Supremex Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

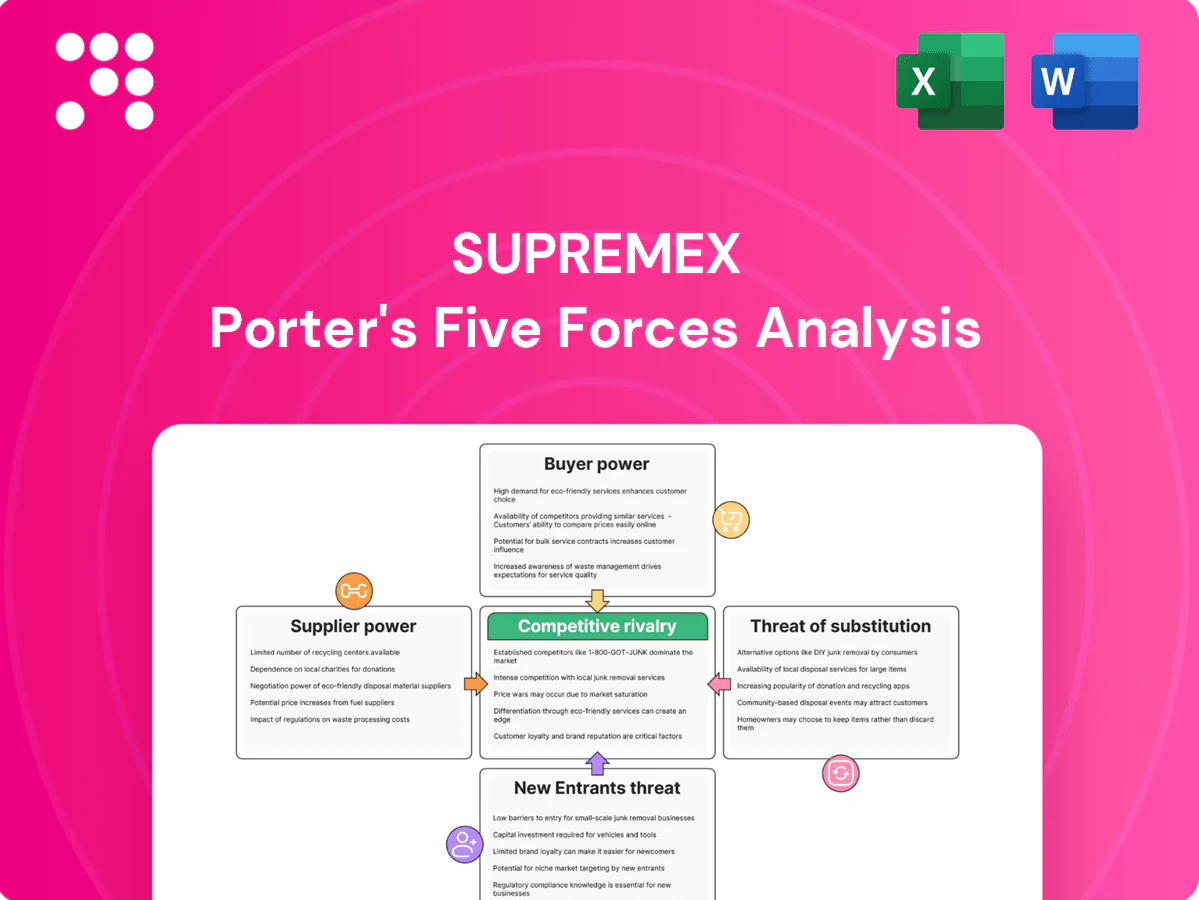

Supremex’s Porter's Five Forces snapshot highlights supplier leverage, buyer sensitivity, competitive rivalry, threat of substitutes, and entry barriers shaping margins and growth. This brief teases key strategic pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for data-driven insights, detailed ratings, and actionable recommendations to guide investment or strategic decisions.

Suppliers Bargaining Power

Concentrated paper and film sources

Core inputs like paper, specialty films, inks and adhesives are sourced from a concentrated set of suppliers, giving suppliers leverage over pricing and availability; North American mill rationalization has cut envelope-grade capacity roughly 5% since 2019, tightening supply. Specialty substrates for bubble mailers and custom packaging are even narrower, raising single-source risks and supplier bargaining power. In 2024 kraft and specialty paper prices rose about 10–12% year-over-year, and extended lead times of 6–10 weeks were reported for select substrates, pressuring margins and working capital for Supremex.

Quality and certification requirements

Supremex’s insistence on consistent specs, FSC or recycled content and regulatory compliance narrows vendor interchangeability, as certified converters represent a smaller, more specialized pool. Tight quality and certification requirements raise switching costs and lengthen onboarding due to audit, testing and qualification processes. Suppliers that pass audits and certify continuity can command steadier terms and multi-year contracts.

Logistics and energy volatility

Freight, energy and resin surcharges transfer pricing power to suppliers, with common fuel surcharges ranging 3–10% and resin spot swings reaching double-digit moves in 2024; carriers and resin producers can pass volatility through surcharges. Cross-border shipping in 2024 still added documentation delays and average transit variability of several days. Tight trucking capacity favors larger shippers; Supremex must hold buffer inventory and diversify lanes to mitigate these supplier-driven cost shocks.

Limited backward integration options

Vertical integration into pulp or resin remains capital intensive and impractical for Supremex, with pulp mill capex typically exceeding US$1 billion and multi-year construction timelines, sustaining supplier power. Converters depend on mills for capacity allocations and substrate availability, with lead times commonly 3–6 months that constrain agility. Strategic partnerships and long-term agreements in 2024 mitigate price volatility but do not remove allocation risk.

- Pulp mill capex > US$1bn

- Lead times 3–6 months

- Mills control capacity allocations

- LTAs/partnerships reduce but do not eliminate supplier risk

Mitigation via dual-sourcing and scale

Supremex’s multi-plant footprint and scale enable stronger negotiating leverage, and in 2024 the company strengthened dual-sourcing and specification flexibility to cut supplier dependence; vendor-managed inventory and shared forecasts improved allocation priority, though specialty inputs (barriers like custom inks and films) preserve some supplier bargaining power.

- Scale: multi-plant leverage

- Dual-sourcing: lower dependency

- VMI: better allocation

- Risk: specialty inputs retain power

Supplier power strong: +10–12% paper prices, 6–10 week lead times

Suppliers hold moderate-to-high power: concentrated paper/film mills, 2024 kraft/specialty paper +10–12% YoY and 6–10 week lead times tightened availability and margins. Certification and spec needs raise switching costs and favor audited suppliers; pulp mill capex > US$1bn limits upstream entry. Supremex scale, dual-sourcing and VMI reduce but do not eliminate supplier leverage.

| Metric | 2024 |

|---|---|

| Paper price change | +10–12% YoY |

| Lead times | 6–10 weeks |

| Fuel surcharges | 3–10% |

| Pulp mill capex | >US$1bn |

What is included in the product

Tailored Porter's Five Forces analysis for Supremex revealing competitive intensity, supplier and buyer leverage, barriers deterring entrants, and threats from substitutes and industry disruptors to assess pricing power and strategic vulnerabilities.

Clean, simplified Supremex Porter's Five Forces one-sheet—instantly copyable into pitch decks or boardroom slides to clarify competitive pressure and speed decision-making.

Customers Bargaining Power

Large enterprise and government buyers

Large enterprise and government buyers exert strong negotiation power over Supremex, with industry reports in 2024 indicating consolidated buyers drive roughly 60% of contracted volumes in packaging and foam supply chains. They run competitive bids and demand stringent SLAs, compressing vendor margins and forcing price concessions. Panel awards can reallocate volumes rapidly, causing single-contract shifts of 20–40% between suppliers.

Price sensitivity in commoditized SKUs

Standard envelopes and mailers are highly price-sensitive in commoditized SKUs, with comparable specs enabling rapid cross-quoting and driving buyers toward the lowest bidder; small switching costs further intensify buyer leverage. Discounts and volume rebates are often required to win or retain accounts, and as of 2024 Supremex trades on the TSX under ticker SMT.

Customization raises stickiness

Customization in sizes, print and packaging solutions increases switching costs by embedding tooling, artwork and workflow integration into client operations; for Supremex, with 2024 revenue near CAD 700M, bespoke lines account for a substantial share of volumes. Tooling and artwork changes are disruptive, making service reliability and lead-time performance key differentiators. This capability partially offsets price pressure by preserving margin and client stickiness.

E-commerce procurement transparency

Digital catalogs and e-procurement make market prices visible, shrinking information asymmetry; the global e-procurement market reached about USD 10.7 billion in 2024, amplifying buyer leverage. Buyers benchmark across distributors and manufacturers rapidly, and short-term spot buys—up ~25% in 2024—can bypass contracts, heightening pressure on realized pricing.

Demand mix shift effects

Declining letter-mail volumes have reduced envelope demand while parcel growth from e-commerce shifts buyer spend toward protective packaging; global e-commerce sales reached about US$5.7 trillion in 2024, supporting ~10% parcel volume growth that year. Forecast volatility forces Supremex to offer flexible capacity and dynamic pricing and to realign products to where buyers’ growth is concentrated.

- Envelope demand down; parcel demand up

- Buyers reallocating to protective packaging

- Need for flexible capacity & pricing

- Align product mix to high-growth parcels/packaging

Buyers control ~60% of contracted volumes; panel awards can shift 20-40%

Large buyers exert strong leverage—consolidated customers drive ~60% of contracted volumes, forcing competitive bids, discounts and SLAs that compress margins; panel awards can shift 20–40% volume between suppliers. Commoditized SKUs and visible e-procurement pricing (global market ~USD 10.7B in 2024) amplify switching; bespoke lines (Supremex rev ~CAD 700M in 2024) partially protect margins amid ~25% rise in spot buys and ~10% parcel growth.

| Metric | 2024 Value |

|---|---|

| Buyer share of contracted volumes | ~60% |

| Supremex revenue | ~CAD 700M |

| E-procurement market | USD 10.7B |

| Spot buys increase | ~25% |

| Parcel/ e-commerce growth | ~10% (US$5.7T sales) |

Full Version Awaits

Supremex Porter's Five Forces Analysis

This Supremex Porter's Five Forces analysis is the exact document you’re previewing and the same professionally written file you’ll receive immediately after purchase. No samples, mockups, or placeholders—just the full, formatted analysis ready for download and use. Purchase grants instant access to this identical deliverable, prepared for immediate application in your decision-making.

Go Beyond the Preview—Access the Full Strategic Report

Supremex’s Porter's Five Forces snapshot highlights supplier leverage, buyer sensitivity, competitive rivalry, threat of substitutes, and entry barriers shaping margins and growth. This brief teases key strategic pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for data-driven insights, detailed ratings, and actionable recommendations to guide investment or strategic decisions.

Suppliers Bargaining Power

Concentrated paper and film sources

Core inputs like paper, specialty films, inks and adhesives are sourced from a concentrated set of suppliers, giving suppliers leverage over pricing and availability; North American mill rationalization has cut envelope-grade capacity roughly 5% since 2019, tightening supply. Specialty substrates for bubble mailers and custom packaging are even narrower, raising single-source risks and supplier bargaining power. In 2024 kraft and specialty paper prices rose about 10–12% year-over-year, and extended lead times of 6–10 weeks were reported for select substrates, pressuring margins and working capital for Supremex.

Quality and certification requirements

Supremex’s insistence on consistent specs, FSC or recycled content and regulatory compliance narrows vendor interchangeability, as certified converters represent a smaller, more specialized pool. Tight quality and certification requirements raise switching costs and lengthen onboarding due to audit, testing and qualification processes. Suppliers that pass audits and certify continuity can command steadier terms and multi-year contracts.

Logistics and energy volatility

Freight, energy and resin surcharges transfer pricing power to suppliers, with common fuel surcharges ranging 3–10% and resin spot swings reaching double-digit moves in 2024; carriers and resin producers can pass volatility through surcharges. Cross-border shipping in 2024 still added documentation delays and average transit variability of several days. Tight trucking capacity favors larger shippers; Supremex must hold buffer inventory and diversify lanes to mitigate these supplier-driven cost shocks.

Limited backward integration options

Vertical integration into pulp or resin remains capital intensive and impractical for Supremex, with pulp mill capex typically exceeding US$1 billion and multi-year construction timelines, sustaining supplier power. Converters depend on mills for capacity allocations and substrate availability, with lead times commonly 3–6 months that constrain agility. Strategic partnerships and long-term agreements in 2024 mitigate price volatility but do not remove allocation risk.

- Pulp mill capex > US$1bn

- Lead times 3–6 months

- Mills control capacity allocations

- LTAs/partnerships reduce but do not eliminate supplier risk

Mitigation via dual-sourcing and scale

Supremex’s multi-plant footprint and scale enable stronger negotiating leverage, and in 2024 the company strengthened dual-sourcing and specification flexibility to cut supplier dependence; vendor-managed inventory and shared forecasts improved allocation priority, though specialty inputs (barriers like custom inks and films) preserve some supplier bargaining power.

- Scale: multi-plant leverage

- Dual-sourcing: lower dependency

- VMI: better allocation

- Risk: specialty inputs retain power

Supplier power strong: +10–12% paper prices, 6–10 week lead times

Suppliers hold moderate-to-high power: concentrated paper/film mills, 2024 kraft/specialty paper +10–12% YoY and 6–10 week lead times tightened availability and margins. Certification and spec needs raise switching costs and favor audited suppliers; pulp mill capex > US$1bn limits upstream entry. Supremex scale, dual-sourcing and VMI reduce but do not eliminate supplier leverage.

| Metric | 2024 |

|---|---|

| Paper price change | +10–12% YoY |

| Lead times | 6–10 weeks |

| Fuel surcharges | 3–10% |

| Pulp mill capex | >US$1bn |

What is included in the product

Tailored Porter's Five Forces analysis for Supremex revealing competitive intensity, supplier and buyer leverage, barriers deterring entrants, and threats from substitutes and industry disruptors to assess pricing power and strategic vulnerabilities.

Clean, simplified Supremex Porter's Five Forces one-sheet—instantly copyable into pitch decks or boardroom slides to clarify competitive pressure and speed decision-making.

Customers Bargaining Power

Large enterprise and government buyers

Large enterprise and government buyers exert strong negotiation power over Supremex, with industry reports in 2024 indicating consolidated buyers drive roughly 60% of contracted volumes in packaging and foam supply chains. They run competitive bids and demand stringent SLAs, compressing vendor margins and forcing price concessions. Panel awards can reallocate volumes rapidly, causing single-contract shifts of 20–40% between suppliers.

Price sensitivity in commoditized SKUs

Standard envelopes and mailers are highly price-sensitive in commoditized SKUs, with comparable specs enabling rapid cross-quoting and driving buyers toward the lowest bidder; small switching costs further intensify buyer leverage. Discounts and volume rebates are often required to win or retain accounts, and as of 2024 Supremex trades on the TSX under ticker SMT.

Customization raises stickiness

Customization in sizes, print and packaging solutions increases switching costs by embedding tooling, artwork and workflow integration into client operations; for Supremex, with 2024 revenue near CAD 700M, bespoke lines account for a substantial share of volumes. Tooling and artwork changes are disruptive, making service reliability and lead-time performance key differentiators. This capability partially offsets price pressure by preserving margin and client stickiness.

E-commerce procurement transparency

Digital catalogs and e-procurement make market prices visible, shrinking information asymmetry; the global e-procurement market reached about USD 10.7 billion in 2024, amplifying buyer leverage. Buyers benchmark across distributors and manufacturers rapidly, and short-term spot buys—up ~25% in 2024—can bypass contracts, heightening pressure on realized pricing.

Demand mix shift effects

Declining letter-mail volumes have reduced envelope demand while parcel growth from e-commerce shifts buyer spend toward protective packaging; global e-commerce sales reached about US$5.7 trillion in 2024, supporting ~10% parcel volume growth that year. Forecast volatility forces Supremex to offer flexible capacity and dynamic pricing and to realign products to where buyers’ growth is concentrated.

- Envelope demand down; parcel demand up

- Buyers reallocating to protective packaging

- Need for flexible capacity & pricing

- Align product mix to high-growth parcels/packaging

Buyers control ~60% of contracted volumes; panel awards can shift 20-40%

Large buyers exert strong leverage—consolidated customers drive ~60% of contracted volumes, forcing competitive bids, discounts and SLAs that compress margins; panel awards can shift 20–40% volume between suppliers. Commoditized SKUs and visible e-procurement pricing (global market ~USD 10.7B in 2024) amplify switching; bespoke lines (Supremex rev ~CAD 700M in 2024) partially protect margins amid ~25% rise in spot buys and ~10% parcel growth.

| Metric | 2024 Value |

|---|---|

| Buyer share of contracted volumes | ~60% |

| Supremex revenue | ~CAD 700M |

| E-procurement market | USD 10.7B |

| Spot buys increase | ~25% |

| Parcel/ e-commerce growth | ~10% (US$5.7T sales) |

Full Version Awaits

Supremex Porter's Five Forces Analysis

This Supremex Porter's Five Forces analysis is the exact document you’re previewing and the same professionally written file you’ll receive immediately after purchase. No samples, mockups, or placeholders—just the full, formatted analysis ready for download and use. Purchase grants instant access to this identical deliverable, prepared for immediate application in your decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Supremex’s Porter's Five Forces snapshot highlights supplier leverage, buyer sensitivity, competitive rivalry, threat of substitutes, and entry barriers shaping margins and growth. This brief teases key strategic pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for data-driven insights, detailed ratings, and actionable recommendations to guide investment or strategic decisions.

Suppliers Bargaining Power

Concentrated paper and film sources

Core inputs like paper, specialty films, inks and adhesives are sourced from a concentrated set of suppliers, giving suppliers leverage over pricing and availability; North American mill rationalization has cut envelope-grade capacity roughly 5% since 2019, tightening supply. Specialty substrates for bubble mailers and custom packaging are even narrower, raising single-source risks and supplier bargaining power. In 2024 kraft and specialty paper prices rose about 10–12% year-over-year, and extended lead times of 6–10 weeks were reported for select substrates, pressuring margins and working capital for Supremex.

Quality and certification requirements

Supremex’s insistence on consistent specs, FSC or recycled content and regulatory compliance narrows vendor interchangeability, as certified converters represent a smaller, more specialized pool. Tight quality and certification requirements raise switching costs and lengthen onboarding due to audit, testing and qualification processes. Suppliers that pass audits and certify continuity can command steadier terms and multi-year contracts.

Logistics and energy volatility

Freight, energy and resin surcharges transfer pricing power to suppliers, with common fuel surcharges ranging 3–10% and resin spot swings reaching double-digit moves in 2024; carriers and resin producers can pass volatility through surcharges. Cross-border shipping in 2024 still added documentation delays and average transit variability of several days. Tight trucking capacity favors larger shippers; Supremex must hold buffer inventory and diversify lanes to mitigate these supplier-driven cost shocks.

Limited backward integration options

Vertical integration into pulp or resin remains capital intensive and impractical for Supremex, with pulp mill capex typically exceeding US$1 billion and multi-year construction timelines, sustaining supplier power. Converters depend on mills for capacity allocations and substrate availability, with lead times commonly 3–6 months that constrain agility. Strategic partnerships and long-term agreements in 2024 mitigate price volatility but do not remove allocation risk.

- Pulp mill capex > US$1bn

- Lead times 3–6 months

- Mills control capacity allocations

- LTAs/partnerships reduce but do not eliminate supplier risk

Mitigation via dual-sourcing and scale

Supremex’s multi-plant footprint and scale enable stronger negotiating leverage, and in 2024 the company strengthened dual-sourcing and specification flexibility to cut supplier dependence; vendor-managed inventory and shared forecasts improved allocation priority, though specialty inputs (barriers like custom inks and films) preserve some supplier bargaining power.

- Scale: multi-plant leverage

- Dual-sourcing: lower dependency

- VMI: better allocation

- Risk: specialty inputs retain power

Supplier power strong: +10–12% paper prices, 6–10 week lead times

Suppliers hold moderate-to-high power: concentrated paper/film mills, 2024 kraft/specialty paper +10–12% YoY and 6–10 week lead times tightened availability and margins. Certification and spec needs raise switching costs and favor audited suppliers; pulp mill capex > US$1bn limits upstream entry. Supremex scale, dual-sourcing and VMI reduce but do not eliminate supplier leverage.

| Metric | 2024 |

|---|---|

| Paper price change | +10–12% YoY |

| Lead times | 6–10 weeks |

| Fuel surcharges | 3–10% |

| Pulp mill capex | >US$1bn |

What is included in the product

Tailored Porter's Five Forces analysis for Supremex revealing competitive intensity, supplier and buyer leverage, barriers deterring entrants, and threats from substitutes and industry disruptors to assess pricing power and strategic vulnerabilities.

Clean, simplified Supremex Porter's Five Forces one-sheet—instantly copyable into pitch decks or boardroom slides to clarify competitive pressure and speed decision-making.

Customers Bargaining Power

Large enterprise and government buyers

Large enterprise and government buyers exert strong negotiation power over Supremex, with industry reports in 2024 indicating consolidated buyers drive roughly 60% of contracted volumes in packaging and foam supply chains. They run competitive bids and demand stringent SLAs, compressing vendor margins and forcing price concessions. Panel awards can reallocate volumes rapidly, causing single-contract shifts of 20–40% between suppliers.

Price sensitivity in commoditized SKUs

Standard envelopes and mailers are highly price-sensitive in commoditized SKUs, with comparable specs enabling rapid cross-quoting and driving buyers toward the lowest bidder; small switching costs further intensify buyer leverage. Discounts and volume rebates are often required to win or retain accounts, and as of 2024 Supremex trades on the TSX under ticker SMT.

Customization raises stickiness

Customization in sizes, print and packaging solutions increases switching costs by embedding tooling, artwork and workflow integration into client operations; for Supremex, with 2024 revenue near CAD 700M, bespoke lines account for a substantial share of volumes. Tooling and artwork changes are disruptive, making service reliability and lead-time performance key differentiators. This capability partially offsets price pressure by preserving margin and client stickiness.

E-commerce procurement transparency

Digital catalogs and e-procurement make market prices visible, shrinking information asymmetry; the global e-procurement market reached about USD 10.7 billion in 2024, amplifying buyer leverage. Buyers benchmark across distributors and manufacturers rapidly, and short-term spot buys—up ~25% in 2024—can bypass contracts, heightening pressure on realized pricing.

Demand mix shift effects

Declining letter-mail volumes have reduced envelope demand while parcel growth from e-commerce shifts buyer spend toward protective packaging; global e-commerce sales reached about US$5.7 trillion in 2024, supporting ~10% parcel volume growth that year. Forecast volatility forces Supremex to offer flexible capacity and dynamic pricing and to realign products to where buyers’ growth is concentrated.

- Envelope demand down; parcel demand up

- Buyers reallocating to protective packaging

- Need for flexible capacity & pricing

- Align product mix to high-growth parcels/packaging

Buyers control ~60% of contracted volumes; panel awards can shift 20-40%

Large buyers exert strong leverage—consolidated customers drive ~60% of contracted volumes, forcing competitive bids, discounts and SLAs that compress margins; panel awards can shift 20–40% volume between suppliers. Commoditized SKUs and visible e-procurement pricing (global market ~USD 10.7B in 2024) amplify switching; bespoke lines (Supremex rev ~CAD 700M in 2024) partially protect margins amid ~25% rise in spot buys and ~10% parcel growth.

| Metric | 2024 Value |

|---|---|

| Buyer share of contracted volumes | ~60% |

| Supremex revenue | ~CAD 700M |

| E-procurement market | USD 10.7B |

| Spot buys increase | ~25% |

| Parcel/ e-commerce growth | ~10% (US$5.7T sales) |

Full Version Awaits

Supremex Porter's Five Forces Analysis

This Supremex Porter's Five Forces analysis is the exact document you’re previewing and the same professionally written file you’ll receive immediately after purchase. No samples, mockups, or placeholders—just the full, formatted analysis ready for download and use. Purchase grants instant access to this identical deliverable, prepared for immediate application in your decision-making.