Sun Pharma Industries Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

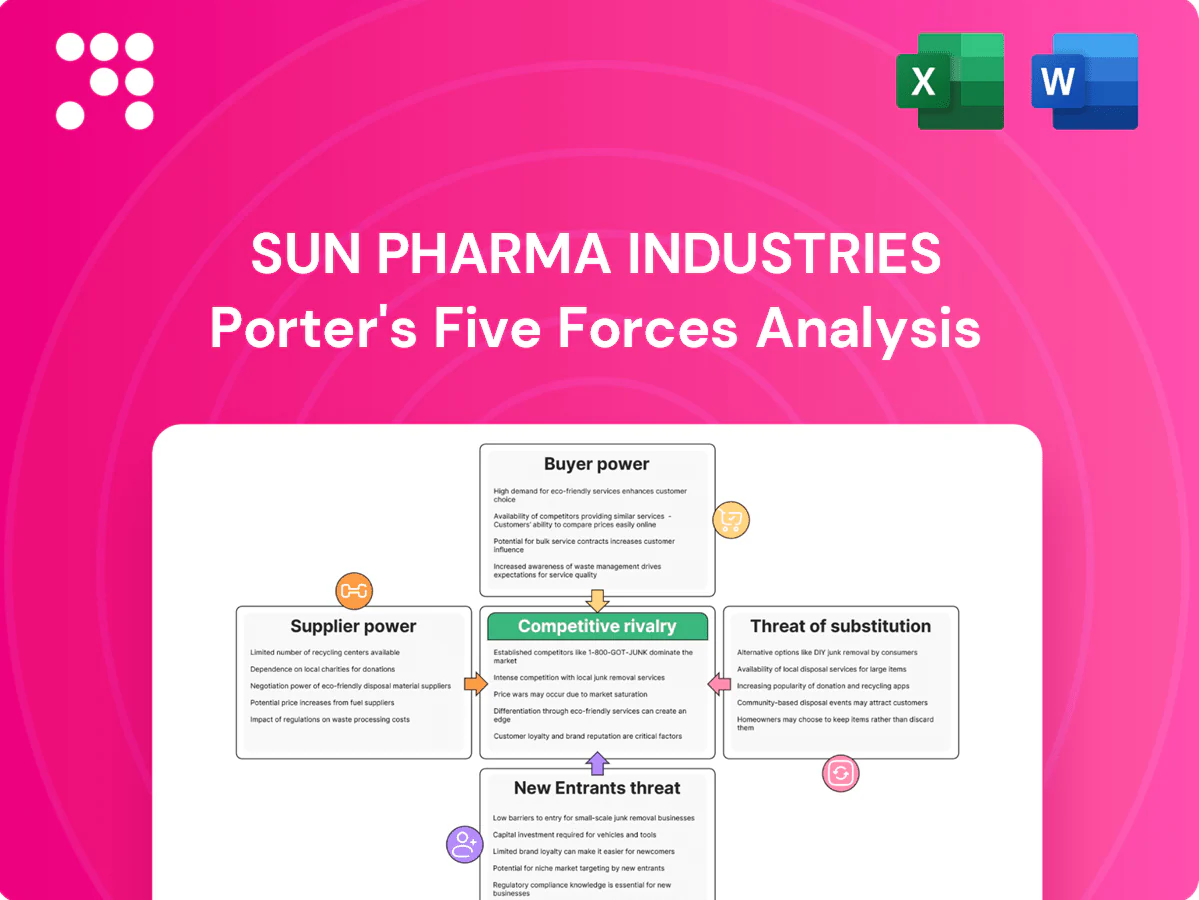

Sun Pharma faces intense competitive rivalry from global generics and branded peers, pricing pressure and regulatory risk, with moderate supplier power, strong buyer leverage, and limited threat from new entrants due to scale and regulation; substitutes remain a manageable concern. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sun Pharma Industries’s competitive dynamics in detail.

Suppliers Bargaining Power

API concentration risk

Many key starting materials and APIs remain concentrated among a few suppliers, with India importing around 70% of certain KSMs/APIs from China, elevating switching costs and lead times for Sun Pharma. Supply disruptions can compress margins and degrade service levels, as seen in 2020–22 volatility. Sun mitigates risk through multi-sourcing and localisation programs but exposure persists for complex inputs.

Backward integration buffer

Sun Pharma's in-house API capabilities reduce reliance on external vendors, enhancing negotiation leverage on price, quality and delivery and supporting its cost-leadership in generics; as India’s largest pharma by market capitalization in 2024 this scale strengthens bargaining power, but gaps remain as not all specialty inputs are vertically integrated, leaving exposure in niche molecules and advanced formulations.

Regulatory-grade inputs

Suppliers for regulatory-grade inputs must meet stringent cGMP and audit standards, narrowing the vendor pool and elevating bargaining power of qualified suppliers. Compliant vendors command price and contractual premiums, and supplier failures can trigger supply interruptions and recalls with major commercial impact. Sun Pharma operates 44 manufacturing facilities across 6 countries and uses robust quality systems to monitor and qualify alternative sources.

Packaging and specialized equipment

Packaging and sterile consumables for Sun Pharma are high-spec and sourced from a small set of OEMs such as Sartorius and Thermo Fisher, concentrating supplier bargaining power.

Limited substitutes and regulatory validation increase stickiness through service contracts and equipment qualification, raising switching costs.

Volume commitments and global tenders, supported by Sun Pharma consolidated revenue INR 46,118 crore in FY2024, help temper pricing and secure better terms.

- Few OEMs: increases supplier power

- Service contracts: raises switching costs

- Validation tie-ins: regulatory lock-in

- Volume/tenders: lever for pricing

Logistics and lead-time sensitivity

Logistics for cold-chain, hazardous goods and cross-border documentation raise supplier leverage as specialized carriers and certification add cost; reliable logistics networks command premiums, especially for temperature-sensitive biologics. Longer lead times increase Sun Pharma’s working capital and inventory days, but Sun’s presence in 100+ countries helps negotiate better slots and terms.

- Cold-chain complexity raises transport premiums

- Hazardous goods require certified carriers

- Long lead times inflate inventory days

- 100+ country scale strengthens bargaining

KSM/API supplier power high; India imports ~70% from China, 44 plants partly reduce risk

Supplier power is elevated for key KSMs/APIs (India imports ~70% from China), specialised packaging and cold-chain OEMs, and cGMP-qualified vendors, creating switching costs and price premiums. Sun Pharma’s scale (consol. revenue INR 46,118 crore FY2024), 44 plants across 6 countries and 100+ market presence reduce but do not eliminate exposure in niche inputs.

| Metric | Value |

|---|---|

| Revenue FY2024 | INR 46,118 crore |

| KSM/API import (China) | ~70% |

| Manufacturing sites | 44 |

| Markets | 100+ |

What is included in the product

Tailored analysis of competitive forces facing Sun Pharma, evaluating supplier and buyer power, threat of new entrants, intensity of rivalry, and substitutes while highlighting disruptive threats, entry barriers, and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Sun Pharma that highlights competitive pressures and regulatory risks—ideal for quick decision-making and boardroom slides. Customize force levels with current market or policy changes and export a spider chart to visualize strategic pressure instantly.

Customers Bargaining Power

Consolidated purchasers

Large distributors, group purchasing organizations and government tenders aggregate demand, enabling aggressive price negotiations and winner-take-most contract awards; Sun Pharma, India's largest pharma by market capitalization in 2024, faces concentrated buyer power. The company must trade lower prices for assured supply, service levels and formulary access to protect volume and margin.

Therapeutic substitutability

In generics, buyers can switch among bioequivalent products easily—generics comprised about 90% of US prescriptions by volume in 2024—so low switching costs intensify buyer power and drive price erosion (prices often fall up to 80% after generic entry). Complex formulations or delivery systems lower therapeutic substitutability, while reliability, consistent supply and robust regulatory dossiers (proven approvals and PV records) allow Sun Pharma to soften pricing pressure.

Reimbursement and PBM influence

Formularies and PBM rebates—managed by three PBMs covering about 80% of US lives—shape volumes and net pricing, with brand rebates often in the 20–30% range. Exclusion from preferred tiers can cut product volumes and revenues by over 50% in the US market. Demonstrating cost-effectiveness is vital in specialty and dermatology where payer coverage depends on value and budget impact. Real-world evidence increasingly secures preferential placement and favorable reimbursement.

Quality and supply assurance demands

Buyers penalize shortages, recalls and quality lapses, driving contracts with service-level penalties and dual-sourcing; Sun Pharma’s broad manufacturing footprint and presence in over 100 markets (2024) helps sustain fill-rates and mitigate penalty risk. Consistently high OTIF performance can justify modest price premiums from large buyers.

- Buyers enforce SLAs

- Dual-sourcing standard

- Sun in 100+ markets (2024)

- High OTIF supports premiums

International tender dynamics

- Price-driven awards: lowest-bid emphasis

- Contract length: 2–5 year impact magnifier

- Thresholds: compliance and docs

- Value-adds: local supply, tech transfer

Buyer concentration and PBMs (~80% lives) drive steep price compression in generics market

Buyers are concentrated—large distributors, PBMs (~80% US lives) and government tenders—forcing aggressive price negotiation and winner-take-most awards; Sun Pharma (present in 100+ markets) trades price for volume and formulary access. Low switching costs in generics (≈90% of US Rx by volume) and steep post-entry price falls (up to 80%) amplify buyer power. International tenders and 2–5 year contracts intensify margin risk; Sun Pharma FY2024 revenue ₹41,696 crore.

| Metric | 2024 |

|---|---|

| FY2024 revenue | ₹41,696 crore |

| US generic Rx by volume | ≈90% |

| PBM coverage | ≈80% US lives |

| Markets | 100+ |

What You See Is What You Get

Sun Pharma Industries Porter's Five Forces Analysis

This preview shows the exact Sun Pharma Industries Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical document.

Go Beyond the Preview—Access the Full Strategic Report

Sun Pharma faces intense competitive rivalry from global generics and branded peers, pricing pressure and regulatory risk, with moderate supplier power, strong buyer leverage, and limited threat from new entrants due to scale and regulation; substitutes remain a manageable concern. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sun Pharma Industries’s competitive dynamics in detail.

Suppliers Bargaining Power

API concentration risk

Many key starting materials and APIs remain concentrated among a few suppliers, with India importing around 70% of certain KSMs/APIs from China, elevating switching costs and lead times for Sun Pharma. Supply disruptions can compress margins and degrade service levels, as seen in 2020–22 volatility. Sun mitigates risk through multi-sourcing and localisation programs but exposure persists for complex inputs.

Backward integration buffer

Sun Pharma's in-house API capabilities reduce reliance on external vendors, enhancing negotiation leverage on price, quality and delivery and supporting its cost-leadership in generics; as India’s largest pharma by market capitalization in 2024 this scale strengthens bargaining power, but gaps remain as not all specialty inputs are vertically integrated, leaving exposure in niche molecules and advanced formulations.

Regulatory-grade inputs

Suppliers for regulatory-grade inputs must meet stringent cGMP and audit standards, narrowing the vendor pool and elevating bargaining power of qualified suppliers. Compliant vendors command price and contractual premiums, and supplier failures can trigger supply interruptions and recalls with major commercial impact. Sun Pharma operates 44 manufacturing facilities across 6 countries and uses robust quality systems to monitor and qualify alternative sources.

Packaging and specialized equipment

Packaging and sterile consumables for Sun Pharma are high-spec and sourced from a small set of OEMs such as Sartorius and Thermo Fisher, concentrating supplier bargaining power.

Limited substitutes and regulatory validation increase stickiness through service contracts and equipment qualification, raising switching costs.

Volume commitments and global tenders, supported by Sun Pharma consolidated revenue INR 46,118 crore in FY2024, help temper pricing and secure better terms.

- Few OEMs: increases supplier power

- Service contracts: raises switching costs

- Validation tie-ins: regulatory lock-in

- Volume/tenders: lever for pricing

Logistics and lead-time sensitivity

Logistics for cold-chain, hazardous goods and cross-border documentation raise supplier leverage as specialized carriers and certification add cost; reliable logistics networks command premiums, especially for temperature-sensitive biologics. Longer lead times increase Sun Pharma’s working capital and inventory days, but Sun’s presence in 100+ countries helps negotiate better slots and terms.

- Cold-chain complexity raises transport premiums

- Hazardous goods require certified carriers

- Long lead times inflate inventory days

- 100+ country scale strengthens bargaining

KSM/API supplier power high; India imports ~70% from China, 44 plants partly reduce risk

Supplier power is elevated for key KSMs/APIs (India imports ~70% from China), specialised packaging and cold-chain OEMs, and cGMP-qualified vendors, creating switching costs and price premiums. Sun Pharma’s scale (consol. revenue INR 46,118 crore FY2024), 44 plants across 6 countries and 100+ market presence reduce but do not eliminate exposure in niche inputs.

| Metric | Value |

|---|---|

| Revenue FY2024 | INR 46,118 crore |

| KSM/API import (China) | ~70% |

| Manufacturing sites | 44 |

| Markets | 100+ |

What is included in the product

Tailored analysis of competitive forces facing Sun Pharma, evaluating supplier and buyer power, threat of new entrants, intensity of rivalry, and substitutes while highlighting disruptive threats, entry barriers, and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Sun Pharma that highlights competitive pressures and regulatory risks—ideal for quick decision-making and boardroom slides. Customize force levels with current market or policy changes and export a spider chart to visualize strategic pressure instantly.

Customers Bargaining Power

Consolidated purchasers

Large distributors, group purchasing organizations and government tenders aggregate demand, enabling aggressive price negotiations and winner-take-most contract awards; Sun Pharma, India's largest pharma by market capitalization in 2024, faces concentrated buyer power. The company must trade lower prices for assured supply, service levels and formulary access to protect volume and margin.

Therapeutic substitutability

In generics, buyers can switch among bioequivalent products easily—generics comprised about 90% of US prescriptions by volume in 2024—so low switching costs intensify buyer power and drive price erosion (prices often fall up to 80% after generic entry). Complex formulations or delivery systems lower therapeutic substitutability, while reliability, consistent supply and robust regulatory dossiers (proven approvals and PV records) allow Sun Pharma to soften pricing pressure.

Reimbursement and PBM influence

Formularies and PBM rebates—managed by three PBMs covering about 80% of US lives—shape volumes and net pricing, with brand rebates often in the 20–30% range. Exclusion from preferred tiers can cut product volumes and revenues by over 50% in the US market. Demonstrating cost-effectiveness is vital in specialty and dermatology where payer coverage depends on value and budget impact. Real-world evidence increasingly secures preferential placement and favorable reimbursement.

Quality and supply assurance demands

Buyers penalize shortages, recalls and quality lapses, driving contracts with service-level penalties and dual-sourcing; Sun Pharma’s broad manufacturing footprint and presence in over 100 markets (2024) helps sustain fill-rates and mitigate penalty risk. Consistently high OTIF performance can justify modest price premiums from large buyers.

- Buyers enforce SLAs

- Dual-sourcing standard

- Sun in 100+ markets (2024)

- High OTIF supports premiums

International tender dynamics

- Price-driven awards: lowest-bid emphasis

- Contract length: 2–5 year impact magnifier

- Thresholds: compliance and docs

- Value-adds: local supply, tech transfer

Buyer concentration and PBMs (~80% lives) drive steep price compression in generics market

Buyers are concentrated—large distributors, PBMs (~80% US lives) and government tenders—forcing aggressive price negotiation and winner-take-most awards; Sun Pharma (present in 100+ markets) trades price for volume and formulary access. Low switching costs in generics (≈90% of US Rx by volume) and steep post-entry price falls (up to 80%) amplify buyer power. International tenders and 2–5 year contracts intensify margin risk; Sun Pharma FY2024 revenue ₹41,696 crore.

| Metric | 2024 |

|---|---|

| FY2024 revenue | ₹41,696 crore |

| US generic Rx by volume | ≈90% |

| PBM coverage | ≈80% US lives |

| Markets | 100+ |

What You See Is What You Get

Sun Pharma Industries Porter's Five Forces Analysis

This preview shows the exact Sun Pharma Industries Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical document.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Sun Pharma faces intense competitive rivalry from global generics and branded peers, pricing pressure and regulatory risk, with moderate supplier power, strong buyer leverage, and limited threat from new entrants due to scale and regulation; substitutes remain a manageable concern. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sun Pharma Industries’s competitive dynamics in detail.

Suppliers Bargaining Power

API concentration risk

Many key starting materials and APIs remain concentrated among a few suppliers, with India importing around 70% of certain KSMs/APIs from China, elevating switching costs and lead times for Sun Pharma. Supply disruptions can compress margins and degrade service levels, as seen in 2020–22 volatility. Sun mitigates risk through multi-sourcing and localisation programs but exposure persists for complex inputs.

Backward integration buffer

Sun Pharma's in-house API capabilities reduce reliance on external vendors, enhancing negotiation leverage on price, quality and delivery and supporting its cost-leadership in generics; as India’s largest pharma by market capitalization in 2024 this scale strengthens bargaining power, but gaps remain as not all specialty inputs are vertically integrated, leaving exposure in niche molecules and advanced formulations.

Regulatory-grade inputs

Suppliers for regulatory-grade inputs must meet stringent cGMP and audit standards, narrowing the vendor pool and elevating bargaining power of qualified suppliers. Compliant vendors command price and contractual premiums, and supplier failures can trigger supply interruptions and recalls with major commercial impact. Sun Pharma operates 44 manufacturing facilities across 6 countries and uses robust quality systems to monitor and qualify alternative sources.

Packaging and specialized equipment

Packaging and sterile consumables for Sun Pharma are high-spec and sourced from a small set of OEMs such as Sartorius and Thermo Fisher, concentrating supplier bargaining power.

Limited substitutes and regulatory validation increase stickiness through service contracts and equipment qualification, raising switching costs.

Volume commitments and global tenders, supported by Sun Pharma consolidated revenue INR 46,118 crore in FY2024, help temper pricing and secure better terms.

- Few OEMs: increases supplier power

- Service contracts: raises switching costs

- Validation tie-ins: regulatory lock-in

- Volume/tenders: lever for pricing

Logistics and lead-time sensitivity

Logistics for cold-chain, hazardous goods and cross-border documentation raise supplier leverage as specialized carriers and certification add cost; reliable logistics networks command premiums, especially for temperature-sensitive biologics. Longer lead times increase Sun Pharma’s working capital and inventory days, but Sun’s presence in 100+ countries helps negotiate better slots and terms.

- Cold-chain complexity raises transport premiums

- Hazardous goods require certified carriers

- Long lead times inflate inventory days

- 100+ country scale strengthens bargaining

KSM/API supplier power high; India imports ~70% from China, 44 plants partly reduce risk

Supplier power is elevated for key KSMs/APIs (India imports ~70% from China), specialised packaging and cold-chain OEMs, and cGMP-qualified vendors, creating switching costs and price premiums. Sun Pharma’s scale (consol. revenue INR 46,118 crore FY2024), 44 plants across 6 countries and 100+ market presence reduce but do not eliminate exposure in niche inputs.

| Metric | Value |

|---|---|

| Revenue FY2024 | INR 46,118 crore |

| KSM/API import (China) | ~70% |

| Manufacturing sites | 44 |

| Markets | 100+ |

What is included in the product

Tailored analysis of competitive forces facing Sun Pharma, evaluating supplier and buyer power, threat of new entrants, intensity of rivalry, and substitutes while highlighting disruptive threats, entry barriers, and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for Sun Pharma that highlights competitive pressures and regulatory risks—ideal for quick decision-making and boardroom slides. Customize force levels with current market or policy changes and export a spider chart to visualize strategic pressure instantly.

Customers Bargaining Power

Consolidated purchasers

Large distributors, group purchasing organizations and government tenders aggregate demand, enabling aggressive price negotiations and winner-take-most contract awards; Sun Pharma, India's largest pharma by market capitalization in 2024, faces concentrated buyer power. The company must trade lower prices for assured supply, service levels and formulary access to protect volume and margin.

Therapeutic substitutability

In generics, buyers can switch among bioequivalent products easily—generics comprised about 90% of US prescriptions by volume in 2024—so low switching costs intensify buyer power and drive price erosion (prices often fall up to 80% after generic entry). Complex formulations or delivery systems lower therapeutic substitutability, while reliability, consistent supply and robust regulatory dossiers (proven approvals and PV records) allow Sun Pharma to soften pricing pressure.

Reimbursement and PBM influence

Formularies and PBM rebates—managed by three PBMs covering about 80% of US lives—shape volumes and net pricing, with brand rebates often in the 20–30% range. Exclusion from preferred tiers can cut product volumes and revenues by over 50% in the US market. Demonstrating cost-effectiveness is vital in specialty and dermatology where payer coverage depends on value and budget impact. Real-world evidence increasingly secures preferential placement and favorable reimbursement.

Quality and supply assurance demands

Buyers penalize shortages, recalls and quality lapses, driving contracts with service-level penalties and dual-sourcing; Sun Pharma’s broad manufacturing footprint and presence in over 100 markets (2024) helps sustain fill-rates and mitigate penalty risk. Consistently high OTIF performance can justify modest price premiums from large buyers.

- Buyers enforce SLAs

- Dual-sourcing standard

- Sun in 100+ markets (2024)

- High OTIF supports premiums

International tender dynamics

- Price-driven awards: lowest-bid emphasis

- Contract length: 2–5 year impact magnifier

- Thresholds: compliance and docs

- Value-adds: local supply, tech transfer

Buyer concentration and PBMs (~80% lives) drive steep price compression in generics market

Buyers are concentrated—large distributors, PBMs (~80% US lives) and government tenders—forcing aggressive price negotiation and winner-take-most awards; Sun Pharma (present in 100+ markets) trades price for volume and formulary access. Low switching costs in generics (≈90% of US Rx by volume) and steep post-entry price falls (up to 80%) amplify buyer power. International tenders and 2–5 year contracts intensify margin risk; Sun Pharma FY2024 revenue ₹41,696 crore.

| Metric | 2024 |

|---|---|

| FY2024 revenue | ₹41,696 crore |

| US generic Rx by volume | ≈90% |

| PBM coverage | ≈80% US lives |

| Markets | 100+ |

What You See Is What You Get

Sun Pharma Industries Porter's Five Forces Analysis

This preview shows the exact Sun Pharma Industries Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical document.