Strauss Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Strauss’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barrier strength, and substitute threats shaping its margins and growth prospects. This concise view surfaces key pressures but omits granular metrics, trend drivers, and force-by-force ratings. Unlock the full analysis for data-driven insights, visuals, and strategic recommendations to inform investment or corporate strategy.

Suppliers Bargaining Power

Diverse raw inputs

Strauss sources dairy, coffee beans, cocoa, oils, sugar, pulses and packaging from multiple regions, which reduces dependence on any single supplier and limits individual leverage. This geographic and category diversification lowers aggregate supplier power but raises procurement and quality-control complexity. Tightness in specialty coffee or high-grade dairy markets can still concentrate power, while long-term supply agreements and joint programs mitigate price and availability volatility.

Commodity volatility

Coffee, dairy and edible oils face weather, geopolitics and FX swings that amplify supplier leverage; Brazil supplies ~35% of coffee, New Zealand ~30% of dairy exports and Indonesia ~58% of palm oil exports, concentrating risk. Hedging and multi-sourcing dampen but don’t erase spikes, and suppliers often push pass-through pricing. Strauss must trade cost stability against strict quality specs.

Quality and certification

Requirements for sustainability, traceability and food safety—certified coffee and audited dairies—shrink the qualified supplier pool; certified coffee represents roughly 25% of global volumes, raising supplier leverage where compliant capacity is limited.

Premium inputs for innovation-driven SKUs concentrate power further as demand for specialty Arabica and branded dairy rises, pushing suppliers to command price premiums.

Long-term strategic partnerships and multi-year contracts are therefore essential to secure compliant supply and cap supplier influence.

Switching costs

Reformulating dairy, coffee blends, or dips to new suppliers risks altering taste, texture, and brand equity, while qualification, trials, and regulatory approvals lengthen and raise switching costs. This stickiness increases entrenched supplier leverage, raising negotiation power and potential price pass-through. Implementing dual-sourcing strategies preserves optionality and reduces single-supplier risk.

- Reformulation risk

- Approval & trials raise costs

- Supplier stickiness = leverage

- Dual-sourcing preserves optionality

Packaging and logistics

Specialized packaging (barrier films, capsules) and cold-chain logistics create chokepoints for Strauss, with the global flexible packaging market ~USD 200B and cold-chain logistics ~USD 220B in 2024, concentrating bargaining power among converters and 3PLs. Limited converter or 3PL capacity during peak seasons pushes spot premiums and tighter lead times, strengthening supplier terms. Localizing suppliers reduces exposure but requires scale to stay cost-competitive, while collaborative design with converters can lower dependency and unit costs.

- Chokepoints: barrier films, cold chain

- 2024 markets: flexible packaging ~USD 200B; cold chain ~USD 220B

- Peak demand: limited 3PL/converter capacity raises supplier leverage

- Mitigants: localization needs scale; co-design lowers dependency

Diversified sourcing lowers supplier power; concentrated commodities, weather and FX heighten spikes

Strauss’ multi‑regional sourcing lowers overall supplier leverage, but specialty coffee/dairy, palm oil concentration and certified-supplier limits raise bargaining power; weather, geopolitics and FX amplify spikes. Long‑term contracts, hedging, dual‑sourcing and co‑design mitigate but don’t eliminate switching costs and quality risk.

| Input | 2024 stat | Impact |

|---|---|---|

| Coffee | Brazil ~35% exports | High concentration |

| Dairy | NZ ~30% exports | Quality tightness |

| Palm oil | Indonesia ~58% exports | Supply risk |

| Certified coffee | ~25% global vol. | Limited suppliers |

| Packaging/cold chain | $200B/$220B | Chokepoints |

What is included in the product

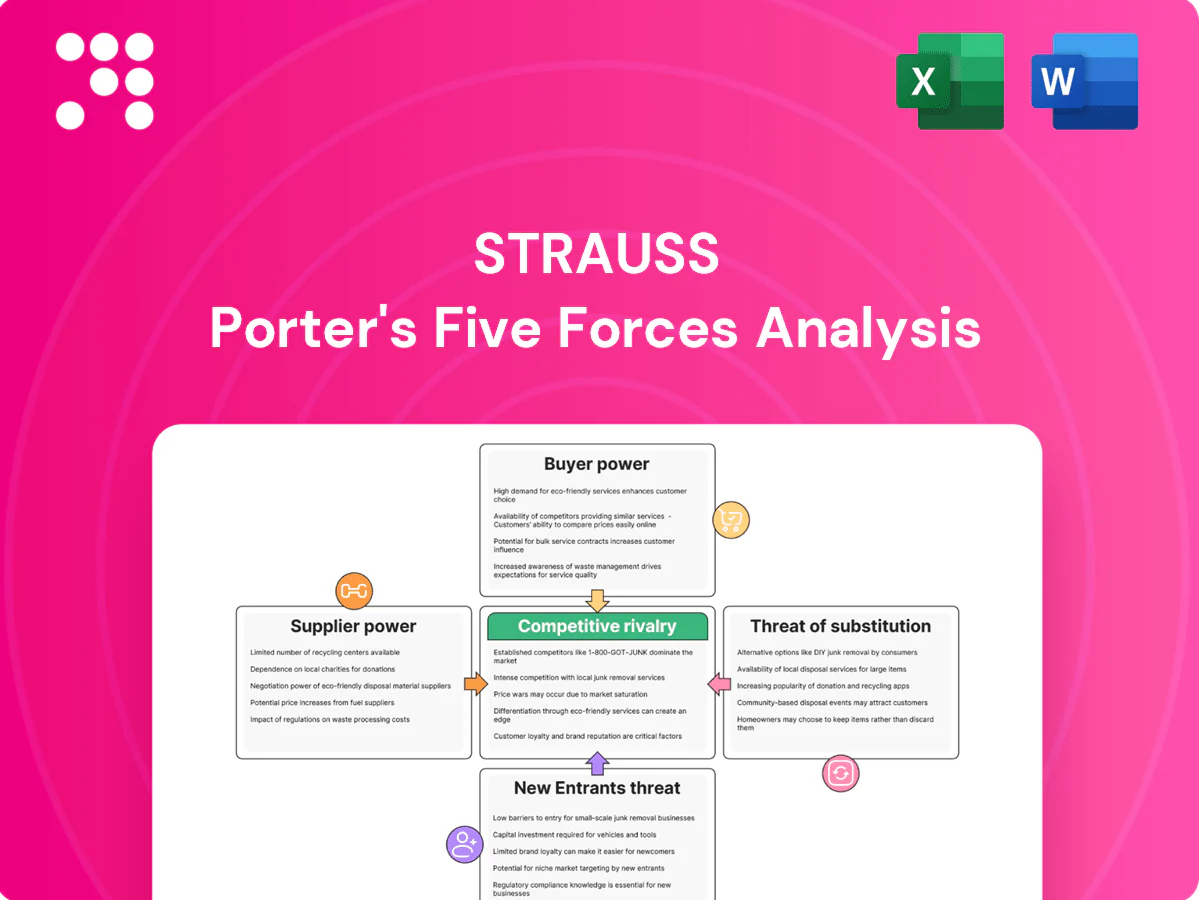

Porter’s Five Forces analysis for Strauss examines rivalry, buyer and supplier bargaining power, and threats from new entrants and substitutes, identifying strategic levers and vulnerabilities; it combines industry data with actionable insights to guide pricing, entry barriers, and defensive tactics.

Quickly pinpoint competitive pain points with Strauss Porter's Five Forces summary—customize force intensities, swap in your data, and export clean visuals for decks or dashboards to speed strategic decisions.

Customers Bargaining Power

Concentrated retail

Concentrated retail means large chains control shelf space, promo calendars and slotting fees (typically $25k–$250k per SKU in major markets), increasing price pressure and demands for trade terms. Strauss, with 2024 revenue ~NIS 8.0bn, must deliver velocity and category growth to retain facings. Joint business plans and shared KPIs can align incentives and protect shelf presence.

Private label pressure

Retailers’ push into private labels—UK grocery private-label penetration exceeded 50% in 2024—expands cheaper dairy, snacks and spreads, raising buyer leverage and compressing industry margins for suppliers like Strauss. To counteract margin pressure, Strauss must prioritize differentiation via premium quality, wellness positioning and strong brands, while maintaining a rapid innovation cadence to defend share and justify price premiums.

Elasticity and health

Consumers remain price-sensitive for staples but exhibit double-digit willingness-to-pay premiums for healthful, functional or indulgent SKUs, with 2024 NielsenIQ data showing health-focused SKUs growing faster than core staples. Health and clean-label shifts changed portfolio mix and raised elasticity for basic lines while lowering it for premium health offers. Strauss can segment pricing and pack sizes and use transparent labeling to build trust and capture premium margins.

Multi-channel shift

The multi-channel shift—e-commerce now 22% of global retail sales in 2024—plus quick commerce (orders +35% YoY in 2024) and HoReCa diversify buyers but strengthen platforms that control data and reach; algorithmic shelves prioritize price, ratings and availability, squeezing branded visibility. Strauss must upgrade digital merchandising and fulfillment; D2C can capture richer insight and ~10–15% higher margins.

- e-commerce 22% (2024)

- quick-commerce orders +35% YoY (2024)

- algorithmic bias: price, ratings, availability

- D2C potential: +10–15% margin

Switching ease

Category alternatives are abundant on shelves, making brand switching easy; private-label penetration reached around 18% in many developed markets in 2024, increasing retailer leverage. Promotions and coupons can tilt decisions rapidly, with weekly promotions driving short-term volume spikes. Loyalty programs and distinctive taste profiles reduce churn, while consistent quality anchors repeat purchase for Strauss brands.

- High alternatives — private-label ~18% (2024)

- Promotions drive short-term shifts

- Loyalty and taste lower churn

- Consistent quality sustains repeats

Retail consolidation and private-label squeeze margins; health SKUs and D2C unlock premium gains

Retail consolidation and private-label (≈18% penetration) give buyers strong leverage versus Strauss (2024 rev ~NIS 8.0bn), forcing trade terms and slotting fees. Health-forward SKUs show faster growth, enabling premium pricing while staples remain price-sensitive. Digital channels (e‑commerce 22%, quick‑commerce +35% YoY) shift power to platforms; D2C can recover ~10–15% margin.

| Metric | 2024 | Implication |

|---|---|---|

| Revenue | NIS 8.0bn | Scale to fund slotting/promos |

| E‑commerce | 22% | Platform leverage |

| Private‑label | 18% | Margin pressure |

| D2C margin lift | +10–15% | Value capture |

Preview the Actual Deliverable

Strauss Porter's Five Forces Analysis

Strauss Porter’s Five Forces analysis evaluates industry rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry to reveal competitive strength and profit potential. This preview is the exact document you'll receive upon purchase—fully formatted and ready to download. No placeholders, no edits needed. Use it straightaway for decision-making or reporting.

Don't Miss the Bigger Picture

Strauss’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barrier strength, and substitute threats shaping its margins and growth prospects. This concise view surfaces key pressures but omits granular metrics, trend drivers, and force-by-force ratings. Unlock the full analysis for data-driven insights, visuals, and strategic recommendations to inform investment or corporate strategy.

Suppliers Bargaining Power

Diverse raw inputs

Strauss sources dairy, coffee beans, cocoa, oils, sugar, pulses and packaging from multiple regions, which reduces dependence on any single supplier and limits individual leverage. This geographic and category diversification lowers aggregate supplier power but raises procurement and quality-control complexity. Tightness in specialty coffee or high-grade dairy markets can still concentrate power, while long-term supply agreements and joint programs mitigate price and availability volatility.

Commodity volatility

Coffee, dairy and edible oils face weather, geopolitics and FX swings that amplify supplier leverage; Brazil supplies ~35% of coffee, New Zealand ~30% of dairy exports and Indonesia ~58% of palm oil exports, concentrating risk. Hedging and multi-sourcing dampen but don’t erase spikes, and suppliers often push pass-through pricing. Strauss must trade cost stability against strict quality specs.

Quality and certification

Requirements for sustainability, traceability and food safety—certified coffee and audited dairies—shrink the qualified supplier pool; certified coffee represents roughly 25% of global volumes, raising supplier leverage where compliant capacity is limited.

Premium inputs for innovation-driven SKUs concentrate power further as demand for specialty Arabica and branded dairy rises, pushing suppliers to command price premiums.

Long-term strategic partnerships and multi-year contracts are therefore essential to secure compliant supply and cap supplier influence.

Switching costs

Reformulating dairy, coffee blends, or dips to new suppliers risks altering taste, texture, and brand equity, while qualification, trials, and regulatory approvals lengthen and raise switching costs. This stickiness increases entrenched supplier leverage, raising negotiation power and potential price pass-through. Implementing dual-sourcing strategies preserves optionality and reduces single-supplier risk.

- Reformulation risk

- Approval & trials raise costs

- Supplier stickiness = leverage

- Dual-sourcing preserves optionality

Packaging and logistics

Specialized packaging (barrier films, capsules) and cold-chain logistics create chokepoints for Strauss, with the global flexible packaging market ~USD 200B and cold-chain logistics ~USD 220B in 2024, concentrating bargaining power among converters and 3PLs. Limited converter or 3PL capacity during peak seasons pushes spot premiums and tighter lead times, strengthening supplier terms. Localizing suppliers reduces exposure but requires scale to stay cost-competitive, while collaborative design with converters can lower dependency and unit costs.

- Chokepoints: barrier films, cold chain

- 2024 markets: flexible packaging ~USD 200B; cold chain ~USD 220B

- Peak demand: limited 3PL/converter capacity raises supplier leverage

- Mitigants: localization needs scale; co-design lowers dependency

Diversified sourcing lowers supplier power; concentrated commodities, weather and FX heighten spikes

Strauss’ multi‑regional sourcing lowers overall supplier leverage, but specialty coffee/dairy, palm oil concentration and certified-supplier limits raise bargaining power; weather, geopolitics and FX amplify spikes. Long‑term contracts, hedging, dual‑sourcing and co‑design mitigate but don’t eliminate switching costs and quality risk.

| Input | 2024 stat | Impact |

|---|---|---|

| Coffee | Brazil ~35% exports | High concentration |

| Dairy | NZ ~30% exports | Quality tightness |

| Palm oil | Indonesia ~58% exports | Supply risk |

| Certified coffee | ~25% global vol. | Limited suppliers |

| Packaging/cold chain | $200B/$220B | Chokepoints |

What is included in the product

Porter’s Five Forces analysis for Strauss examines rivalry, buyer and supplier bargaining power, and threats from new entrants and substitutes, identifying strategic levers and vulnerabilities; it combines industry data with actionable insights to guide pricing, entry barriers, and defensive tactics.

Quickly pinpoint competitive pain points with Strauss Porter's Five Forces summary—customize force intensities, swap in your data, and export clean visuals for decks or dashboards to speed strategic decisions.

Customers Bargaining Power

Concentrated retail

Concentrated retail means large chains control shelf space, promo calendars and slotting fees (typically $25k–$250k per SKU in major markets), increasing price pressure and demands for trade terms. Strauss, with 2024 revenue ~NIS 8.0bn, must deliver velocity and category growth to retain facings. Joint business plans and shared KPIs can align incentives and protect shelf presence.

Private label pressure

Retailers’ push into private labels—UK grocery private-label penetration exceeded 50% in 2024—expands cheaper dairy, snacks and spreads, raising buyer leverage and compressing industry margins for suppliers like Strauss. To counteract margin pressure, Strauss must prioritize differentiation via premium quality, wellness positioning and strong brands, while maintaining a rapid innovation cadence to defend share and justify price premiums.

Elasticity and health

Consumers remain price-sensitive for staples but exhibit double-digit willingness-to-pay premiums for healthful, functional or indulgent SKUs, with 2024 NielsenIQ data showing health-focused SKUs growing faster than core staples. Health and clean-label shifts changed portfolio mix and raised elasticity for basic lines while lowering it for premium health offers. Strauss can segment pricing and pack sizes and use transparent labeling to build trust and capture premium margins.

Multi-channel shift

The multi-channel shift—e-commerce now 22% of global retail sales in 2024—plus quick commerce (orders +35% YoY in 2024) and HoReCa diversify buyers but strengthen platforms that control data and reach; algorithmic shelves prioritize price, ratings and availability, squeezing branded visibility. Strauss must upgrade digital merchandising and fulfillment; D2C can capture richer insight and ~10–15% higher margins.

- e-commerce 22% (2024)

- quick-commerce orders +35% YoY (2024)

- algorithmic bias: price, ratings, availability

- D2C potential: +10–15% margin

Switching ease

Category alternatives are abundant on shelves, making brand switching easy; private-label penetration reached around 18% in many developed markets in 2024, increasing retailer leverage. Promotions and coupons can tilt decisions rapidly, with weekly promotions driving short-term volume spikes. Loyalty programs and distinctive taste profiles reduce churn, while consistent quality anchors repeat purchase for Strauss brands.

- High alternatives — private-label ~18% (2024)

- Promotions drive short-term shifts

- Loyalty and taste lower churn

- Consistent quality sustains repeats

Retail consolidation and private-label squeeze margins; health SKUs and D2C unlock premium gains

Retail consolidation and private-label (≈18% penetration) give buyers strong leverage versus Strauss (2024 rev ~NIS 8.0bn), forcing trade terms and slotting fees. Health-forward SKUs show faster growth, enabling premium pricing while staples remain price-sensitive. Digital channels (e‑commerce 22%, quick‑commerce +35% YoY) shift power to platforms; D2C can recover ~10–15% margin.

| Metric | 2024 | Implication |

|---|---|---|

| Revenue | NIS 8.0bn | Scale to fund slotting/promos |

| E‑commerce | 22% | Platform leverage |

| Private‑label | 18% | Margin pressure |

| D2C margin lift | +10–15% | Value capture |

Preview the Actual Deliverable

Strauss Porter's Five Forces Analysis

Strauss Porter’s Five Forces analysis evaluates industry rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry to reveal competitive strength and profit potential. This preview is the exact document you'll receive upon purchase—fully formatted and ready to download. No placeholders, no edits needed. Use it straightaway for decision-making or reporting.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Strauss’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barrier strength, and substitute threats shaping its margins and growth prospects. This concise view surfaces key pressures but omits granular metrics, trend drivers, and force-by-force ratings. Unlock the full analysis for data-driven insights, visuals, and strategic recommendations to inform investment or corporate strategy.

Suppliers Bargaining Power

Diverse raw inputs

Strauss sources dairy, coffee beans, cocoa, oils, sugar, pulses and packaging from multiple regions, which reduces dependence on any single supplier and limits individual leverage. This geographic and category diversification lowers aggregate supplier power but raises procurement and quality-control complexity. Tightness in specialty coffee or high-grade dairy markets can still concentrate power, while long-term supply agreements and joint programs mitigate price and availability volatility.

Commodity volatility

Coffee, dairy and edible oils face weather, geopolitics and FX swings that amplify supplier leverage; Brazil supplies ~35% of coffee, New Zealand ~30% of dairy exports and Indonesia ~58% of palm oil exports, concentrating risk. Hedging and multi-sourcing dampen but don’t erase spikes, and suppliers often push pass-through pricing. Strauss must trade cost stability against strict quality specs.

Quality and certification

Requirements for sustainability, traceability and food safety—certified coffee and audited dairies—shrink the qualified supplier pool; certified coffee represents roughly 25% of global volumes, raising supplier leverage where compliant capacity is limited.

Premium inputs for innovation-driven SKUs concentrate power further as demand for specialty Arabica and branded dairy rises, pushing suppliers to command price premiums.

Long-term strategic partnerships and multi-year contracts are therefore essential to secure compliant supply and cap supplier influence.

Switching costs

Reformulating dairy, coffee blends, or dips to new suppliers risks altering taste, texture, and brand equity, while qualification, trials, and regulatory approvals lengthen and raise switching costs. This stickiness increases entrenched supplier leverage, raising negotiation power and potential price pass-through. Implementing dual-sourcing strategies preserves optionality and reduces single-supplier risk.

- Reformulation risk

- Approval & trials raise costs

- Supplier stickiness = leverage

- Dual-sourcing preserves optionality

Packaging and logistics

Specialized packaging (barrier films, capsules) and cold-chain logistics create chokepoints for Strauss, with the global flexible packaging market ~USD 200B and cold-chain logistics ~USD 220B in 2024, concentrating bargaining power among converters and 3PLs. Limited converter or 3PL capacity during peak seasons pushes spot premiums and tighter lead times, strengthening supplier terms. Localizing suppliers reduces exposure but requires scale to stay cost-competitive, while collaborative design with converters can lower dependency and unit costs.

- Chokepoints: barrier films, cold chain

- 2024 markets: flexible packaging ~USD 200B; cold chain ~USD 220B

- Peak demand: limited 3PL/converter capacity raises supplier leverage

- Mitigants: localization needs scale; co-design lowers dependency

Diversified sourcing lowers supplier power; concentrated commodities, weather and FX heighten spikes

Strauss’ multi‑regional sourcing lowers overall supplier leverage, but specialty coffee/dairy, palm oil concentration and certified-supplier limits raise bargaining power; weather, geopolitics and FX amplify spikes. Long‑term contracts, hedging, dual‑sourcing and co‑design mitigate but don’t eliminate switching costs and quality risk.

| Input | 2024 stat | Impact |

|---|---|---|

| Coffee | Brazil ~35% exports | High concentration |

| Dairy | NZ ~30% exports | Quality tightness |

| Palm oil | Indonesia ~58% exports | Supply risk |

| Certified coffee | ~25% global vol. | Limited suppliers |

| Packaging/cold chain | $200B/$220B | Chokepoints |

What is included in the product

Porter’s Five Forces analysis for Strauss examines rivalry, buyer and supplier bargaining power, and threats from new entrants and substitutes, identifying strategic levers and vulnerabilities; it combines industry data with actionable insights to guide pricing, entry barriers, and defensive tactics.

Quickly pinpoint competitive pain points with Strauss Porter's Five Forces summary—customize force intensities, swap in your data, and export clean visuals for decks or dashboards to speed strategic decisions.

Customers Bargaining Power

Concentrated retail

Concentrated retail means large chains control shelf space, promo calendars and slotting fees (typically $25k–$250k per SKU in major markets), increasing price pressure and demands for trade terms. Strauss, with 2024 revenue ~NIS 8.0bn, must deliver velocity and category growth to retain facings. Joint business plans and shared KPIs can align incentives and protect shelf presence.

Private label pressure

Retailers’ push into private labels—UK grocery private-label penetration exceeded 50% in 2024—expands cheaper dairy, snacks and spreads, raising buyer leverage and compressing industry margins for suppliers like Strauss. To counteract margin pressure, Strauss must prioritize differentiation via premium quality, wellness positioning and strong brands, while maintaining a rapid innovation cadence to defend share and justify price premiums.

Elasticity and health

Consumers remain price-sensitive for staples but exhibit double-digit willingness-to-pay premiums for healthful, functional or indulgent SKUs, with 2024 NielsenIQ data showing health-focused SKUs growing faster than core staples. Health and clean-label shifts changed portfolio mix and raised elasticity for basic lines while lowering it for premium health offers. Strauss can segment pricing and pack sizes and use transparent labeling to build trust and capture premium margins.

Multi-channel shift

The multi-channel shift—e-commerce now 22% of global retail sales in 2024—plus quick commerce (orders +35% YoY in 2024) and HoReCa diversify buyers but strengthen platforms that control data and reach; algorithmic shelves prioritize price, ratings and availability, squeezing branded visibility. Strauss must upgrade digital merchandising and fulfillment; D2C can capture richer insight and ~10–15% higher margins.

- e-commerce 22% (2024)

- quick-commerce orders +35% YoY (2024)

- algorithmic bias: price, ratings, availability

- D2C potential: +10–15% margin

Switching ease

Category alternatives are abundant on shelves, making brand switching easy; private-label penetration reached around 18% in many developed markets in 2024, increasing retailer leverage. Promotions and coupons can tilt decisions rapidly, with weekly promotions driving short-term volume spikes. Loyalty programs and distinctive taste profiles reduce churn, while consistent quality anchors repeat purchase for Strauss brands.

- High alternatives — private-label ~18% (2024)

- Promotions drive short-term shifts

- Loyalty and taste lower churn

- Consistent quality sustains repeats

Retail consolidation and private-label squeeze margins; health SKUs and D2C unlock premium gains

Retail consolidation and private-label (≈18% penetration) give buyers strong leverage versus Strauss (2024 rev ~NIS 8.0bn), forcing trade terms and slotting fees. Health-forward SKUs show faster growth, enabling premium pricing while staples remain price-sensitive. Digital channels (e‑commerce 22%, quick‑commerce +35% YoY) shift power to platforms; D2C can recover ~10–15% margin.

| Metric | 2024 | Implication |

|---|---|---|

| Revenue | NIS 8.0bn | Scale to fund slotting/promos |

| E‑commerce | 22% | Platform leverage |

| Private‑label | 18% | Margin pressure |

| D2C margin lift | +10–15% | Value capture |

Preview the Actual Deliverable

Strauss Porter's Five Forces Analysis

Strauss Porter’s Five Forces analysis evaluates industry rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry to reveal competitive strength and profit potential. This preview is the exact document you'll receive upon purchase—fully formatted and ready to download. No placeholders, no edits needed. Use it straightaway for decision-making or reporting.