Sulzer Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

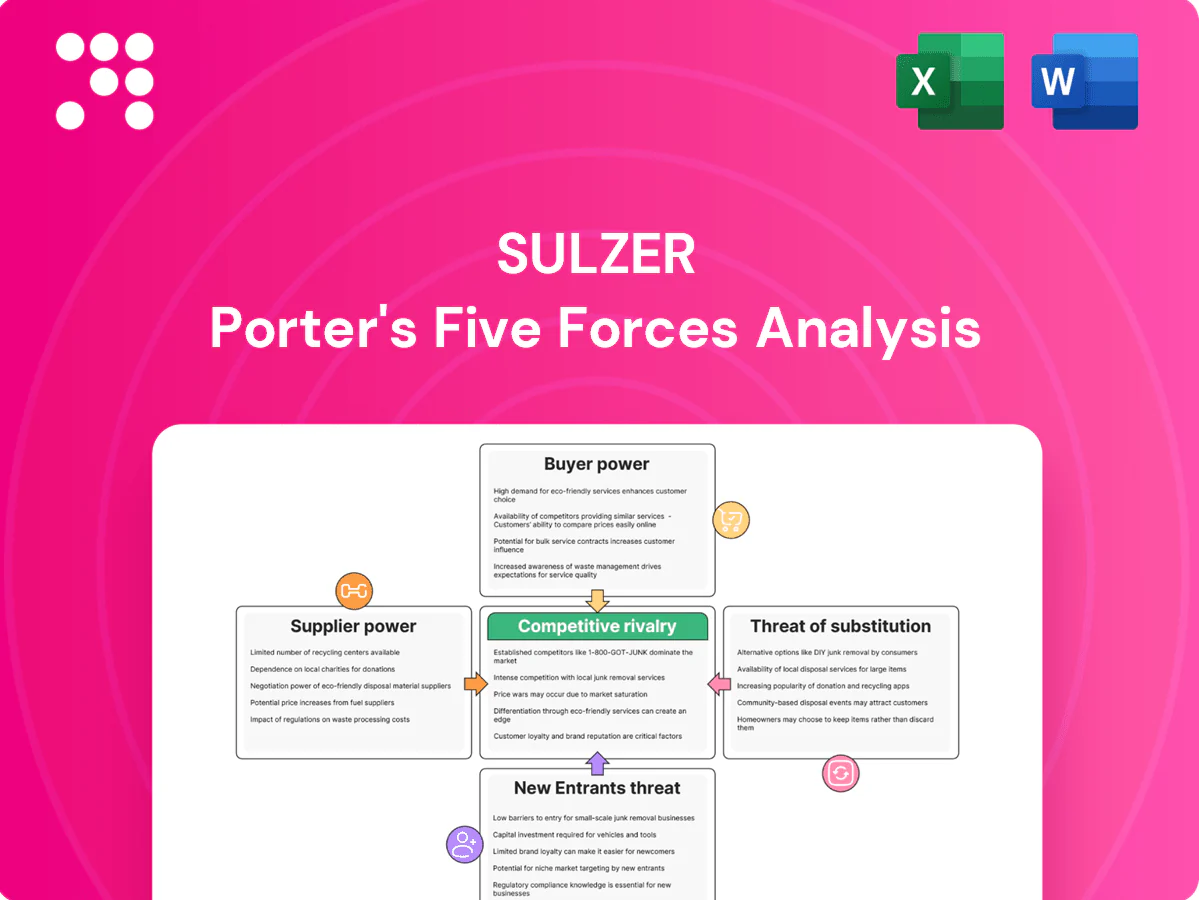

Sulzer’s Porter's Five Forces snapshot highlights competitive intensity across suppliers, customers, new entrants, substitutes, and industry rivalry, revealing where margins and strategic vulnerabilities lie. The brief flags critical pressure points—supply-chain concentration and pricing power—that shape Sulzer’s profitability and growth outlook. This preview only scratches the surface; unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized component inputs

Many pump and rotating-equipment parts are precision-engineered and sourced from niche suppliers, concentrating supply and elevating switching costs and delivery risk; qualification cycles commonly range from 6 to 18 months, which in 2024 kept supplier leverage high in the industry. Dual-sourcing and design-for-substitution are proven mitigants, reducing single-supplier supply interruption risk and procurement lead times materially.

Metals and alloy price volatility

Sulzer depends on stainless steels, superalloys and specialty coatings for pumps and rotating equipment. Commodity price swings and energy surcharges eroded margins in 2024, with metal prices moving about ±20% year-on-year and energy surcharges averaging near 3% of order value. Index-linked contracts allow only partial, lagged pass-through. Hedging and inventory buffers reduce exposure but do not eliminate residual margin risk.

Critical electronics and controls

For Sulzer, critical electronics—VFDs, sensors and PLCs—come from a concentrated vendor pool (top 5 suppliers ≈60% market share in 2024), allowing suppliers leverage via firmware lock‑ins and warranty/cybersecurity clauses; lead times now typically 8–12 weeks but can spike beyond 20 weeks under disruption, while adoption of standardized interfaces (Modbus, OPC UA) helps preserve Sulzer’s bargaining room.

Service subcontractors and field labor

Regional service partners, riggers, and certified welders are indispensable for outages; the American Welding Society estimated a 400,000-welder shortfall by 2024, tightening availability and contributing to roughly 6% wage growth in skilled trades that year. Safety and certification requirements limit quick supplier swaps, while framework agreements and joint training can rebalance power.

- High dependency on regional partners

- 400,000 welder shortfall (AWS, 2024)

- 6% skilled-labor wage growth (2024)

- Frameworks/training reduce supplier leverage

IP, coatings, and seal technologies

Mechanical seals, wear-resistant coatings and membranes are often proprietary, with licensing and qualification trials commonly taking 6–18 months and performance guarantees of 1–5 years that tie Sulzer to proven vendors; internal R&D and co-development programs progressively reduce supplier dependence over time.

- Proprietary IP

- 6–18 months trials

- 1–5 year guarantees

- Growing internal R&D

Supplier leverage high in 2024: top‑5 ≈ 60%, metal volatility ±20%

Supplier leverage remained high in 2024 due to concentrated vendors (top 5 ≈60%), long qualification cycles (6–18 months) and proprietary seals/coatings; metal price swings (~±20% YoY) and energy surcharges (~3% of order value) squeezed margins. Regional skill shortages (400,000-welder gap) and ~6% skilled‑wage growth sustained supplier pricing power, while dual‑sourcing and DfS cut risk.

| Metric | 2024 |

|---|---|

| Top‑5 supplier share (electronics) | ≈60% |

| Metal price volatility | ±20% YoY |

| Energy surcharge | ≈3% order value |

| Qualification cycle | 6–18 months |

| Welder shortfall (AWS) | 400,000 |

| Skilled wage growth | ≈6% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, entry risks and substitutes specifically for Sulzer, with strategic insights on how these forces shape its pricing, margins and market positioning.

Clear, one-sheet Porter's Five Forces for Sulzer that instantly highlights competitive pressures and relieves analysis bottlenecks, with editable pressure levels and a ready-to-use spider chart for fast, boardroom-ready insights.

Customers Bargaining Power

Large industrial buyers consolidate spend

Large oil & gas, power and water utilities consolidate spend across sites, using volume leverage to extract 5–15% price concessions and extend payment terms commonly to 60–120 days. Preferred vendor lists and panel agreements often block suppliers without top-quartile pricing, concentrating wallet share among a few incumbents. Multi-year performance contracts (3–5 years) trade lower unit price for contractual stickiness and predictable revenue streams.

High switching costs but competitive tenders

Installed base creates strong lifecycle lock-in for Sulzer spares and services, supporting recurring revenue after Sulzer reported CHF 3.6 billion sales in 2024 with services a material share of revenue. New projects, however, run open tenders focused on strict life-cycle cost criteria that intensify buyer bargaining. Qualification frameworks standardize comparisons and pressure margins, though OEM upgrades and retrofit packages defend share despite tender-driven price competition.

Demand for uptime and warranties

Customers demand MTBF >20,000 hours, pump efficiencies >90% and guaranteed outputs with SLAs often targeting 99.9% uptime; 2024 surveys show 62% of industrial firms require remote monitoring and transparent performance data. Strong SLAs with penalty clauses (commonly 0.5–2% of contract value per unplanned hour) shift risk to suppliers. Remote monitoring adoption enables value-based selling that supports 10–15% premium when KPIs are met.

Sustainability and energy-efficiency mandates

Buyers increasingly demand energy savings, lower emissions and recyclable materials; EU CSRD began phasing in for large firms in 2024, making ESG criteria bid-gates. Procurement shifts bargaining to lifecycle economics because for pumps and rotating equipment energy can represent up to 90% of lifetime cost. Demonstrated efficiency gains thus cut pure price pressure.

- ESG as bid filter (CSRD 2024)

- Lifecycle cost focus (energy ≈90% lifetime cost)

- Efficiency proofs reduce price sensitivity

Global buyers, local specs

Global buyers source across borders but demand regional certifications and local approvals, so the global industrial pumps market (~64 billion USD in 2024) still sees fragmented volumes by region. Localization requirements and certification compliance raise bid complexity and costs, creating openings for local competitors. Regional manufacturing footprints by suppliers like Sulzer reduce buyer leverage in those markets.

- Global buying vs local specs

- Certification-driven fragmentation

- Compliance raises bid cost/complexity

- Local plants lower buyer leverage

Buyers secure 5–15% concessions, 60–120 day terms; 62% demand remote KPI premium

Large buyers secure 5–15% price concessions and 60–120 day terms; multi-year contracts create stickiness despite open tenders. Sulzer reported CHF 3.6bn sales in 2024 with services material; 62% of firms require remote monitoring, enabling 10–15% premium for KPI-based selling. Energy ≈90% lifetime cost shifts bargaining to efficiency/ESG (CSRD 2024).

| Metric | Value |

|---|---|

| Sulzer 2024 sales | CHF 3.6bn |

| Market size 2024 | USD 64bn |

| Buyer concessions | 5–15% |

| Remote monitoring demand | 62% |

Preview Before You Purchase

Sulzer Porter's Five Forces Analysis

This preview shows the exact Sulzer Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written and ready for download and use the moment you buy. You're looking at the actual deliverable; once payment is complete, you'll get instant access to this identical file.

Go Beyond the Preview—Access the Full Strategic Report

Sulzer’s Porter's Five Forces snapshot highlights competitive intensity across suppliers, customers, new entrants, substitutes, and industry rivalry, revealing where margins and strategic vulnerabilities lie. The brief flags critical pressure points—supply-chain concentration and pricing power—that shape Sulzer’s profitability and growth outlook. This preview only scratches the surface; unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized component inputs

Many pump and rotating-equipment parts are precision-engineered and sourced from niche suppliers, concentrating supply and elevating switching costs and delivery risk; qualification cycles commonly range from 6 to 18 months, which in 2024 kept supplier leverage high in the industry. Dual-sourcing and design-for-substitution are proven mitigants, reducing single-supplier supply interruption risk and procurement lead times materially.

Metals and alloy price volatility

Sulzer depends on stainless steels, superalloys and specialty coatings for pumps and rotating equipment. Commodity price swings and energy surcharges eroded margins in 2024, with metal prices moving about ±20% year-on-year and energy surcharges averaging near 3% of order value. Index-linked contracts allow only partial, lagged pass-through. Hedging and inventory buffers reduce exposure but do not eliminate residual margin risk.

Critical electronics and controls

For Sulzer, critical electronics—VFDs, sensors and PLCs—come from a concentrated vendor pool (top 5 suppliers ≈60% market share in 2024), allowing suppliers leverage via firmware lock‑ins and warranty/cybersecurity clauses; lead times now typically 8–12 weeks but can spike beyond 20 weeks under disruption, while adoption of standardized interfaces (Modbus, OPC UA) helps preserve Sulzer’s bargaining room.

Service subcontractors and field labor

Regional service partners, riggers, and certified welders are indispensable for outages; the American Welding Society estimated a 400,000-welder shortfall by 2024, tightening availability and contributing to roughly 6% wage growth in skilled trades that year. Safety and certification requirements limit quick supplier swaps, while framework agreements and joint training can rebalance power.

- High dependency on regional partners

- 400,000 welder shortfall (AWS, 2024)

- 6% skilled-labor wage growth (2024)

- Frameworks/training reduce supplier leverage

IP, coatings, and seal technologies

Mechanical seals, wear-resistant coatings and membranes are often proprietary, with licensing and qualification trials commonly taking 6–18 months and performance guarantees of 1–5 years that tie Sulzer to proven vendors; internal R&D and co-development programs progressively reduce supplier dependence over time.

- Proprietary IP

- 6–18 months trials

- 1–5 year guarantees

- Growing internal R&D

Supplier leverage high in 2024: top‑5 ≈ 60%, metal volatility ±20%

Supplier leverage remained high in 2024 due to concentrated vendors (top 5 ≈60%), long qualification cycles (6–18 months) and proprietary seals/coatings; metal price swings (~±20% YoY) and energy surcharges (~3% of order value) squeezed margins. Regional skill shortages (400,000-welder gap) and ~6% skilled‑wage growth sustained supplier pricing power, while dual‑sourcing and DfS cut risk.

| Metric | 2024 |

|---|---|

| Top‑5 supplier share (electronics) | ≈60% |

| Metal price volatility | ±20% YoY |

| Energy surcharge | ≈3% order value |

| Qualification cycle | 6–18 months |

| Welder shortfall (AWS) | 400,000 |

| Skilled wage growth | ≈6% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, entry risks and substitutes specifically for Sulzer, with strategic insights on how these forces shape its pricing, margins and market positioning.

Clear, one-sheet Porter's Five Forces for Sulzer that instantly highlights competitive pressures and relieves analysis bottlenecks, with editable pressure levels and a ready-to-use spider chart for fast, boardroom-ready insights.

Customers Bargaining Power

Large industrial buyers consolidate spend

Large oil & gas, power and water utilities consolidate spend across sites, using volume leverage to extract 5–15% price concessions and extend payment terms commonly to 60–120 days. Preferred vendor lists and panel agreements often block suppliers without top-quartile pricing, concentrating wallet share among a few incumbents. Multi-year performance contracts (3–5 years) trade lower unit price for contractual stickiness and predictable revenue streams.

High switching costs but competitive tenders

Installed base creates strong lifecycle lock-in for Sulzer spares and services, supporting recurring revenue after Sulzer reported CHF 3.6 billion sales in 2024 with services a material share of revenue. New projects, however, run open tenders focused on strict life-cycle cost criteria that intensify buyer bargaining. Qualification frameworks standardize comparisons and pressure margins, though OEM upgrades and retrofit packages defend share despite tender-driven price competition.

Demand for uptime and warranties

Customers demand MTBF >20,000 hours, pump efficiencies >90% and guaranteed outputs with SLAs often targeting 99.9% uptime; 2024 surveys show 62% of industrial firms require remote monitoring and transparent performance data. Strong SLAs with penalty clauses (commonly 0.5–2% of contract value per unplanned hour) shift risk to suppliers. Remote monitoring adoption enables value-based selling that supports 10–15% premium when KPIs are met.

Sustainability and energy-efficiency mandates

Buyers increasingly demand energy savings, lower emissions and recyclable materials; EU CSRD began phasing in for large firms in 2024, making ESG criteria bid-gates. Procurement shifts bargaining to lifecycle economics because for pumps and rotating equipment energy can represent up to 90% of lifetime cost. Demonstrated efficiency gains thus cut pure price pressure.

- ESG as bid filter (CSRD 2024)

- Lifecycle cost focus (energy ≈90% lifetime cost)

- Efficiency proofs reduce price sensitivity

Global buyers, local specs

Global buyers source across borders but demand regional certifications and local approvals, so the global industrial pumps market (~64 billion USD in 2024) still sees fragmented volumes by region. Localization requirements and certification compliance raise bid complexity and costs, creating openings for local competitors. Regional manufacturing footprints by suppliers like Sulzer reduce buyer leverage in those markets.

- Global buying vs local specs

- Certification-driven fragmentation

- Compliance raises bid cost/complexity

- Local plants lower buyer leverage

Buyers secure 5–15% concessions, 60–120 day terms; 62% demand remote KPI premium

Large buyers secure 5–15% price concessions and 60–120 day terms; multi-year contracts create stickiness despite open tenders. Sulzer reported CHF 3.6bn sales in 2024 with services material; 62% of firms require remote monitoring, enabling 10–15% premium for KPI-based selling. Energy ≈90% lifetime cost shifts bargaining to efficiency/ESG (CSRD 2024).

| Metric | Value |

|---|---|

| Sulzer 2024 sales | CHF 3.6bn |

| Market size 2024 | USD 64bn |

| Buyer concessions | 5–15% |

| Remote monitoring demand | 62% |

Preview Before You Purchase

Sulzer Porter's Five Forces Analysis

This preview shows the exact Sulzer Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written and ready for download and use the moment you buy. You're looking at the actual deliverable; once payment is complete, you'll get instant access to this identical file.

Description

Go Beyond the Preview—Access the Full Strategic Report

Sulzer’s Porter's Five Forces snapshot highlights competitive intensity across suppliers, customers, new entrants, substitutes, and industry rivalry, revealing where margins and strategic vulnerabilities lie. The brief flags critical pressure points—supply-chain concentration and pricing power—that shape Sulzer’s profitability and growth outlook. This preview only scratches the surface; unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized component inputs

Many pump and rotating-equipment parts are precision-engineered and sourced from niche suppliers, concentrating supply and elevating switching costs and delivery risk; qualification cycles commonly range from 6 to 18 months, which in 2024 kept supplier leverage high in the industry. Dual-sourcing and design-for-substitution are proven mitigants, reducing single-supplier supply interruption risk and procurement lead times materially.

Metals and alloy price volatility

Sulzer depends on stainless steels, superalloys and specialty coatings for pumps and rotating equipment. Commodity price swings and energy surcharges eroded margins in 2024, with metal prices moving about ±20% year-on-year and energy surcharges averaging near 3% of order value. Index-linked contracts allow only partial, lagged pass-through. Hedging and inventory buffers reduce exposure but do not eliminate residual margin risk.

Critical electronics and controls

For Sulzer, critical electronics—VFDs, sensors and PLCs—come from a concentrated vendor pool (top 5 suppliers ≈60% market share in 2024), allowing suppliers leverage via firmware lock‑ins and warranty/cybersecurity clauses; lead times now typically 8–12 weeks but can spike beyond 20 weeks under disruption, while adoption of standardized interfaces (Modbus, OPC UA) helps preserve Sulzer’s bargaining room.

Service subcontractors and field labor

Regional service partners, riggers, and certified welders are indispensable for outages; the American Welding Society estimated a 400,000-welder shortfall by 2024, tightening availability and contributing to roughly 6% wage growth in skilled trades that year. Safety and certification requirements limit quick supplier swaps, while framework agreements and joint training can rebalance power.

- High dependency on regional partners

- 400,000 welder shortfall (AWS, 2024)

- 6% skilled-labor wage growth (2024)

- Frameworks/training reduce supplier leverage

IP, coatings, and seal technologies

Mechanical seals, wear-resistant coatings and membranes are often proprietary, with licensing and qualification trials commonly taking 6–18 months and performance guarantees of 1–5 years that tie Sulzer to proven vendors; internal R&D and co-development programs progressively reduce supplier dependence over time.

- Proprietary IP

- 6–18 months trials

- 1–5 year guarantees

- Growing internal R&D

Supplier leverage high in 2024: top‑5 ≈ 60%, metal volatility ±20%

Supplier leverage remained high in 2024 due to concentrated vendors (top 5 ≈60%), long qualification cycles (6–18 months) and proprietary seals/coatings; metal price swings (~±20% YoY) and energy surcharges (~3% of order value) squeezed margins. Regional skill shortages (400,000-welder gap) and ~6% skilled‑wage growth sustained supplier pricing power, while dual‑sourcing and DfS cut risk.

| Metric | 2024 |

|---|---|

| Top‑5 supplier share (electronics) | ≈60% |

| Metal price volatility | ±20% YoY |

| Energy surcharge | ≈3% order value |

| Qualification cycle | 6–18 months |

| Welder shortfall (AWS) | 400,000 |

| Skilled wage growth | ≈6% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, entry risks and substitutes specifically for Sulzer, with strategic insights on how these forces shape its pricing, margins and market positioning.

Clear, one-sheet Porter's Five Forces for Sulzer that instantly highlights competitive pressures and relieves analysis bottlenecks, with editable pressure levels and a ready-to-use spider chart for fast, boardroom-ready insights.

Customers Bargaining Power

Large industrial buyers consolidate spend

Large oil & gas, power and water utilities consolidate spend across sites, using volume leverage to extract 5–15% price concessions and extend payment terms commonly to 60–120 days. Preferred vendor lists and panel agreements often block suppliers without top-quartile pricing, concentrating wallet share among a few incumbents. Multi-year performance contracts (3–5 years) trade lower unit price for contractual stickiness and predictable revenue streams.

High switching costs but competitive tenders

Installed base creates strong lifecycle lock-in for Sulzer spares and services, supporting recurring revenue after Sulzer reported CHF 3.6 billion sales in 2024 with services a material share of revenue. New projects, however, run open tenders focused on strict life-cycle cost criteria that intensify buyer bargaining. Qualification frameworks standardize comparisons and pressure margins, though OEM upgrades and retrofit packages defend share despite tender-driven price competition.

Demand for uptime and warranties

Customers demand MTBF >20,000 hours, pump efficiencies >90% and guaranteed outputs with SLAs often targeting 99.9% uptime; 2024 surveys show 62% of industrial firms require remote monitoring and transparent performance data. Strong SLAs with penalty clauses (commonly 0.5–2% of contract value per unplanned hour) shift risk to suppliers. Remote monitoring adoption enables value-based selling that supports 10–15% premium when KPIs are met.

Sustainability and energy-efficiency mandates

Buyers increasingly demand energy savings, lower emissions and recyclable materials; EU CSRD began phasing in for large firms in 2024, making ESG criteria bid-gates. Procurement shifts bargaining to lifecycle economics because for pumps and rotating equipment energy can represent up to 90% of lifetime cost. Demonstrated efficiency gains thus cut pure price pressure.

- ESG as bid filter (CSRD 2024)

- Lifecycle cost focus (energy ≈90% lifetime cost)

- Efficiency proofs reduce price sensitivity

Global buyers, local specs

Global buyers source across borders but demand regional certifications and local approvals, so the global industrial pumps market (~64 billion USD in 2024) still sees fragmented volumes by region. Localization requirements and certification compliance raise bid complexity and costs, creating openings for local competitors. Regional manufacturing footprints by suppliers like Sulzer reduce buyer leverage in those markets.

- Global buying vs local specs

- Certification-driven fragmentation

- Compliance raises bid cost/complexity

- Local plants lower buyer leverage

Buyers secure 5–15% concessions, 60–120 day terms; 62% demand remote KPI premium

Large buyers secure 5–15% price concessions and 60–120 day terms; multi-year contracts create stickiness despite open tenders. Sulzer reported CHF 3.6bn sales in 2024 with services material; 62% of firms require remote monitoring, enabling 10–15% premium for KPI-based selling. Energy ≈90% lifetime cost shifts bargaining to efficiency/ESG (CSRD 2024).

| Metric | Value |

|---|---|

| Sulzer 2024 sales | CHF 3.6bn |

| Market size 2024 | USD 64bn |

| Buyer concessions | 5–15% |

| Remote monitoring demand | 62% |

Preview Before You Purchase

Sulzer Porter's Five Forces Analysis

This preview shows the exact Sulzer Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written and ready for download and use the moment you buy. You're looking at the actual deliverable; once payment is complete, you'll get instant access to this identical file.