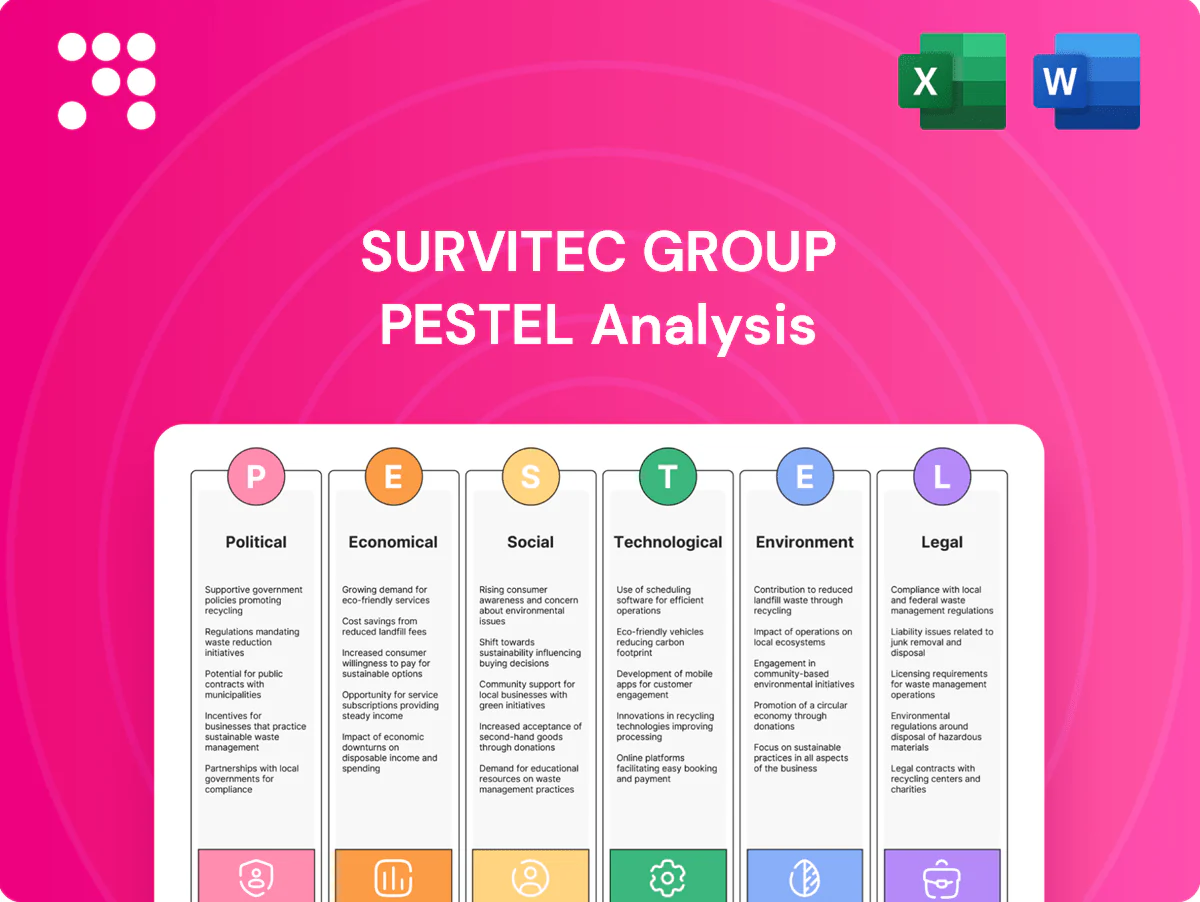

Survitec Group PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how geopolitical shifts, safety regulations, and sustainability trends are reshaping Survitec Group’s market position and product strategy. Our PESTLE distills critical risks and opportunities into clear, actionable insights for investors and strategists. Download the full analysis now to get the complete, ready-to-use breakdown and stay ahead.

Political factors

Defense spending and procurement cycles

Government defense budgets drive demand for aviation and military survival equipment as global military spending reached about $2.24 trillion in 2023 (US $858 billion, China $293 billion), underpinning procurement for survival systems. Multi‑year procurement cycles (typically 3–7 years) give revenue visibility but extend sales lead times. Shifts in geopolitical priorities reallocate funds across maritime, aviation and land programs, so Survitec must align bids to evolving defense modernization roadmaps.

Maritime policy and flag-state oversight

International conventions such as SOLAS, enforced through the IMO (175 Member States as of 2024), set mandatory carriage standards that directly determine demand for Survitec life‑saving appliances. Variations in flag‑state inspection regimes and port state control (Paris/Tokyo/USCG) enforcement intensity alter service frequency and scope, affecting aftermarket revenue. Policy tightening and retrofit mandates expand addressable markets by forcing upgrades and shaping service‑network deployment across major ports.

Trade policy, tariffs, and localization

Tariffs on technical textiles, electronics and components — global applied MFN tariffs average about 2.7% — can compress Survitec’s margins and raise landed costs on lifesaving gear. Localization policies and offset rules, often requiring 30–50% local content in defense and energy contracts, influence where Survitec locates manufacturing and service hubs. Regional content rules can be decisive in awards; diversifying suppliers and assembly reduces exposure to tariffs and quota shocks.

Geopolitical instability and sanctions

Geopolitical instability and sanctions disrupt Survitec Group supply chains and can block sales to flagged fleets or jurisdictions; routing volatility and port closures increase service-scheduling complexity. Migration crises (UNHCR 110 million displaced in 2023) and rising naval activity amid $2.2 trillion global defence spending (SIPRI 2023) can spike demand for life‑saving and evacuation equipment. Compliance teams must track evolving sanction lists and end‑use controls in real time.

- Sanctions: restrict market access, raise KYC costs

- Supply chains: longer lead times, higher freight costs

- Demand shocks: migration/naval ops increase PPE/raft demand

- Compliance: continuous monitoring of lists and end‑use rules

Public-sector safety initiatives

Global defense spend $2.24T fuels multiyear procurement, SOLAS retrofits

Rising government defense spending (global ~$2.24T in 2023; US $858B, China $293B) supports multiyear procurement for survival systems and gives revenue visibility. IMO/SOLAS (175 Member States, 2024) and SOLAS retrofits mandate lifesaving appliances, boosting aftermarket. Tariffs (global MFN ~2.7%), localization/offsets (30–50%) and sanctions raise costs, shape manufacturing and restrict market access.

| Indicator | Value |

|---|---|

| Global defence spend 2023 | $2.24T |

| IMO members (2024) | 175 |

| Horizon Europe 2021–27 | €95.5B |

What is included in the product

Explores how macro-environmental factors uniquely affect Survitec Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples. Designed for executives and investors to identify strategic risks, opportunities and scenario-led actions.

A succinct, category-segmented PESTLE summary of Survitec Group that highlights external risks and opportunities for quick insertion into presentations, collaborative planning, or client reports; editable notes support regional or product-line context and easy sharing across teams.

Economic factors

Shipping and offshore energy cycles

Commercial shipping volumes drive newbuild and retrofit orders, with UNCTAD reporting modest seaborne trade growth of about 1.5% in 2023, directly influencing OEM capex for safety systems. Downturns suppress newbuild capex but sustain service and compliance-driven revenue streams for life‑saving equipment providers. Global offshore wind pipeline exceeds 300 GW (GWEC 2024), adding counter‑cyclical demand for PPE and rescue systems. A balanced portfolio across merchant, offshore E&P and renewables smooths Survitec’s revenue volatility.

Inflation and input cost volatility

Textiles, foams, metals and electronics have seen large price swings that squeeze Survitec margins; energy shocks (EU gas spiking up to 300% in 2022) and raw-material volatility persisted into 2024. Index-linked contracts and value engineering have been used to protect profitability, while inventory buffers and hedging reduced exposure as container freight rates fell roughly 70% from 2022 peaks by 2024. Mandatory maritime safety compliance timelines sustain pricing power.

Foreign exchange exposure

Survitec Group faces translation and transaction risk from global sales billed in USD, EUR, GBP and other currencies, while multi-currency suppliers complicate COGS and margin management. Natural hedging from matched costs and revenues limits residual exposure, and centralized treasury policies plus use of forwards and options are used to smooth earnings variability.

Aftermarket and recurring revenues

Aftermarket inspection, servicing and recertification for Survitec are anchored by SOLAS-mandated annual liferaft servicing (12-month intervals), creating predictable, regulatory-driven cash flows that persist independent of macro cycles. Digital scheduling and subscription-style service agreements boost retention and allow smoothing of revenue recognition. Higher installed-base density improves route efficiency, lowering unit servicing costs and lifting margins.

- Regulatory lock-in: SOLAS 12-month liferaft servicing

- Revenue type: predictable recurring inspection/recertification

- Retention: digital scheduling/subscription models

- Margin driver: higher installed-base density → route efficiency

Emerging market fleet expansion

Emerging market fleet expansion in Asia, the Middle East and Africa increases demand for Survitec’s survival equipment, with Asia-Pacific newbuilds accounting for circa 90% of global shipbuilding activity in 2024. Port infrastructure upgrades and rising regional compliance create higher-spec service opportunities. Local partnerships accelerate market access and can reduce logistics lead times and costs materially. Price-sensitive buyers require tiered offerings that maintain SOLAS/MED compliance.

Global defense spend $2.24T fuels multiyear procurement, SOLAS retrofits

Moderate seaborne trade growth (UNCTAD ~1.5% 2023) and a 300+ GW offshore wind pipeline (GWEC 2024) create mixed demand for newbuilds and countercyclical PPE/rescue sales. Raw-material and energy shocks (EU gas up ~300% in 2022) plus container rates down ~70% by 2024 press margins; index‑linked contracts and hedging mitigate. SOLAS 12‑month servicing and Asia‑Pacific ~90% newbuilds (2024) anchor recurring revenues.

| Metric | Value |

|---|---|

| Seaborne trade growth (2023) | ~1.5% |

| Offshore wind pipeline (2024) | >300 GW |

| Asia‑Pacific newbuilds (2024) | ~90% |

| Container rates change (2022→2024) | ≈-70% |

| EU gas spike (2022) | ~+300% |

Full Version Awaits

Survitec Group PESTLE Analysis

This Survitec Group PESTLE Analysis delivers a concise evaluation of political, economic, social, technological, legal, and environmental factors affecting the business, plus strategic implications for stakeholders. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Actionable insights and clear structure make it immediately deployable for decision-making.

Skip the Research. Get the Strategy.

Discover how geopolitical shifts, safety regulations, and sustainability trends are reshaping Survitec Group’s market position and product strategy. Our PESTLE distills critical risks and opportunities into clear, actionable insights for investors and strategists. Download the full analysis now to get the complete, ready-to-use breakdown and stay ahead.

Political factors

Defense spending and procurement cycles

Government defense budgets drive demand for aviation and military survival equipment as global military spending reached about $2.24 trillion in 2023 (US $858 billion, China $293 billion), underpinning procurement for survival systems. Multi‑year procurement cycles (typically 3–7 years) give revenue visibility but extend sales lead times. Shifts in geopolitical priorities reallocate funds across maritime, aviation and land programs, so Survitec must align bids to evolving defense modernization roadmaps.

Maritime policy and flag-state oversight

International conventions such as SOLAS, enforced through the IMO (175 Member States as of 2024), set mandatory carriage standards that directly determine demand for Survitec life‑saving appliances. Variations in flag‑state inspection regimes and port state control (Paris/Tokyo/USCG) enforcement intensity alter service frequency and scope, affecting aftermarket revenue. Policy tightening and retrofit mandates expand addressable markets by forcing upgrades and shaping service‑network deployment across major ports.

Trade policy, tariffs, and localization

Tariffs on technical textiles, electronics and components — global applied MFN tariffs average about 2.7% — can compress Survitec’s margins and raise landed costs on lifesaving gear. Localization policies and offset rules, often requiring 30–50% local content in defense and energy contracts, influence where Survitec locates manufacturing and service hubs. Regional content rules can be decisive in awards; diversifying suppliers and assembly reduces exposure to tariffs and quota shocks.

Geopolitical instability and sanctions

Geopolitical instability and sanctions disrupt Survitec Group supply chains and can block sales to flagged fleets or jurisdictions; routing volatility and port closures increase service-scheduling complexity. Migration crises (UNHCR 110 million displaced in 2023) and rising naval activity amid $2.2 trillion global defence spending (SIPRI 2023) can spike demand for life‑saving and evacuation equipment. Compliance teams must track evolving sanction lists and end‑use controls in real time.

- Sanctions: restrict market access, raise KYC costs

- Supply chains: longer lead times, higher freight costs

- Demand shocks: migration/naval ops increase PPE/raft demand

- Compliance: continuous monitoring of lists and end‑use rules

Public-sector safety initiatives

Global defense spend $2.24T fuels multiyear procurement, SOLAS retrofits

Rising government defense spending (global ~$2.24T in 2023; US $858B, China $293B) supports multiyear procurement for survival systems and gives revenue visibility. IMO/SOLAS (175 Member States, 2024) and SOLAS retrofits mandate lifesaving appliances, boosting aftermarket. Tariffs (global MFN ~2.7%), localization/offsets (30–50%) and sanctions raise costs, shape manufacturing and restrict market access.

| Indicator | Value |

|---|---|

| Global defence spend 2023 | $2.24T |

| IMO members (2024) | 175 |

| Horizon Europe 2021–27 | €95.5B |

What is included in the product

Explores how macro-environmental factors uniquely affect Survitec Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples. Designed for executives and investors to identify strategic risks, opportunities and scenario-led actions.

A succinct, category-segmented PESTLE summary of Survitec Group that highlights external risks and opportunities for quick insertion into presentations, collaborative planning, or client reports; editable notes support regional or product-line context and easy sharing across teams.

Economic factors

Shipping and offshore energy cycles

Commercial shipping volumes drive newbuild and retrofit orders, with UNCTAD reporting modest seaborne trade growth of about 1.5% in 2023, directly influencing OEM capex for safety systems. Downturns suppress newbuild capex but sustain service and compliance-driven revenue streams for life‑saving equipment providers. Global offshore wind pipeline exceeds 300 GW (GWEC 2024), adding counter‑cyclical demand for PPE and rescue systems. A balanced portfolio across merchant, offshore E&P and renewables smooths Survitec’s revenue volatility.

Inflation and input cost volatility

Textiles, foams, metals and electronics have seen large price swings that squeeze Survitec margins; energy shocks (EU gas spiking up to 300% in 2022) and raw-material volatility persisted into 2024. Index-linked contracts and value engineering have been used to protect profitability, while inventory buffers and hedging reduced exposure as container freight rates fell roughly 70% from 2022 peaks by 2024. Mandatory maritime safety compliance timelines sustain pricing power.

Foreign exchange exposure

Survitec Group faces translation and transaction risk from global sales billed in USD, EUR, GBP and other currencies, while multi-currency suppliers complicate COGS and margin management. Natural hedging from matched costs and revenues limits residual exposure, and centralized treasury policies plus use of forwards and options are used to smooth earnings variability.

Aftermarket and recurring revenues

Aftermarket inspection, servicing and recertification for Survitec are anchored by SOLAS-mandated annual liferaft servicing (12-month intervals), creating predictable, regulatory-driven cash flows that persist independent of macro cycles. Digital scheduling and subscription-style service agreements boost retention and allow smoothing of revenue recognition. Higher installed-base density improves route efficiency, lowering unit servicing costs and lifting margins.

- Regulatory lock-in: SOLAS 12-month liferaft servicing

- Revenue type: predictable recurring inspection/recertification

- Retention: digital scheduling/subscription models

- Margin driver: higher installed-base density → route efficiency

Emerging market fleet expansion

Emerging market fleet expansion in Asia, the Middle East and Africa increases demand for Survitec’s survival equipment, with Asia-Pacific newbuilds accounting for circa 90% of global shipbuilding activity in 2024. Port infrastructure upgrades and rising regional compliance create higher-spec service opportunities. Local partnerships accelerate market access and can reduce logistics lead times and costs materially. Price-sensitive buyers require tiered offerings that maintain SOLAS/MED compliance.

Global defense spend $2.24T fuels multiyear procurement, SOLAS retrofits

Moderate seaborne trade growth (UNCTAD ~1.5% 2023) and a 300+ GW offshore wind pipeline (GWEC 2024) create mixed demand for newbuilds and countercyclical PPE/rescue sales. Raw-material and energy shocks (EU gas up ~300% in 2022) plus container rates down ~70% by 2024 press margins; index‑linked contracts and hedging mitigate. SOLAS 12‑month servicing and Asia‑Pacific ~90% newbuilds (2024) anchor recurring revenues.

| Metric | Value |

|---|---|

| Seaborne trade growth (2023) | ~1.5% |

| Offshore wind pipeline (2024) | >300 GW |

| Asia‑Pacific newbuilds (2024) | ~90% |

| Container rates change (2022→2024) | ≈-70% |

| EU gas spike (2022) | ~+300% |

Full Version Awaits

Survitec Group PESTLE Analysis

This Survitec Group PESTLE Analysis delivers a concise evaluation of political, economic, social, technological, legal, and environmental factors affecting the business, plus strategic implications for stakeholders. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Actionable insights and clear structure make it immediately deployable for decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Discover how geopolitical shifts, safety regulations, and sustainability trends are reshaping Survitec Group’s market position and product strategy. Our PESTLE distills critical risks and opportunities into clear, actionable insights for investors and strategists. Download the full analysis now to get the complete, ready-to-use breakdown and stay ahead.

Political factors

Defense spending and procurement cycles

Government defense budgets drive demand for aviation and military survival equipment as global military spending reached about $2.24 trillion in 2023 (US $858 billion, China $293 billion), underpinning procurement for survival systems. Multi‑year procurement cycles (typically 3–7 years) give revenue visibility but extend sales lead times. Shifts in geopolitical priorities reallocate funds across maritime, aviation and land programs, so Survitec must align bids to evolving defense modernization roadmaps.

Maritime policy and flag-state oversight

International conventions such as SOLAS, enforced through the IMO (175 Member States as of 2024), set mandatory carriage standards that directly determine demand for Survitec life‑saving appliances. Variations in flag‑state inspection regimes and port state control (Paris/Tokyo/USCG) enforcement intensity alter service frequency and scope, affecting aftermarket revenue. Policy tightening and retrofit mandates expand addressable markets by forcing upgrades and shaping service‑network deployment across major ports.

Trade policy, tariffs, and localization

Tariffs on technical textiles, electronics and components — global applied MFN tariffs average about 2.7% — can compress Survitec’s margins and raise landed costs on lifesaving gear. Localization policies and offset rules, often requiring 30–50% local content in defense and energy contracts, influence where Survitec locates manufacturing and service hubs. Regional content rules can be decisive in awards; diversifying suppliers and assembly reduces exposure to tariffs and quota shocks.

Geopolitical instability and sanctions

Geopolitical instability and sanctions disrupt Survitec Group supply chains and can block sales to flagged fleets or jurisdictions; routing volatility and port closures increase service-scheduling complexity. Migration crises (UNHCR 110 million displaced in 2023) and rising naval activity amid $2.2 trillion global defence spending (SIPRI 2023) can spike demand for life‑saving and evacuation equipment. Compliance teams must track evolving sanction lists and end‑use controls in real time.

- Sanctions: restrict market access, raise KYC costs

- Supply chains: longer lead times, higher freight costs

- Demand shocks: migration/naval ops increase PPE/raft demand

- Compliance: continuous monitoring of lists and end‑use rules

Public-sector safety initiatives

Global defense spend $2.24T fuels multiyear procurement, SOLAS retrofits

Rising government defense spending (global ~$2.24T in 2023; US $858B, China $293B) supports multiyear procurement for survival systems and gives revenue visibility. IMO/SOLAS (175 Member States, 2024) and SOLAS retrofits mandate lifesaving appliances, boosting aftermarket. Tariffs (global MFN ~2.7%), localization/offsets (30–50%) and sanctions raise costs, shape manufacturing and restrict market access.

| Indicator | Value |

|---|---|

| Global defence spend 2023 | $2.24T |

| IMO members (2024) | 175 |

| Horizon Europe 2021–27 | €95.5B |

What is included in the product

Explores how macro-environmental factors uniquely affect Survitec Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples. Designed for executives and investors to identify strategic risks, opportunities and scenario-led actions.

A succinct, category-segmented PESTLE summary of Survitec Group that highlights external risks and opportunities for quick insertion into presentations, collaborative planning, or client reports; editable notes support regional or product-line context and easy sharing across teams.

Economic factors

Shipping and offshore energy cycles

Commercial shipping volumes drive newbuild and retrofit orders, with UNCTAD reporting modest seaborne trade growth of about 1.5% in 2023, directly influencing OEM capex for safety systems. Downturns suppress newbuild capex but sustain service and compliance-driven revenue streams for life‑saving equipment providers. Global offshore wind pipeline exceeds 300 GW (GWEC 2024), adding counter‑cyclical demand for PPE and rescue systems. A balanced portfolio across merchant, offshore E&P and renewables smooths Survitec’s revenue volatility.

Inflation and input cost volatility

Textiles, foams, metals and electronics have seen large price swings that squeeze Survitec margins; energy shocks (EU gas spiking up to 300% in 2022) and raw-material volatility persisted into 2024. Index-linked contracts and value engineering have been used to protect profitability, while inventory buffers and hedging reduced exposure as container freight rates fell roughly 70% from 2022 peaks by 2024. Mandatory maritime safety compliance timelines sustain pricing power.

Foreign exchange exposure

Survitec Group faces translation and transaction risk from global sales billed in USD, EUR, GBP and other currencies, while multi-currency suppliers complicate COGS and margin management. Natural hedging from matched costs and revenues limits residual exposure, and centralized treasury policies plus use of forwards and options are used to smooth earnings variability.

Aftermarket and recurring revenues

Aftermarket inspection, servicing and recertification for Survitec are anchored by SOLAS-mandated annual liferaft servicing (12-month intervals), creating predictable, regulatory-driven cash flows that persist independent of macro cycles. Digital scheduling and subscription-style service agreements boost retention and allow smoothing of revenue recognition. Higher installed-base density improves route efficiency, lowering unit servicing costs and lifting margins.

- Regulatory lock-in: SOLAS 12-month liferaft servicing

- Revenue type: predictable recurring inspection/recertification

- Retention: digital scheduling/subscription models

- Margin driver: higher installed-base density → route efficiency

Emerging market fleet expansion

Emerging market fleet expansion in Asia, the Middle East and Africa increases demand for Survitec’s survival equipment, with Asia-Pacific newbuilds accounting for circa 90% of global shipbuilding activity in 2024. Port infrastructure upgrades and rising regional compliance create higher-spec service opportunities. Local partnerships accelerate market access and can reduce logistics lead times and costs materially. Price-sensitive buyers require tiered offerings that maintain SOLAS/MED compliance.

Global defense spend $2.24T fuels multiyear procurement, SOLAS retrofits

Moderate seaborne trade growth (UNCTAD ~1.5% 2023) and a 300+ GW offshore wind pipeline (GWEC 2024) create mixed demand for newbuilds and countercyclical PPE/rescue sales. Raw-material and energy shocks (EU gas up ~300% in 2022) plus container rates down ~70% by 2024 press margins; index‑linked contracts and hedging mitigate. SOLAS 12‑month servicing and Asia‑Pacific ~90% newbuilds (2024) anchor recurring revenues.

| Metric | Value |

|---|---|

| Seaborne trade growth (2023) | ~1.5% |

| Offshore wind pipeline (2024) | >300 GW |

| Asia‑Pacific newbuilds (2024) | ~90% |

| Container rates change (2022→2024) | ≈-70% |

| EU gas spike (2022) | ~+300% |

Full Version Awaits

Survitec Group PESTLE Analysis

This Survitec Group PESTLE Analysis delivers a concise evaluation of political, economic, social, technological, legal, and environmental factors affecting the business, plus strategic implications for stakeholders. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Actionable insights and clear structure make it immediately deployable for decision-making.