Sumitomo Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

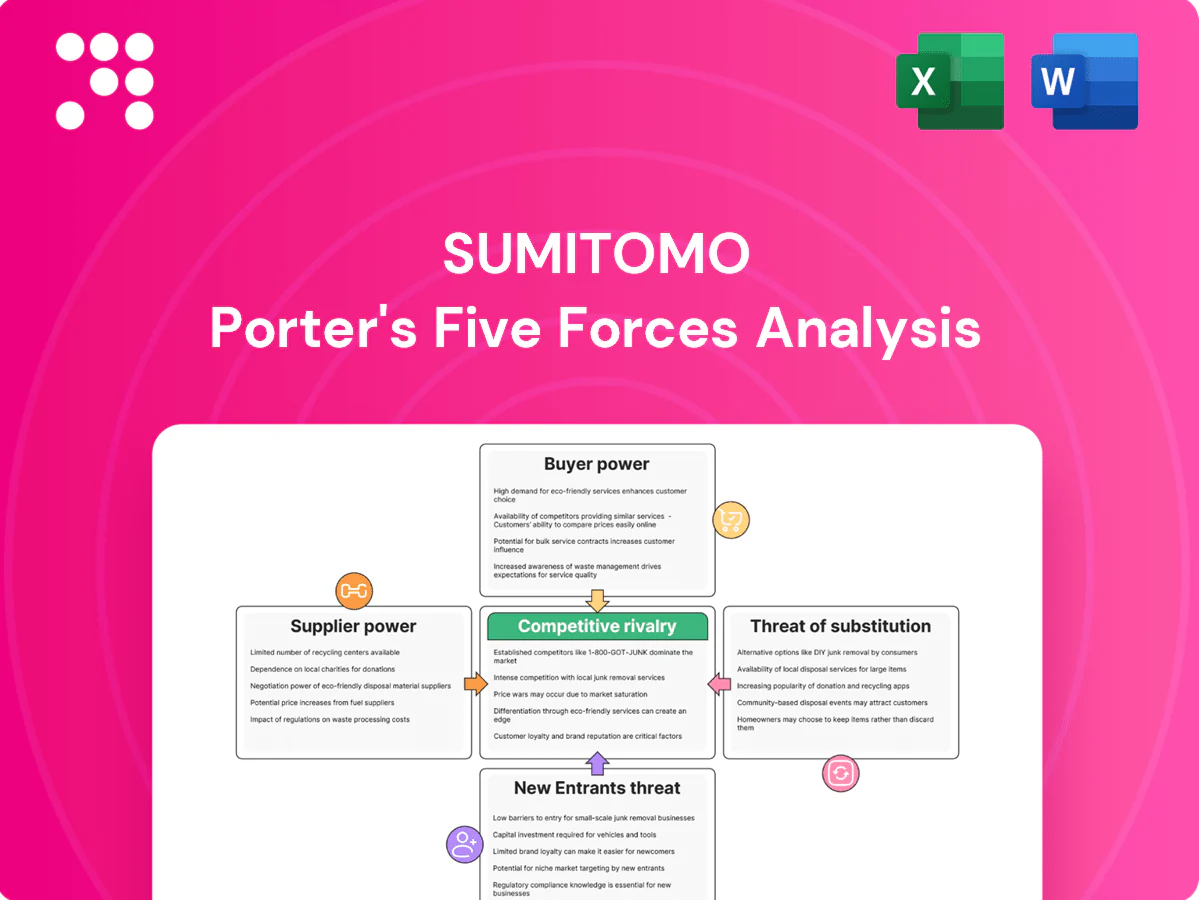

Sumitomo’s Five Forces snapshot highlights strong supplier ties, diversified buyer segments, moderate threat of substitutes, and barriers shaped by capital intensity and regulation. This concise view reveals where competitive pressure is highest and where strategic advantage can be built. This preview only scratches the surface — unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Supplier Power 1

Sumitomo’s vast, diversified supplier network across metals, energy and chemicals reduces dependence on any single vendor, with long-term offtake, JV equity stakes and co-development deals aligning incentives and stabilizing contract terms.

Scarcity in critical minerals such as lithium, nickel and copper, however, can shift leverage to upstream owners, tightening access and raising spot volatility.

Consolidation among key upstream suppliers further risks pricing power and allocation constraints for Sumitomo in niche segments.

Supplier Power 2

Resource nationalism and geopolitics constrain supply and strengthen supplier bargaining positions. Export controls, royalties and local-content rules raise switching costs and renegotiation complexity. China accounted for about 60% of global rare-earth output in 2024, illustrating supplier concentration. Sumitomo's 2024 annual report emphasizes multi-region sourcing and political-risk management, yet sudden policy shifts can reprice contracts and timelines.

Supplier Power 3

Commodity price transparency limits opportunistic markups but scarcity premiums persist, with World Bank commodity price data showing industrial metals spot prices up about 10% in 2024 versus 2023. For specialized catalysts and high-spec alloys, supplier differentiation raises dependence as top-tier suppliers control technical IP and 20–30% of global niche capacity. Framework agreements and volume commitments have cut input volatility for Sumitomo peers by roughly 6% annually, while standardization and dual-sourcing steadily reduce long-term lock-in.

Supplier Power 4

ESG compliance tightens supplier criteria, shrinking the qualified pool and elevating supplier power; 2024 surveys showed roughly 70% of large buyers increased ESG demands, raising switching costs and premiums.

Traceability, emissions data and safety standards add audit burdens and CAPEX for suppliers, pushing up input costs and bargaining leverage.

Sumitomo’s stewardship programs (training, co-investment) can help upgrade suppliers and rebalance power, but ESG bottlenecks in early-stage chains remain a persistent pressure point.

- ESG demand spike — ~70% buyers (2024)

- Audit/CAPEX increase — higher supplier margins

- Sumitomo support — reduces upgrade time/cost

- Early-stage supplier gaps — ongoing risk

Supplier Power 5

Supplier Power 5: Advanced procurement analytics, digital marketplaces and logistics-visibility tools can boost negotiating leverage and are reported to improve procurement efficiency by about 10% in 2024, while inventory optimization and contractual optionality raise flexibility versus supply shocks. Physical constraints like port disruptions still can overpower data advantages, so strategic stockpiles and freight partnerships hedge residual risk.

- Procurement efficiency ~10% (2024)

- Inventory optionality reduces stockout risk

- Visibility tools cut lead-time variance

- Stockpiles + freight partners = residual risk hedge

Diversified sourcing eases vendor risk; rare-earth scarcity and China dominance lift supplier power

Sumitomo’s diversified supplier base, long-term offtakes and JVs limit single-vendor risk, yet critical-mineral scarcity and upstream consolidation raise supplier leverage. China supplied ~60% of rare-earths in 2024; industrial metals spot prices rose ~10% y/y (2024). ESG demands (~70% large buyers 2024) and niche IP (≈25% global niche capacity) sustain higher switching costs.

| Metric | 2024 |

|---|---|

| Rare-earth share (China) | 60% |

| Metals price change | +10% y/y |

| Buyers upping ESG | 70% |

| Niche supplier capacity | ≈25% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Sumitomo, examining competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and identifying disruptive trends, regulatory risks, and strategic levers to protect margins and guide growth—fully editable for integration into investor decks and strategy reports.

A concise Sumitomo-specific Five Forces one-sheet—instantly highlight supplier, buyer, and competitive pressures with an editable radar chart so teams can prioritize strategic responses and drop directly into board slides.

Customers Bargaining Power

Buyer Power 1

Large industrials, utilities and governments command volume and can negotiate aggressively, using sophisticated procurement and tender processes that increase price pressure. In 2024 benchmark publishers such as Platts and S&P Global continued daily spot/forward pricing, amplifying buyer leverage, while deep service relationships and bundling partially offset raw-price exposure.

Buyer Power 2

Sumitomo’s integrated offerings—financing, logistics, engineering support—raise switching costs for customers, with multi-year (typically 3–7 year) contracts and 99.5%+ performance SLAs embedding the company in operations. Tailored solutions reduce pure price comparability, while standardized commodities and spot services remain contestable.

Buyer Power 3

End-market cyclicality allows buyers to reopen terms in downturns, with IMF projecting global growth at 3.2% in 2024 so demand shocks are material. Inventory destocking and capex pauses compress margins across the chain as firms push for tighter payment and price concessions. Flexible pricing formulas and hedging pass-throughs shift part of commodity and FX risk back to buyers. Sumitomo’s diversified portfolio across energy, metals, and logistics buffers buyer-driven shocks.

Buyer Power 4

Digital procurement and e-auctions have driven transparency and competition—by 2024 over 50% of procurement teams deploy e-auctions, letting buyers unbundle services to cherry-pick lowest-cost components; Sumitomo counters by bundling harder-to-commoditize value-added services and using data-driven performance reporting, which the firm reports boosts renewal odds by about 12%.

- e-auctions: >50% adoption (2024)

- Unbundling risk: increased price shopping

- Defense: bundled value-added services

- Metric: ~12% higher renewals with bundles

Buyer Power 5

- Regulation: IMO 40% CII cut by 2030; EU ETS maritime in 2024

- Advantage: certified/LCAs = premium access, lower buyer leverage

- Risk: failure to meet thresholds = higher switching by buyers

Buyers volume leverage pressures commoditized services; bundled contracts and ESG premiums

Large buyers (industrials, utilities, governments) wield strong price leverage via volume, tenders and >50% e-auction adoption (2024), pressuring commoditized services.

Sumitomo mitigates through 3–7 year bundled contracts, integrated financing/logistics and 99.5%+ SLAs, raising switching costs and boosting renewals ~12%.

ESG rules (IMO CII −40% by 2030; EU ETS maritime 2024) create premium for compliant ports, reducing buyer price power for certified providers.

| Metric | 2024 Value | Impact |

|---|---|---|

| e-auction adoption | >50% | ↑ buyer leverage |

| Growth (IMF) | 3.2% | cyclicality |

| Renewal lift | ~12% | defense |

What You See Is What You Get

Sumitomo Porter's Five Forces Analysis

This Sumitomo Porter's Five Forces Analysis delivers a concise evaluation of industry rivalry, buyer and supplier power, threat of new entrants, and substitutes, tailored to Sumitomo's strategic position. The preview you see is the exact, fully formatted document you'll receive instantly after purchase—no placeholders, no mockups. Use it immediately for decision-making or reporting.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sumitomo’s Five Forces snapshot highlights strong supplier ties, diversified buyer segments, moderate threat of substitutes, and barriers shaped by capital intensity and regulation. This concise view reveals where competitive pressure is highest and where strategic advantage can be built. This preview only scratches the surface — unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Supplier Power 1

Sumitomo’s vast, diversified supplier network across metals, energy and chemicals reduces dependence on any single vendor, with long-term offtake, JV equity stakes and co-development deals aligning incentives and stabilizing contract terms.

Scarcity in critical minerals such as lithium, nickel and copper, however, can shift leverage to upstream owners, tightening access and raising spot volatility.

Consolidation among key upstream suppliers further risks pricing power and allocation constraints for Sumitomo in niche segments.

Supplier Power 2

Resource nationalism and geopolitics constrain supply and strengthen supplier bargaining positions. Export controls, royalties and local-content rules raise switching costs and renegotiation complexity. China accounted for about 60% of global rare-earth output in 2024, illustrating supplier concentration. Sumitomo's 2024 annual report emphasizes multi-region sourcing and political-risk management, yet sudden policy shifts can reprice contracts and timelines.

Supplier Power 3

Commodity price transparency limits opportunistic markups but scarcity premiums persist, with World Bank commodity price data showing industrial metals spot prices up about 10% in 2024 versus 2023. For specialized catalysts and high-spec alloys, supplier differentiation raises dependence as top-tier suppliers control technical IP and 20–30% of global niche capacity. Framework agreements and volume commitments have cut input volatility for Sumitomo peers by roughly 6% annually, while standardization and dual-sourcing steadily reduce long-term lock-in.

Supplier Power 4

ESG compliance tightens supplier criteria, shrinking the qualified pool and elevating supplier power; 2024 surveys showed roughly 70% of large buyers increased ESG demands, raising switching costs and premiums.

Traceability, emissions data and safety standards add audit burdens and CAPEX for suppliers, pushing up input costs and bargaining leverage.

Sumitomo’s stewardship programs (training, co-investment) can help upgrade suppliers and rebalance power, but ESG bottlenecks in early-stage chains remain a persistent pressure point.

- ESG demand spike — ~70% buyers (2024)

- Audit/CAPEX increase — higher supplier margins

- Sumitomo support — reduces upgrade time/cost

- Early-stage supplier gaps — ongoing risk

Supplier Power 5

Supplier Power 5: Advanced procurement analytics, digital marketplaces and logistics-visibility tools can boost negotiating leverage and are reported to improve procurement efficiency by about 10% in 2024, while inventory optimization and contractual optionality raise flexibility versus supply shocks. Physical constraints like port disruptions still can overpower data advantages, so strategic stockpiles and freight partnerships hedge residual risk.

- Procurement efficiency ~10% (2024)

- Inventory optionality reduces stockout risk

- Visibility tools cut lead-time variance

- Stockpiles + freight partners = residual risk hedge

Diversified sourcing eases vendor risk; rare-earth scarcity and China dominance lift supplier power

Sumitomo’s diversified supplier base, long-term offtakes and JVs limit single-vendor risk, yet critical-mineral scarcity and upstream consolidation raise supplier leverage. China supplied ~60% of rare-earths in 2024; industrial metals spot prices rose ~10% y/y (2024). ESG demands (~70% large buyers 2024) and niche IP (≈25% global niche capacity) sustain higher switching costs.

| Metric | 2024 |

|---|---|

| Rare-earth share (China) | 60% |

| Metals price change | +10% y/y |

| Buyers upping ESG | 70% |

| Niche supplier capacity | ≈25% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Sumitomo, examining competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and identifying disruptive trends, regulatory risks, and strategic levers to protect margins and guide growth—fully editable for integration into investor decks and strategy reports.

A concise Sumitomo-specific Five Forces one-sheet—instantly highlight supplier, buyer, and competitive pressures with an editable radar chart so teams can prioritize strategic responses and drop directly into board slides.

Customers Bargaining Power

Buyer Power 1

Large industrials, utilities and governments command volume and can negotiate aggressively, using sophisticated procurement and tender processes that increase price pressure. In 2024 benchmark publishers such as Platts and S&P Global continued daily spot/forward pricing, amplifying buyer leverage, while deep service relationships and bundling partially offset raw-price exposure.

Buyer Power 2

Sumitomo’s integrated offerings—financing, logistics, engineering support—raise switching costs for customers, with multi-year (typically 3–7 year) contracts and 99.5%+ performance SLAs embedding the company in operations. Tailored solutions reduce pure price comparability, while standardized commodities and spot services remain contestable.

Buyer Power 3

End-market cyclicality allows buyers to reopen terms in downturns, with IMF projecting global growth at 3.2% in 2024 so demand shocks are material. Inventory destocking and capex pauses compress margins across the chain as firms push for tighter payment and price concessions. Flexible pricing formulas and hedging pass-throughs shift part of commodity and FX risk back to buyers. Sumitomo’s diversified portfolio across energy, metals, and logistics buffers buyer-driven shocks.

Buyer Power 4

Digital procurement and e-auctions have driven transparency and competition—by 2024 over 50% of procurement teams deploy e-auctions, letting buyers unbundle services to cherry-pick lowest-cost components; Sumitomo counters by bundling harder-to-commoditize value-added services and using data-driven performance reporting, which the firm reports boosts renewal odds by about 12%.

- e-auctions: >50% adoption (2024)

- Unbundling risk: increased price shopping

- Defense: bundled value-added services

- Metric: ~12% higher renewals with bundles

Buyer Power 5

- Regulation: IMO 40% CII cut by 2030; EU ETS maritime in 2024

- Advantage: certified/LCAs = premium access, lower buyer leverage

- Risk: failure to meet thresholds = higher switching by buyers

Buyers volume leverage pressures commoditized services; bundled contracts and ESG premiums

Large buyers (industrials, utilities, governments) wield strong price leverage via volume, tenders and >50% e-auction adoption (2024), pressuring commoditized services.

Sumitomo mitigates through 3–7 year bundled contracts, integrated financing/logistics and 99.5%+ SLAs, raising switching costs and boosting renewals ~12%.

ESG rules (IMO CII −40% by 2030; EU ETS maritime 2024) create premium for compliant ports, reducing buyer price power for certified providers.

| Metric | 2024 Value | Impact |

|---|---|---|

| e-auction adoption | >50% | ↑ buyer leverage |

| Growth (IMF) | 3.2% | cyclicality |

| Renewal lift | ~12% | defense |

What You See Is What You Get

Sumitomo Porter's Five Forces Analysis

This Sumitomo Porter's Five Forces Analysis delivers a concise evaluation of industry rivalry, buyer and supplier power, threat of new entrants, and substitutes, tailored to Sumitomo's strategic position. The preview you see is the exact, fully formatted document you'll receive instantly after purchase—no placeholders, no mockups. Use it immediately for decision-making or reporting.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sumitomo’s Five Forces snapshot highlights strong supplier ties, diversified buyer segments, moderate threat of substitutes, and barriers shaped by capital intensity and regulation. This concise view reveals where competitive pressure is highest and where strategic advantage can be built. This preview only scratches the surface — unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Supplier Power 1

Sumitomo’s vast, diversified supplier network across metals, energy and chemicals reduces dependence on any single vendor, with long-term offtake, JV equity stakes and co-development deals aligning incentives and stabilizing contract terms.

Scarcity in critical minerals such as lithium, nickel and copper, however, can shift leverage to upstream owners, tightening access and raising spot volatility.

Consolidation among key upstream suppliers further risks pricing power and allocation constraints for Sumitomo in niche segments.

Supplier Power 2

Resource nationalism and geopolitics constrain supply and strengthen supplier bargaining positions. Export controls, royalties and local-content rules raise switching costs and renegotiation complexity. China accounted for about 60% of global rare-earth output in 2024, illustrating supplier concentration. Sumitomo's 2024 annual report emphasizes multi-region sourcing and political-risk management, yet sudden policy shifts can reprice contracts and timelines.

Supplier Power 3

Commodity price transparency limits opportunistic markups but scarcity premiums persist, with World Bank commodity price data showing industrial metals spot prices up about 10% in 2024 versus 2023. For specialized catalysts and high-spec alloys, supplier differentiation raises dependence as top-tier suppliers control technical IP and 20–30% of global niche capacity. Framework agreements and volume commitments have cut input volatility for Sumitomo peers by roughly 6% annually, while standardization and dual-sourcing steadily reduce long-term lock-in.

Supplier Power 4

ESG compliance tightens supplier criteria, shrinking the qualified pool and elevating supplier power; 2024 surveys showed roughly 70% of large buyers increased ESG demands, raising switching costs and premiums.

Traceability, emissions data and safety standards add audit burdens and CAPEX for suppliers, pushing up input costs and bargaining leverage.

Sumitomo’s stewardship programs (training, co-investment) can help upgrade suppliers and rebalance power, but ESG bottlenecks in early-stage chains remain a persistent pressure point.

- ESG demand spike — ~70% buyers (2024)

- Audit/CAPEX increase — higher supplier margins

- Sumitomo support — reduces upgrade time/cost

- Early-stage supplier gaps — ongoing risk

Supplier Power 5

Supplier Power 5: Advanced procurement analytics, digital marketplaces and logistics-visibility tools can boost negotiating leverage and are reported to improve procurement efficiency by about 10% in 2024, while inventory optimization and contractual optionality raise flexibility versus supply shocks. Physical constraints like port disruptions still can overpower data advantages, so strategic stockpiles and freight partnerships hedge residual risk.

- Procurement efficiency ~10% (2024)

- Inventory optionality reduces stockout risk

- Visibility tools cut lead-time variance

- Stockpiles + freight partners = residual risk hedge

Diversified sourcing eases vendor risk; rare-earth scarcity and China dominance lift supplier power

Sumitomo’s diversified supplier base, long-term offtakes and JVs limit single-vendor risk, yet critical-mineral scarcity and upstream consolidation raise supplier leverage. China supplied ~60% of rare-earths in 2024; industrial metals spot prices rose ~10% y/y (2024). ESG demands (~70% large buyers 2024) and niche IP (≈25% global niche capacity) sustain higher switching costs.

| Metric | 2024 |

|---|---|

| Rare-earth share (China) | 60% |

| Metals price change | +10% y/y |

| Buyers upping ESG | 70% |

| Niche supplier capacity | ≈25% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Sumitomo, examining competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and identifying disruptive trends, regulatory risks, and strategic levers to protect margins and guide growth—fully editable for integration into investor decks and strategy reports.

A concise Sumitomo-specific Five Forces one-sheet—instantly highlight supplier, buyer, and competitive pressures with an editable radar chart so teams can prioritize strategic responses and drop directly into board slides.

Customers Bargaining Power

Buyer Power 1

Large industrials, utilities and governments command volume and can negotiate aggressively, using sophisticated procurement and tender processes that increase price pressure. In 2024 benchmark publishers such as Platts and S&P Global continued daily spot/forward pricing, amplifying buyer leverage, while deep service relationships and bundling partially offset raw-price exposure.

Buyer Power 2

Sumitomo’s integrated offerings—financing, logistics, engineering support—raise switching costs for customers, with multi-year (typically 3–7 year) contracts and 99.5%+ performance SLAs embedding the company in operations. Tailored solutions reduce pure price comparability, while standardized commodities and spot services remain contestable.

Buyer Power 3

End-market cyclicality allows buyers to reopen terms in downturns, with IMF projecting global growth at 3.2% in 2024 so demand shocks are material. Inventory destocking and capex pauses compress margins across the chain as firms push for tighter payment and price concessions. Flexible pricing formulas and hedging pass-throughs shift part of commodity and FX risk back to buyers. Sumitomo’s diversified portfolio across energy, metals, and logistics buffers buyer-driven shocks.

Buyer Power 4

Digital procurement and e-auctions have driven transparency and competition—by 2024 over 50% of procurement teams deploy e-auctions, letting buyers unbundle services to cherry-pick lowest-cost components; Sumitomo counters by bundling harder-to-commoditize value-added services and using data-driven performance reporting, which the firm reports boosts renewal odds by about 12%.

- e-auctions: >50% adoption (2024)

- Unbundling risk: increased price shopping

- Defense: bundled value-added services

- Metric: ~12% higher renewals with bundles

Buyer Power 5

- Regulation: IMO 40% CII cut by 2030; EU ETS maritime in 2024

- Advantage: certified/LCAs = premium access, lower buyer leverage

- Risk: failure to meet thresholds = higher switching by buyers

Buyers volume leverage pressures commoditized services; bundled contracts and ESG premiums

Large buyers (industrials, utilities, governments) wield strong price leverage via volume, tenders and >50% e-auction adoption (2024), pressuring commoditized services.

Sumitomo mitigates through 3–7 year bundled contracts, integrated financing/logistics and 99.5%+ SLAs, raising switching costs and boosting renewals ~12%.

ESG rules (IMO CII −40% by 2030; EU ETS maritime 2024) create premium for compliant ports, reducing buyer price power for certified providers.

| Metric | 2024 Value | Impact |

|---|---|---|

| e-auction adoption | >50% | ↑ buyer leverage |

| Growth (IMF) | 3.2% | cyclicality |

| Renewal lift | ~12% | defense |

What You See Is What You Get

Sumitomo Porter's Five Forces Analysis

This Sumitomo Porter's Five Forces Analysis delivers a concise evaluation of industry rivalry, buyer and supplier power, threat of new entrants, and substitutes, tailored to Sumitomo's strategic position. The preview you see is the exact, fully formatted document you'll receive instantly after purchase—no placeholders, no mockups. Use it immediately for decision-making or reporting.