensitive, amplifying their bargaining power in 2024.

OEM concentration in $95B IVD market risks mid-single to double-digit% of a €280m supplier

Concentrated OEMs (~95B USD IVD market in 2024) exert strong price and SLA pressure; losing one OEM can cut mid-single to double-digit percent of STRATEC revenue (STRATEC ~€280m in 2024). Design-in and regulatory lock-in (6–12 months, €200k–€300k) reduce switching. Service/SLA demands raise OPEX and shift risk, increasing buyer bargaining power.

| Metric | 2024 value |

|---|---|

| Global IVD market | $95B |

| STRATEC revenue | €280m |

| Switch cost/time | €200k–€300k / 6–12m |

Preview Before You Purchase

STRATEC Porter's Five Forces Analysis

This preview shows the exact STRATEC Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy. You're looking at the actual deliverable with all findings, data and recommendations included.