Sumitomo Bakelite Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

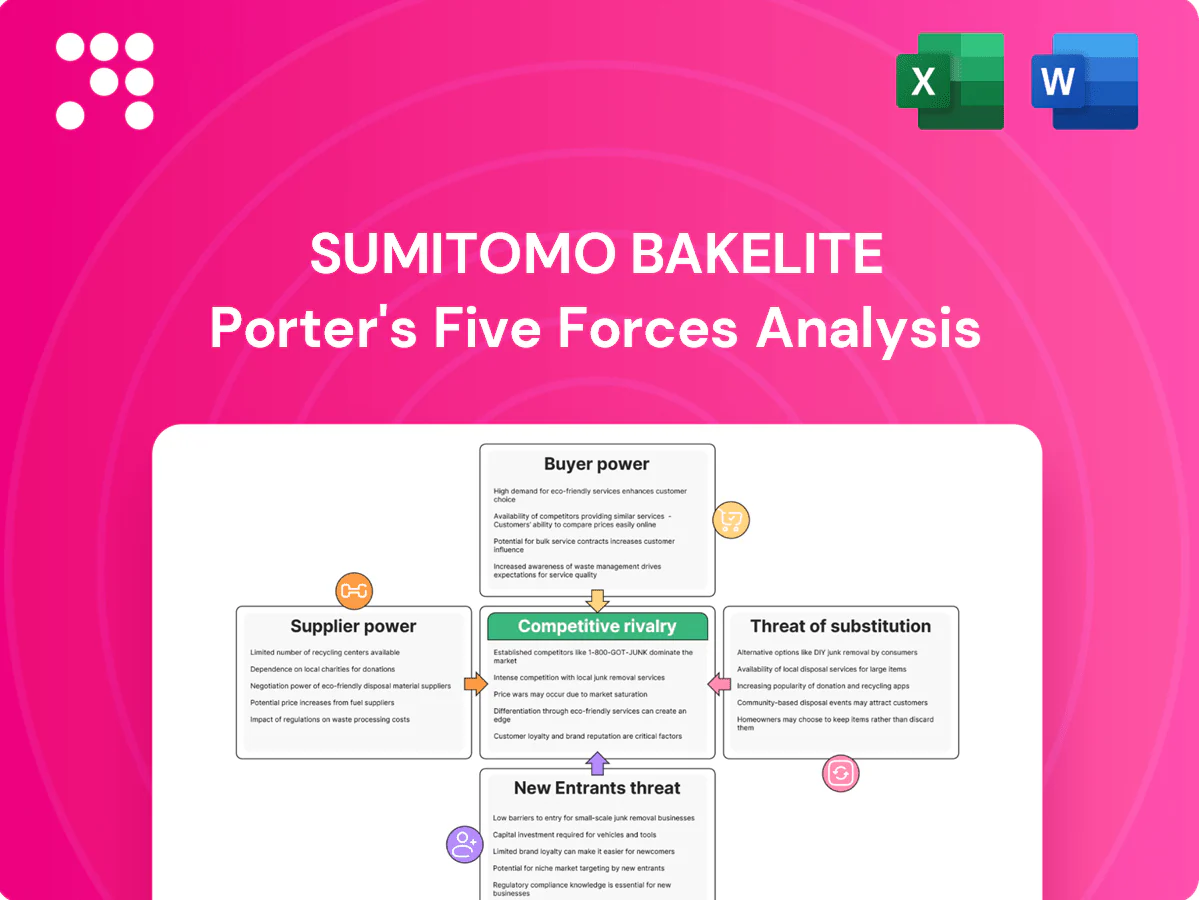

Sumitomo Bakelite faces moderate buyer power, concentrated suppliers for specialty resins, and varying threat levels from substitutes and new entrants shaped by technology and scale, creating a nuanced competitive landscape. Strategic positioning hinges on product differentiation and supply-chain advantage to sustain margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore these dynamics in detail.

Suppliers Bargaining Power

Specialty monomer concentration

Suppliers of phenol, formaldehyde, epoxy precursors and advanced monomers remain highly concentrated, giving established chemical players significant leverage over pricing and terms. Qualification of new sources is slow because of stringent performance specs and lengthy validation cycles spanning months to years. This concentration lets incumbents push prices, while long-term contracts and dual-sourcing partially mitigate supply risk for Sumitomo Bakelite.

Switching costs and qualification

Changing resin/additive suppliers requires requalification, line trials and customer approvals, with electronics typically 6–18 months and automotive/medical often 12–36 months, so switching costs are high and boost supplier bargaining power. High costs can lock pricing and timelines for Sumitomo Bakelite. Strategic safety stock (commonly 3–6 months) and technical-equivalency programs reduce dependence on single suppliers.

Energy and logistics sensitivity

Feedstock and resin costs for Sumitomo Bakelite closely track energy and freight markets: Brent crude averaged about $85/bbl in 2024 and Henry Hub gas near $3.50/MMBtu, while shipping indices often ran in the 2,000–3,000 range, boosting supplier leverage. Volatility enables suppliers to pass surcharges faster than buyers accept, squeezing margins. Hedging and regionalized sourcing mitigate this exposure.

Backward integration risk

Large petrochemical firms can forward-integrate into specialty resins and films, raising supplier bargaining power; the global specialty resins market was ~USD 40bn in 2024, concentrating scale advantages with majors. This threat intensifies negotiations, though co-development agreements secure priority allocation and align incentives. Sumitomo Bakelite's proprietary formulations reduce direct comparability, buffering margin pressure.

- Backward integration risk: high

- Market size 2024: ~USD 40bn

- Mitigant: co-development agreements

- Defensive: proprietary formulations

ESG and regulatory constraints

Tighter environmental rules on formaldehyde, PFAS and VOCs — including the EU push to restrict PFAS in 2024 — raise compliance costs and can constrict feedstock availability, concentrating supply among better‑capitalized chemical suppliers and increasing supplier leverage over Sumitomo Bakelite.

- Compliance investments concentrate suppliers

- Narrower qualified vendor pools raise leverage

- Proactive green‑chemistry sourcing broadens options

Concentrated resin suppliers raise bargaining power; market ~USD 40bn

Suppliers of phenol/formaldehyde/epoxy are concentrated, giving high bargaining power; specialty resins market ~USD 40bn (2024) and backward‑integration risk high. Long validation (6–36 months) and 3–6 months safety stock raise switching costs; Brent ~$85/bbl, Henry Hub ~$3.50/MMBtu in 2024 increased feedstock pass‑through. Co‑development and proprietary formulations partially mitigate supplier leverage.

| Metric | 2024 Value |

|---|---|

| Specialty resins market | ~USD 40bn |

| Brent crude | ~USD 85/bbl |

| Henry Hub | ~USD 3.50/MMBtu |

| Validation time | 6–36 months |

| Safety stock | 3–6 months |

What is included in the product

Provides a tailored Porter's Five Forces analysis for Sumitomo Bakelite, uncovering competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and industry rivalry, while highlighting disruptive forces, pricing influence, and protective barriers to inform strategic decisions.

A one-sheet Porter's Five Forces for Sumitomo Bakelite that visualizes competitive pressures and offers customizable inputs to quickly identify pain points and guide strategic responses.

Customers Bargaining Power

Large OEMs and Tier-1 buyers

Automotive, electronics and medical multinationals buy Sumitomo Bakelite volumes at scale and commonly push annual price-downs of roughly 1–3%, using sophisticated should-cost models that squeeze supplier margins; vendor scorecards and annual audits are standard in procurement. Large OEM design-in positions, however, can secure mid-cycle price stability and higher margins on specialized phenolics and compound formulations.

Long qualification, high reliability

Approved-vendor lists and stringent post-qualification specs lock in Sumitomo Bakelite suppliers, meaning switching is limited even where buyers have strong negotiating power. Regulatory and performance-in-use requirements such as ISO and FDA-oriented controls increase supplier stickiness because failures in critical applications carry high safety and recall costs. Buyers therefore prioritize continuity and validated performance over lowest-price sourcing.

Customization and co-development

Tailored resin systems and films create higher dependency on specific Sumitomo Bakelite suppliers, a trend reinforced in 2024 as demand for specialty grades rose across electronics and automotive segments.

Custom IP and process know-how restrict easy substitution by buyers, reducing price-driven switching and strengthening supplier leverage in specialized product lines.

Consequently buyer bargaining power is weakened for niche grades, making service quality and technical support decisive competitive differentiators.

Multi-sourcing strategies

End-market cyclicality

- Autos: cyclical OEM orders

- Smartphones: 2024 shipments ~1.15B

- Semiconductors: allocation flips leverage

- Portfolio diversity = smoother cash flow

Moderate buyer power - OEMs push 1-3% cuts; specialty resins resist amid ~1.15B phones

Buyers exert moderate bargaining power: large OEMs push annual price-downs of 1–3% and maintain at least two qualified sources per critical grade, but design-ins and regulatory specs limit switching for specialty grades. Custom resins and technical support strengthen Sumitomo Bakelite’s leverage in niche products, while cyclical demand (smartphones ~1.15B shipments in 2024) amplifies buyer power in downturns.

| Metric | 2024 |

|---|---|

| Buyer price-downs | 1–3% p.a. |

| Qualified sources | ≥2 per critical grade |

| Smartphone shipments | ~1.15B |

Preview Before You Purchase

Sumitomo Bakelite Porter's Five Forces Analysis

You’re previewing the Sumitomo Bakelite Porter’s Five Forces Analysis and this is the exact document you’ll receive after purchase. It’s fully formatted, final, and ready for immediate download—no placeholders or partial samples. Use it as-is for research, reporting, or decision-making the moment you buy.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sumitomo Bakelite faces moderate buyer power, concentrated suppliers for specialty resins, and varying threat levels from substitutes and new entrants shaped by technology and scale, creating a nuanced competitive landscape. Strategic positioning hinges on product differentiation and supply-chain advantage to sustain margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore these dynamics in detail.

Suppliers Bargaining Power

Specialty monomer concentration

Suppliers of phenol, formaldehyde, epoxy precursors and advanced monomers remain highly concentrated, giving established chemical players significant leverage over pricing and terms. Qualification of new sources is slow because of stringent performance specs and lengthy validation cycles spanning months to years. This concentration lets incumbents push prices, while long-term contracts and dual-sourcing partially mitigate supply risk for Sumitomo Bakelite.

Switching costs and qualification

Changing resin/additive suppliers requires requalification, line trials and customer approvals, with electronics typically 6–18 months and automotive/medical often 12–36 months, so switching costs are high and boost supplier bargaining power. High costs can lock pricing and timelines for Sumitomo Bakelite. Strategic safety stock (commonly 3–6 months) and technical-equivalency programs reduce dependence on single suppliers.

Energy and logistics sensitivity

Feedstock and resin costs for Sumitomo Bakelite closely track energy and freight markets: Brent crude averaged about $85/bbl in 2024 and Henry Hub gas near $3.50/MMBtu, while shipping indices often ran in the 2,000–3,000 range, boosting supplier leverage. Volatility enables suppliers to pass surcharges faster than buyers accept, squeezing margins. Hedging and regionalized sourcing mitigate this exposure.

Backward integration risk

Large petrochemical firms can forward-integrate into specialty resins and films, raising supplier bargaining power; the global specialty resins market was ~USD 40bn in 2024, concentrating scale advantages with majors. This threat intensifies negotiations, though co-development agreements secure priority allocation and align incentives. Sumitomo Bakelite's proprietary formulations reduce direct comparability, buffering margin pressure.

- Backward integration risk: high

- Market size 2024: ~USD 40bn

- Mitigant: co-development agreements

- Defensive: proprietary formulations

ESG and regulatory constraints

Tighter environmental rules on formaldehyde, PFAS and VOCs — including the EU push to restrict PFAS in 2024 — raise compliance costs and can constrict feedstock availability, concentrating supply among better‑capitalized chemical suppliers and increasing supplier leverage over Sumitomo Bakelite.

- Compliance investments concentrate suppliers

- Narrower qualified vendor pools raise leverage

- Proactive green‑chemistry sourcing broadens options

Concentrated resin suppliers raise bargaining power; market ~USD 40bn

Suppliers of phenol/formaldehyde/epoxy are concentrated, giving high bargaining power; specialty resins market ~USD 40bn (2024) and backward‑integration risk high. Long validation (6–36 months) and 3–6 months safety stock raise switching costs; Brent ~$85/bbl, Henry Hub ~$3.50/MMBtu in 2024 increased feedstock pass‑through. Co‑development and proprietary formulations partially mitigate supplier leverage.

| Metric | 2024 Value |

|---|---|

| Specialty resins market | ~USD 40bn |

| Brent crude | ~USD 85/bbl |

| Henry Hub | ~USD 3.50/MMBtu |

| Validation time | 6–36 months |

| Safety stock | 3–6 months |

What is included in the product

Provides a tailored Porter's Five Forces analysis for Sumitomo Bakelite, uncovering competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and industry rivalry, while highlighting disruptive forces, pricing influence, and protective barriers to inform strategic decisions.

A one-sheet Porter's Five Forces for Sumitomo Bakelite that visualizes competitive pressures and offers customizable inputs to quickly identify pain points and guide strategic responses.

Customers Bargaining Power

Large OEMs and Tier-1 buyers

Automotive, electronics and medical multinationals buy Sumitomo Bakelite volumes at scale and commonly push annual price-downs of roughly 1–3%, using sophisticated should-cost models that squeeze supplier margins; vendor scorecards and annual audits are standard in procurement. Large OEM design-in positions, however, can secure mid-cycle price stability and higher margins on specialized phenolics and compound formulations.

Long qualification, high reliability

Approved-vendor lists and stringent post-qualification specs lock in Sumitomo Bakelite suppliers, meaning switching is limited even where buyers have strong negotiating power. Regulatory and performance-in-use requirements such as ISO and FDA-oriented controls increase supplier stickiness because failures in critical applications carry high safety and recall costs. Buyers therefore prioritize continuity and validated performance over lowest-price sourcing.

Customization and co-development

Tailored resin systems and films create higher dependency on specific Sumitomo Bakelite suppliers, a trend reinforced in 2024 as demand for specialty grades rose across electronics and automotive segments.

Custom IP and process know-how restrict easy substitution by buyers, reducing price-driven switching and strengthening supplier leverage in specialized product lines.

Consequently buyer bargaining power is weakened for niche grades, making service quality and technical support decisive competitive differentiators.

Multi-sourcing strategies

End-market cyclicality

- Autos: cyclical OEM orders

- Smartphones: 2024 shipments ~1.15B

- Semiconductors: allocation flips leverage

- Portfolio diversity = smoother cash flow

Moderate buyer power - OEMs push 1-3% cuts; specialty resins resist amid ~1.15B phones

Buyers exert moderate bargaining power: large OEMs push annual price-downs of 1–3% and maintain at least two qualified sources per critical grade, but design-ins and regulatory specs limit switching for specialty grades. Custom resins and technical support strengthen Sumitomo Bakelite’s leverage in niche products, while cyclical demand (smartphones ~1.15B shipments in 2024) amplifies buyer power in downturns.

| Metric | 2024 |

|---|---|

| Buyer price-downs | 1–3% p.a. |

| Qualified sources | ≥2 per critical grade |

| Smartphone shipments | ~1.15B |

Preview Before You Purchase

Sumitomo Bakelite Porter's Five Forces Analysis

You’re previewing the Sumitomo Bakelite Porter’s Five Forces Analysis and this is the exact document you’ll receive after purchase. It’s fully formatted, final, and ready for immediate download—no placeholders or partial samples. Use it as-is for research, reporting, or decision-making the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sumitomo Bakelite faces moderate buyer power, concentrated suppliers for specialty resins, and varying threat levels from substitutes and new entrants shaped by technology and scale, creating a nuanced competitive landscape. Strategic positioning hinges on product differentiation and supply-chain advantage to sustain margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore these dynamics in detail.

Suppliers Bargaining Power

Specialty monomer concentration

Suppliers of phenol, formaldehyde, epoxy precursors and advanced monomers remain highly concentrated, giving established chemical players significant leverage over pricing and terms. Qualification of new sources is slow because of stringent performance specs and lengthy validation cycles spanning months to years. This concentration lets incumbents push prices, while long-term contracts and dual-sourcing partially mitigate supply risk for Sumitomo Bakelite.

Switching costs and qualification

Changing resin/additive suppliers requires requalification, line trials and customer approvals, with electronics typically 6–18 months and automotive/medical often 12–36 months, so switching costs are high and boost supplier bargaining power. High costs can lock pricing and timelines for Sumitomo Bakelite. Strategic safety stock (commonly 3–6 months) and technical-equivalency programs reduce dependence on single suppliers.

Energy and logistics sensitivity

Feedstock and resin costs for Sumitomo Bakelite closely track energy and freight markets: Brent crude averaged about $85/bbl in 2024 and Henry Hub gas near $3.50/MMBtu, while shipping indices often ran in the 2,000–3,000 range, boosting supplier leverage. Volatility enables suppliers to pass surcharges faster than buyers accept, squeezing margins. Hedging and regionalized sourcing mitigate this exposure.

Backward integration risk

Large petrochemical firms can forward-integrate into specialty resins and films, raising supplier bargaining power; the global specialty resins market was ~USD 40bn in 2024, concentrating scale advantages with majors. This threat intensifies negotiations, though co-development agreements secure priority allocation and align incentives. Sumitomo Bakelite's proprietary formulations reduce direct comparability, buffering margin pressure.

- Backward integration risk: high

- Market size 2024: ~USD 40bn

- Mitigant: co-development agreements

- Defensive: proprietary formulations

ESG and regulatory constraints

Tighter environmental rules on formaldehyde, PFAS and VOCs — including the EU push to restrict PFAS in 2024 — raise compliance costs and can constrict feedstock availability, concentrating supply among better‑capitalized chemical suppliers and increasing supplier leverage over Sumitomo Bakelite.

- Compliance investments concentrate suppliers

- Narrower qualified vendor pools raise leverage

- Proactive green‑chemistry sourcing broadens options

Concentrated resin suppliers raise bargaining power; market ~USD 40bn

Suppliers of phenol/formaldehyde/epoxy are concentrated, giving high bargaining power; specialty resins market ~USD 40bn (2024) and backward‑integration risk high. Long validation (6–36 months) and 3–6 months safety stock raise switching costs; Brent ~$85/bbl, Henry Hub ~$3.50/MMBtu in 2024 increased feedstock pass‑through. Co‑development and proprietary formulations partially mitigate supplier leverage.

| Metric | 2024 Value |

|---|---|

| Specialty resins market | ~USD 40bn |

| Brent crude | ~USD 85/bbl |

| Henry Hub | ~USD 3.50/MMBtu |

| Validation time | 6–36 months |

| Safety stock | 3–6 months |

What is included in the product

Provides a tailored Porter's Five Forces analysis for Sumitomo Bakelite, uncovering competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and industry rivalry, while highlighting disruptive forces, pricing influence, and protective barriers to inform strategic decisions.

A one-sheet Porter's Five Forces for Sumitomo Bakelite that visualizes competitive pressures and offers customizable inputs to quickly identify pain points and guide strategic responses.

Customers Bargaining Power

Large OEMs and Tier-1 buyers

Automotive, electronics and medical multinationals buy Sumitomo Bakelite volumes at scale and commonly push annual price-downs of roughly 1–3%, using sophisticated should-cost models that squeeze supplier margins; vendor scorecards and annual audits are standard in procurement. Large OEM design-in positions, however, can secure mid-cycle price stability and higher margins on specialized phenolics and compound formulations.

Long qualification, high reliability

Approved-vendor lists and stringent post-qualification specs lock in Sumitomo Bakelite suppliers, meaning switching is limited even where buyers have strong negotiating power. Regulatory and performance-in-use requirements such as ISO and FDA-oriented controls increase supplier stickiness because failures in critical applications carry high safety and recall costs. Buyers therefore prioritize continuity and validated performance over lowest-price sourcing.

Customization and co-development

Tailored resin systems and films create higher dependency on specific Sumitomo Bakelite suppliers, a trend reinforced in 2024 as demand for specialty grades rose across electronics and automotive segments.

Custom IP and process know-how restrict easy substitution by buyers, reducing price-driven switching and strengthening supplier leverage in specialized product lines.

Consequently buyer bargaining power is weakened for niche grades, making service quality and technical support decisive competitive differentiators.

Multi-sourcing strategies

End-market cyclicality

- Autos: cyclical OEM orders

- Smartphones: 2024 shipments ~1.15B

- Semiconductors: allocation flips leverage

- Portfolio diversity = smoother cash flow

Moderate buyer power - OEMs push 1-3% cuts; specialty resins resist amid ~1.15B phones

Buyers exert moderate bargaining power: large OEMs push annual price-downs of 1–3% and maintain at least two qualified sources per critical grade, but design-ins and regulatory specs limit switching for specialty grades. Custom resins and technical support strengthen Sumitomo Bakelite’s leverage in niche products, while cyclical demand (smartphones ~1.15B shipments in 2024) amplifies buyer power in downturns.

| Metric | 2024 |

|---|---|

| Buyer price-downs | 1–3% p.a. |

| Qualified sources | ≥2 per critical grade |

| Smartphone shipments | ~1.15B |

Preview Before You Purchase

Sumitomo Bakelite Porter's Five Forces Analysis

You’re previewing the Sumitomo Bakelite Porter’s Five Forces Analysis and this is the exact document you’ll receive after purchase. It’s fully formatted, final, and ready for immediate download—no placeholders or partial samples. Use it as-is for research, reporting, or decision-making the moment you buy.