Subsea 7 Boston Consulting Group Matrix

Download Your Competitive Advantage

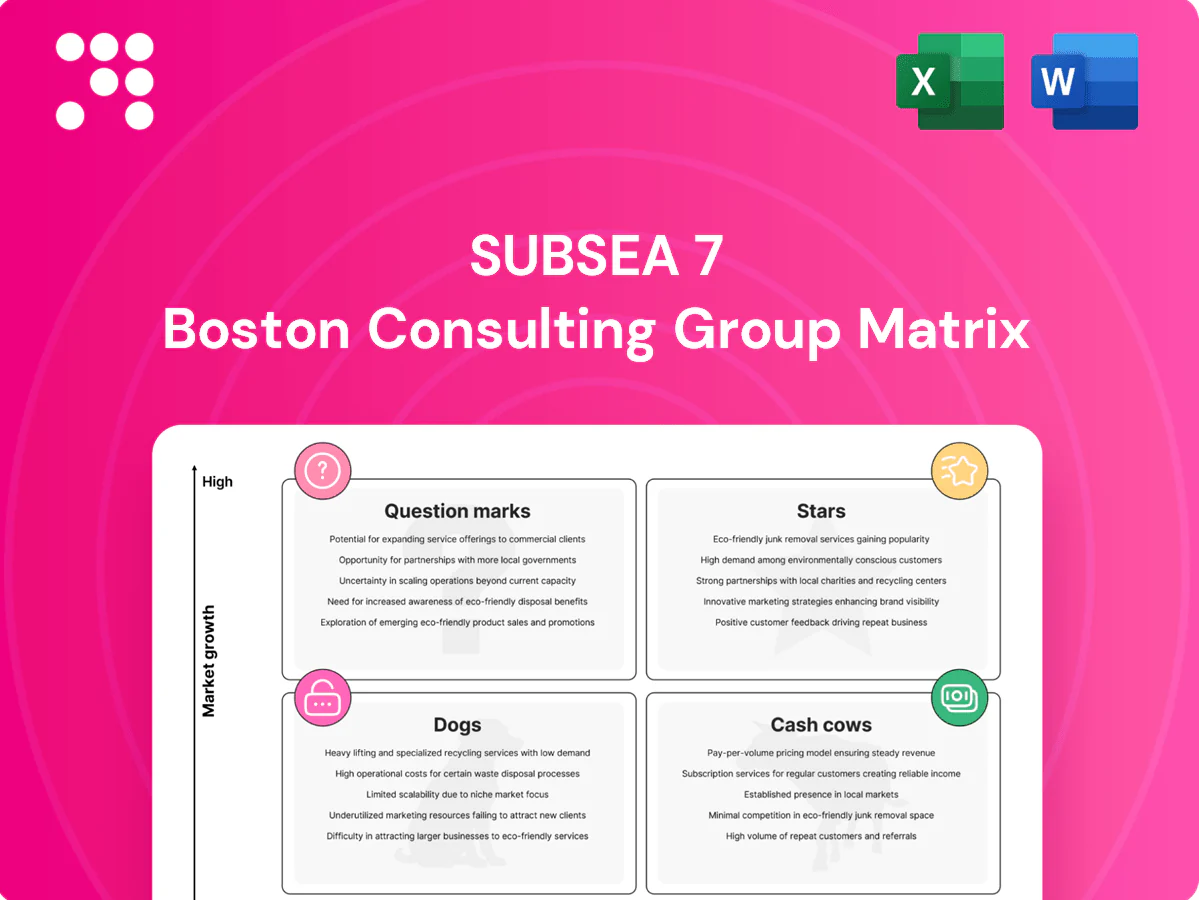

Curious where Subsea 7’s services and assets land—Stars, Cash Cows, Dogs or Question Marks? This snapshot points the way, but the full BCG Matrix gives quadrant-by-quadrant placement, clear data-backed recommendations, and a ready-to-use strategy you can act on. Buy the complete report to get a polished Word analysis plus an Excel summary for quick boardroom use. Skip the guesswork—purchase now and start reallocating capital with confidence.

Stars

Integrated SURF leadership

Subsea 7 leads complex SURF EPIC/EPCI awards across multiple basins, capturing high share and momentum in an expanding deepwater tie-back market; 2024 backlog remains multi-billion dollars, underpinning heavy vessel utilization. It soaks up cash for fleet, welding spreads and engineering, driving elevated capex and working capital needs. Returns have tracked growth, so continued investment to lock the lead is warranted to mature into outsized cash later.

Subsea Integration Alliance

The OneSubsea + Subsea 7 model wins large integrated scopes and front-end-to-execution packages, aligning with a market shifting toward integrated awards and positioning the alliance as a leader in a fast-growing procurement model. Integration consumes working capital and bid muscle, yet the visible pipeline across long-cycle E&P programs justifies continued investment. Strategy: hold share, double down on capture capability, and defend pricing discipline to protect margins.

Brazil & West Africa deepwater

Brazil pre-salt and West Africa tie-backs drive multi-year capex cycles, with basin investment sustaining >US$30bn project pipelines through 2024; Subsea7 reported a 2024 backlog around US$6bn and deploys ~40 vessels and extensive welding capacity. The company’s track record on large SURF and tie-back contracts gives it high share in a high-growth segment. Cash generation is lumpy but rich net of fleet spend, making the theater a priority for vessels and welding capacity.

Harsh-environment installation

Harsh-environment installation is a Star in Subsea 7s BCG matrix: 2024 North Sea and Atlantic weather windows favor top-tier assets and experience, and Subsea 7s heavy construction fleet and seasoned crews form a clear operational moat. Demand in 2024 is brisk as operators compress schedules and bundle scopes; keeping assets primed preserves premium day rates and Star status.

- Moat: heavy construction fleet

- Advantage: veteran crews, proven weather capability

- Market: 2024 brisk demand, compressed schedules

- Strategy: maintain readiness, capture premium day rates

Complex tie-back programs

Complex tie-back programs are the preferred low-carbon-barrel path as step-outs lengthen and dynamic risers rise in complexity; Subsea 7 wins where engineering and execution risk peak, converting challenging scopes into durable positions and future cash cows.

- High engineering share

- Rising step-out complexity

- Competitive 2024 bids

- Solid growth, real cash needs

Deepwater SURF leader: ~US$6bn backlog, ~40 vessels, >US$30bn pipeline

Subsea 7 is a Star in deepwater SURF: 2024 backlog ~US$6bn, ~40 vessels and heavy capex/working capital needs. High share in Brazil pre‑salt and West Africa where >US$30bn project pipelines run through 2024. Strategy: sustain fleet readiness, bid muscle and pricing to convert growth into future cash.

| Metric | 2024 | Implication |

|---|---|---|

| Backlog | ~US$6bn | Revenue visibility |

| Fleet | ~40 vessels | Operational moat |

| Pipeline | >US$30bn | Growth runway |

What is included in the product

BCG analysis of Subsea 7’s units: identifies Stars, Cash Cows, Question Marks and Dogs with investment, hold and divest guidance.

One-page Subsea 7 BCG Matrix placing each business unit in a quadrant for fast C-level clarity.

Cash Cows

Conventional EPCI in mature basins

Conventional EPCI in mature basins delivers stable demand and repeatable scopes with strong incumbent relationships; Subsea7 reported revenue of about USD 4.6bn (2023) and maintained healthy EPCI margins into 2024 as growth stayed modest. Margins are resilient when vessels are sequenced well, requiring low incremental promo spend and focus on delivery and efficiency. Milk with discipline and reinvest in fleet upkeep, not flash.

IMR and life-of-field

Inspection, maintenance and repair (IMR) sustain Subsea 7s life-of-field cash cows through predictable call-offs and multi-year frame agreements that convert installed-base activity into steady cashflow. Growth is low while vessel and ROV utilization remains high and unit costs are well understood, supporting margins and working-capital predictability. Optimize crew scheduling and tooling inventories to protect service levels, maximize asset utilization and bank recurring cash for higher-return investments.

Engineering/FEED and studies

Engineering/FEED and studies act as cash cows for Subsea7: front-end work funnels execution awards while largely paying its own way, converting FEED wins into higher-probability EPC contracts. It scales with pipeline activity but is not a high-growth engine; industry FEED margins often sit in the mid‑teens (around 15–20%) when standardized. Capex is low versus execution assets, and maintaining capacity and toolkits keeps deal flow sticky and conversion rates high.

Pipeline replacement and decommissioning

Pipeline replacement and decommissioning in Subsea7 are steady cash cows: legacy North Sea fields need orderly retirement with selective renewals, market growth is modest (~3% p.a.) but backlog remained dependable at around USD 5.5bn in 2024; margins improve as learned curves and asset planning reduce unit costs, while projects act as schedule filler that reliably throws off cash.

- Legacy retirements

- Modest market growth ~3% p.a.

- 2024 backlog ~USD 5.5bn

- Improving margins via learning curve

- Schedule filler → steady cash

Procurement frameworks and alliances

Long-running supplier deals and client frameworks lower bid costs and smooth workload, preserving market share without high growth; Subsea7 leverages recurring frameworks to keep margins stable and cash-positive when working capital is tightly managed.

Keep SLAs strict, harvest rebates and rigorously control scope creep to protect profitability and free cash flow.

- Defensible share via frameworks

- Reduced bid costs, smoother load

- Tight SLAs, reclaim rebates

- Strict scope control to protect cash

Lock recurring cash: EPCI + FEED margins, IMR utilization — fleet upkeep, tight SLAs

Conventional EPCI and IMR deliver steady cash for Subsea7: 2023 revenue ~USD 4.6bn, 2024 backlog ~USD 5.5bn. FEED yields mid‑teens margins (15–20%) with low capex; IMR and decommissioning show ~3% p.a. market growth and high utilization. Prioritize fleet upkeep, tight SLAs and scope control to harvest recurring cash.

| Segment | Metric | Margin | Growth |

|---|---|---|---|

| EPCI | Rev 2023 ~USD 4.6bn | EBITDA ~low‑teens | Modest |

| IMR | Multi‑yr frames | High | ~3% p.a. |

| FEED | FEED→EPC funnel | 15–20% | Stable |

| Decom | Backlog ~USD 5.5bn (2024) | Improving | ~3% p.a. |

What You See Is What You Get

Subsea 7 BCG Matrix

The file you're previewing is the exact Subsea 7 BCG Matrix report you'll receive after purchase. No watermarks, no demo sections—just a fully formatted, analysis-ready document crafted by strategy experts. Once bought, the full file is instantly downloadable and editable for presentations or planning. No surprises—what you see is what you get.

Download Your Competitive Advantage

Curious where Subsea 7’s services and assets land—Stars, Cash Cows, Dogs or Question Marks? This snapshot points the way, but the full BCG Matrix gives quadrant-by-quadrant placement, clear data-backed recommendations, and a ready-to-use strategy you can act on. Buy the complete report to get a polished Word analysis plus an Excel summary for quick boardroom use. Skip the guesswork—purchase now and start reallocating capital with confidence.

Stars

Integrated SURF leadership

Subsea 7 leads complex SURF EPIC/EPCI awards across multiple basins, capturing high share and momentum in an expanding deepwater tie-back market; 2024 backlog remains multi-billion dollars, underpinning heavy vessel utilization. It soaks up cash for fleet, welding spreads and engineering, driving elevated capex and working capital needs. Returns have tracked growth, so continued investment to lock the lead is warranted to mature into outsized cash later.

Subsea Integration Alliance

The OneSubsea + Subsea 7 model wins large integrated scopes and front-end-to-execution packages, aligning with a market shifting toward integrated awards and positioning the alliance as a leader in a fast-growing procurement model. Integration consumes working capital and bid muscle, yet the visible pipeline across long-cycle E&P programs justifies continued investment. Strategy: hold share, double down on capture capability, and defend pricing discipline to protect margins.

Brazil & West Africa deepwater

Brazil pre-salt and West Africa tie-backs drive multi-year capex cycles, with basin investment sustaining >US$30bn project pipelines through 2024; Subsea7 reported a 2024 backlog around US$6bn and deploys ~40 vessels and extensive welding capacity. The company’s track record on large SURF and tie-back contracts gives it high share in a high-growth segment. Cash generation is lumpy but rich net of fleet spend, making the theater a priority for vessels and welding capacity.

Harsh-environment installation

Harsh-environment installation is a Star in Subsea 7s BCG matrix: 2024 North Sea and Atlantic weather windows favor top-tier assets and experience, and Subsea 7s heavy construction fleet and seasoned crews form a clear operational moat. Demand in 2024 is brisk as operators compress schedules and bundle scopes; keeping assets primed preserves premium day rates and Star status.

- Moat: heavy construction fleet

- Advantage: veteran crews, proven weather capability

- Market: 2024 brisk demand, compressed schedules

- Strategy: maintain readiness, capture premium day rates

Complex tie-back programs

Complex tie-back programs are the preferred low-carbon-barrel path as step-outs lengthen and dynamic risers rise in complexity; Subsea 7 wins where engineering and execution risk peak, converting challenging scopes into durable positions and future cash cows.

- High engineering share

- Rising step-out complexity

- Competitive 2024 bids

- Solid growth, real cash needs

Deepwater SURF leader: ~US$6bn backlog, ~40 vessels, >US$30bn pipeline

Subsea 7 is a Star in deepwater SURF: 2024 backlog ~US$6bn, ~40 vessels and heavy capex/working capital needs. High share in Brazil pre‑salt and West Africa where >US$30bn project pipelines run through 2024. Strategy: sustain fleet readiness, bid muscle and pricing to convert growth into future cash.

| Metric | 2024 | Implication |

|---|---|---|

| Backlog | ~US$6bn | Revenue visibility |

| Fleet | ~40 vessels | Operational moat |

| Pipeline | >US$30bn | Growth runway |

What is included in the product

BCG analysis of Subsea 7’s units: identifies Stars, Cash Cows, Question Marks and Dogs with investment, hold and divest guidance.

One-page Subsea 7 BCG Matrix placing each business unit in a quadrant for fast C-level clarity.

Cash Cows

Conventional EPCI in mature basins

Conventional EPCI in mature basins delivers stable demand and repeatable scopes with strong incumbent relationships; Subsea7 reported revenue of about USD 4.6bn (2023) and maintained healthy EPCI margins into 2024 as growth stayed modest. Margins are resilient when vessels are sequenced well, requiring low incremental promo spend and focus on delivery and efficiency. Milk with discipline and reinvest in fleet upkeep, not flash.

IMR and life-of-field

Inspection, maintenance and repair (IMR) sustain Subsea 7s life-of-field cash cows through predictable call-offs and multi-year frame agreements that convert installed-base activity into steady cashflow. Growth is low while vessel and ROV utilization remains high and unit costs are well understood, supporting margins and working-capital predictability. Optimize crew scheduling and tooling inventories to protect service levels, maximize asset utilization and bank recurring cash for higher-return investments.

Engineering/FEED and studies

Engineering/FEED and studies act as cash cows for Subsea7: front-end work funnels execution awards while largely paying its own way, converting FEED wins into higher-probability EPC contracts. It scales with pipeline activity but is not a high-growth engine; industry FEED margins often sit in the mid‑teens (around 15–20%) when standardized. Capex is low versus execution assets, and maintaining capacity and toolkits keeps deal flow sticky and conversion rates high.

Pipeline replacement and decommissioning

Pipeline replacement and decommissioning in Subsea7 are steady cash cows: legacy North Sea fields need orderly retirement with selective renewals, market growth is modest (~3% p.a.) but backlog remained dependable at around USD 5.5bn in 2024; margins improve as learned curves and asset planning reduce unit costs, while projects act as schedule filler that reliably throws off cash.

- Legacy retirements

- Modest market growth ~3% p.a.

- 2024 backlog ~USD 5.5bn

- Improving margins via learning curve

- Schedule filler → steady cash

Procurement frameworks and alliances

Long-running supplier deals and client frameworks lower bid costs and smooth workload, preserving market share without high growth; Subsea7 leverages recurring frameworks to keep margins stable and cash-positive when working capital is tightly managed.

Keep SLAs strict, harvest rebates and rigorously control scope creep to protect profitability and free cash flow.

- Defensible share via frameworks

- Reduced bid costs, smoother load

- Tight SLAs, reclaim rebates

- Strict scope control to protect cash

Lock recurring cash: EPCI + FEED margins, IMR utilization — fleet upkeep, tight SLAs

Conventional EPCI and IMR deliver steady cash for Subsea7: 2023 revenue ~USD 4.6bn, 2024 backlog ~USD 5.5bn. FEED yields mid‑teens margins (15–20%) with low capex; IMR and decommissioning show ~3% p.a. market growth and high utilization. Prioritize fleet upkeep, tight SLAs and scope control to harvest recurring cash.

| Segment | Metric | Margin | Growth |

|---|---|---|---|

| EPCI | Rev 2023 ~USD 4.6bn | EBITDA ~low‑teens | Modest |

| IMR | Multi‑yr frames | High | ~3% p.a. |

| FEED | FEED→EPC funnel | 15–20% | Stable |

| Decom | Backlog ~USD 5.5bn (2024) | Improving | ~3% p.a. |

What You See Is What You Get

Subsea 7 BCG Matrix

The file you're previewing is the exact Subsea 7 BCG Matrix report you'll receive after purchase. No watermarks, no demo sections—just a fully formatted, analysis-ready document crafted by strategy experts. Once bought, the full file is instantly downloadable and editable for presentations or planning. No surprises—what you see is what you get.

Description

Download Your Competitive Advantage

Curious where Subsea 7’s services and assets land—Stars, Cash Cows, Dogs or Question Marks? This snapshot points the way, but the full BCG Matrix gives quadrant-by-quadrant placement, clear data-backed recommendations, and a ready-to-use strategy you can act on. Buy the complete report to get a polished Word analysis plus an Excel summary for quick boardroom use. Skip the guesswork—purchase now and start reallocating capital with confidence.

Stars

Integrated SURF leadership

Subsea 7 leads complex SURF EPIC/EPCI awards across multiple basins, capturing high share and momentum in an expanding deepwater tie-back market; 2024 backlog remains multi-billion dollars, underpinning heavy vessel utilization. It soaks up cash for fleet, welding spreads and engineering, driving elevated capex and working capital needs. Returns have tracked growth, so continued investment to lock the lead is warranted to mature into outsized cash later.

Subsea Integration Alliance

The OneSubsea + Subsea 7 model wins large integrated scopes and front-end-to-execution packages, aligning with a market shifting toward integrated awards and positioning the alliance as a leader in a fast-growing procurement model. Integration consumes working capital and bid muscle, yet the visible pipeline across long-cycle E&P programs justifies continued investment. Strategy: hold share, double down on capture capability, and defend pricing discipline to protect margins.

Brazil & West Africa deepwater

Brazil pre-salt and West Africa tie-backs drive multi-year capex cycles, with basin investment sustaining >US$30bn project pipelines through 2024; Subsea7 reported a 2024 backlog around US$6bn and deploys ~40 vessels and extensive welding capacity. The company’s track record on large SURF and tie-back contracts gives it high share in a high-growth segment. Cash generation is lumpy but rich net of fleet spend, making the theater a priority for vessels and welding capacity.

Harsh-environment installation

Harsh-environment installation is a Star in Subsea 7s BCG matrix: 2024 North Sea and Atlantic weather windows favor top-tier assets and experience, and Subsea 7s heavy construction fleet and seasoned crews form a clear operational moat. Demand in 2024 is brisk as operators compress schedules and bundle scopes; keeping assets primed preserves premium day rates and Star status.

- Moat: heavy construction fleet

- Advantage: veteran crews, proven weather capability

- Market: 2024 brisk demand, compressed schedules

- Strategy: maintain readiness, capture premium day rates

Complex tie-back programs

Complex tie-back programs are the preferred low-carbon-barrel path as step-outs lengthen and dynamic risers rise in complexity; Subsea 7 wins where engineering and execution risk peak, converting challenging scopes into durable positions and future cash cows.

- High engineering share

- Rising step-out complexity

- Competitive 2024 bids

- Solid growth, real cash needs

Deepwater SURF leader: ~US$6bn backlog, ~40 vessels, >US$30bn pipeline

Subsea 7 is a Star in deepwater SURF: 2024 backlog ~US$6bn, ~40 vessels and heavy capex/working capital needs. High share in Brazil pre‑salt and West Africa where >US$30bn project pipelines run through 2024. Strategy: sustain fleet readiness, bid muscle and pricing to convert growth into future cash.

| Metric | 2024 | Implication |

|---|---|---|

| Backlog | ~US$6bn | Revenue visibility |

| Fleet | ~40 vessels | Operational moat |

| Pipeline | >US$30bn | Growth runway |

What is included in the product

BCG analysis of Subsea 7’s units: identifies Stars, Cash Cows, Question Marks and Dogs with investment, hold and divest guidance.

One-page Subsea 7 BCG Matrix placing each business unit in a quadrant for fast C-level clarity.

Cash Cows

Conventional EPCI in mature basins

Conventional EPCI in mature basins delivers stable demand and repeatable scopes with strong incumbent relationships; Subsea7 reported revenue of about USD 4.6bn (2023) and maintained healthy EPCI margins into 2024 as growth stayed modest. Margins are resilient when vessels are sequenced well, requiring low incremental promo spend and focus on delivery and efficiency. Milk with discipline and reinvest in fleet upkeep, not flash.

IMR and life-of-field

Inspection, maintenance and repair (IMR) sustain Subsea 7s life-of-field cash cows through predictable call-offs and multi-year frame agreements that convert installed-base activity into steady cashflow. Growth is low while vessel and ROV utilization remains high and unit costs are well understood, supporting margins and working-capital predictability. Optimize crew scheduling and tooling inventories to protect service levels, maximize asset utilization and bank recurring cash for higher-return investments.

Engineering/FEED and studies

Engineering/FEED and studies act as cash cows for Subsea7: front-end work funnels execution awards while largely paying its own way, converting FEED wins into higher-probability EPC contracts. It scales with pipeline activity but is not a high-growth engine; industry FEED margins often sit in the mid‑teens (around 15–20%) when standardized. Capex is low versus execution assets, and maintaining capacity and toolkits keeps deal flow sticky and conversion rates high.

Pipeline replacement and decommissioning

Pipeline replacement and decommissioning in Subsea7 are steady cash cows: legacy North Sea fields need orderly retirement with selective renewals, market growth is modest (~3% p.a.) but backlog remained dependable at around USD 5.5bn in 2024; margins improve as learned curves and asset planning reduce unit costs, while projects act as schedule filler that reliably throws off cash.

- Legacy retirements

- Modest market growth ~3% p.a.

- 2024 backlog ~USD 5.5bn

- Improving margins via learning curve

- Schedule filler → steady cash

Procurement frameworks and alliances

Long-running supplier deals and client frameworks lower bid costs and smooth workload, preserving market share without high growth; Subsea7 leverages recurring frameworks to keep margins stable and cash-positive when working capital is tightly managed.

Keep SLAs strict, harvest rebates and rigorously control scope creep to protect profitability and free cash flow.

- Defensible share via frameworks

- Reduced bid costs, smoother load

- Tight SLAs, reclaim rebates

- Strict scope control to protect cash

Lock recurring cash: EPCI + FEED margins, IMR utilization — fleet upkeep, tight SLAs

Conventional EPCI and IMR deliver steady cash for Subsea7: 2023 revenue ~USD 4.6bn, 2024 backlog ~USD 5.5bn. FEED yields mid‑teens margins (15–20%) with low capex; IMR and decommissioning show ~3% p.a. market growth and high utilization. Prioritize fleet upkeep, tight SLAs and scope control to harvest recurring cash.

| Segment | Metric | Margin | Growth |

|---|---|---|---|

| EPCI | Rev 2023 ~USD 4.6bn | EBITDA ~low‑teens | Modest |

| IMR | Multi‑yr frames | High | ~3% p.a. |

| FEED | FEED→EPC funnel | 15–20% | Stable |

| Decom | Backlog ~USD 5.5bn (2024) | Improving | ~3% p.a. |

What You See Is What You Get

Subsea 7 BCG Matrix

The file you're previewing is the exact Subsea 7 BCG Matrix report you'll receive after purchase. No watermarks, no demo sections—just a fully formatted, analysis-ready document crafted by strategy experts. Once bought, the full file is instantly downloadable and editable for presentations or planning. No surprises—what you see is what you get.