Sun Country Airlines PESTLE Analysis

Skip the Research. Get the Strategy.

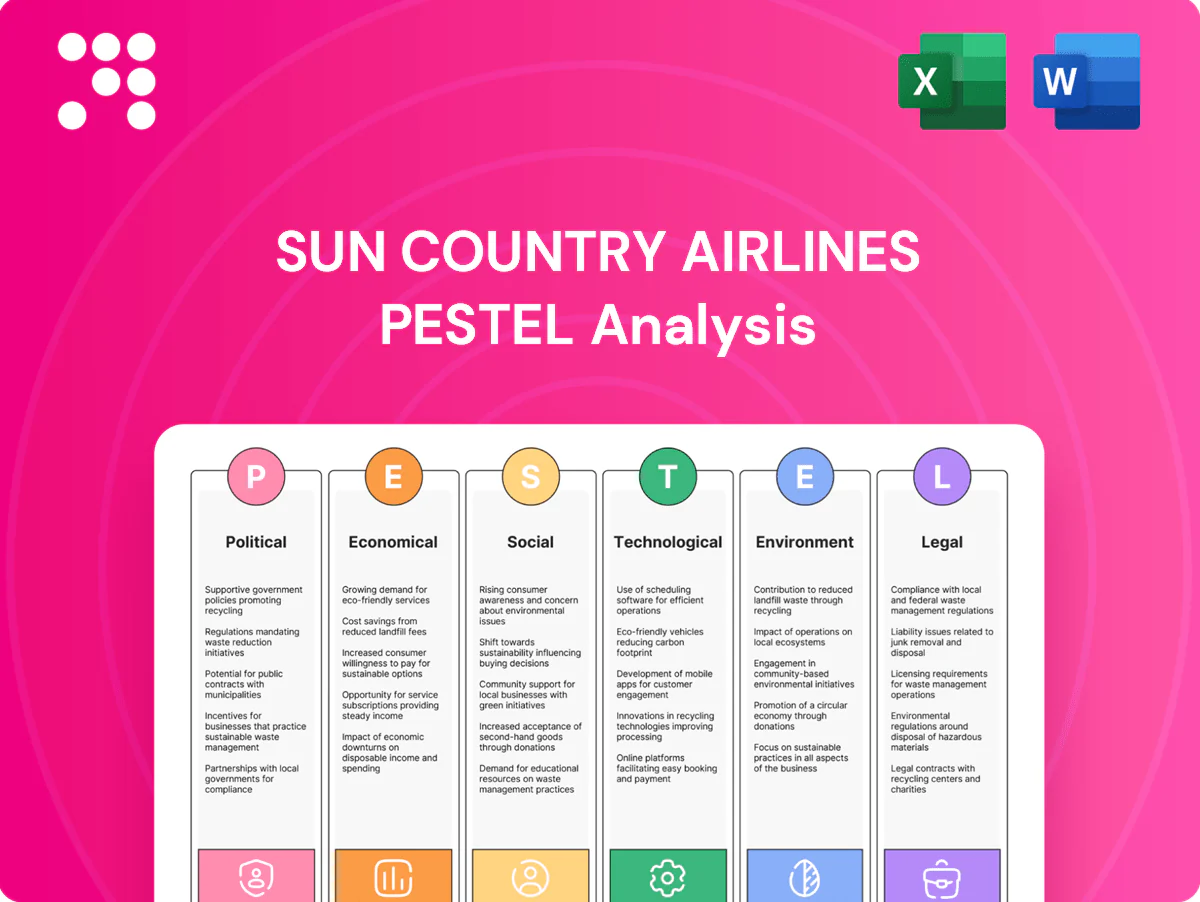

Unlock strategic clarity with our PESTLE Analysis of Sun Country Airlines—three to five expert-level insights into political, economic, social, technological, legal, and environmental forces shaping its future. Perfect for investors and strategists, the full report delivers actionable intelligence and editable files. Purchase now to get the complete, ready-to-use analysis instantly.

Political factors

Bilateral air agreements

Access to Mexico, Central America and Caribbean routes for Sun Country hinges on bilateral and Open Skies agreements—the US had over 120 Open Skies partners by 2024—so renegotiation can cap frequencies, gates or slots and directly reduce leisure seat capacity. Stable accords let Sun Country flex charters and seasonals to match peak demand, supporting higher unit revenues. Disruptions force redeployment to domestic sectors, compressing yields and increasing unit costs.

Cabotage and foreign ownership limits

US cabotage rules bar foreign airlines from operating domestic US flights, forcing Sun Country to design networks solely under US traffic rights. US law requires at least 75% voting control by US citizens, effectively capping foreign ownership at about 25% and limiting overseas strategic capital. These constraints preserve domestic focus but reduce cross-border integration options; charter growth must structure partnerships within those limits.

Aviation security mandates

TSA and DHS mandate programs such as Secure Flight that require passenger vetting and secondary screening, adding fixed time and operational cost per flight; enhanced screening for select geographies or threat alerts can lengthen turns and reduce aircraft utilization. Charters frequently face bespoke protocols — pre-cleared passenger lists, law‑enforcement escorts or K‑9 sweeps — increasing planning complexity and cost. Reliable compliance and low-security disruption rates serve as a measurable competitive differentiator for Sun Country when bidding charters and tight-turn schedules.

Geopolitical and travel advisories

Shifts in State Department advisories can quickly dampen leisure demand to Caribbean hotspots; NOAA's May 2024 outlook projected an above‑normal Atlantic season with 14–21 named storms, elevating cancellation risk. Political unrest or hurricane impacts drive re‑accommodation costs and lost yield; charter contracts often cover only portions of losses. Agile scheduling and targeted marketing are essential to backfill displaced demand and protect load factors.

- NOAA May 2024: 14–21 named storms

- Charters: partial revenue protection, not full

- Key response: agile schedule + targeted marketing

Airport access and slot constraints

Slot-controlled airports like LaGuardia and Reagan National (which enforces a 1,250-mile perimeter) constrain Sun Country’s growth despite leisure demand, while local regulators often favor incumbents or flag carriers, limiting new entrant access. Routing to secondary airports eases capacity but typically increases ground costs and can depress yields; charter flexibility helps bridge peak-season constraints.

- Reagan National perimeter: 1,250 miles

- Secondary airports: lower slots, higher costs

- Charters: seasonal capacity buffer, protects schedule

Open Skies risk: 120+ partners, 75% US control and 2024 storms threaten international capacity

Sun Country's international leisure capacity depends on Open Skies/bilateral accords (US had 120+ Open Skies partners by 2024), so renegotiation or limits can cut frequencies and yield. US cabotage and 75% US voting-control rule cap foreign investment and cross-border network integration. Security, State Dept advisories and NOAA's May 2024 14–21 named storms raise screening, disruption and re‑accommodation costs.

| Metric | Value |

|---|---|

| Open Skies partners (2024) | 120+ |

| US voting control | 75% minimum |

| NOAA May 2024 | 14–21 named storms |

| Reagan Natl perimeter | 1,250 miles |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Sun Country Airlines, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists preparing business plans, decks, or scenario strategies.

A concise, visually segmented PESTLE summary of Sun Country Airlines that simplifies external risks, regulatory and market impacts for quick meetings or slide decks, supports cross‑team alignment and planning, and is editable for region‑ or business‑specific notes.

Economic factors

Jet fuel price volatility

Fuel is a major cost driver for hybrid LCC Sun Country, with jet fuel representing about 24% of airline operating costs in 2024 (IATA); rapid moves in crack spreads can compress margins before fares adjust. Fuel surcharges are tougher on leisure, price-sensitive passengers and can suppress demand. As a result, hedging programs and fleet efficiency (younger, more fuel‑efficient narrowbodies) become pivotal to protect margins.

Leisure demand elasticity

Sun Country skews heavily to discretionary leisure travel, making demand highly price-sensitive; macro slowdowns, inflation, or falling household savings quickly depress loads. Promotions and ancillary upsells can recover volume but risk diluting yields. The airline’s charter business—tour and contract flying—provides counter-cyclical revenue stability during weaker leisure demand.

Seasonality and network utilization

In 2024 Sun Country's leisure-focused network showed pronounced winter peaks to sun destinations, driving uneven fleet utilization across quarters. Off-peak periods exert upward pressure on CASM unless aircraft are redeployed to cargo operations or ad hoc charters. Active dynamic capacity management and seasonal schedule adjustments help smooth revenue volatility, while contracted flying and cargo contracts raise asset productivity and lower idle time.

Labor market and pilot supply

Pilot scarcity raises wages and training costs across US carriers; Boeing 2024 Pilot & Technician Outlook projects about 118,000 North America pilot hires needed 2024–2043, while mandatory retirement at 65 and training pipeline limits tighten capacity. Efficient scheduling and retention at Sun Country can cut disruption, and charter premiums provide a revenue offset to cover labor inflation.

- 118,000 — Boeing 2024 North America pilot demand

- 65 — mandatory pilot retirement age

- 1,500 hrs — ATP requirement, training cost commonly ~$70k–$150k

- Charter premiums help offset higher wages

FX and cross-border spending

Sun Country earns the bulk of revenue in USD while key operating costs and demand drivers are tied to MXN and Central American currencies; USD/MXN was roughly 17.5 in mid‑2025, increasing exposure to peso moves. FX swings directly affect destination affordability for US travelers and can shift leisure demand seasonally. Vendor contracts abroad frequently reprice with local inflation (mid‑single digits in 2024–25), so balanced contracting and currency clauses mitigate volatility.

- Revenue currency: predominantly USD

- Cost/demand exposure: MXN + Central American currencies

- USD/MXN ~17.5 (mid‑2025)

- Local inflation: mid‑single digits (2024–25)

- Mitigation: balanced contracting, currency clauses

Open Skies risk: 120+ partners, 75% US control and 2024 storms threaten international capacity

Fuel ~24% of ops (IATA 2024); hedging and fuel‑efficient fleet key to margins.

Leisure demand is price‑sensitive; charters provide counter‑cyclical revenue.

Revenue USD vs MXN exposure (USD/MXN ~17.5 mid‑2025); pilot shortage (Boeing 118,000 N.A. hires 2024–2043) raises labor costs.

| Metric | Value |

|---|---|

| Fuel share | ~24% |

| USD/MXN | ~17.5 (mid‑2025) |

| Pilot demand | 118,000 (2024–2043) |

Preview the Actual Deliverable

Sun Country Airlines PESTLE Analysis

The Sun Country Airlines PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This file includes the complete political, economic, social, technological, legal, and environmental assessment as displayed, with no placeholders or teasers. After payment you’ll instantly download this same professionally structured report.

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Sun Country Airlines—three to five expert-level insights into political, economic, social, technological, legal, and environmental forces shaping its future. Perfect for investors and strategists, the full report delivers actionable intelligence and editable files. Purchase now to get the complete, ready-to-use analysis instantly.

Political factors

Bilateral air agreements

Access to Mexico, Central America and Caribbean routes for Sun Country hinges on bilateral and Open Skies agreements—the US had over 120 Open Skies partners by 2024—so renegotiation can cap frequencies, gates or slots and directly reduce leisure seat capacity. Stable accords let Sun Country flex charters and seasonals to match peak demand, supporting higher unit revenues. Disruptions force redeployment to domestic sectors, compressing yields and increasing unit costs.

Cabotage and foreign ownership limits

US cabotage rules bar foreign airlines from operating domestic US flights, forcing Sun Country to design networks solely under US traffic rights. US law requires at least 75% voting control by US citizens, effectively capping foreign ownership at about 25% and limiting overseas strategic capital. These constraints preserve domestic focus but reduce cross-border integration options; charter growth must structure partnerships within those limits.

Aviation security mandates

TSA and DHS mandate programs such as Secure Flight that require passenger vetting and secondary screening, adding fixed time and operational cost per flight; enhanced screening for select geographies or threat alerts can lengthen turns and reduce aircraft utilization. Charters frequently face bespoke protocols — pre-cleared passenger lists, law‑enforcement escorts or K‑9 sweeps — increasing planning complexity and cost. Reliable compliance and low-security disruption rates serve as a measurable competitive differentiator for Sun Country when bidding charters and tight-turn schedules.

Geopolitical and travel advisories

Shifts in State Department advisories can quickly dampen leisure demand to Caribbean hotspots; NOAA's May 2024 outlook projected an above‑normal Atlantic season with 14–21 named storms, elevating cancellation risk. Political unrest or hurricane impacts drive re‑accommodation costs and lost yield; charter contracts often cover only portions of losses. Agile scheduling and targeted marketing are essential to backfill displaced demand and protect load factors.

- NOAA May 2024: 14–21 named storms

- Charters: partial revenue protection, not full

- Key response: agile schedule + targeted marketing

Airport access and slot constraints

Slot-controlled airports like LaGuardia and Reagan National (which enforces a 1,250-mile perimeter) constrain Sun Country’s growth despite leisure demand, while local regulators often favor incumbents or flag carriers, limiting new entrant access. Routing to secondary airports eases capacity but typically increases ground costs and can depress yields; charter flexibility helps bridge peak-season constraints.

- Reagan National perimeter: 1,250 miles

- Secondary airports: lower slots, higher costs

- Charters: seasonal capacity buffer, protects schedule

Open Skies risk: 120+ partners, 75% US control and 2024 storms threaten international capacity

Sun Country's international leisure capacity depends on Open Skies/bilateral accords (US had 120+ Open Skies partners by 2024), so renegotiation or limits can cut frequencies and yield. US cabotage and 75% US voting-control rule cap foreign investment and cross-border network integration. Security, State Dept advisories and NOAA's May 2024 14–21 named storms raise screening, disruption and re‑accommodation costs.

| Metric | Value |

|---|---|

| Open Skies partners (2024) | 120+ |

| US voting control | 75% minimum |

| NOAA May 2024 | 14–21 named storms |

| Reagan Natl perimeter | 1,250 miles |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Sun Country Airlines, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists preparing business plans, decks, or scenario strategies.

A concise, visually segmented PESTLE summary of Sun Country Airlines that simplifies external risks, regulatory and market impacts for quick meetings or slide decks, supports cross‑team alignment and planning, and is editable for region‑ or business‑specific notes.

Economic factors

Jet fuel price volatility

Fuel is a major cost driver for hybrid LCC Sun Country, with jet fuel representing about 24% of airline operating costs in 2024 (IATA); rapid moves in crack spreads can compress margins before fares adjust. Fuel surcharges are tougher on leisure, price-sensitive passengers and can suppress demand. As a result, hedging programs and fleet efficiency (younger, more fuel‑efficient narrowbodies) become pivotal to protect margins.

Leisure demand elasticity

Sun Country skews heavily to discretionary leisure travel, making demand highly price-sensitive; macro slowdowns, inflation, or falling household savings quickly depress loads. Promotions and ancillary upsells can recover volume but risk diluting yields. The airline’s charter business—tour and contract flying—provides counter-cyclical revenue stability during weaker leisure demand.

Seasonality and network utilization

In 2024 Sun Country's leisure-focused network showed pronounced winter peaks to sun destinations, driving uneven fleet utilization across quarters. Off-peak periods exert upward pressure on CASM unless aircraft are redeployed to cargo operations or ad hoc charters. Active dynamic capacity management and seasonal schedule adjustments help smooth revenue volatility, while contracted flying and cargo contracts raise asset productivity and lower idle time.

Labor market and pilot supply

Pilot scarcity raises wages and training costs across US carriers; Boeing 2024 Pilot & Technician Outlook projects about 118,000 North America pilot hires needed 2024–2043, while mandatory retirement at 65 and training pipeline limits tighten capacity. Efficient scheduling and retention at Sun Country can cut disruption, and charter premiums provide a revenue offset to cover labor inflation.

- 118,000 — Boeing 2024 North America pilot demand

- 65 — mandatory pilot retirement age

- 1,500 hrs — ATP requirement, training cost commonly ~$70k–$150k

- Charter premiums help offset higher wages

FX and cross-border spending

Sun Country earns the bulk of revenue in USD while key operating costs and demand drivers are tied to MXN and Central American currencies; USD/MXN was roughly 17.5 in mid‑2025, increasing exposure to peso moves. FX swings directly affect destination affordability for US travelers and can shift leisure demand seasonally. Vendor contracts abroad frequently reprice with local inflation (mid‑single digits in 2024–25), so balanced contracting and currency clauses mitigate volatility.

- Revenue currency: predominantly USD

- Cost/demand exposure: MXN + Central American currencies

- USD/MXN ~17.5 (mid‑2025)

- Local inflation: mid‑single digits (2024–25)

- Mitigation: balanced contracting, currency clauses

Open Skies risk: 120+ partners, 75% US control and 2024 storms threaten international capacity

Fuel ~24% of ops (IATA 2024); hedging and fuel‑efficient fleet key to margins.

Leisure demand is price‑sensitive; charters provide counter‑cyclical revenue.

Revenue USD vs MXN exposure (USD/MXN ~17.5 mid‑2025); pilot shortage (Boeing 118,000 N.A. hires 2024–2043) raises labor costs.

| Metric | Value |

|---|---|

| Fuel share | ~24% |

| USD/MXN | ~17.5 (mid‑2025) |

| Pilot demand | 118,000 (2024–2043) |

Preview the Actual Deliverable

Sun Country Airlines PESTLE Analysis

The Sun Country Airlines PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This file includes the complete political, economic, social, technological, legal, and environmental assessment as displayed, with no placeholders or teasers. After payment you’ll instantly download this same professionally structured report.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Sun Country Airlines—three to five expert-level insights into political, economic, social, technological, legal, and environmental forces shaping its future. Perfect for investors and strategists, the full report delivers actionable intelligence and editable files. Purchase now to get the complete, ready-to-use analysis instantly.

Political factors

Bilateral air agreements

Access to Mexico, Central America and Caribbean routes for Sun Country hinges on bilateral and Open Skies agreements—the US had over 120 Open Skies partners by 2024—so renegotiation can cap frequencies, gates or slots and directly reduce leisure seat capacity. Stable accords let Sun Country flex charters and seasonals to match peak demand, supporting higher unit revenues. Disruptions force redeployment to domestic sectors, compressing yields and increasing unit costs.

Cabotage and foreign ownership limits

US cabotage rules bar foreign airlines from operating domestic US flights, forcing Sun Country to design networks solely under US traffic rights. US law requires at least 75% voting control by US citizens, effectively capping foreign ownership at about 25% and limiting overseas strategic capital. These constraints preserve domestic focus but reduce cross-border integration options; charter growth must structure partnerships within those limits.

Aviation security mandates

TSA and DHS mandate programs such as Secure Flight that require passenger vetting and secondary screening, adding fixed time and operational cost per flight; enhanced screening for select geographies or threat alerts can lengthen turns and reduce aircraft utilization. Charters frequently face bespoke protocols — pre-cleared passenger lists, law‑enforcement escorts or K‑9 sweeps — increasing planning complexity and cost. Reliable compliance and low-security disruption rates serve as a measurable competitive differentiator for Sun Country when bidding charters and tight-turn schedules.

Geopolitical and travel advisories

Shifts in State Department advisories can quickly dampen leisure demand to Caribbean hotspots; NOAA's May 2024 outlook projected an above‑normal Atlantic season with 14–21 named storms, elevating cancellation risk. Political unrest or hurricane impacts drive re‑accommodation costs and lost yield; charter contracts often cover only portions of losses. Agile scheduling and targeted marketing are essential to backfill displaced demand and protect load factors.

- NOAA May 2024: 14–21 named storms

- Charters: partial revenue protection, not full

- Key response: agile schedule + targeted marketing

Airport access and slot constraints

Slot-controlled airports like LaGuardia and Reagan National (which enforces a 1,250-mile perimeter) constrain Sun Country’s growth despite leisure demand, while local regulators often favor incumbents or flag carriers, limiting new entrant access. Routing to secondary airports eases capacity but typically increases ground costs and can depress yields; charter flexibility helps bridge peak-season constraints.

- Reagan National perimeter: 1,250 miles

- Secondary airports: lower slots, higher costs

- Charters: seasonal capacity buffer, protects schedule

Open Skies risk: 120+ partners, 75% US control and 2024 storms threaten international capacity

Sun Country's international leisure capacity depends on Open Skies/bilateral accords (US had 120+ Open Skies partners by 2024), so renegotiation or limits can cut frequencies and yield. US cabotage and 75% US voting-control rule cap foreign investment and cross-border network integration. Security, State Dept advisories and NOAA's May 2024 14–21 named storms raise screening, disruption and re‑accommodation costs.

| Metric | Value |

|---|---|

| Open Skies partners (2024) | 120+ |

| US voting control | 75% minimum |

| NOAA May 2024 | 14–21 named storms |

| Reagan Natl perimeter | 1,250 miles |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Sun Country Airlines, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists preparing business plans, decks, or scenario strategies.

A concise, visually segmented PESTLE summary of Sun Country Airlines that simplifies external risks, regulatory and market impacts for quick meetings or slide decks, supports cross‑team alignment and planning, and is editable for region‑ or business‑specific notes.

Economic factors

Jet fuel price volatility

Fuel is a major cost driver for hybrid LCC Sun Country, with jet fuel representing about 24% of airline operating costs in 2024 (IATA); rapid moves in crack spreads can compress margins before fares adjust. Fuel surcharges are tougher on leisure, price-sensitive passengers and can suppress demand. As a result, hedging programs and fleet efficiency (younger, more fuel‑efficient narrowbodies) become pivotal to protect margins.

Leisure demand elasticity

Sun Country skews heavily to discretionary leisure travel, making demand highly price-sensitive; macro slowdowns, inflation, or falling household savings quickly depress loads. Promotions and ancillary upsells can recover volume but risk diluting yields. The airline’s charter business—tour and contract flying—provides counter-cyclical revenue stability during weaker leisure demand.

Seasonality and network utilization

In 2024 Sun Country's leisure-focused network showed pronounced winter peaks to sun destinations, driving uneven fleet utilization across quarters. Off-peak periods exert upward pressure on CASM unless aircraft are redeployed to cargo operations or ad hoc charters. Active dynamic capacity management and seasonal schedule adjustments help smooth revenue volatility, while contracted flying and cargo contracts raise asset productivity and lower idle time.

Labor market and pilot supply

Pilot scarcity raises wages and training costs across US carriers; Boeing 2024 Pilot & Technician Outlook projects about 118,000 North America pilot hires needed 2024–2043, while mandatory retirement at 65 and training pipeline limits tighten capacity. Efficient scheduling and retention at Sun Country can cut disruption, and charter premiums provide a revenue offset to cover labor inflation.

- 118,000 — Boeing 2024 North America pilot demand

- 65 — mandatory pilot retirement age

- 1,500 hrs — ATP requirement, training cost commonly ~$70k–$150k

- Charter premiums help offset higher wages

FX and cross-border spending

Sun Country earns the bulk of revenue in USD while key operating costs and demand drivers are tied to MXN and Central American currencies; USD/MXN was roughly 17.5 in mid‑2025, increasing exposure to peso moves. FX swings directly affect destination affordability for US travelers and can shift leisure demand seasonally. Vendor contracts abroad frequently reprice with local inflation (mid‑single digits in 2024–25), so balanced contracting and currency clauses mitigate volatility.

- Revenue currency: predominantly USD

- Cost/demand exposure: MXN + Central American currencies

- USD/MXN ~17.5 (mid‑2025)

- Local inflation: mid‑single digits (2024–25)

- Mitigation: balanced contracting, currency clauses

Open Skies risk: 120+ partners, 75% US control and 2024 storms threaten international capacity

Fuel ~24% of ops (IATA 2024); hedging and fuel‑efficient fleet key to margins.

Leisure demand is price‑sensitive; charters provide counter‑cyclical revenue.

Revenue USD vs MXN exposure (USD/MXN ~17.5 mid‑2025); pilot shortage (Boeing 118,000 N.A. hires 2024–2043) raises labor costs.

| Metric | Value |

|---|---|

| Fuel share | ~24% |

| USD/MXN | ~17.5 (mid‑2025) |

| Pilot demand | 118,000 (2024–2043) |

Preview the Actual Deliverable

Sun Country Airlines PESTLE Analysis

The Sun Country Airlines PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This file includes the complete political, economic, social, technological, legal, and environmental assessment as displayed, with no placeholders or teasers. After payment you’ll instantly download this same professionally structured report.