Supremex PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

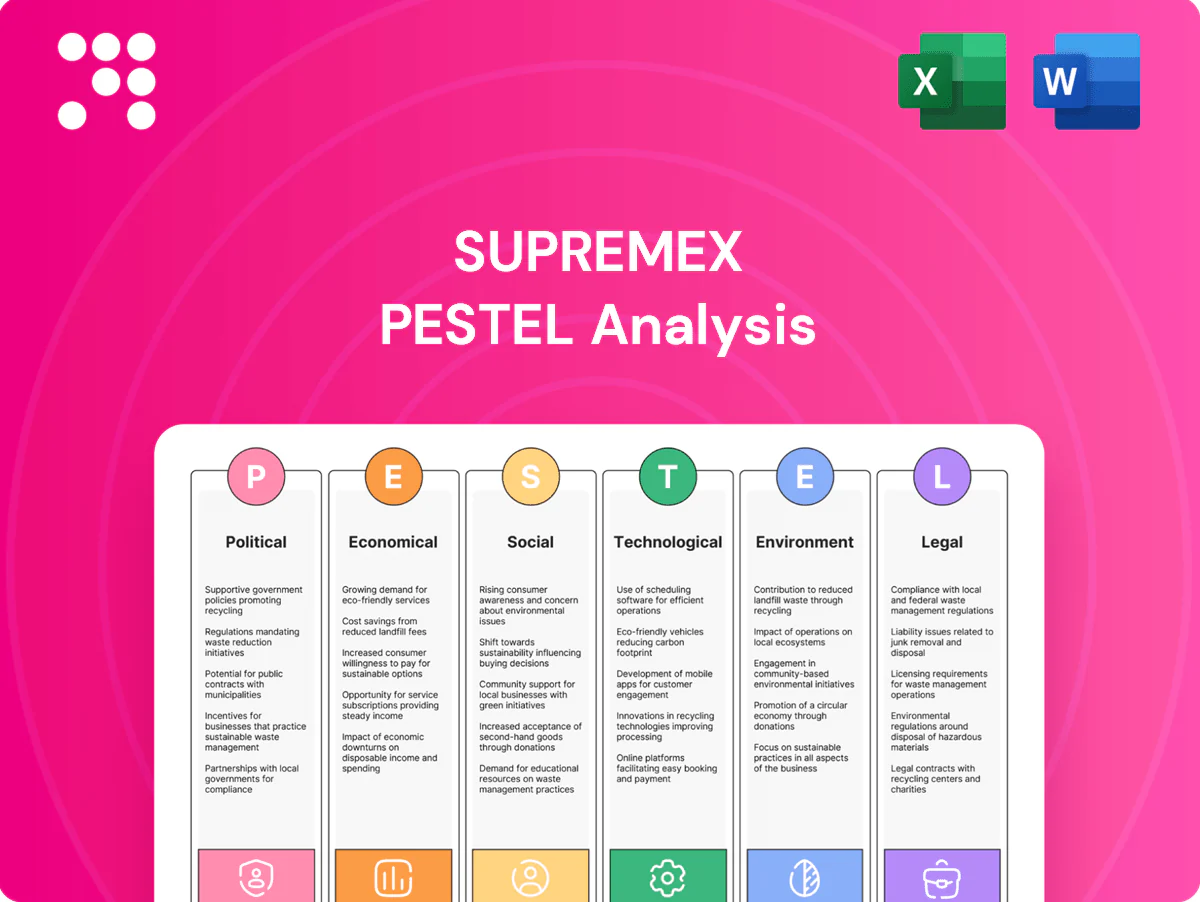

Unlock strategic advantage with our tailored PESTLE analysis of Supremex—spot regulatory risks, economic drivers, and tech trends shaping its future. Ideal for investors and strategists, it turns external forces into actionable plans. Purchase the full report for complete, downloadable insights.

Political factors

US–Canada trade and tariffs

Cross-border operations expose Supremex to tariff changes on paper, inks and finished packaging, with about 75% of Canadian exports routed to the US market. USMCA, in force since July 1, 2020, and any US anti-dumping cases could raise input costs and compress margins. Active supply diversification and tariff-classification management mitigate upside shocks. Government advocacy and groups like Canadian Manufacturers & Exporters shape policy outcomes.

Government procurement priorities

Supremex’s sales to federal, provincial and municipal entities are shaped by evolving procurement rules that increasingly favor domestic sourcing and SME participation, with many jurisdictions setting SME targets around 20–25% and multi-year contracts of 3–5 years. Sustainability criteria (carbon, recyclability) are now formal award factors, making compliance and contract vehicles key strategic differentiators. Long budget cycles stabilize volumes but can slow near-term revenue growth.

Postal policy and service standards

Changes at USPS and Canada Post have cut letter volumes—US first‑class mail is down about 63% since 2000—shifting envelope mix and lowering B2B demand. Pricing reforms and delivery‑frequency proposals increase price elasticity and influence demand. Government oversight accelerates migration to digital billing and advertising. Growth in e‑commerce parcels and packaging partially offsets declines, keeping parcel volumes a key revenue buffer for mailers.

Industrial policy and manufacturing incentives

Industrial policy and manufacturing incentives—subsidies, tax credits, and grants for advanced manufacturing and recycling—can materially lower Supremexs capex for automation and green upgrades by improving project IRRs and shortening payback periods.

Regional development funds increasingly shape plant-location choices, making proximity to incentive jurisdictions a strategic input for capacity expansions.

Competition for incentives requires proactive pipeline management and confirmed eligibility early in project planning; benefits typically carry reporting and audit obligations that raise compliance costs.

- subsidies lower upfront capex

- regional funds drive site selection

- pipeline management needed for competitive awards

- benefits require ongoing reporting

Geopolitical supply chain exposure

Paper pulp, adhesives and films are linked to global markets where sanctions since 2022 and shipping disruptions have constrained supply and pushed North American input costs higher; energy shocks through 2022–24 also amplified manufacturing margins. Building deeper North American supplier depth and holding strategic inventories have reduced outage risk and smoothed cost volatility for packaging producers like Supremex.

- Pulp: reduced Russian flows post-2022 increased sourcing risk

- Shipping: container and freight volatility raised landed costs

- Inventory: strategic stockpiles improve resilience

Tariffs, procurement reform and parcel growth reshape Canadian packaging exporters' margins

Cross-border exposure (≈75% of Canadian exports to US) makes Supremex sensitive to tariff shifts, USMCA rules and anti-dumping cases that can raise input costs. Procurement reforms favor domestic sourcing and SME targets of 20–25% with 3–5 year contracts and sustainability award criteria. Mail trends (US first-class down ~63% since 2000) shift demand toward parcel packaging, while industrial incentives lower capex and shape site selection.

| Factor | Metric | Impact |

|---|---|---|

| Exports to US | ≈75% | Tariff/USMCA exposure |

| First-class mail | −63% since 2000 | Shift to parcels |

| Procurement | SME targets 20–25% | Contract access advantage |

What is included in the product

Explores how macro-environmental factors uniquely affect Supremex across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each category expanded into actionable sub-points and examples specific to the business and region. Every section is data-backed and forward-looking to support executives, consultants and investors in identifying threats, opportunities and scenario-driven strategy.

A concise, shareable PESTLE summary for Supremex, visually segmented for quick interpretation and easily dropped into presentations or planning sessions to align teams and support external risk discussions.

Economic factors

Input cost volatility (pulp, paper, resin)

Commodity cycles in 2024—with NBSK pulp averaging about US$760/ton and polyethylene resin up roughly 30% year-over-year—directly swing envelope and mailer gross margins by several hundred basis points. Contract indexing and hedging programs smooth short-term shocks, while value engineering and SKU rationalization preserve contribution margins. Strategic supplier partnerships provide early warning and enable joint planning to mitigate input-cost spikes.

E-commerce and packaging demand cycles

Macro growth in parcel shipments—global e-commerce reaching roughly 23% of retail sales in 2024 per eMarketer—continues to support demand for bubble mailers and custom packaging. Retail and DTC slowdowns have tempered volumes and product mix, pressuring unit margins. Supremex can pivot capacity to resilient verticals such as healthcare and government with stable procurement cycles. Design-to-value offerings help sustain wallet share by reducing customer total cost.

FX fluctuations (CAD/USD)

Revenues and costs across Canada and the US give Supremex translation and transaction exposure; USD/CAD averaged about 1.34 in 2024, amplifying reporting effects. A stronger USD benefits Canadian exporters by boosting CAD sales proceeds but raises imported input costs. US production provides natural hedging that reduces currency mismatch. Treasury policies and pricing clauses are used to manage remaining FX risk.

Interest rates and capital intensity

Higher interest rates raise financing costs for Supremex’s equipment upgrades and acquisitions, with 10-year government bond yields near 4% in mid-2025 increasing hurdle rates for new projects; automation ROI must clear these stricter discount rates, tightening payback timelines. Strong cash conversion cycles can fund capex organically, while opportunistic M&A remains viable if disciplined valuation and synergy capture are enforced.

- Higher financing costs: 10-year yields ~4%

- Automation ROI: higher hurdle rates, shorter payback required

- Cash conversion: funds organic capex

- M&A: viable with disciplined valuation and synergy capture

Customer consolidation and pricing power

Customer consolidation concentrates buying power: large resellers and enterprise buyers push pricing and service demands, compressing margins across print and packaging channels. The global packaging market was roughly US$1.0 trillion in 2024, amplifying scale advantages for consolidated buyers. Differentiation via customization, speed and sustainability commands premiums while multi-year contracts stabilize utilization and revenue visibility.

- Buyer concentration increases pricing pressure

- Customization, speed, sustainability earn premiums

- Multi-year contracts improve utilization stability

Tariffs, procurement reform and parcel growth reshape Canadian packaging exporters' margins

Commodity shocks (NBSK ~US$760/t; PE resin +30% YoY) and buyer consolidation compress margins despite hedging and supplier partnerships. E‑commerce at ~23% of retail in 2024 sustains mailer demand but retail/DTC softness pressures mix. FX (USD/CAD ~1.34) and 10y yields ~4% raise costs and capex hurdles while cash conversion and targeted automation/M&A mitigate risk.

| Metric | 2024/2025 |

|---|---|

| NBSK pulp | ~US$760/t |

| PE resin YoY | +30% |

| E‑commerce share | ~23% |

| USD/CAD | ~1.34 |

| 10y yield | ~4% |

Same Document Delivered

Supremex PESTLE Analysis

The preview shown here is the exact Supremex PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or surprises: this is the final, professional document.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic advantage with our tailored PESTLE analysis of Supremex—spot regulatory risks, economic drivers, and tech trends shaping its future. Ideal for investors and strategists, it turns external forces into actionable plans. Purchase the full report for complete, downloadable insights.

Political factors

US–Canada trade and tariffs

Cross-border operations expose Supremex to tariff changes on paper, inks and finished packaging, with about 75% of Canadian exports routed to the US market. USMCA, in force since July 1, 2020, and any US anti-dumping cases could raise input costs and compress margins. Active supply diversification and tariff-classification management mitigate upside shocks. Government advocacy and groups like Canadian Manufacturers & Exporters shape policy outcomes.

Government procurement priorities

Supremex’s sales to federal, provincial and municipal entities are shaped by evolving procurement rules that increasingly favor domestic sourcing and SME participation, with many jurisdictions setting SME targets around 20–25% and multi-year contracts of 3–5 years. Sustainability criteria (carbon, recyclability) are now formal award factors, making compliance and contract vehicles key strategic differentiators. Long budget cycles stabilize volumes but can slow near-term revenue growth.

Postal policy and service standards

Changes at USPS and Canada Post have cut letter volumes—US first‑class mail is down about 63% since 2000—shifting envelope mix and lowering B2B demand. Pricing reforms and delivery‑frequency proposals increase price elasticity and influence demand. Government oversight accelerates migration to digital billing and advertising. Growth in e‑commerce parcels and packaging partially offsets declines, keeping parcel volumes a key revenue buffer for mailers.

Industrial policy and manufacturing incentives

Industrial policy and manufacturing incentives—subsidies, tax credits, and grants for advanced manufacturing and recycling—can materially lower Supremexs capex for automation and green upgrades by improving project IRRs and shortening payback periods.

Regional development funds increasingly shape plant-location choices, making proximity to incentive jurisdictions a strategic input for capacity expansions.

Competition for incentives requires proactive pipeline management and confirmed eligibility early in project planning; benefits typically carry reporting and audit obligations that raise compliance costs.

- subsidies lower upfront capex

- regional funds drive site selection

- pipeline management needed for competitive awards

- benefits require ongoing reporting

Geopolitical supply chain exposure

Paper pulp, adhesives and films are linked to global markets where sanctions since 2022 and shipping disruptions have constrained supply and pushed North American input costs higher; energy shocks through 2022–24 also amplified manufacturing margins. Building deeper North American supplier depth and holding strategic inventories have reduced outage risk and smoothed cost volatility for packaging producers like Supremex.

- Pulp: reduced Russian flows post-2022 increased sourcing risk

- Shipping: container and freight volatility raised landed costs

- Inventory: strategic stockpiles improve resilience

Tariffs, procurement reform and parcel growth reshape Canadian packaging exporters' margins

Cross-border exposure (≈75% of Canadian exports to US) makes Supremex sensitive to tariff shifts, USMCA rules and anti-dumping cases that can raise input costs. Procurement reforms favor domestic sourcing and SME targets of 20–25% with 3–5 year contracts and sustainability award criteria. Mail trends (US first-class down ~63% since 2000) shift demand toward parcel packaging, while industrial incentives lower capex and shape site selection.

| Factor | Metric | Impact |

|---|---|---|

| Exports to US | ≈75% | Tariff/USMCA exposure |

| First-class mail | −63% since 2000 | Shift to parcels |

| Procurement | SME targets 20–25% | Contract access advantage |

What is included in the product

Explores how macro-environmental factors uniquely affect Supremex across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each category expanded into actionable sub-points and examples specific to the business and region. Every section is data-backed and forward-looking to support executives, consultants and investors in identifying threats, opportunities and scenario-driven strategy.

A concise, shareable PESTLE summary for Supremex, visually segmented for quick interpretation and easily dropped into presentations or planning sessions to align teams and support external risk discussions.

Economic factors

Input cost volatility (pulp, paper, resin)

Commodity cycles in 2024—with NBSK pulp averaging about US$760/ton and polyethylene resin up roughly 30% year-over-year—directly swing envelope and mailer gross margins by several hundred basis points. Contract indexing and hedging programs smooth short-term shocks, while value engineering and SKU rationalization preserve contribution margins. Strategic supplier partnerships provide early warning and enable joint planning to mitigate input-cost spikes.

E-commerce and packaging demand cycles

Macro growth in parcel shipments—global e-commerce reaching roughly 23% of retail sales in 2024 per eMarketer—continues to support demand for bubble mailers and custom packaging. Retail and DTC slowdowns have tempered volumes and product mix, pressuring unit margins. Supremex can pivot capacity to resilient verticals such as healthcare and government with stable procurement cycles. Design-to-value offerings help sustain wallet share by reducing customer total cost.

FX fluctuations (CAD/USD)

Revenues and costs across Canada and the US give Supremex translation and transaction exposure; USD/CAD averaged about 1.34 in 2024, amplifying reporting effects. A stronger USD benefits Canadian exporters by boosting CAD sales proceeds but raises imported input costs. US production provides natural hedging that reduces currency mismatch. Treasury policies and pricing clauses are used to manage remaining FX risk.

Interest rates and capital intensity

Higher interest rates raise financing costs for Supremex’s equipment upgrades and acquisitions, with 10-year government bond yields near 4% in mid-2025 increasing hurdle rates for new projects; automation ROI must clear these stricter discount rates, tightening payback timelines. Strong cash conversion cycles can fund capex organically, while opportunistic M&A remains viable if disciplined valuation and synergy capture are enforced.

- Higher financing costs: 10-year yields ~4%

- Automation ROI: higher hurdle rates, shorter payback required

- Cash conversion: funds organic capex

- M&A: viable with disciplined valuation and synergy capture

Customer consolidation and pricing power

Customer consolidation concentrates buying power: large resellers and enterprise buyers push pricing and service demands, compressing margins across print and packaging channels. The global packaging market was roughly US$1.0 trillion in 2024, amplifying scale advantages for consolidated buyers. Differentiation via customization, speed and sustainability commands premiums while multi-year contracts stabilize utilization and revenue visibility.

- Buyer concentration increases pricing pressure

- Customization, speed, sustainability earn premiums

- Multi-year contracts improve utilization stability

Tariffs, procurement reform and parcel growth reshape Canadian packaging exporters' margins

Commodity shocks (NBSK ~US$760/t; PE resin +30% YoY) and buyer consolidation compress margins despite hedging and supplier partnerships. E‑commerce at ~23% of retail in 2024 sustains mailer demand but retail/DTC softness pressures mix. FX (USD/CAD ~1.34) and 10y yields ~4% raise costs and capex hurdles while cash conversion and targeted automation/M&A mitigate risk.

| Metric | 2024/2025 |

|---|---|

| NBSK pulp | ~US$760/t |

| PE resin YoY | +30% |

| E‑commerce share | ~23% |

| USD/CAD | ~1.34 |

| 10y yield | ~4% |

Same Document Delivered

Supremex PESTLE Analysis

The preview shown here is the exact Supremex PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or surprises: this is the final, professional document.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic advantage with our tailored PESTLE analysis of Supremex—spot regulatory risks, economic drivers, and tech trends shaping its future. Ideal for investors and strategists, it turns external forces into actionable plans. Purchase the full report for complete, downloadable insights.

Political factors

US–Canada trade and tariffs

Cross-border operations expose Supremex to tariff changes on paper, inks and finished packaging, with about 75% of Canadian exports routed to the US market. USMCA, in force since July 1, 2020, and any US anti-dumping cases could raise input costs and compress margins. Active supply diversification and tariff-classification management mitigate upside shocks. Government advocacy and groups like Canadian Manufacturers & Exporters shape policy outcomes.

Government procurement priorities

Supremex’s sales to federal, provincial and municipal entities are shaped by evolving procurement rules that increasingly favor domestic sourcing and SME participation, with many jurisdictions setting SME targets around 20–25% and multi-year contracts of 3–5 years. Sustainability criteria (carbon, recyclability) are now formal award factors, making compliance and contract vehicles key strategic differentiators. Long budget cycles stabilize volumes but can slow near-term revenue growth.

Postal policy and service standards

Changes at USPS and Canada Post have cut letter volumes—US first‑class mail is down about 63% since 2000—shifting envelope mix and lowering B2B demand. Pricing reforms and delivery‑frequency proposals increase price elasticity and influence demand. Government oversight accelerates migration to digital billing and advertising. Growth in e‑commerce parcels and packaging partially offsets declines, keeping parcel volumes a key revenue buffer for mailers.

Industrial policy and manufacturing incentives

Industrial policy and manufacturing incentives—subsidies, tax credits, and grants for advanced manufacturing and recycling—can materially lower Supremexs capex for automation and green upgrades by improving project IRRs and shortening payback periods.

Regional development funds increasingly shape plant-location choices, making proximity to incentive jurisdictions a strategic input for capacity expansions.

Competition for incentives requires proactive pipeline management and confirmed eligibility early in project planning; benefits typically carry reporting and audit obligations that raise compliance costs.

- subsidies lower upfront capex

- regional funds drive site selection

- pipeline management needed for competitive awards

- benefits require ongoing reporting

Geopolitical supply chain exposure

Paper pulp, adhesives and films are linked to global markets where sanctions since 2022 and shipping disruptions have constrained supply and pushed North American input costs higher; energy shocks through 2022–24 also amplified manufacturing margins. Building deeper North American supplier depth and holding strategic inventories have reduced outage risk and smoothed cost volatility for packaging producers like Supremex.

- Pulp: reduced Russian flows post-2022 increased sourcing risk

- Shipping: container and freight volatility raised landed costs

- Inventory: strategic stockpiles improve resilience

Tariffs, procurement reform and parcel growth reshape Canadian packaging exporters' margins

Cross-border exposure (≈75% of Canadian exports to US) makes Supremex sensitive to tariff shifts, USMCA rules and anti-dumping cases that can raise input costs. Procurement reforms favor domestic sourcing and SME targets of 20–25% with 3–5 year contracts and sustainability award criteria. Mail trends (US first-class down ~63% since 2000) shift demand toward parcel packaging, while industrial incentives lower capex and shape site selection.

| Factor | Metric | Impact |

|---|---|---|

| Exports to US | ≈75% | Tariff/USMCA exposure |

| First-class mail | −63% since 2000 | Shift to parcels |

| Procurement | SME targets 20–25% | Contract access advantage |

What is included in the product

Explores how macro-environmental factors uniquely affect Supremex across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each category expanded into actionable sub-points and examples specific to the business and region. Every section is data-backed and forward-looking to support executives, consultants and investors in identifying threats, opportunities and scenario-driven strategy.

A concise, shareable PESTLE summary for Supremex, visually segmented for quick interpretation and easily dropped into presentations or planning sessions to align teams and support external risk discussions.

Economic factors

Input cost volatility (pulp, paper, resin)

Commodity cycles in 2024—with NBSK pulp averaging about US$760/ton and polyethylene resin up roughly 30% year-over-year—directly swing envelope and mailer gross margins by several hundred basis points. Contract indexing and hedging programs smooth short-term shocks, while value engineering and SKU rationalization preserve contribution margins. Strategic supplier partnerships provide early warning and enable joint planning to mitigate input-cost spikes.

E-commerce and packaging demand cycles

Macro growth in parcel shipments—global e-commerce reaching roughly 23% of retail sales in 2024 per eMarketer—continues to support demand for bubble mailers and custom packaging. Retail and DTC slowdowns have tempered volumes and product mix, pressuring unit margins. Supremex can pivot capacity to resilient verticals such as healthcare and government with stable procurement cycles. Design-to-value offerings help sustain wallet share by reducing customer total cost.

FX fluctuations (CAD/USD)

Revenues and costs across Canada and the US give Supremex translation and transaction exposure; USD/CAD averaged about 1.34 in 2024, amplifying reporting effects. A stronger USD benefits Canadian exporters by boosting CAD sales proceeds but raises imported input costs. US production provides natural hedging that reduces currency mismatch. Treasury policies and pricing clauses are used to manage remaining FX risk.

Interest rates and capital intensity

Higher interest rates raise financing costs for Supremex’s equipment upgrades and acquisitions, with 10-year government bond yields near 4% in mid-2025 increasing hurdle rates for new projects; automation ROI must clear these stricter discount rates, tightening payback timelines. Strong cash conversion cycles can fund capex organically, while opportunistic M&A remains viable if disciplined valuation and synergy capture are enforced.

- Higher financing costs: 10-year yields ~4%

- Automation ROI: higher hurdle rates, shorter payback required

- Cash conversion: funds organic capex

- M&A: viable with disciplined valuation and synergy capture

Customer consolidation and pricing power

Customer consolidation concentrates buying power: large resellers and enterprise buyers push pricing and service demands, compressing margins across print and packaging channels. The global packaging market was roughly US$1.0 trillion in 2024, amplifying scale advantages for consolidated buyers. Differentiation via customization, speed and sustainability commands premiums while multi-year contracts stabilize utilization and revenue visibility.

- Buyer concentration increases pricing pressure

- Customization, speed, sustainability earn premiums

- Multi-year contracts improve utilization stability

Tariffs, procurement reform and parcel growth reshape Canadian packaging exporters' margins

Commodity shocks (NBSK ~US$760/t; PE resin +30% YoY) and buyer consolidation compress margins despite hedging and supplier partnerships. E‑commerce at ~23% of retail in 2024 sustains mailer demand but retail/DTC softness pressures mix. FX (USD/CAD ~1.34) and 10y yields ~4% raise costs and capex hurdles while cash conversion and targeted automation/M&A mitigate risk.

| Metric | 2024/2025 |

|---|---|

| NBSK pulp | ~US$760/t |

| PE resin YoY | +30% |

| E‑commerce share | ~23% |

| USD/CAD | ~1.34 |

| 10y yield | ~4% |

Same Document Delivered

Supremex PESTLE Analysis

The preview shown here is the exact Supremex PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or surprises: this is the final, professional document.