Sundt Construction Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

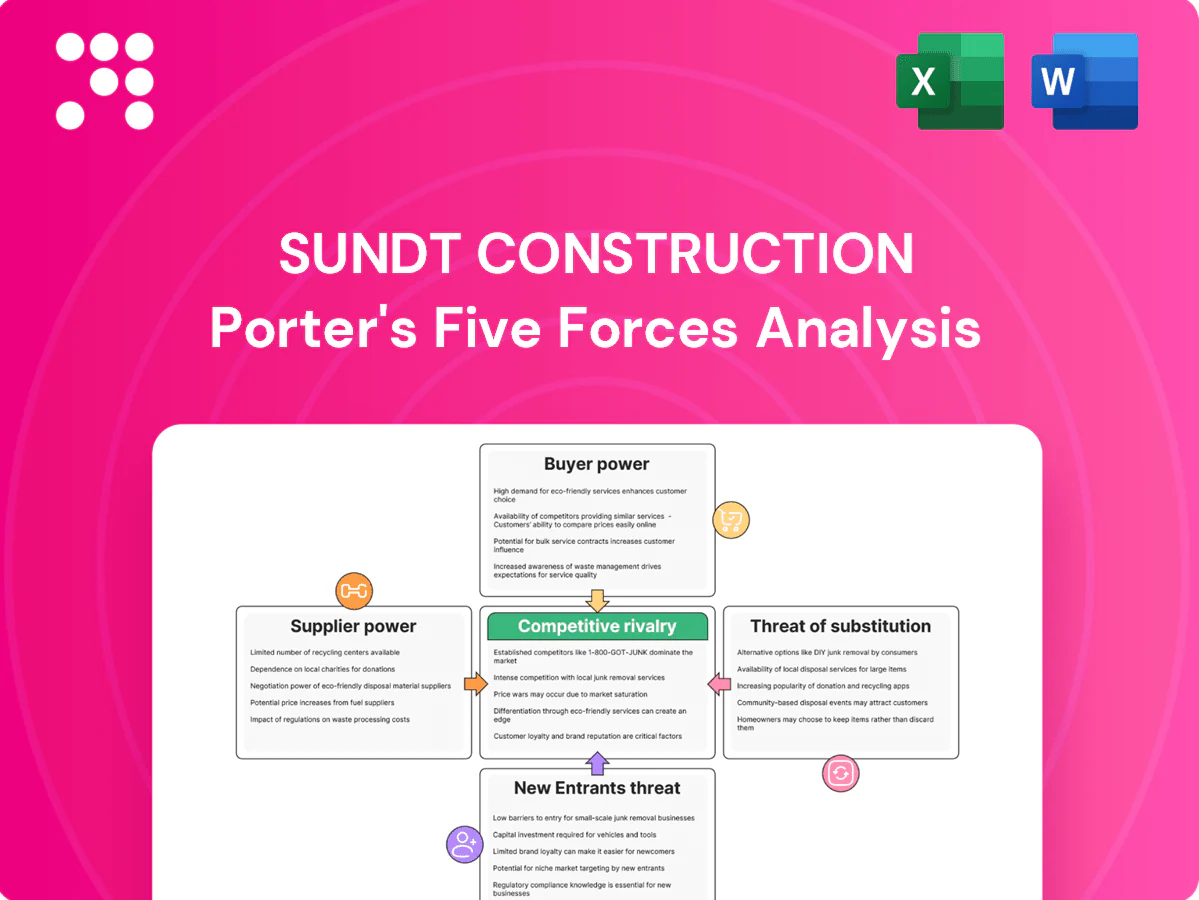

Sundt Construction faces moderate competitive intensity with strong project-level rivalry, significant buyer negotiation from large developers, concentrated supplier impacts on specialized materials, moderate threat of new entrants due to scale and bonding requirements, and low immediate substitute risk; this snapshot highlights key pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Critical materials volatility

Concrete, steel, asphalt and aggregates show high volatility—Brent crude averaged about $86/bbl in 2024, driving asphalt and energy-linked inputs higher while spot steel and aggregate indices swung materially, pressuring margins on fixed-price work. Suppliers typically pass through cost moves within 30–90 days, constraining Sundt on fixed contracts. Long-lead and specialty items often carry 15–25% price premia; hedging, escalators and early procurement mitigate but do not remove exposure.

Specialty subcontractor scarcity

Trades like electrical, mechanical and bridge work are capacity constrained and, per AGC 2024 survey, 79% of contractors reported difficulty hiring craft workers, letting top subs command premium pricing and preferential scheduling. Performance risk concentrates when only a few qualified firms exist, raising delay and warranty exposure. Prequalification and partner-of-choice programs have lowered subcontractor lead times and improved contract terms for Sundt.

Equipment and tech dependencies

Heavy equipment fleets and OEM parts give dealers/leasing firms leverage—aftermarket and parts scarcity can force concessions when uptime matters; BIM and project-management tool adoption exceeded 70% among large contractors by 2024, raising switching costs; downtime penalties (often contractual liquidated damages) amplify urgency and price flexibility; Sundt’s multi-vendor sourcing and owned-fleet strategies help rebalance supplier power.

Logistics and lead-time pressures

Transportation projects and remote sites magnify freight, crane time, and delivery risk, with 2024 industry reports noting persistent port congestion and permitting backlogs that tighten supplier control over schedules. Late deliveries trigger cascading cost impacts across labor, equipment idle time, and contract penalties; early buyout and integrated planning materially reduce exposure and stabilise margins.

- Freight & crane cost exposure

- Port/permitting schedule risk

- Cascading delay costs

- Mitigation: early buyout, integrated planning

Sustainability and compliance inputs

Sustainability and compliance inputs raise supplier leverage for Sundt as low-carbon materials, EPDs and expanded Buy America requirements narrow qualified sources and raise documentation burdens. Mandatory testing and certifications intensify supplier influence while renewable and industrial clients specify tighter performance limits that reduce substitutes. Strategic sourcing and supplier development are critical to preserve options and manage costs.

- Low-carbon materials narrow supplier pool

- EPDs and testing increase supplier influence

- Buy America limits imports for federally funded projects

- Strategic sourcing offsets concentration risk

Construction margins squeezed: Brent $86, craft shortages 79%, long-lead premia 15–25%

Input volatility (Brent $86/bbl in 2024) and 30–90 day supplier pass-throughs compress margins on fixed-price work. AGC 2024: 79% report craft shortages, letting subs charge premiums; long‑lead/specialty items carry 15–25% price premia. Owned fleet, early buyout and partner programs reduce leverage, but Buy America and low‑carbon specs concentrate suppliers.

| Metric | 2024 | Impact |

|---|---|---|

| Brent | $86/bbl | Higher asphalt/energy costs |

| Craft shortage | 79% contractors | Sub premiums/scheduling |

| Long‑lead premia | 15–25% | Margin pressure |

What is included in the product

Uncovers key competitive drivers—supplier and buyer power, rivalry, entry barriers, and substitutes—shaping Sundt Construction's profitability and pricing power. Identifies emerging threats and strategic levers to defend market share and inform investor or management decisions.

One-sheet Porter's Five Forces for Sundt Construction—quickly spot competitive pressure and risks; customize force levels with current bids, regulation shifts, or supplier data for instant scenario comparisons.

Customers Bargaining Power

Large institutional buyers

Public agencies and Fortune 500 owners bundle sizable scopes with stringent procurement rules, and in 2024 U.S. public construction spending remained near $430B, concentrating buying power among a few large owners. Their scale drives pricing pressure and owner-favorable contract terms, forcing Sundt to accept tighter margins. Competitive bidding compresses margins further, so differentiation through safety, quality, and on-time delivery is essential to win and protect profit.

Design-build and CMAR leverage

Alternative delivery (design-build, CMAR) lets owners evaluate best value beyond low bid, and sophisticated buyers increasingly use target value design and open-book accounting to negotiate down costs. Risk-sharing clauses and contingent pricing shift cost exposure to contractors, pressuring margins. Strong preconstruction services and detailed cost modeling can rebalance bargaining power by revealing real trade-offs and reducing information asymmetry. For Sundt, excelling in preconstruction and transparent cost control is central to defending margin under these owner-driven dynamics.

Project concentration and pipelines

Transportation, industrial and renewable clients often control multi-year programs, and in 2024 these sectors continued to drive large framework tenders that can span 3–7 years. Winning access frequently requires concessions on fees and staffing levels, increasing bargaining power of customers. Repeat work raises dependence on a few key accounts, while account diversification and framework agreements help stabilize contract terms and margins.

Specification tightness and change control

Detailed specifications and aggressive 2024 schedules limit Sundt’s contractor flexibility, as owners’ PM teams enforce liquidated damages and scrutinize change orders, narrowing mid-project pricing discretion.

- Scope clarity protects margin

- Collaborative planning reduces disputes

- Owner enforcement increases contract risk

Reputation and past performance data

Public scorecards such as CPARS and safety metrics (EMR, OSHA rates) are routinely used in award decisions, forcing buyers to compare contractors on cost, quality and claims history. Transparency from these metrics reduces the ability to charge premiums absent clear differentiation, while consistent KPI outperformance (safety, schedule, quality) materially improves Sundt’s negotiating leverage.

- CPARS and EMR referenced in federal/state awards

- Buyers benchmark cost, quality, claims

- Transparency compresses premium room

- Consistent KPI wins raise bargaining power

~$430B public spend and 3-7yr frameworks boost owner leverage; CPARS/EMR wins restore firm clout

Large public/Fortune 500 owners concentrated ~$430B public construction spend in 2024, driving price pressure and owner-favorable terms. Alternative delivery and open-book practices shift risk to contractors, while multi-year frameworks (3–7 yrs) increase client leverage. Strong preconstruction, safety (EMR) and CPARS outperformance materially restores Sundt’s negotiating power.

| Metric | 2024 | Impact |

|---|---|---|

| Public spend | $430B | Concentrated buying |

| Framework length | 3–7 yrs | Higher dependence |

| KPIs | CPARS/EMR | Leverage if strong |

Full Version Awaits

Sundt Construction Porter's Five Forces Analysis

This preview shows the exact Sundt Construction Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full, professionally formatted document is ready for download and immediate use upon payment. What you see is what you get.

A Must-Have Tool for Decision-Makers

Sundt Construction faces moderate competitive intensity with strong project-level rivalry, significant buyer negotiation from large developers, concentrated supplier impacts on specialized materials, moderate threat of new entrants due to scale and bonding requirements, and low immediate substitute risk; this snapshot highlights key pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Critical materials volatility

Concrete, steel, asphalt and aggregates show high volatility—Brent crude averaged about $86/bbl in 2024, driving asphalt and energy-linked inputs higher while spot steel and aggregate indices swung materially, pressuring margins on fixed-price work. Suppliers typically pass through cost moves within 30–90 days, constraining Sundt on fixed contracts. Long-lead and specialty items often carry 15–25% price premia; hedging, escalators and early procurement mitigate but do not remove exposure.

Specialty subcontractor scarcity

Trades like electrical, mechanical and bridge work are capacity constrained and, per AGC 2024 survey, 79% of contractors reported difficulty hiring craft workers, letting top subs command premium pricing and preferential scheduling. Performance risk concentrates when only a few qualified firms exist, raising delay and warranty exposure. Prequalification and partner-of-choice programs have lowered subcontractor lead times and improved contract terms for Sundt.

Equipment and tech dependencies

Heavy equipment fleets and OEM parts give dealers/leasing firms leverage—aftermarket and parts scarcity can force concessions when uptime matters; BIM and project-management tool adoption exceeded 70% among large contractors by 2024, raising switching costs; downtime penalties (often contractual liquidated damages) amplify urgency and price flexibility; Sundt’s multi-vendor sourcing and owned-fleet strategies help rebalance supplier power.

Logistics and lead-time pressures

Transportation projects and remote sites magnify freight, crane time, and delivery risk, with 2024 industry reports noting persistent port congestion and permitting backlogs that tighten supplier control over schedules. Late deliveries trigger cascading cost impacts across labor, equipment idle time, and contract penalties; early buyout and integrated planning materially reduce exposure and stabilise margins.

- Freight & crane cost exposure

- Port/permitting schedule risk

- Cascading delay costs

- Mitigation: early buyout, integrated planning

Sustainability and compliance inputs

Sustainability and compliance inputs raise supplier leverage for Sundt as low-carbon materials, EPDs and expanded Buy America requirements narrow qualified sources and raise documentation burdens. Mandatory testing and certifications intensify supplier influence while renewable and industrial clients specify tighter performance limits that reduce substitutes. Strategic sourcing and supplier development are critical to preserve options and manage costs.

- Low-carbon materials narrow supplier pool

- EPDs and testing increase supplier influence

- Buy America limits imports for federally funded projects

- Strategic sourcing offsets concentration risk

Construction margins squeezed: Brent $86, craft shortages 79%, long-lead premia 15–25%

Input volatility (Brent $86/bbl in 2024) and 30–90 day supplier pass-throughs compress margins on fixed-price work. AGC 2024: 79% report craft shortages, letting subs charge premiums; long‑lead/specialty items carry 15–25% price premia. Owned fleet, early buyout and partner programs reduce leverage, but Buy America and low‑carbon specs concentrate suppliers.

| Metric | 2024 | Impact |

|---|---|---|

| Brent | $86/bbl | Higher asphalt/energy costs |

| Craft shortage | 79% contractors | Sub premiums/scheduling |

| Long‑lead premia | 15–25% | Margin pressure |

What is included in the product

Uncovers key competitive drivers—supplier and buyer power, rivalry, entry barriers, and substitutes—shaping Sundt Construction's profitability and pricing power. Identifies emerging threats and strategic levers to defend market share and inform investor or management decisions.

One-sheet Porter's Five Forces for Sundt Construction—quickly spot competitive pressure and risks; customize force levels with current bids, regulation shifts, or supplier data for instant scenario comparisons.

Customers Bargaining Power

Large institutional buyers

Public agencies and Fortune 500 owners bundle sizable scopes with stringent procurement rules, and in 2024 U.S. public construction spending remained near $430B, concentrating buying power among a few large owners. Their scale drives pricing pressure and owner-favorable contract terms, forcing Sundt to accept tighter margins. Competitive bidding compresses margins further, so differentiation through safety, quality, and on-time delivery is essential to win and protect profit.

Design-build and CMAR leverage

Alternative delivery (design-build, CMAR) lets owners evaluate best value beyond low bid, and sophisticated buyers increasingly use target value design and open-book accounting to negotiate down costs. Risk-sharing clauses and contingent pricing shift cost exposure to contractors, pressuring margins. Strong preconstruction services and detailed cost modeling can rebalance bargaining power by revealing real trade-offs and reducing information asymmetry. For Sundt, excelling in preconstruction and transparent cost control is central to defending margin under these owner-driven dynamics.

Project concentration and pipelines

Transportation, industrial and renewable clients often control multi-year programs, and in 2024 these sectors continued to drive large framework tenders that can span 3–7 years. Winning access frequently requires concessions on fees and staffing levels, increasing bargaining power of customers. Repeat work raises dependence on a few key accounts, while account diversification and framework agreements help stabilize contract terms and margins.

Specification tightness and change control

Detailed specifications and aggressive 2024 schedules limit Sundt’s contractor flexibility, as owners’ PM teams enforce liquidated damages and scrutinize change orders, narrowing mid-project pricing discretion.

- Scope clarity protects margin

- Collaborative planning reduces disputes

- Owner enforcement increases contract risk

Reputation and past performance data

Public scorecards such as CPARS and safety metrics (EMR, OSHA rates) are routinely used in award decisions, forcing buyers to compare contractors on cost, quality and claims history. Transparency from these metrics reduces the ability to charge premiums absent clear differentiation, while consistent KPI outperformance (safety, schedule, quality) materially improves Sundt’s negotiating leverage.

- CPARS and EMR referenced in federal/state awards

- Buyers benchmark cost, quality, claims

- Transparency compresses premium room

- Consistent KPI wins raise bargaining power

~$430B public spend and 3-7yr frameworks boost owner leverage; CPARS/EMR wins restore firm clout

Large public/Fortune 500 owners concentrated ~$430B public construction spend in 2024, driving price pressure and owner-favorable terms. Alternative delivery and open-book practices shift risk to contractors, while multi-year frameworks (3–7 yrs) increase client leverage. Strong preconstruction, safety (EMR) and CPARS outperformance materially restores Sundt’s negotiating power.

| Metric | 2024 | Impact |

|---|---|---|

| Public spend | $430B | Concentrated buying |

| Framework length | 3–7 yrs | Higher dependence |

| KPIs | CPARS/EMR | Leverage if strong |

Full Version Awaits

Sundt Construction Porter's Five Forces Analysis

This preview shows the exact Sundt Construction Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full, professionally formatted document is ready for download and immediate use upon payment. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Sundt Construction faces moderate competitive intensity with strong project-level rivalry, significant buyer negotiation from large developers, concentrated supplier impacts on specialized materials, moderate threat of new entrants due to scale and bonding requirements, and low immediate substitute risk; this snapshot highlights key pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Critical materials volatility

Concrete, steel, asphalt and aggregates show high volatility—Brent crude averaged about $86/bbl in 2024, driving asphalt and energy-linked inputs higher while spot steel and aggregate indices swung materially, pressuring margins on fixed-price work. Suppliers typically pass through cost moves within 30–90 days, constraining Sundt on fixed contracts. Long-lead and specialty items often carry 15–25% price premia; hedging, escalators and early procurement mitigate but do not remove exposure.

Specialty subcontractor scarcity

Trades like electrical, mechanical and bridge work are capacity constrained and, per AGC 2024 survey, 79% of contractors reported difficulty hiring craft workers, letting top subs command premium pricing and preferential scheduling. Performance risk concentrates when only a few qualified firms exist, raising delay and warranty exposure. Prequalification and partner-of-choice programs have lowered subcontractor lead times and improved contract terms for Sundt.

Equipment and tech dependencies

Heavy equipment fleets and OEM parts give dealers/leasing firms leverage—aftermarket and parts scarcity can force concessions when uptime matters; BIM and project-management tool adoption exceeded 70% among large contractors by 2024, raising switching costs; downtime penalties (often contractual liquidated damages) amplify urgency and price flexibility; Sundt’s multi-vendor sourcing and owned-fleet strategies help rebalance supplier power.

Logistics and lead-time pressures

Transportation projects and remote sites magnify freight, crane time, and delivery risk, with 2024 industry reports noting persistent port congestion and permitting backlogs that tighten supplier control over schedules. Late deliveries trigger cascading cost impacts across labor, equipment idle time, and contract penalties; early buyout and integrated planning materially reduce exposure and stabilise margins.

- Freight & crane cost exposure

- Port/permitting schedule risk

- Cascading delay costs

- Mitigation: early buyout, integrated planning

Sustainability and compliance inputs

Sustainability and compliance inputs raise supplier leverage for Sundt as low-carbon materials, EPDs and expanded Buy America requirements narrow qualified sources and raise documentation burdens. Mandatory testing and certifications intensify supplier influence while renewable and industrial clients specify tighter performance limits that reduce substitutes. Strategic sourcing and supplier development are critical to preserve options and manage costs.

- Low-carbon materials narrow supplier pool

- EPDs and testing increase supplier influence

- Buy America limits imports for federally funded projects

- Strategic sourcing offsets concentration risk

Construction margins squeezed: Brent $86, craft shortages 79%, long-lead premia 15–25%

Input volatility (Brent $86/bbl in 2024) and 30–90 day supplier pass-throughs compress margins on fixed-price work. AGC 2024: 79% report craft shortages, letting subs charge premiums; long‑lead/specialty items carry 15–25% price premia. Owned fleet, early buyout and partner programs reduce leverage, but Buy America and low‑carbon specs concentrate suppliers.

| Metric | 2024 | Impact |

|---|---|---|

| Brent | $86/bbl | Higher asphalt/energy costs |

| Craft shortage | 79% contractors | Sub premiums/scheduling |

| Long‑lead premia | 15–25% | Margin pressure |

What is included in the product

Uncovers key competitive drivers—supplier and buyer power, rivalry, entry barriers, and substitutes—shaping Sundt Construction's profitability and pricing power. Identifies emerging threats and strategic levers to defend market share and inform investor or management decisions.

One-sheet Porter's Five Forces for Sundt Construction—quickly spot competitive pressure and risks; customize force levels with current bids, regulation shifts, or supplier data for instant scenario comparisons.

Customers Bargaining Power

Large institutional buyers

Public agencies and Fortune 500 owners bundle sizable scopes with stringent procurement rules, and in 2024 U.S. public construction spending remained near $430B, concentrating buying power among a few large owners. Their scale drives pricing pressure and owner-favorable contract terms, forcing Sundt to accept tighter margins. Competitive bidding compresses margins further, so differentiation through safety, quality, and on-time delivery is essential to win and protect profit.

Design-build and CMAR leverage

Alternative delivery (design-build, CMAR) lets owners evaluate best value beyond low bid, and sophisticated buyers increasingly use target value design and open-book accounting to negotiate down costs. Risk-sharing clauses and contingent pricing shift cost exposure to contractors, pressuring margins. Strong preconstruction services and detailed cost modeling can rebalance bargaining power by revealing real trade-offs and reducing information asymmetry. For Sundt, excelling in preconstruction and transparent cost control is central to defending margin under these owner-driven dynamics.

Project concentration and pipelines

Transportation, industrial and renewable clients often control multi-year programs, and in 2024 these sectors continued to drive large framework tenders that can span 3–7 years. Winning access frequently requires concessions on fees and staffing levels, increasing bargaining power of customers. Repeat work raises dependence on a few key accounts, while account diversification and framework agreements help stabilize contract terms and margins.

Specification tightness and change control

Detailed specifications and aggressive 2024 schedules limit Sundt’s contractor flexibility, as owners’ PM teams enforce liquidated damages and scrutinize change orders, narrowing mid-project pricing discretion.

- Scope clarity protects margin

- Collaborative planning reduces disputes

- Owner enforcement increases contract risk

Reputation and past performance data

Public scorecards such as CPARS and safety metrics (EMR, OSHA rates) are routinely used in award decisions, forcing buyers to compare contractors on cost, quality and claims history. Transparency from these metrics reduces the ability to charge premiums absent clear differentiation, while consistent KPI outperformance (safety, schedule, quality) materially improves Sundt’s negotiating leverage.

- CPARS and EMR referenced in federal/state awards

- Buyers benchmark cost, quality, claims

- Transparency compresses premium room

- Consistent KPI wins raise bargaining power

~$430B public spend and 3-7yr frameworks boost owner leverage; CPARS/EMR wins restore firm clout

Large public/Fortune 500 owners concentrated ~$430B public construction spend in 2024, driving price pressure and owner-favorable terms. Alternative delivery and open-book practices shift risk to contractors, while multi-year frameworks (3–7 yrs) increase client leverage. Strong preconstruction, safety (EMR) and CPARS outperformance materially restores Sundt’s negotiating power.

| Metric | 2024 | Impact |

|---|---|---|

| Public spend | $430B | Concentrated buying |

| Framework length | 3–7 yrs | Higher dependence |

| KPIs | CPARS/EMR | Leverage if strong |

Full Version Awaits

Sundt Construction Porter's Five Forces Analysis

This preview shows the exact Sundt Construction Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full, professionally formatted document is ready for download and immediate use upon payment. What you see is what you get.