STRATTEC Porter's Five Forces Analysis

From Overview to Strategy Blueprint

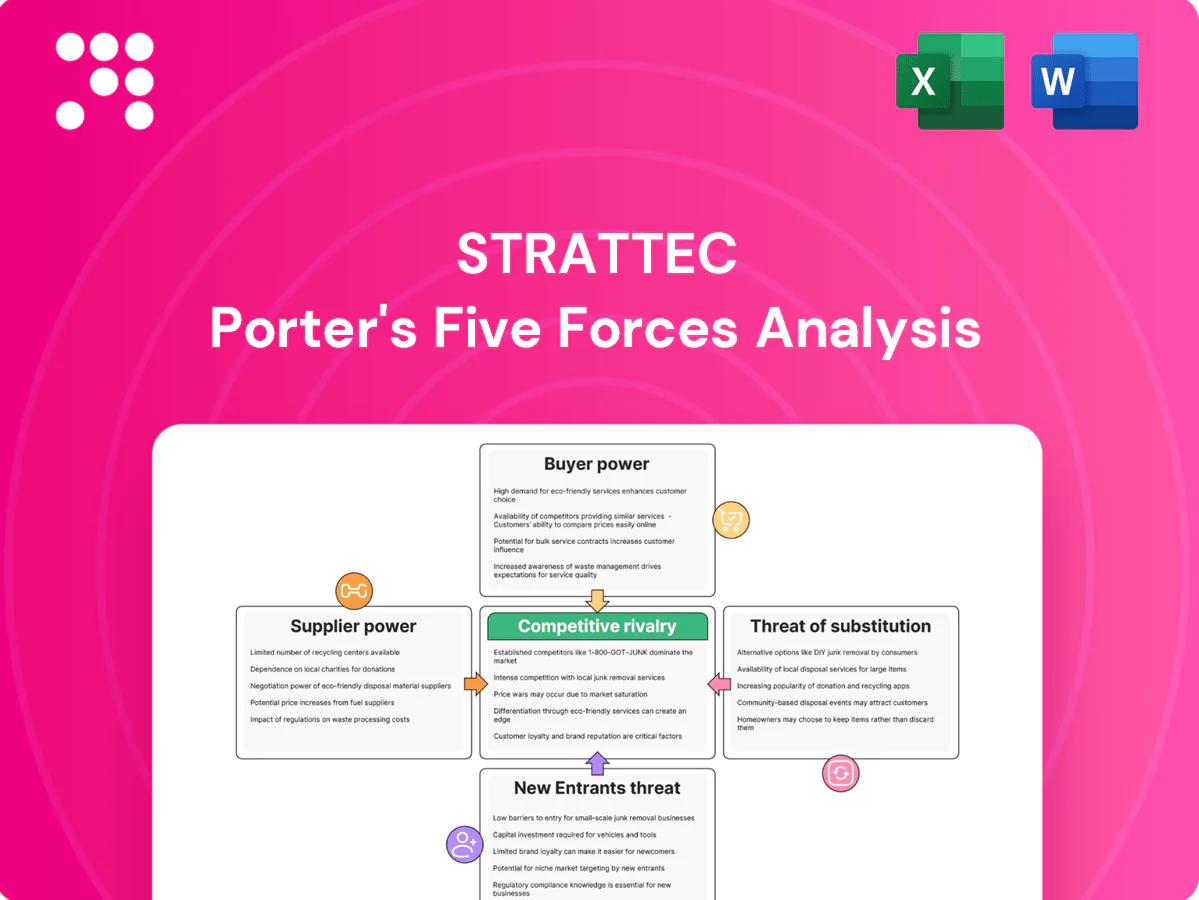

STRATTEC’s Porter's Five Forces snapshot highlights intense supplier negotiation for specialized components, moderate buyer power from OEMs, low threat of substitutes, and concentrated rivalry driven by scale and technology. Emerging entrants face high barriers due to certifications and capital needs. This preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Specialized materials and electronics

STRATTEC relies on proprietary alloys, precision stampings, micro-motors and semiconductors for mechatronic locks, and limited qualified sources for safety-critical parts concentrates supplier power. With the global semiconductor market about $600B in 2024 and wafer fab utilization near 90%, allocation often favors larger OEMs, raising costs and lead times (often 12–20+ weeks). Qualification cycles of 6–12 months impede rapid re-sourcing, sustaining supplier leverage.

High switching costs and tooling

Custom dies, molds and PPAP-qualified parts tie programs to specific suppliers; automotive tooling often costs $250k–$2M and PPAP/OEM validation typically takes 30–90 days, so changing vendors risks months-long delays, scrap and reapproval. Tooling amortization terms of 3–7 years commonly lock pricing and raise supplier bargaining power during renegotiations.

Quality and compliance constraints

IATF 16949, end-to-end traceability and strict safety standards shrink the supplier pool for STRATTEC, as only certified firms can support automotive PPAP, cybersecurity for electronics and ISO 26262 functional safety requirements. Non-conformances risk heavy penalties and production line-stops that cost OEMs thousands of dollars per minute, elevating operational exposure. This compliance scarcity strengthens incumbent, certified suppliers and raises switching costs.

Logistics and geopolitical exposure

Global supply chains for resins, metals and semiconductors face freight volatility, tariffs and regional disruptions that raised supplier leverage; spot freight and component surcharges pushed input costs higher, with suppliers passing through surcharges of roughly 8–12% in 2024, cyclically strengthening their bargaining position for firms like STRATTEC.

- Freight & surcharges: ~8–12% in 2024

- Nearshoring: reduces but not eliminates concentrated upstream capacity

- Geopolitical risk: elevates supplier pass-through power

Countervailing buyer volume leverage

Large OEM volumes in 2024 drive flow-down terms that temper supplier power; STRATTEC aggregates demand across platforms to secure better pricing and contract terms. Dual-qualifying key inputs mitigates single-source risk, but dual-sourcing complex locking systems increases cost and lengthens qualification timelines.

- OEM flow-downs reduce supplier margins

- Aggregated demand boosts negotiating leverage

- Dual-qualification lowers single-source risk

- Dual-sourcing raises cost and slows delivery

Chip supply strain: lead times 12–20+ wks, fabs ~90%

STRATTEC depends on proprietary materials and limited certified suppliers; global semiconductors ~$600B in 2024 and wafer fab utilization ~90% drive 12–20+ week lead times. Tooling ($250k–$2M) and qualification (6–12 months; PPAP 30–90 days) lock-in suppliers. Compliance and freight surcharges (~8–12% in 2024) increase supplier leverage, while OEM flow-downs and demand aggregation partially counterbalance.

| Metric | 2024 / Value |

|---|---|

| Semiconductor market | $600B |

| Wafer fab utilization | ~90% |

| Lead times | 12–20+ weeks |

| Tooling cost | $250k–$2M |

| Qualification | 6–12 months |

| Surcharges | 8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for STRATTEC, uncovering key drivers of competition, supplier and buyer influence, and barriers protecting incumbents. Identifies disruptive threats, substitutes, and market entry risks with strategic commentary for investor and strategic use.

A clear, one-sheet summary of STRATTEC's five forces—ideal for quick strategic decisions, investor briefs, and boardroom slides to relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated OEM customer base

Automotive OEMs are few, large and price-aggressive, with the top five OEMs accounting for roughly 50% of global light-vehicle production in 2024, giving them strong leverage over suppliers. They run competitive bids and enforce annual cost-downs typically of 2–4%, making program wins critical and increasing supplier dependence on each award. OEMs can also shape specifications to favor alternate suppliers, raising switching risk for STRATTEC.

High switching costs but dual-sourcing

While re-qualification for locks and latches is costly, OEMs routinely dual-source critical components, keeping price and service under constant pressure; performance scorecards directly influence future nominations. STRATTEC must continuously defend share through competitive pricing, quality and on-time delivery. Dual-sourcing preserves OEM leverage, forcing ongoing investment to retain business.

Long contracts with stringent SLAs

Long, multi-year platform contracts embed PPAP, warranty obligations and delivery-penalty clauses that lock suppliers into strict SLAs; buyers demand on-time delivery and zero-defect targets enforced through formal scorecards. Any lapse triggers chargebacks and jeopardizes future allocations, turning operational performance directly into economic risk; SLAs thus codify buyer bargaining power into measurable cash-flow consequences.

Design influence and integration

Access systems increasingly integrate with BCMs, cybersecurity stacks and vehicle architecture, and OEM engineering choices in 2024 continue to shift value from hardware to software, commoditizing locks and keys; early design-in still locks STRATTEC in but exposes it to OEM design dictates and cost pressures as buyers leverage integration to push prices down.

- Design-in locks position but limits margins

- Software value shift risks hardware commoditization

- OEM integration gives buyers leverage to reduce costs

Aftermarket offers limited counterbalance

Aftermarket sales diversify STRATTEC revenue but remain smaller and more price-sensitive than OE channels; independent parts buyers often prioritize cost over brand. OEM key-coding and immobilizer technology restrict independent replacement and require dealer or authorized programming, narrowing non-OE alternatives. This constraint limits STRATTEC pricing power outside original equipment channels and keeps buyer power elevated.

- Aftermarket: smaller, price-sensitive

- OEM immobilizers: restrict independent replacement

- Limits non-OE pricing power

- Net: elevated buyer leverage

OEM consolidation: top 5 hold ~50%, forcing 2–4%/yr supplier cost cuts

Automotive OEMs are few and large: top five OEMs accounted for roughly 50% of global light-vehicle production in 2024, giving them strong leverage and enforcing 2–4% annual cost-downs. Dual-sourcing and strict SLAs with chargebacks keep price and service pressure high; OEM software-led integration commoditizes hardware, limiting STRATTEC margins. Aftermarket remains smaller and more price-sensitive, constrained by OEM immobilizer controls.

| Metric (2024) | Value |

|---|---|

| Top-5 OEM share | ~50% |

| Typical OEM cost-downs | 2–4%/yr |

Full Version Awaits

STRATTEC Porter's Five Forces Analysis

This preview shows the exact STRATTEC Porter’s Five Forces Analysis you’ll receive—no placeholders, no samples. The document displayed is the full, professionally formatted analysis ready for immediate download upon purchase. You’re viewing the final deliverable, identical to the file you’ll get. Use it instantly for due diligence, strategy, or reporting.

From Overview to Strategy Blueprint

STRATTEC’s Porter's Five Forces snapshot highlights intense supplier negotiation for specialized components, moderate buyer power from OEMs, low threat of substitutes, and concentrated rivalry driven by scale and technology. Emerging entrants face high barriers due to certifications and capital needs. This preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Specialized materials and electronics

STRATTEC relies on proprietary alloys, precision stampings, micro-motors and semiconductors for mechatronic locks, and limited qualified sources for safety-critical parts concentrates supplier power. With the global semiconductor market about $600B in 2024 and wafer fab utilization near 90%, allocation often favors larger OEMs, raising costs and lead times (often 12–20+ weeks). Qualification cycles of 6–12 months impede rapid re-sourcing, sustaining supplier leverage.

High switching costs and tooling

Custom dies, molds and PPAP-qualified parts tie programs to specific suppliers; automotive tooling often costs $250k–$2M and PPAP/OEM validation typically takes 30–90 days, so changing vendors risks months-long delays, scrap and reapproval. Tooling amortization terms of 3–7 years commonly lock pricing and raise supplier bargaining power during renegotiations.

Quality and compliance constraints

IATF 16949, end-to-end traceability and strict safety standards shrink the supplier pool for STRATTEC, as only certified firms can support automotive PPAP, cybersecurity for electronics and ISO 26262 functional safety requirements. Non-conformances risk heavy penalties and production line-stops that cost OEMs thousands of dollars per minute, elevating operational exposure. This compliance scarcity strengthens incumbent, certified suppliers and raises switching costs.

Logistics and geopolitical exposure

Global supply chains for resins, metals and semiconductors face freight volatility, tariffs and regional disruptions that raised supplier leverage; spot freight and component surcharges pushed input costs higher, with suppliers passing through surcharges of roughly 8–12% in 2024, cyclically strengthening their bargaining position for firms like STRATTEC.

- Freight & surcharges: ~8–12% in 2024

- Nearshoring: reduces but not eliminates concentrated upstream capacity

- Geopolitical risk: elevates supplier pass-through power

Countervailing buyer volume leverage

Large OEM volumes in 2024 drive flow-down terms that temper supplier power; STRATTEC aggregates demand across platforms to secure better pricing and contract terms. Dual-qualifying key inputs mitigates single-source risk, but dual-sourcing complex locking systems increases cost and lengthens qualification timelines.

- OEM flow-downs reduce supplier margins

- Aggregated demand boosts negotiating leverage

- Dual-qualification lowers single-source risk

- Dual-sourcing raises cost and slows delivery

Chip supply strain: lead times 12–20+ wks, fabs ~90%

STRATTEC depends on proprietary materials and limited certified suppliers; global semiconductors ~$600B in 2024 and wafer fab utilization ~90% drive 12–20+ week lead times. Tooling ($250k–$2M) and qualification (6–12 months; PPAP 30–90 days) lock-in suppliers. Compliance and freight surcharges (~8–12% in 2024) increase supplier leverage, while OEM flow-downs and demand aggregation partially counterbalance.

| Metric | 2024 / Value |

|---|---|

| Semiconductor market | $600B |

| Wafer fab utilization | ~90% |

| Lead times | 12–20+ weeks |

| Tooling cost | $250k–$2M |

| Qualification | 6–12 months |

| Surcharges | 8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for STRATTEC, uncovering key drivers of competition, supplier and buyer influence, and barriers protecting incumbents. Identifies disruptive threats, substitutes, and market entry risks with strategic commentary for investor and strategic use.

A clear, one-sheet summary of STRATTEC's five forces—ideal for quick strategic decisions, investor briefs, and boardroom slides to relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated OEM customer base

Automotive OEMs are few, large and price-aggressive, with the top five OEMs accounting for roughly 50% of global light-vehicle production in 2024, giving them strong leverage over suppliers. They run competitive bids and enforce annual cost-downs typically of 2–4%, making program wins critical and increasing supplier dependence on each award. OEMs can also shape specifications to favor alternate suppliers, raising switching risk for STRATTEC.

High switching costs but dual-sourcing

While re-qualification for locks and latches is costly, OEMs routinely dual-source critical components, keeping price and service under constant pressure; performance scorecards directly influence future nominations. STRATTEC must continuously defend share through competitive pricing, quality and on-time delivery. Dual-sourcing preserves OEM leverage, forcing ongoing investment to retain business.

Long contracts with stringent SLAs

Long, multi-year platform contracts embed PPAP, warranty obligations and delivery-penalty clauses that lock suppliers into strict SLAs; buyers demand on-time delivery and zero-defect targets enforced through formal scorecards. Any lapse triggers chargebacks and jeopardizes future allocations, turning operational performance directly into economic risk; SLAs thus codify buyer bargaining power into measurable cash-flow consequences.

Design influence and integration

Access systems increasingly integrate with BCMs, cybersecurity stacks and vehicle architecture, and OEM engineering choices in 2024 continue to shift value from hardware to software, commoditizing locks and keys; early design-in still locks STRATTEC in but exposes it to OEM design dictates and cost pressures as buyers leverage integration to push prices down.

- Design-in locks position but limits margins

- Software value shift risks hardware commoditization

- OEM integration gives buyers leverage to reduce costs

Aftermarket offers limited counterbalance

Aftermarket sales diversify STRATTEC revenue but remain smaller and more price-sensitive than OE channels; independent parts buyers often prioritize cost over brand. OEM key-coding and immobilizer technology restrict independent replacement and require dealer or authorized programming, narrowing non-OE alternatives. This constraint limits STRATTEC pricing power outside original equipment channels and keeps buyer power elevated.

- Aftermarket: smaller, price-sensitive

- OEM immobilizers: restrict independent replacement

- Limits non-OE pricing power

- Net: elevated buyer leverage

OEM consolidation: top 5 hold ~50%, forcing 2–4%/yr supplier cost cuts

Automotive OEMs are few and large: top five OEMs accounted for roughly 50% of global light-vehicle production in 2024, giving them strong leverage and enforcing 2–4% annual cost-downs. Dual-sourcing and strict SLAs with chargebacks keep price and service pressure high; OEM software-led integration commoditizes hardware, limiting STRATTEC margins. Aftermarket remains smaller and more price-sensitive, constrained by OEM immobilizer controls.

| Metric (2024) | Value |

|---|---|

| Top-5 OEM share | ~50% |

| Typical OEM cost-downs | 2–4%/yr |

Full Version Awaits

STRATTEC Porter's Five Forces Analysis

This preview shows the exact STRATTEC Porter’s Five Forces Analysis you’ll receive—no placeholders, no samples. The document displayed is the full, professionally formatted analysis ready for immediate download upon purchase. You’re viewing the final deliverable, identical to the file you’ll get. Use it instantly for due diligence, strategy, or reporting.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

STRATTEC’s Porter's Five Forces snapshot highlights intense supplier negotiation for specialized components, moderate buyer power from OEMs, low threat of substitutes, and concentrated rivalry driven by scale and technology. Emerging entrants face high barriers due to certifications and capital needs. This preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Specialized materials and electronics

STRATTEC relies on proprietary alloys, precision stampings, micro-motors and semiconductors for mechatronic locks, and limited qualified sources for safety-critical parts concentrates supplier power. With the global semiconductor market about $600B in 2024 and wafer fab utilization near 90%, allocation often favors larger OEMs, raising costs and lead times (often 12–20+ weeks). Qualification cycles of 6–12 months impede rapid re-sourcing, sustaining supplier leverage.

High switching costs and tooling

Custom dies, molds and PPAP-qualified parts tie programs to specific suppliers; automotive tooling often costs $250k–$2M and PPAP/OEM validation typically takes 30–90 days, so changing vendors risks months-long delays, scrap and reapproval. Tooling amortization terms of 3–7 years commonly lock pricing and raise supplier bargaining power during renegotiations.

Quality and compliance constraints

IATF 16949, end-to-end traceability and strict safety standards shrink the supplier pool for STRATTEC, as only certified firms can support automotive PPAP, cybersecurity for electronics and ISO 26262 functional safety requirements. Non-conformances risk heavy penalties and production line-stops that cost OEMs thousands of dollars per minute, elevating operational exposure. This compliance scarcity strengthens incumbent, certified suppliers and raises switching costs.

Logistics and geopolitical exposure

Global supply chains for resins, metals and semiconductors face freight volatility, tariffs and regional disruptions that raised supplier leverage; spot freight and component surcharges pushed input costs higher, with suppliers passing through surcharges of roughly 8–12% in 2024, cyclically strengthening their bargaining position for firms like STRATTEC.

- Freight & surcharges: ~8–12% in 2024

- Nearshoring: reduces but not eliminates concentrated upstream capacity

- Geopolitical risk: elevates supplier pass-through power

Countervailing buyer volume leverage

Large OEM volumes in 2024 drive flow-down terms that temper supplier power; STRATTEC aggregates demand across platforms to secure better pricing and contract terms. Dual-qualifying key inputs mitigates single-source risk, but dual-sourcing complex locking systems increases cost and lengthens qualification timelines.

- OEM flow-downs reduce supplier margins

- Aggregated demand boosts negotiating leverage

- Dual-qualification lowers single-source risk

- Dual-sourcing raises cost and slows delivery

Chip supply strain: lead times 12–20+ wks, fabs ~90%

STRATTEC depends on proprietary materials and limited certified suppliers; global semiconductors ~$600B in 2024 and wafer fab utilization ~90% drive 12–20+ week lead times. Tooling ($250k–$2M) and qualification (6–12 months; PPAP 30–90 days) lock-in suppliers. Compliance and freight surcharges (~8–12% in 2024) increase supplier leverage, while OEM flow-downs and demand aggregation partially counterbalance.

| Metric | 2024 / Value |

|---|---|

| Semiconductor market | $600B |

| Wafer fab utilization | ~90% |

| Lead times | 12–20+ weeks |

| Tooling cost | $250k–$2M |

| Qualification | 6–12 months |

| Surcharges | 8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for STRATTEC, uncovering key drivers of competition, supplier and buyer influence, and barriers protecting incumbents. Identifies disruptive threats, substitutes, and market entry risks with strategic commentary for investor and strategic use.

A clear, one-sheet summary of STRATTEC's five forces—ideal for quick strategic decisions, investor briefs, and boardroom slides to relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated OEM customer base

Automotive OEMs are few, large and price-aggressive, with the top five OEMs accounting for roughly 50% of global light-vehicle production in 2024, giving them strong leverage over suppliers. They run competitive bids and enforce annual cost-downs typically of 2–4%, making program wins critical and increasing supplier dependence on each award. OEMs can also shape specifications to favor alternate suppliers, raising switching risk for STRATTEC.

High switching costs but dual-sourcing

While re-qualification for locks and latches is costly, OEMs routinely dual-source critical components, keeping price and service under constant pressure; performance scorecards directly influence future nominations. STRATTEC must continuously defend share through competitive pricing, quality and on-time delivery. Dual-sourcing preserves OEM leverage, forcing ongoing investment to retain business.

Long contracts with stringent SLAs

Long, multi-year platform contracts embed PPAP, warranty obligations and delivery-penalty clauses that lock suppliers into strict SLAs; buyers demand on-time delivery and zero-defect targets enforced through formal scorecards. Any lapse triggers chargebacks and jeopardizes future allocations, turning operational performance directly into economic risk; SLAs thus codify buyer bargaining power into measurable cash-flow consequences.

Design influence and integration

Access systems increasingly integrate with BCMs, cybersecurity stacks and vehicle architecture, and OEM engineering choices in 2024 continue to shift value from hardware to software, commoditizing locks and keys; early design-in still locks STRATTEC in but exposes it to OEM design dictates and cost pressures as buyers leverage integration to push prices down.

- Design-in locks position but limits margins

- Software value shift risks hardware commoditization

- OEM integration gives buyers leverage to reduce costs

Aftermarket offers limited counterbalance

Aftermarket sales diversify STRATTEC revenue but remain smaller and more price-sensitive than OE channels; independent parts buyers often prioritize cost over brand. OEM key-coding and immobilizer technology restrict independent replacement and require dealer or authorized programming, narrowing non-OE alternatives. This constraint limits STRATTEC pricing power outside original equipment channels and keeps buyer power elevated.

- Aftermarket: smaller, price-sensitive

- OEM immobilizers: restrict independent replacement

- Limits non-OE pricing power

- Net: elevated buyer leverage

OEM consolidation: top 5 hold ~50%, forcing 2–4%/yr supplier cost cuts

Automotive OEMs are few and large: top five OEMs accounted for roughly 50% of global light-vehicle production in 2024, giving them strong leverage and enforcing 2–4% annual cost-downs. Dual-sourcing and strict SLAs with chargebacks keep price and service pressure high; OEM software-led integration commoditizes hardware, limiting STRATTEC margins. Aftermarket remains smaller and more price-sensitive, constrained by OEM immobilizer controls.

| Metric (2024) | Value |

|---|---|

| Top-5 OEM share | ~50% |

| Typical OEM cost-downs | 2–4%/yr |

Full Version Awaits

STRATTEC Porter's Five Forces Analysis

This preview shows the exact STRATTEC Porter’s Five Forces Analysis you’ll receive—no placeholders, no samples. The document displayed is the full, professionally formatted analysis ready for immediate download upon purchase. You’re viewing the final deliverable, identical to the file you’ll get. Use it instantly for due diligence, strategy, or reporting.