S&U Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

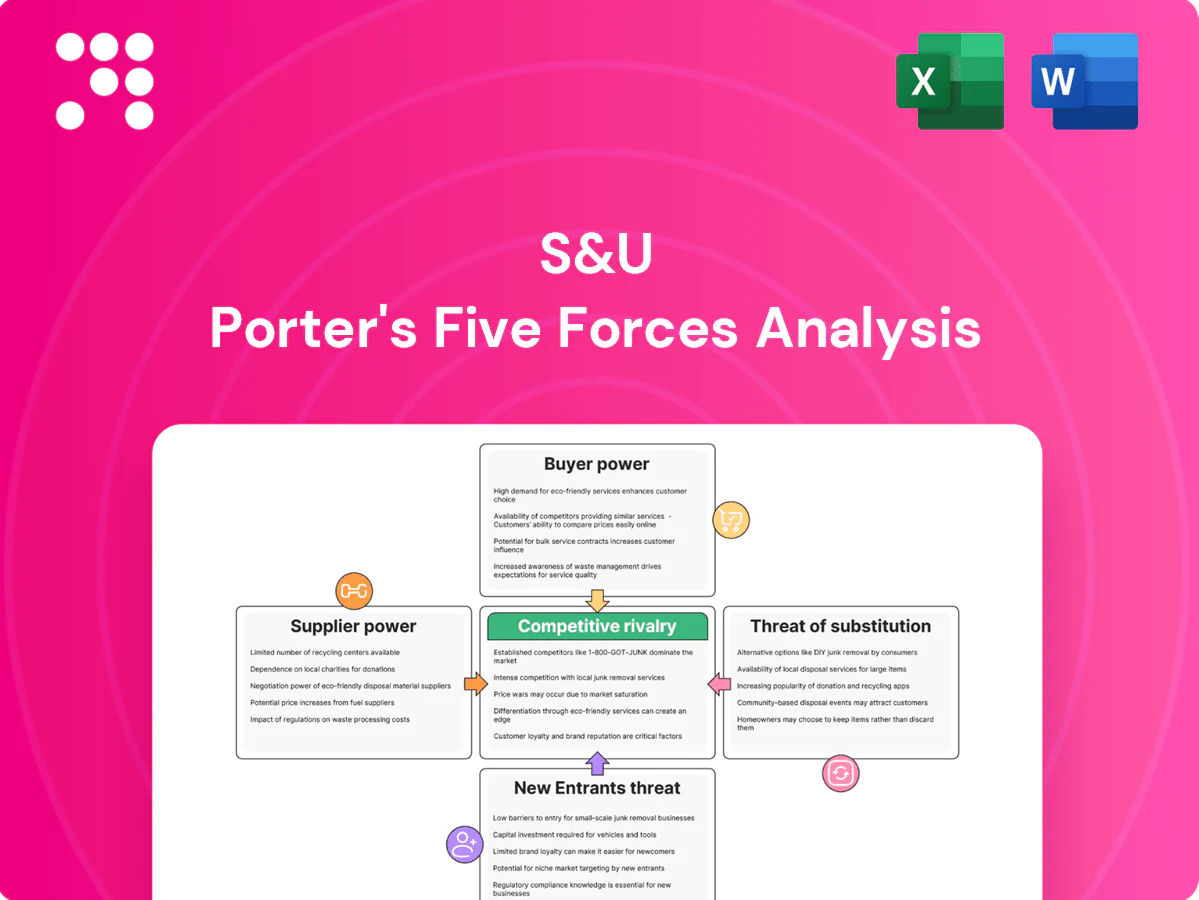

S&U’s competitive landscape is shaped by concentrated buyer segments, regulatory headwinds, and moderate supplier leverage, while digital disruptors and credit substitutes raise strategic risk. This snapshot highlights key pressure points and opportunities for value capture. Unlock the full Porter's Five Forces Analysis to explore S&U’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

S&U’s key suppliers are wholesale funders, banks and noteholders that provide debt; concentrated funding lines give lenders pricing power and can force wider margins. Diversifying facilities and keeping conservative leverage reduces dependence. Tight credit markets in 2024, with the Bank of England base rate at 5.25%, raised funding costs and constrained growth.

Supplier Power 2

Dealers, brokers and introducers channel roughly 70% of UK motor finance volumes in 2024, with high-performing introducers able to command commissions up to 15% or secure preferential terms; broad dealer networks and a rising direct-to-consumer origination share (about 30% in 2024) reduce reliance on any single introducer, while tighter compliance and oversight (compliance costs +20% YoY in 2024) cap introducer leverage.

Supplier Power 3

Data and tech vendors—credit bureaus, decisioning platforms and open-banking providers—are critical inputs, with the three major bureaus handling billions of consumer records and dominating markets in 2024. Switching costs and integration complexity give vendors moderate leverage, although multi-bureau sourcing and in-house analytics blunt pricing power. Vendor price creep has eroded margins for lenders, materially impacting unit economics.

Supplier Power 4

Supplier Power 5

Regulatory environment acts as a quasi-supplier of permissions and rules, with FCA expectations—notably Consumer Duty coming into full effect for open products in July 2024—forcing process and cost changes. Compliance investments are non-negotiable, lifting fixed costs and operating leverage. Strong governance reduces surprise shocks to supply-side economics and preserves margins.

Suppliers exert moderate-to-high power: BoE 5.25%, introducers ~70%, costs +20%

S&U’s suppliers (funders, introducers, data vendors, conveyancers) exert moderate-to-high bargaining power in 2024: BoE base rate 5.25% lifted funding costs; introducers account for ~70% volumes (D2C ~30%), commissions up to 15%; conveyancing 10–14 weeks and fall-throughs ~6–8%; compliance costs +20% YoY.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Funders | BoE 5.25% | Higher margins |

| Introducers | ~70% vol; 15% comms | Pricing power |

| Conveyancers | 10–14 wks; 6–8% fall-through | Delay/cost |

| Compliance | +20% costs YoY | Higher fixed costs |

What is included in the product

Concise Porter's Five Forces assessment tailored to S&U, uncovering competitive rivalry, buyer and supplier leverage, threat of new entrants and substitutes, and highlighting disruptive pressures and defensive advantages for strategic use in reports and presentations.

S&U Porter's Five Forces Analysis delivers a concise one-sheet mapping supplier, buyer, entrant, substitute, and rivalry pressures—relieving strategic uncertainty for quick decision-making, pitch decks, and boardroom discussions.

Customers Bargaining Power

Buyer Power 1

Motor finance customers are price-sensitive but a large share are near-prime/subprime, limiting alternatives; UK motor finance outstanding was c.£80bn in 2024. Switching costs are low via dealer finance menus and online comparison tools, and while no APR caps exist, FCA Consumer Duty (effective July 2023) pressures fair value. S&U counters with risk-based pricing and faster service to retain margins.

Buyer Power 2

Bridging borrowers (investors/developers) shop aggressively on rate, fees, LTV and speed, with typical UK bridging rates around 7–12% in 2024 driving strong price sensitivity. Broker intermediation—responsible for roughly 70% of transactions—heightens transparency and intensifies price competition. Lenders offering fast approvals and flexible underwriting can command a 0.5–1.5% pricing premium. Repeat borrowers, representing about 40% of volume, reduce churn pressure.

Buyer Power 3

Economic cycles shift buyer power: tight household budgets raise delinquency risk and push demand for concessions, with many borrowers seeking forbearance or refinancing in downturns. UK Bank Rate was 5.25% in July 2024, amplifying affordability stress. Robust collections frameworks help preserve contract terms without reputational damage. Affordability rules (income-verified checks) constrain excessive concessions.

Buyer Power 4

Digital comparison tools have raised buyer knowledge, making rate spreads highly visible and exerting downward pressure on margins, though differentiation through superior customer experience, speed, and certainty reduces pure price-based switching.

Clear disclosures build trust and improve retention, shifting competition toward service quality and reliability rather than only price.

- Visible rate spreads

- Experience and speed as differentiators

- Disclosures support retention

Buyer Power 5

Dealer partners in motor finance can steer borrowers to alternative lenders, giving buyers leverage; S&U reported in 2024 that dealer relationships remain central to origination strategy.

High-volume dealers negotiate higher commissions and tighter service SLAs, shifting bargaining power toward dealers on pricing and terms.

A broad dealer network lowers counterparty concentration risk for S&U, while performance-linked incentives align dealer behavior and partially rebalance power.

- Dealer steering: increases buyer options

- High-volume dealers: stronger commission leverage

- Broad network: reduces concentration risk

- Incentives: tie performance to referrals and service

UK motor finance: £80bn market, brokers lead as 7-12% rates and 5.25% Bank Rate squeeze buyers

Customers are price-sensitive; UK motor finance outstanding c.£80bn in 2024 and switching is easy via dealer menus and comparison tools. Bridging borrowers hunt rates (7–12% in 2024) and brokers (~70% of deals) raise transparency. Repeat borrowers (~40% of volume) and faster service/clear disclosures reduce churn. Bank Rate 5.25% (Jul 2024) tightens affordability, increasing concession pressure.

| Metric | 2024 |

|---|---|

| Motor finance outstanding | £80bn |

| Bridging rates | 7–12% |

| Broker share (bridging) | ~70% |

| Repeat borrower volume | ~40% |

| UK Bank Rate (Jul) | 5.25% |

What You See Is What You Get

S&U Porter's Five Forces Analysis

This preview displays the complete S&U Porter's Five Forces Analysis you’ll receive after purchase—no placeholders or samples. The file is fully formatted, professionally written and ready for immediate download and use. What you see here is exactly what you’ll get upon payment.

Go Beyond the Preview—Access the Full Strategic Report

S&U’s competitive landscape is shaped by concentrated buyer segments, regulatory headwinds, and moderate supplier leverage, while digital disruptors and credit substitutes raise strategic risk. This snapshot highlights key pressure points and opportunities for value capture. Unlock the full Porter's Five Forces Analysis to explore S&U’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

S&U’s key suppliers are wholesale funders, banks and noteholders that provide debt; concentrated funding lines give lenders pricing power and can force wider margins. Diversifying facilities and keeping conservative leverage reduces dependence. Tight credit markets in 2024, with the Bank of England base rate at 5.25%, raised funding costs and constrained growth.

Supplier Power 2

Dealers, brokers and introducers channel roughly 70% of UK motor finance volumes in 2024, with high-performing introducers able to command commissions up to 15% or secure preferential terms; broad dealer networks and a rising direct-to-consumer origination share (about 30% in 2024) reduce reliance on any single introducer, while tighter compliance and oversight (compliance costs +20% YoY in 2024) cap introducer leverage.

Supplier Power 3

Data and tech vendors—credit bureaus, decisioning platforms and open-banking providers—are critical inputs, with the three major bureaus handling billions of consumer records and dominating markets in 2024. Switching costs and integration complexity give vendors moderate leverage, although multi-bureau sourcing and in-house analytics blunt pricing power. Vendor price creep has eroded margins for lenders, materially impacting unit economics.

Supplier Power 4

Supplier Power 5

Regulatory environment acts as a quasi-supplier of permissions and rules, with FCA expectations—notably Consumer Duty coming into full effect for open products in July 2024—forcing process and cost changes. Compliance investments are non-negotiable, lifting fixed costs and operating leverage. Strong governance reduces surprise shocks to supply-side economics and preserves margins.

Suppliers exert moderate-to-high power: BoE 5.25%, introducers ~70%, costs +20%

S&U’s suppliers (funders, introducers, data vendors, conveyancers) exert moderate-to-high bargaining power in 2024: BoE base rate 5.25% lifted funding costs; introducers account for ~70% volumes (D2C ~30%), commissions up to 15%; conveyancing 10–14 weeks and fall-throughs ~6–8%; compliance costs +20% YoY.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Funders | BoE 5.25% | Higher margins |

| Introducers | ~70% vol; 15% comms | Pricing power |

| Conveyancers | 10–14 wks; 6–8% fall-through | Delay/cost |

| Compliance | +20% costs YoY | Higher fixed costs |

What is included in the product

Concise Porter's Five Forces assessment tailored to S&U, uncovering competitive rivalry, buyer and supplier leverage, threat of new entrants and substitutes, and highlighting disruptive pressures and defensive advantages for strategic use in reports and presentations.

S&U Porter's Five Forces Analysis delivers a concise one-sheet mapping supplier, buyer, entrant, substitute, and rivalry pressures—relieving strategic uncertainty for quick decision-making, pitch decks, and boardroom discussions.

Customers Bargaining Power

Buyer Power 1

Motor finance customers are price-sensitive but a large share are near-prime/subprime, limiting alternatives; UK motor finance outstanding was c.£80bn in 2024. Switching costs are low via dealer finance menus and online comparison tools, and while no APR caps exist, FCA Consumer Duty (effective July 2023) pressures fair value. S&U counters with risk-based pricing and faster service to retain margins.

Buyer Power 2

Bridging borrowers (investors/developers) shop aggressively on rate, fees, LTV and speed, with typical UK bridging rates around 7–12% in 2024 driving strong price sensitivity. Broker intermediation—responsible for roughly 70% of transactions—heightens transparency and intensifies price competition. Lenders offering fast approvals and flexible underwriting can command a 0.5–1.5% pricing premium. Repeat borrowers, representing about 40% of volume, reduce churn pressure.

Buyer Power 3

Economic cycles shift buyer power: tight household budgets raise delinquency risk and push demand for concessions, with many borrowers seeking forbearance or refinancing in downturns. UK Bank Rate was 5.25% in July 2024, amplifying affordability stress. Robust collections frameworks help preserve contract terms without reputational damage. Affordability rules (income-verified checks) constrain excessive concessions.

Buyer Power 4

Digital comparison tools have raised buyer knowledge, making rate spreads highly visible and exerting downward pressure on margins, though differentiation through superior customer experience, speed, and certainty reduces pure price-based switching.

Clear disclosures build trust and improve retention, shifting competition toward service quality and reliability rather than only price.

- Visible rate spreads

- Experience and speed as differentiators

- Disclosures support retention

Buyer Power 5

Dealer partners in motor finance can steer borrowers to alternative lenders, giving buyers leverage; S&U reported in 2024 that dealer relationships remain central to origination strategy.

High-volume dealers negotiate higher commissions and tighter service SLAs, shifting bargaining power toward dealers on pricing and terms.

A broad dealer network lowers counterparty concentration risk for S&U, while performance-linked incentives align dealer behavior and partially rebalance power.

- Dealer steering: increases buyer options

- High-volume dealers: stronger commission leverage

- Broad network: reduces concentration risk

- Incentives: tie performance to referrals and service

UK motor finance: £80bn market, brokers lead as 7-12% rates and 5.25% Bank Rate squeeze buyers

Customers are price-sensitive; UK motor finance outstanding c.£80bn in 2024 and switching is easy via dealer menus and comparison tools. Bridging borrowers hunt rates (7–12% in 2024) and brokers (~70% of deals) raise transparency. Repeat borrowers (~40% of volume) and faster service/clear disclosures reduce churn. Bank Rate 5.25% (Jul 2024) tightens affordability, increasing concession pressure.

| Metric | 2024 |

|---|---|

| Motor finance outstanding | £80bn |

| Bridging rates | 7–12% |

| Broker share (bridging) | ~70% |

| Repeat borrower volume | ~40% |

| UK Bank Rate (Jul) | 5.25% |

What You See Is What You Get

S&U Porter's Five Forces Analysis

This preview displays the complete S&U Porter's Five Forces Analysis you’ll receive after purchase—no placeholders or samples. The file is fully formatted, professionally written and ready for immediate download and use. What you see here is exactly what you’ll get upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

S&U’s competitive landscape is shaped by concentrated buyer segments, regulatory headwinds, and moderate supplier leverage, while digital disruptors and credit substitutes raise strategic risk. This snapshot highlights key pressure points and opportunities for value capture. Unlock the full Porter's Five Forces Analysis to explore S&U’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

S&U’s key suppliers are wholesale funders, banks and noteholders that provide debt; concentrated funding lines give lenders pricing power and can force wider margins. Diversifying facilities and keeping conservative leverage reduces dependence. Tight credit markets in 2024, with the Bank of England base rate at 5.25%, raised funding costs and constrained growth.

Supplier Power 2

Dealers, brokers and introducers channel roughly 70% of UK motor finance volumes in 2024, with high-performing introducers able to command commissions up to 15% or secure preferential terms; broad dealer networks and a rising direct-to-consumer origination share (about 30% in 2024) reduce reliance on any single introducer, while tighter compliance and oversight (compliance costs +20% YoY in 2024) cap introducer leverage.

Supplier Power 3

Data and tech vendors—credit bureaus, decisioning platforms and open-banking providers—are critical inputs, with the three major bureaus handling billions of consumer records and dominating markets in 2024. Switching costs and integration complexity give vendors moderate leverage, although multi-bureau sourcing and in-house analytics blunt pricing power. Vendor price creep has eroded margins for lenders, materially impacting unit economics.

Supplier Power 4

Supplier Power 5

Regulatory environment acts as a quasi-supplier of permissions and rules, with FCA expectations—notably Consumer Duty coming into full effect for open products in July 2024—forcing process and cost changes. Compliance investments are non-negotiable, lifting fixed costs and operating leverage. Strong governance reduces surprise shocks to supply-side economics and preserves margins.

Suppliers exert moderate-to-high power: BoE 5.25%, introducers ~70%, costs +20%

S&U’s suppliers (funders, introducers, data vendors, conveyancers) exert moderate-to-high bargaining power in 2024: BoE base rate 5.25% lifted funding costs; introducers account for ~70% volumes (D2C ~30%), commissions up to 15%; conveyancing 10–14 weeks and fall-throughs ~6–8%; compliance costs +20% YoY.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Funders | BoE 5.25% | Higher margins |

| Introducers | ~70% vol; 15% comms | Pricing power |

| Conveyancers | 10–14 wks; 6–8% fall-through | Delay/cost |

| Compliance | +20% costs YoY | Higher fixed costs |

What is included in the product

Concise Porter's Five Forces assessment tailored to S&U, uncovering competitive rivalry, buyer and supplier leverage, threat of new entrants and substitutes, and highlighting disruptive pressures and defensive advantages for strategic use in reports and presentations.

S&U Porter's Five Forces Analysis delivers a concise one-sheet mapping supplier, buyer, entrant, substitute, and rivalry pressures—relieving strategic uncertainty for quick decision-making, pitch decks, and boardroom discussions.

Customers Bargaining Power

Buyer Power 1

Motor finance customers are price-sensitive but a large share are near-prime/subprime, limiting alternatives; UK motor finance outstanding was c.£80bn in 2024. Switching costs are low via dealer finance menus and online comparison tools, and while no APR caps exist, FCA Consumer Duty (effective July 2023) pressures fair value. S&U counters with risk-based pricing and faster service to retain margins.

Buyer Power 2

Bridging borrowers (investors/developers) shop aggressively on rate, fees, LTV and speed, with typical UK bridging rates around 7–12% in 2024 driving strong price sensitivity. Broker intermediation—responsible for roughly 70% of transactions—heightens transparency and intensifies price competition. Lenders offering fast approvals and flexible underwriting can command a 0.5–1.5% pricing premium. Repeat borrowers, representing about 40% of volume, reduce churn pressure.

Buyer Power 3

Economic cycles shift buyer power: tight household budgets raise delinquency risk and push demand for concessions, with many borrowers seeking forbearance or refinancing in downturns. UK Bank Rate was 5.25% in July 2024, amplifying affordability stress. Robust collections frameworks help preserve contract terms without reputational damage. Affordability rules (income-verified checks) constrain excessive concessions.

Buyer Power 4

Digital comparison tools have raised buyer knowledge, making rate spreads highly visible and exerting downward pressure on margins, though differentiation through superior customer experience, speed, and certainty reduces pure price-based switching.

Clear disclosures build trust and improve retention, shifting competition toward service quality and reliability rather than only price.

- Visible rate spreads

- Experience and speed as differentiators

- Disclosures support retention

Buyer Power 5

Dealer partners in motor finance can steer borrowers to alternative lenders, giving buyers leverage; S&U reported in 2024 that dealer relationships remain central to origination strategy.

High-volume dealers negotiate higher commissions and tighter service SLAs, shifting bargaining power toward dealers on pricing and terms.

A broad dealer network lowers counterparty concentration risk for S&U, while performance-linked incentives align dealer behavior and partially rebalance power.

- Dealer steering: increases buyer options

- High-volume dealers: stronger commission leverage

- Broad network: reduces concentration risk

- Incentives: tie performance to referrals and service

UK motor finance: £80bn market, brokers lead as 7-12% rates and 5.25% Bank Rate squeeze buyers

Customers are price-sensitive; UK motor finance outstanding c.£80bn in 2024 and switching is easy via dealer menus and comparison tools. Bridging borrowers hunt rates (7–12% in 2024) and brokers (~70% of deals) raise transparency. Repeat borrowers (~40% of volume) and faster service/clear disclosures reduce churn. Bank Rate 5.25% (Jul 2024) tightens affordability, increasing concession pressure.

| Metric | 2024 |

|---|---|

| Motor finance outstanding | £80bn |

| Bridging rates | 7–12% |

| Broker share (bridging) | ~70% |

| Repeat borrower volume | ~40% |

| UK Bank Rate (Jul) | 5.25% |

What You See Is What You Get

S&U Porter's Five Forces Analysis

This preview displays the complete S&U Porter's Five Forces Analysis you’ll receive after purchase—no placeholders or samples. The file is fully formatted, professionally written and ready for immediate download and use. What you see here is exactly what you’ll get upon payment.