Stride Porter's Five Forces Analysis

Don't Miss the Bigger Picture

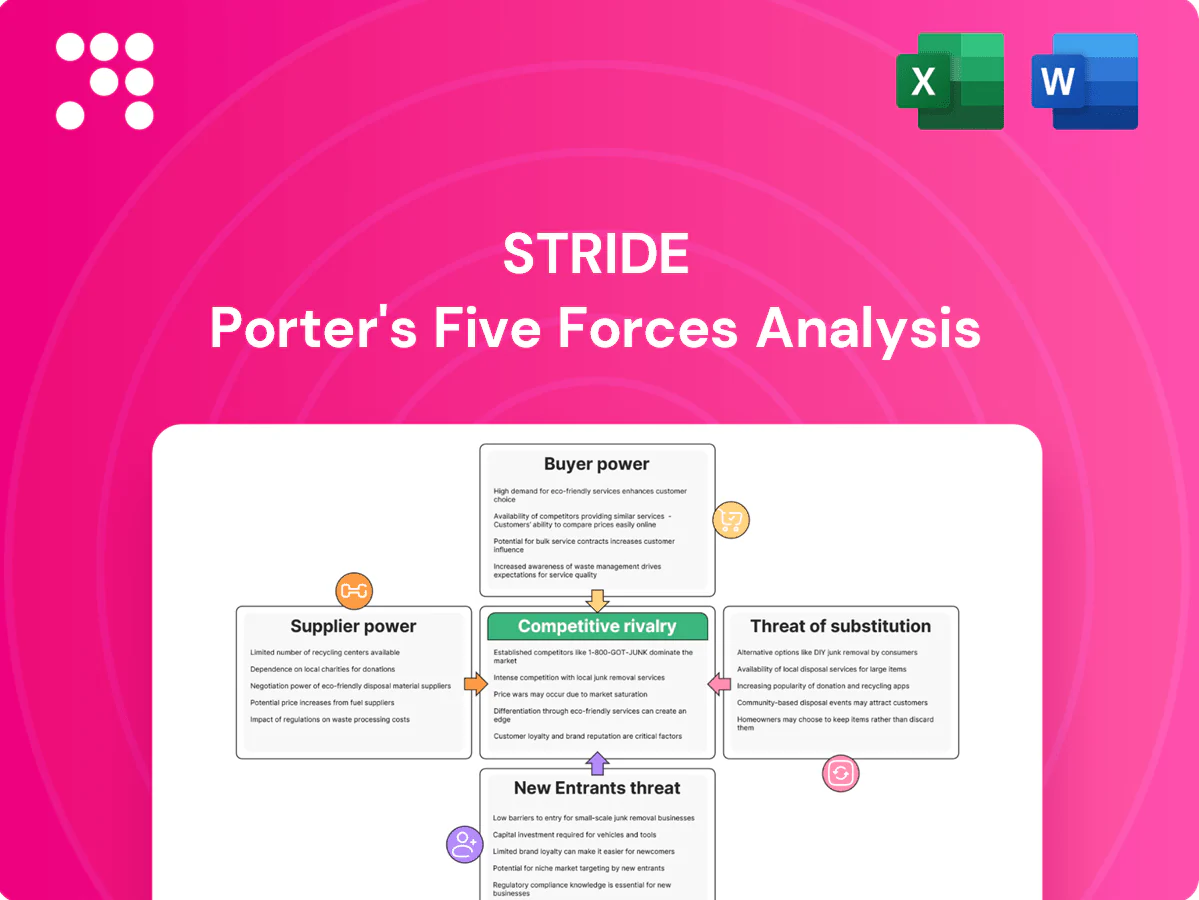

Stride’s Porter's Five Forces snapshot outlines competitive intensity across buyers, suppliers, entrants and substitutes, highlighting key market pressures and strategic levers. This brief view teases critical risks and opportunities. Unlock the full analysis for force-by-force ratings, visuals and actionable recommendations. Get the consultant-grade report to inform investment or strategy.

Suppliers Bargaining Power

Specialized content licensors

High-quality, standards-aligned digital curricula and assessments are concentrated: the top five US educational publishers hold over 60% of the market, creating licensing dependency and elevated switching costs for buyers. Licensing windows and update cycles further entrench suppliers, though Stride reduced exposure by expanding proprietary content and in 2024 reported ~1.2B in revenue, enabling multi-year bundle negotiations to cap supplier leverage.

Cloud and platform infrastructure

Hosting, video and data services are concentrated among hyperscalers (2024 market shares: AWS 32%, Microsoft 23%, Google 11% ≈66%), giving suppliers moderate bargaining power. Volume commitments and deep technical integration drive stickiness and discount leverage. Multi-cloud strategies are widespread (Flexera 2024: 92% use multi-cloud) and in-house platforms can mitigate risk. Uptime SLAs (99.95–99.99%) and FERPA/COPPA needs add negotiation chips.

Edtech tools and integrations

Edtech integrations (LMS, proctoring, analytics, accessibility) remain fragmented, with the global LMS market around USD 18B in 2024, limiting any single supplier’s power; however required certifications and critical integrations raise switching friction. API standards and modular architectures preserve buyer flexibility, though vendor consolidation in proctoring and analytics niches could increase supplier influence over time.

Teacher and specialist labor

Certified teachers, counselors, and SPED providers are strategic inputs for Stride; tight 2023–24 labor markets and licensure-driven shortages elevated supplier leverage, with over half of districts reporting staffing shortfalls and median teacher pay near $64,000 in 2024.

Remote delivery expanded recruiting pools, lowering some pressure, while investment in pipelines and retention (grow-your-own, residency programs) has begun to rebalance bargaining power.

Devices and connectivity enablers

Hardware and broadband underpin Stride’s delivery but supplier clout is muted by competitive device markets and large public programs: US E‑Rate discounts up to 90% for eligible schools and the BEAD program’s $42.5B broadband funding (2023–24) expand buyer power; bulk procurement often yields 15–30% discounts. Supply‑chain shocks have caused component price spikes near 20% and lead times stretching to ~12 weeks, making cost volatility a risk. Providing multiple device options and offline‑friendly content reduces dependence on any single supplier and eases delivery during connectivity disruptions.

- E‑Rate: up to 90% discount

- BEAD funding: $42.5B

- Bulk discounts: ~15–30%

- Price spikes in shocks: ~20%

- Lead times during stress: ~12 weeks

Top 5 publishers >60%; cloud top3 66%; BEAD $42.5B boosts broadband access

Supplier power is elevated for standards-aligned curricula (top 5 >60%) and SPED/STEM specialists, though Stride’s $1.2B 2024 scale and proprietary content reduce exposure. Hyperscalers hold ~66% cloud share (AWS 32%, MS 23%, Google 11%), giving moderate leverage mitigated by multi-cloud (92% adoption). Hardware/broadband buyer power is strengthened by E‑Rate (up to 90%) and BEAD $42.5B funding.

| Metric | 2024 Value |

|---|---|

| Stride revenue | $1.2B |

| Top5 publishers | >60% |

| Cloud share (top3) | 66% |

| LMS market | $18B |

| Median teacher pay | $64k |

| BEAD | $42.5B |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Stride, uncovering competitive drivers, buyer and supplier power, substitutes, and entry threats with strategic commentary. Fully editable for reports, investor decks, or academic use to pinpoint disruptive risks and defendable advantages.

Stride Porter's Five Forces delivers a one-sheet, customizable summary with radar visualization and slide-ready layout—ideal for quick decisions, scenario duplication, easy data swaps, and seamless integration into dashboards without macros, so non-technical teams can assess competitive pressure fast.

Customers Bargaining Power

Districts and public schools

Districts and public schools control roughly $830 billion in annual K-12 spending (2024 est.), using formal RFPs and large contracts that give them strong bargaining power to demand customization, compliance, and outcomes reporting. Contracts commonly span 3–5 years, creating high switching costs as vendors integrate systems. State funding volatility (often ±3–7% year-to-year in some states) intensifies price pressure.

State virtual programs

Concentrated buyers—state education agencies and large districts—wield scale to dictate standards and pricing, leveraging national average per-pupil spending near $15,000 to benchmark contracts. Competitive bids force head-to-head comparisons on per-pupil rates and performance metrics. Contract renewal depends on regulatory alignment and demonstrable student outcomes. High visibility and political oversight raise stakes in negotiations.

Private schools and networks

Private schools and networks prioritize differentiation and flexibility, which reduces pure price sensitivity; the global EdTech market was estimated at about $286 billion in 2024, underscoring investment capacity. They still comparison-shop across platforms and content providers, but deep integration and teacher enablement create high switching costs and lock-in. Tiered bundles and white-label options help defend margins and capture higher ARPU.

Parents and learners

Parents and learners are fragmented but highly discerning, prioritizing experience and measurable outcomes; their bargaining power rises as switching between accredited online programs is feasible when records and credits transfer.

Reviews, NPS, community reputation drive churn, while scholarships and financing reduce price resistance.

- Fragmented buyers

- Low switching friction

- Reputation-driven churn

- Subsidies soften pricing

Employer and adult-learning clients

Corporate buyers demand job-aligned outcomes and measurable ROI, driving Stride Porter to offer outcome metrics as standard; global corporate training spend exceeded 400 billion USD in 2024, amplifying buyer scrutiny. Cohort-scale purchasing for enterprise cohorts (often hundreds of seats) increases negotiating leverage and pushes performance-based pricing and co-design. Stackable credentials and placement support lower churn by improving demonstrable career outcomes.

- Buyer focus: measurable ROI, job-aligned outcomes

- Cohort leverage: enterprise buys amplify negotiation power

- Pricing: performance-based and co-design align incentives

- Retention: stackable credentials + placement reduce churn

BuyersK12 $830B, EdTech $286B, Corp$400B

Buyers hold high bargaining power: K-12 districts control ~$830B (2024) and use RFPs and multi-year contracts to enforce price, customization, and outcomes. Per-pupil benchmarks near $15,000 drive competitive bids; EdTech market ~$286B and corporate training ~$400B (2024) raise buyer leverage. Fragmented parents/learners increase churn via reviews and transferability, while private networks accept premium for integration and outcomes.

| Buyer Segment | 2024 Spend | Leverage | Key Demand |

|---|---|---|---|

| K-12 districts | $830B | High | Compliance, outcomes, low price |

| Private/networks | — (part of $286B) | Medium | Differentiation, integration |

| Parents/learners | — | Low–Medium | Experience, transferability |

| Corporate | $400B | High | Job-aligned ROI |

Preview Before You Purchase

Stride Porter's Five Forces Analysis

This preview shows the exact Stride Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, placeholders, or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the final deliverable and will have instant access to this same document upon payment.

Don't Miss the Bigger Picture

Stride’s Porter's Five Forces snapshot outlines competitive intensity across buyers, suppliers, entrants and substitutes, highlighting key market pressures and strategic levers. This brief view teases critical risks and opportunities. Unlock the full analysis for force-by-force ratings, visuals and actionable recommendations. Get the consultant-grade report to inform investment or strategy.

Suppliers Bargaining Power

Specialized content licensors

High-quality, standards-aligned digital curricula and assessments are concentrated: the top five US educational publishers hold over 60% of the market, creating licensing dependency and elevated switching costs for buyers. Licensing windows and update cycles further entrench suppliers, though Stride reduced exposure by expanding proprietary content and in 2024 reported ~1.2B in revenue, enabling multi-year bundle negotiations to cap supplier leverage.

Cloud and platform infrastructure

Hosting, video and data services are concentrated among hyperscalers (2024 market shares: AWS 32%, Microsoft 23%, Google 11% ≈66%), giving suppliers moderate bargaining power. Volume commitments and deep technical integration drive stickiness and discount leverage. Multi-cloud strategies are widespread (Flexera 2024: 92% use multi-cloud) and in-house platforms can mitigate risk. Uptime SLAs (99.95–99.99%) and FERPA/COPPA needs add negotiation chips.

Edtech tools and integrations

Edtech integrations (LMS, proctoring, analytics, accessibility) remain fragmented, with the global LMS market around USD 18B in 2024, limiting any single supplier’s power; however required certifications and critical integrations raise switching friction. API standards and modular architectures preserve buyer flexibility, though vendor consolidation in proctoring and analytics niches could increase supplier influence over time.

Teacher and specialist labor

Certified teachers, counselors, and SPED providers are strategic inputs for Stride; tight 2023–24 labor markets and licensure-driven shortages elevated supplier leverage, with over half of districts reporting staffing shortfalls and median teacher pay near $64,000 in 2024.

Remote delivery expanded recruiting pools, lowering some pressure, while investment in pipelines and retention (grow-your-own, residency programs) has begun to rebalance bargaining power.

Devices and connectivity enablers

Hardware and broadband underpin Stride’s delivery but supplier clout is muted by competitive device markets and large public programs: US E‑Rate discounts up to 90% for eligible schools and the BEAD program’s $42.5B broadband funding (2023–24) expand buyer power; bulk procurement often yields 15–30% discounts. Supply‑chain shocks have caused component price spikes near 20% and lead times stretching to ~12 weeks, making cost volatility a risk. Providing multiple device options and offline‑friendly content reduces dependence on any single supplier and eases delivery during connectivity disruptions.

- E‑Rate: up to 90% discount

- BEAD funding: $42.5B

- Bulk discounts: ~15–30%

- Price spikes in shocks: ~20%

- Lead times during stress: ~12 weeks

Top 5 publishers >60%; cloud top3 66%; BEAD $42.5B boosts broadband access

Supplier power is elevated for standards-aligned curricula (top 5 >60%) and SPED/STEM specialists, though Stride’s $1.2B 2024 scale and proprietary content reduce exposure. Hyperscalers hold ~66% cloud share (AWS 32%, MS 23%, Google 11%), giving moderate leverage mitigated by multi-cloud (92% adoption). Hardware/broadband buyer power is strengthened by E‑Rate (up to 90%) and BEAD $42.5B funding.

| Metric | 2024 Value |

|---|---|

| Stride revenue | $1.2B |

| Top5 publishers | >60% |

| Cloud share (top3) | 66% |

| LMS market | $18B |

| Median teacher pay | $64k |

| BEAD | $42.5B |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Stride, uncovering competitive drivers, buyer and supplier power, substitutes, and entry threats with strategic commentary. Fully editable for reports, investor decks, or academic use to pinpoint disruptive risks and defendable advantages.

Stride Porter's Five Forces delivers a one-sheet, customizable summary with radar visualization and slide-ready layout—ideal for quick decisions, scenario duplication, easy data swaps, and seamless integration into dashboards without macros, so non-technical teams can assess competitive pressure fast.

Customers Bargaining Power

Districts and public schools

Districts and public schools control roughly $830 billion in annual K-12 spending (2024 est.), using formal RFPs and large contracts that give them strong bargaining power to demand customization, compliance, and outcomes reporting. Contracts commonly span 3–5 years, creating high switching costs as vendors integrate systems. State funding volatility (often ±3–7% year-to-year in some states) intensifies price pressure.

State virtual programs

Concentrated buyers—state education agencies and large districts—wield scale to dictate standards and pricing, leveraging national average per-pupil spending near $15,000 to benchmark contracts. Competitive bids force head-to-head comparisons on per-pupil rates and performance metrics. Contract renewal depends on regulatory alignment and demonstrable student outcomes. High visibility and political oversight raise stakes in negotiations.

Private schools and networks

Private schools and networks prioritize differentiation and flexibility, which reduces pure price sensitivity; the global EdTech market was estimated at about $286 billion in 2024, underscoring investment capacity. They still comparison-shop across platforms and content providers, but deep integration and teacher enablement create high switching costs and lock-in. Tiered bundles and white-label options help defend margins and capture higher ARPU.

Parents and learners

Parents and learners are fragmented but highly discerning, prioritizing experience and measurable outcomes; their bargaining power rises as switching between accredited online programs is feasible when records and credits transfer.

Reviews, NPS, community reputation drive churn, while scholarships and financing reduce price resistance.

- Fragmented buyers

- Low switching friction

- Reputation-driven churn

- Subsidies soften pricing

Employer and adult-learning clients

Corporate buyers demand job-aligned outcomes and measurable ROI, driving Stride Porter to offer outcome metrics as standard; global corporate training spend exceeded 400 billion USD in 2024, amplifying buyer scrutiny. Cohort-scale purchasing for enterprise cohorts (often hundreds of seats) increases negotiating leverage and pushes performance-based pricing and co-design. Stackable credentials and placement support lower churn by improving demonstrable career outcomes.

- Buyer focus: measurable ROI, job-aligned outcomes

- Cohort leverage: enterprise buys amplify negotiation power

- Pricing: performance-based and co-design align incentives

- Retention: stackable credentials + placement reduce churn

BuyersK12 $830B, EdTech $286B, Corp$400B

Buyers hold high bargaining power: K-12 districts control ~$830B (2024) and use RFPs and multi-year contracts to enforce price, customization, and outcomes. Per-pupil benchmarks near $15,000 drive competitive bids; EdTech market ~$286B and corporate training ~$400B (2024) raise buyer leverage. Fragmented parents/learners increase churn via reviews and transferability, while private networks accept premium for integration and outcomes.

| Buyer Segment | 2024 Spend | Leverage | Key Demand |

|---|---|---|---|

| K-12 districts | $830B | High | Compliance, outcomes, low price |

| Private/networks | — (part of $286B) | Medium | Differentiation, integration |

| Parents/learners | — | Low–Medium | Experience, transferability |

| Corporate | $400B | High | Job-aligned ROI |

Preview Before You Purchase

Stride Porter's Five Forces Analysis

This preview shows the exact Stride Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, placeholders, or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the final deliverable and will have instant access to this same document upon payment.

Description

Don't Miss the Bigger Picture

Stride’s Porter's Five Forces snapshot outlines competitive intensity across buyers, suppliers, entrants and substitutes, highlighting key market pressures and strategic levers. This brief view teases critical risks and opportunities. Unlock the full analysis for force-by-force ratings, visuals and actionable recommendations. Get the consultant-grade report to inform investment or strategy.

Suppliers Bargaining Power

Specialized content licensors

High-quality, standards-aligned digital curricula and assessments are concentrated: the top five US educational publishers hold over 60% of the market, creating licensing dependency and elevated switching costs for buyers. Licensing windows and update cycles further entrench suppliers, though Stride reduced exposure by expanding proprietary content and in 2024 reported ~1.2B in revenue, enabling multi-year bundle negotiations to cap supplier leverage.

Cloud and platform infrastructure

Hosting, video and data services are concentrated among hyperscalers (2024 market shares: AWS 32%, Microsoft 23%, Google 11% ≈66%), giving suppliers moderate bargaining power. Volume commitments and deep technical integration drive stickiness and discount leverage. Multi-cloud strategies are widespread (Flexera 2024: 92% use multi-cloud) and in-house platforms can mitigate risk. Uptime SLAs (99.95–99.99%) and FERPA/COPPA needs add negotiation chips.

Edtech tools and integrations

Edtech integrations (LMS, proctoring, analytics, accessibility) remain fragmented, with the global LMS market around USD 18B in 2024, limiting any single supplier’s power; however required certifications and critical integrations raise switching friction. API standards and modular architectures preserve buyer flexibility, though vendor consolidation in proctoring and analytics niches could increase supplier influence over time.

Teacher and specialist labor

Certified teachers, counselors, and SPED providers are strategic inputs for Stride; tight 2023–24 labor markets and licensure-driven shortages elevated supplier leverage, with over half of districts reporting staffing shortfalls and median teacher pay near $64,000 in 2024.

Remote delivery expanded recruiting pools, lowering some pressure, while investment in pipelines and retention (grow-your-own, residency programs) has begun to rebalance bargaining power.

Devices and connectivity enablers

Hardware and broadband underpin Stride’s delivery but supplier clout is muted by competitive device markets and large public programs: US E‑Rate discounts up to 90% for eligible schools and the BEAD program’s $42.5B broadband funding (2023–24) expand buyer power; bulk procurement often yields 15–30% discounts. Supply‑chain shocks have caused component price spikes near 20% and lead times stretching to ~12 weeks, making cost volatility a risk. Providing multiple device options and offline‑friendly content reduces dependence on any single supplier and eases delivery during connectivity disruptions.

- E‑Rate: up to 90% discount

- BEAD funding: $42.5B

- Bulk discounts: ~15–30%

- Price spikes in shocks: ~20%

- Lead times during stress: ~12 weeks

Top 5 publishers >60%; cloud top3 66%; BEAD $42.5B boosts broadband access

Supplier power is elevated for standards-aligned curricula (top 5 >60%) and SPED/STEM specialists, though Stride’s $1.2B 2024 scale and proprietary content reduce exposure. Hyperscalers hold ~66% cloud share (AWS 32%, MS 23%, Google 11%), giving moderate leverage mitigated by multi-cloud (92% adoption). Hardware/broadband buyer power is strengthened by E‑Rate (up to 90%) and BEAD $42.5B funding.

| Metric | 2024 Value |

|---|---|

| Stride revenue | $1.2B |

| Top5 publishers | >60% |

| Cloud share (top3) | 66% |

| LMS market | $18B |

| Median teacher pay | $64k |

| BEAD | $42.5B |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Stride, uncovering competitive drivers, buyer and supplier power, substitutes, and entry threats with strategic commentary. Fully editable for reports, investor decks, or academic use to pinpoint disruptive risks and defendable advantages.

Stride Porter's Five Forces delivers a one-sheet, customizable summary with radar visualization and slide-ready layout—ideal for quick decisions, scenario duplication, easy data swaps, and seamless integration into dashboards without macros, so non-technical teams can assess competitive pressure fast.

Customers Bargaining Power

Districts and public schools

Districts and public schools control roughly $830 billion in annual K-12 spending (2024 est.), using formal RFPs and large contracts that give them strong bargaining power to demand customization, compliance, and outcomes reporting. Contracts commonly span 3–5 years, creating high switching costs as vendors integrate systems. State funding volatility (often ±3–7% year-to-year in some states) intensifies price pressure.

State virtual programs

Concentrated buyers—state education agencies and large districts—wield scale to dictate standards and pricing, leveraging national average per-pupil spending near $15,000 to benchmark contracts. Competitive bids force head-to-head comparisons on per-pupil rates and performance metrics. Contract renewal depends on regulatory alignment and demonstrable student outcomes. High visibility and political oversight raise stakes in negotiations.

Private schools and networks

Private schools and networks prioritize differentiation and flexibility, which reduces pure price sensitivity; the global EdTech market was estimated at about $286 billion in 2024, underscoring investment capacity. They still comparison-shop across platforms and content providers, but deep integration and teacher enablement create high switching costs and lock-in. Tiered bundles and white-label options help defend margins and capture higher ARPU.

Parents and learners

Parents and learners are fragmented but highly discerning, prioritizing experience and measurable outcomes; their bargaining power rises as switching between accredited online programs is feasible when records and credits transfer.

Reviews, NPS, community reputation drive churn, while scholarships and financing reduce price resistance.

- Fragmented buyers

- Low switching friction

- Reputation-driven churn

- Subsidies soften pricing

Employer and adult-learning clients

Corporate buyers demand job-aligned outcomes and measurable ROI, driving Stride Porter to offer outcome metrics as standard; global corporate training spend exceeded 400 billion USD in 2024, amplifying buyer scrutiny. Cohort-scale purchasing for enterprise cohorts (often hundreds of seats) increases negotiating leverage and pushes performance-based pricing and co-design. Stackable credentials and placement support lower churn by improving demonstrable career outcomes.

- Buyer focus: measurable ROI, job-aligned outcomes

- Cohort leverage: enterprise buys amplify negotiation power

- Pricing: performance-based and co-design align incentives

- Retention: stackable credentials + placement reduce churn

BuyersK12 $830B, EdTech $286B, Corp$400B

Buyers hold high bargaining power: K-12 districts control ~$830B (2024) and use RFPs and multi-year contracts to enforce price, customization, and outcomes. Per-pupil benchmarks near $15,000 drive competitive bids; EdTech market ~$286B and corporate training ~$400B (2024) raise buyer leverage. Fragmented parents/learners increase churn via reviews and transferability, while private networks accept premium for integration and outcomes.

| Buyer Segment | 2024 Spend | Leverage | Key Demand |

|---|---|---|---|

| K-12 districts | $830B | High | Compliance, outcomes, low price |

| Private/networks | — (part of $286B) | Medium | Differentiation, integration |

| Parents/learners | — | Low–Medium | Experience, transferability |

| Corporate | $400B | High | Job-aligned ROI |

Preview Before You Purchase

Stride Porter's Five Forces Analysis

This preview shows the exact Stride Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, placeholders, or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the final deliverable and will have instant access to this same document upon payment.