Suncor Energy Porter's Five Forces Analysis

From Overview to Strategy Blueprint

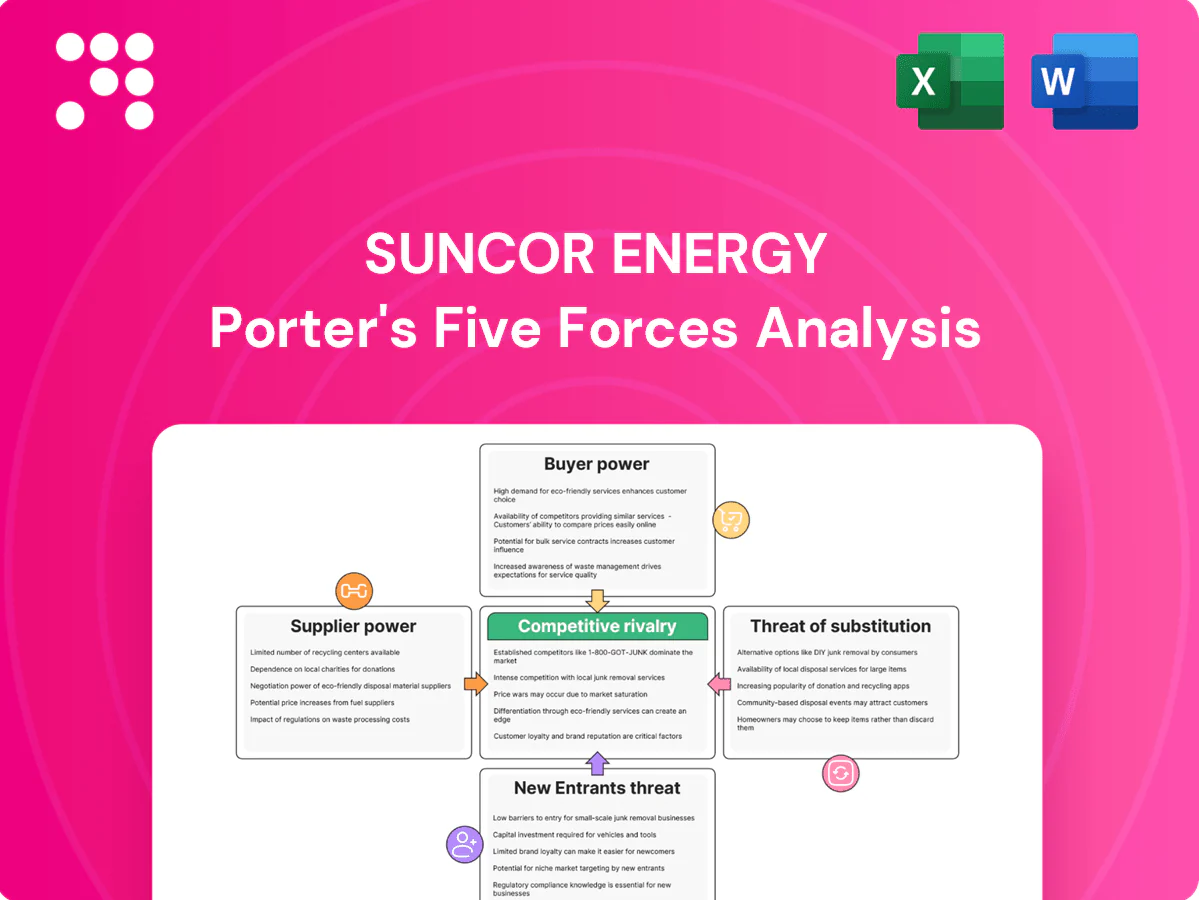

Suncor Energy faces intense rivalry from integrated oil majors and rising renewables, moderate supplier power from specialized oil sands inputs, and variable buyer power tied to commodity pricing and downstream integration. Regulatory and environmental pressures raise substitute threats and entry barriers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Suncor Energy’s competitive dynamics in detail.

Suppliers Bargaining Power

Critical inputs concentration

Suncor depends on specialized mining equipment, catalysts and diluent sourced from a concentrated set of global OEMs and chemical firms, with this supplier concentration evident as of 2024. That concentration gives suppliers leverage on pricing and lead times, though Suncor’s scale and multi-year contracts help cap price spikes and ensure supply. Vertical integration and disciplined inventory planning further reduce supplier power and operational disruption risk.

Midstream bottlenecks

Pipelines, storage and rail in Western Canada are episodically constrained—Enbridge Line 3 replacement restored about 760 kbpd but bottlenecks persist and Keystone is ~590 kbpd—giving midstream providers temporary leverage. Take‑or‑pay contracts and apportionment can raise delivered costs or limit optionality. Suncor mitigates risk via owned and contracted logistics plus refinery integration, yet regional crunches can still tighten supplier terms during peaks.

Labor and services

Skilled labor, maintenance contractors and turnaround services are scarce in oil sands cycles, boosting day rates and scheduling power for suppliers; union dynamics and remote-site premiums further strengthen supplier influence. By 2024 cyclical softening began to normalize rates, easing pressure. Suncor mitigates risk through workforce planning, multi-year framework agreements and expanded in-house capabilities.

Technology and chemicals

Proprietary extraction and upgrading technologies plus reliance on process chemicals such as hydrogen and solvents create switching frictions for Suncor, with vendor-specific performance clauses and warranties increasing supplier leverage.

Suncor reports ongoing supplier diversification and R&D investments in 2024 to reduce lock-in, while standardization efforts for non-core components curb single-supplier risks and improve bargaining position.

- Proprietary tech raises switching costs

- Vendor warranties increase dependency

- 2024 R&D and diversification mitigate lock-in

- Standardization reduces single-supplier leverage

Indigenous and regulatory stakeholders

Indigenous and regulatory stakeholders act like critical suppliers for Suncor by controlling land access, water rights and permits; their consent functions as a license to operate and can halt projects. Structured impact-benefit agreements and community partnerships align incentives, stabilize terms and reduce legal risk, while strong ESG performance cuts delays and opposition. Indigenous peoples represent about 5% of Canada’s population (2021 census), concentrating local influence.

- Consent = operational license

- Impact-benefit agreements stabilize terms

- Permitting bodies control key inputs

- ESG lowers project delays

Moderate supplier power amid concentrated OEMs and midstream bottlenecks

Supplier power is moderate: concentrated OEMs and chemical suppliers lift pricing and lead‑times, but Suncor’s scale, multi‑year contracts, vertical integration and 2024 R&D/diversification lessen risks; regional midstream bottlenecks (Line 3 ~760 kbpd restored, Keystone ~590 kbpd) and scarce skilled contractors still create episodic leverage.

| Factor | 2024 datapoint |

|---|---|

| Line 3 capacity | ~760 kbpd |

| Keystone | ~590 kbpd |

| Indigenous share (Canada) | ~5% (2021) |

What is included in the product

Tailored exclusively for Suncor Energy, this Porter's Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power affecting pricing and profitability, highlights entry barriers protecting incumbents, and identifies disruptive substitutes and emerging threats to market share.

A concise, one-sheet Porter's Five Forces for Suncor that relieves analysis bottlenecks—clarifying competitive pressures, regulatory risks, supplier power and buyer leverage for quick, board-ready decision-making.

Customers Bargaining Power

Commodity price transparency

In 2024 crude, refined products and petrochemicals continued to price off transparent benchmarks (Brent/WTI, gasoil, naphtha), giving buyers strong negotiating leverage. Limited differentiation in bulk fuels amplifies buyer power, compressing spreads for independent sellers. Suncor’s refinery integration and timing/quality optimization help capture downstream margins despite transparency. Active hedging and supply‑planning reduce volatility impacts on earnings.

Contract mix

Suncor sells through spot, term and offtake contracts, using mix to limit buyer leverage while maintaining flexibility. Large industrial and airline customers secure discounts and service commitments, especially on jet fuel and feedstock. Term deals and volume commitments reduce required price concessions, and a diversified customer and ~1,500‑site retail portfolio lowers exposure to any single buyer’s demands.

Petro-Canada retail

Petro-Canada's downstream retail network (over 1,400 stations in 2024) gives Suncor direct access to end customers, reducing wholesale buyer leverage. Loyalty programs and convenience offerings provide mild differentiation and higher basket spend. Pump prices remain locally benchmarked and highly competitive, limiting pricing power. Vertical integration lets Suncor retain retail margins through cycles.

Industrial/offtake buyers

Petrochemical and asphalt offtakers demand tight specs, creating customer stickiness, but abundant North American alternatives limit pricing power; Suncor’s 2024 downstream throughput capacity of about 435,000 barrels per day reinforces its reliability argument. Logistics performance and delivery consistency are primary negotiation levers, where Suncor’s multi-asset footprint and integrated supply chain strengthen bargaining position.

- Stickiness: spec-driven demand

- Alternatives: NA supply caps price

- Levers: reliability & logistics

- Suncor edge: ~435,000 bpd capacity (2024)

Switching costs and logistics

For bulk fuels, switching suppliers is relatively easy where logistics allow, strengthening buyer hand; in remote or pipeline‑tied markets logistics constraints reduce options and buyer power. Suncor leverages its Petro‑Canada retail network (~1,500 sites) and owned terminals to defend volumes, while freight economics often determine bargaining outcomes.

- Switching ease: higher in coastal/road-served markets

- Logistics lock: pipeline/remote markets reduce buyer power

- Suncor defense: owned terminals + ~1,500 Petro‑Canada sites

- Key driver: freight economics dictate delivered-cost bargaining

Refiner-retailer: moderate buyer power, ~1,500 sites, 435k bpd

Suncor faces moderate buyer power: transparent benchmark pricing and easy supplier switching in coastal/road markets strengthen buyers, while pipeline/remote logistics and long-term contracts limit it. Petro-Canada retail (~1,500 sites in 2024) and 435,000 bpd downstream capacity bolster Suncor’s leverage; large industrial/offtake customers still extract discounts via volume and spec demands.

| Metric | 2024 |

|---|---|

| Retail sites | ~1,500 |

| Downstream capacity | ~435,000 bpd |

Preview the Actual Deliverable

Suncor Energy Porter's Five Forces Analysis

This Suncor Energy Porter's Five Forces analysis provides a concise, professional assessment of competitive dynamics, supplier and buyer power, threat of substitutes, and industry rivalry. The document shown is the same professionally written analysis you'll receive—fully formatted and ready for immediate download after purchase.

From Overview to Strategy Blueprint

Suncor Energy faces intense rivalry from integrated oil majors and rising renewables, moderate supplier power from specialized oil sands inputs, and variable buyer power tied to commodity pricing and downstream integration. Regulatory and environmental pressures raise substitute threats and entry barriers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Suncor Energy’s competitive dynamics in detail.

Suppliers Bargaining Power

Critical inputs concentration

Suncor depends on specialized mining equipment, catalysts and diluent sourced from a concentrated set of global OEMs and chemical firms, with this supplier concentration evident as of 2024. That concentration gives suppliers leverage on pricing and lead times, though Suncor’s scale and multi-year contracts help cap price spikes and ensure supply. Vertical integration and disciplined inventory planning further reduce supplier power and operational disruption risk.

Midstream bottlenecks

Pipelines, storage and rail in Western Canada are episodically constrained—Enbridge Line 3 replacement restored about 760 kbpd but bottlenecks persist and Keystone is ~590 kbpd—giving midstream providers temporary leverage. Take‑or‑pay contracts and apportionment can raise delivered costs or limit optionality. Suncor mitigates risk via owned and contracted logistics plus refinery integration, yet regional crunches can still tighten supplier terms during peaks.

Labor and services

Skilled labor, maintenance contractors and turnaround services are scarce in oil sands cycles, boosting day rates and scheduling power for suppliers; union dynamics and remote-site premiums further strengthen supplier influence. By 2024 cyclical softening began to normalize rates, easing pressure. Suncor mitigates risk through workforce planning, multi-year framework agreements and expanded in-house capabilities.

Technology and chemicals

Proprietary extraction and upgrading technologies plus reliance on process chemicals such as hydrogen and solvents create switching frictions for Suncor, with vendor-specific performance clauses and warranties increasing supplier leverage.

Suncor reports ongoing supplier diversification and R&D investments in 2024 to reduce lock-in, while standardization efforts for non-core components curb single-supplier risks and improve bargaining position.

- Proprietary tech raises switching costs

- Vendor warranties increase dependency

- 2024 R&D and diversification mitigate lock-in

- Standardization reduces single-supplier leverage

Indigenous and regulatory stakeholders

Indigenous and regulatory stakeholders act like critical suppliers for Suncor by controlling land access, water rights and permits; their consent functions as a license to operate and can halt projects. Structured impact-benefit agreements and community partnerships align incentives, stabilize terms and reduce legal risk, while strong ESG performance cuts delays and opposition. Indigenous peoples represent about 5% of Canada’s population (2021 census), concentrating local influence.

- Consent = operational license

- Impact-benefit agreements stabilize terms

- Permitting bodies control key inputs

- ESG lowers project delays

Moderate supplier power amid concentrated OEMs and midstream bottlenecks

Supplier power is moderate: concentrated OEMs and chemical suppliers lift pricing and lead‑times, but Suncor’s scale, multi‑year contracts, vertical integration and 2024 R&D/diversification lessen risks; regional midstream bottlenecks (Line 3 ~760 kbpd restored, Keystone ~590 kbpd) and scarce skilled contractors still create episodic leverage.

| Factor | 2024 datapoint |

|---|---|

| Line 3 capacity | ~760 kbpd |

| Keystone | ~590 kbpd |

| Indigenous share (Canada) | ~5% (2021) |

What is included in the product

Tailored exclusively for Suncor Energy, this Porter's Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power affecting pricing and profitability, highlights entry barriers protecting incumbents, and identifies disruptive substitutes and emerging threats to market share.

A concise, one-sheet Porter's Five Forces for Suncor that relieves analysis bottlenecks—clarifying competitive pressures, regulatory risks, supplier power and buyer leverage for quick, board-ready decision-making.

Customers Bargaining Power

Commodity price transparency

In 2024 crude, refined products and petrochemicals continued to price off transparent benchmarks (Brent/WTI, gasoil, naphtha), giving buyers strong negotiating leverage. Limited differentiation in bulk fuels amplifies buyer power, compressing spreads for independent sellers. Suncor’s refinery integration and timing/quality optimization help capture downstream margins despite transparency. Active hedging and supply‑planning reduce volatility impacts on earnings.

Contract mix

Suncor sells through spot, term and offtake contracts, using mix to limit buyer leverage while maintaining flexibility. Large industrial and airline customers secure discounts and service commitments, especially on jet fuel and feedstock. Term deals and volume commitments reduce required price concessions, and a diversified customer and ~1,500‑site retail portfolio lowers exposure to any single buyer’s demands.

Petro-Canada retail

Petro-Canada's downstream retail network (over 1,400 stations in 2024) gives Suncor direct access to end customers, reducing wholesale buyer leverage. Loyalty programs and convenience offerings provide mild differentiation and higher basket spend. Pump prices remain locally benchmarked and highly competitive, limiting pricing power. Vertical integration lets Suncor retain retail margins through cycles.

Industrial/offtake buyers

Petrochemical and asphalt offtakers demand tight specs, creating customer stickiness, but abundant North American alternatives limit pricing power; Suncor’s 2024 downstream throughput capacity of about 435,000 barrels per day reinforces its reliability argument. Logistics performance and delivery consistency are primary negotiation levers, where Suncor’s multi-asset footprint and integrated supply chain strengthen bargaining position.

- Stickiness: spec-driven demand

- Alternatives: NA supply caps price

- Levers: reliability & logistics

- Suncor edge: ~435,000 bpd capacity (2024)

Switching costs and logistics

For bulk fuels, switching suppliers is relatively easy where logistics allow, strengthening buyer hand; in remote or pipeline‑tied markets logistics constraints reduce options and buyer power. Suncor leverages its Petro‑Canada retail network (~1,500 sites) and owned terminals to defend volumes, while freight economics often determine bargaining outcomes.

- Switching ease: higher in coastal/road-served markets

- Logistics lock: pipeline/remote markets reduce buyer power

- Suncor defense: owned terminals + ~1,500 Petro‑Canada sites

- Key driver: freight economics dictate delivered-cost bargaining

Refiner-retailer: moderate buyer power, ~1,500 sites, 435k bpd

Suncor faces moderate buyer power: transparent benchmark pricing and easy supplier switching in coastal/road markets strengthen buyers, while pipeline/remote logistics and long-term contracts limit it. Petro-Canada retail (~1,500 sites in 2024) and 435,000 bpd downstream capacity bolster Suncor’s leverage; large industrial/offtake customers still extract discounts via volume and spec demands.

| Metric | 2024 |

|---|---|

| Retail sites | ~1,500 |

| Downstream capacity | ~435,000 bpd |

Preview the Actual Deliverable

Suncor Energy Porter's Five Forces Analysis

This Suncor Energy Porter's Five Forces analysis provides a concise, professional assessment of competitive dynamics, supplier and buyer power, threat of substitutes, and industry rivalry. The document shown is the same professionally written analysis you'll receive—fully formatted and ready for immediate download after purchase.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Suncor Energy faces intense rivalry from integrated oil majors and rising renewables, moderate supplier power from specialized oil sands inputs, and variable buyer power tied to commodity pricing and downstream integration. Regulatory and environmental pressures raise substitute threats and entry barriers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Suncor Energy’s competitive dynamics in detail.

Suppliers Bargaining Power

Critical inputs concentration

Suncor depends on specialized mining equipment, catalysts and diluent sourced from a concentrated set of global OEMs and chemical firms, with this supplier concentration evident as of 2024. That concentration gives suppliers leverage on pricing and lead times, though Suncor’s scale and multi-year contracts help cap price spikes and ensure supply. Vertical integration and disciplined inventory planning further reduce supplier power and operational disruption risk.

Midstream bottlenecks

Pipelines, storage and rail in Western Canada are episodically constrained—Enbridge Line 3 replacement restored about 760 kbpd but bottlenecks persist and Keystone is ~590 kbpd—giving midstream providers temporary leverage. Take‑or‑pay contracts and apportionment can raise delivered costs or limit optionality. Suncor mitigates risk via owned and contracted logistics plus refinery integration, yet regional crunches can still tighten supplier terms during peaks.

Labor and services

Skilled labor, maintenance contractors and turnaround services are scarce in oil sands cycles, boosting day rates and scheduling power for suppliers; union dynamics and remote-site premiums further strengthen supplier influence. By 2024 cyclical softening began to normalize rates, easing pressure. Suncor mitigates risk through workforce planning, multi-year framework agreements and expanded in-house capabilities.

Technology and chemicals

Proprietary extraction and upgrading technologies plus reliance on process chemicals such as hydrogen and solvents create switching frictions for Suncor, with vendor-specific performance clauses and warranties increasing supplier leverage.

Suncor reports ongoing supplier diversification and R&D investments in 2024 to reduce lock-in, while standardization efforts for non-core components curb single-supplier risks and improve bargaining position.

- Proprietary tech raises switching costs

- Vendor warranties increase dependency

- 2024 R&D and diversification mitigate lock-in

- Standardization reduces single-supplier leverage

Indigenous and regulatory stakeholders

Indigenous and regulatory stakeholders act like critical suppliers for Suncor by controlling land access, water rights and permits; their consent functions as a license to operate and can halt projects. Structured impact-benefit agreements and community partnerships align incentives, stabilize terms and reduce legal risk, while strong ESG performance cuts delays and opposition. Indigenous peoples represent about 5% of Canada’s population (2021 census), concentrating local influence.

- Consent = operational license

- Impact-benefit agreements stabilize terms

- Permitting bodies control key inputs

- ESG lowers project delays

Moderate supplier power amid concentrated OEMs and midstream bottlenecks

Supplier power is moderate: concentrated OEMs and chemical suppliers lift pricing and lead‑times, but Suncor’s scale, multi‑year contracts, vertical integration and 2024 R&D/diversification lessen risks; regional midstream bottlenecks (Line 3 ~760 kbpd restored, Keystone ~590 kbpd) and scarce skilled contractors still create episodic leverage.

| Factor | 2024 datapoint |

|---|---|

| Line 3 capacity | ~760 kbpd |

| Keystone | ~590 kbpd |

| Indigenous share (Canada) | ~5% (2021) |

What is included in the product

Tailored exclusively for Suncor Energy, this Porter's Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power affecting pricing and profitability, highlights entry barriers protecting incumbents, and identifies disruptive substitutes and emerging threats to market share.

A concise, one-sheet Porter's Five Forces for Suncor that relieves analysis bottlenecks—clarifying competitive pressures, regulatory risks, supplier power and buyer leverage for quick, board-ready decision-making.

Customers Bargaining Power

Commodity price transparency

In 2024 crude, refined products and petrochemicals continued to price off transparent benchmarks (Brent/WTI, gasoil, naphtha), giving buyers strong negotiating leverage. Limited differentiation in bulk fuels amplifies buyer power, compressing spreads for independent sellers. Suncor’s refinery integration and timing/quality optimization help capture downstream margins despite transparency. Active hedging and supply‑planning reduce volatility impacts on earnings.

Contract mix

Suncor sells through spot, term and offtake contracts, using mix to limit buyer leverage while maintaining flexibility. Large industrial and airline customers secure discounts and service commitments, especially on jet fuel and feedstock. Term deals and volume commitments reduce required price concessions, and a diversified customer and ~1,500‑site retail portfolio lowers exposure to any single buyer’s demands.

Petro-Canada retail

Petro-Canada's downstream retail network (over 1,400 stations in 2024) gives Suncor direct access to end customers, reducing wholesale buyer leverage. Loyalty programs and convenience offerings provide mild differentiation and higher basket spend. Pump prices remain locally benchmarked and highly competitive, limiting pricing power. Vertical integration lets Suncor retain retail margins through cycles.

Industrial/offtake buyers

Petrochemical and asphalt offtakers demand tight specs, creating customer stickiness, but abundant North American alternatives limit pricing power; Suncor’s 2024 downstream throughput capacity of about 435,000 barrels per day reinforces its reliability argument. Logistics performance and delivery consistency are primary negotiation levers, where Suncor’s multi-asset footprint and integrated supply chain strengthen bargaining position.

- Stickiness: spec-driven demand

- Alternatives: NA supply caps price

- Levers: reliability & logistics

- Suncor edge: ~435,000 bpd capacity (2024)

Switching costs and logistics

For bulk fuels, switching suppliers is relatively easy where logistics allow, strengthening buyer hand; in remote or pipeline‑tied markets logistics constraints reduce options and buyer power. Suncor leverages its Petro‑Canada retail network (~1,500 sites) and owned terminals to defend volumes, while freight economics often determine bargaining outcomes.

- Switching ease: higher in coastal/road-served markets

- Logistics lock: pipeline/remote markets reduce buyer power

- Suncor defense: owned terminals + ~1,500 Petro‑Canada sites

- Key driver: freight economics dictate delivered-cost bargaining

Refiner-retailer: moderate buyer power, ~1,500 sites, 435k bpd

Suncor faces moderate buyer power: transparent benchmark pricing and easy supplier switching in coastal/road markets strengthen buyers, while pipeline/remote logistics and long-term contracts limit it. Petro-Canada retail (~1,500 sites in 2024) and 435,000 bpd downstream capacity bolster Suncor’s leverage; large industrial/offtake customers still extract discounts via volume and spec demands.

| Metric | 2024 |

|---|---|

| Retail sites | ~1,500 |

| Downstream capacity | ~435,000 bpd |

Preview the Actual Deliverable

Suncor Energy Porter's Five Forces Analysis

This Suncor Energy Porter's Five Forces analysis provides a concise, professional assessment of competitive dynamics, supplier and buyer power, threat of substitutes, and industry rivalry. The document shown is the same professionally written analysis you'll receive—fully formatted and ready for immediate download after purchase.