SWARCO AG Porter's Five Forces Analysis

From Overview to Strategy Blueprint

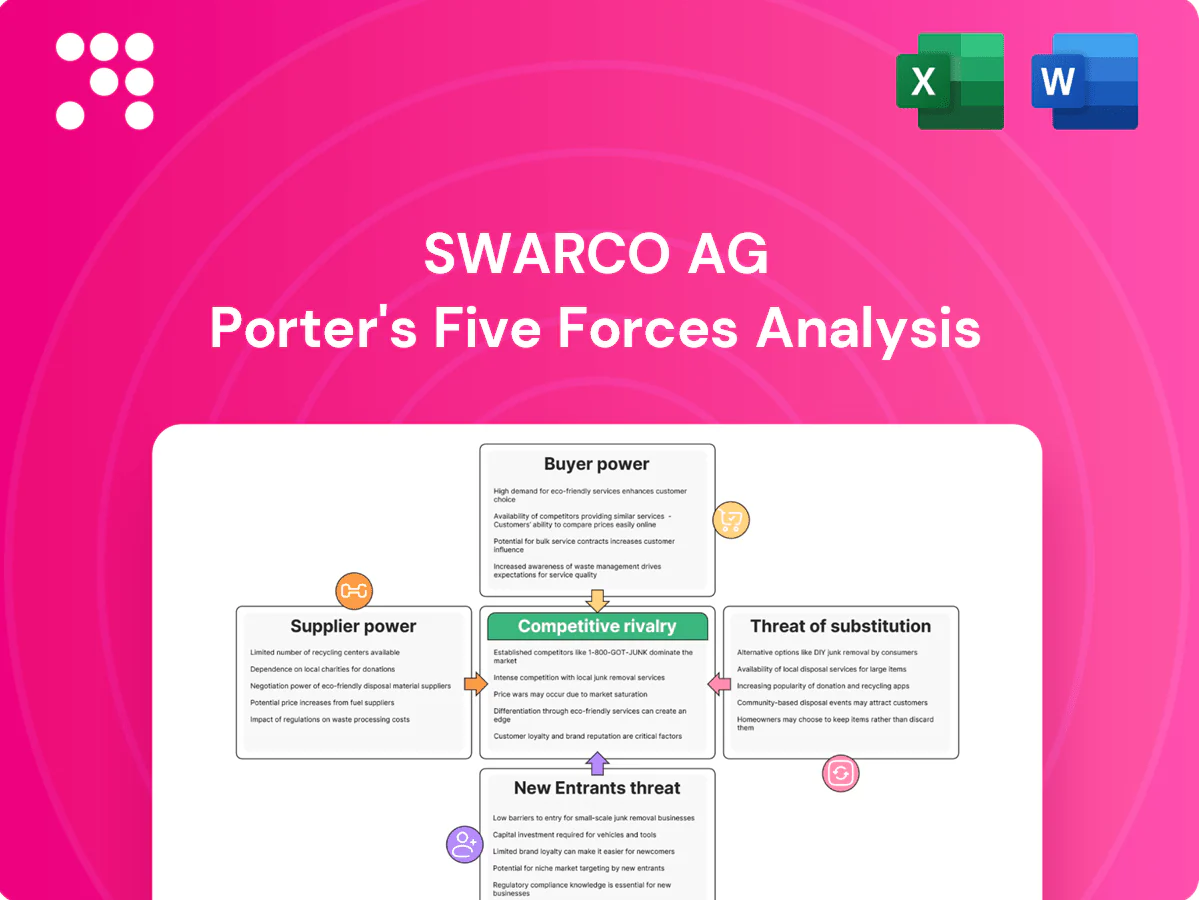

SWARCO AG operates in a technologically driven transport-systems market where buyer power, supplier specialization, and regulatory barriers shape competitive intensity; digital innovation and scale deliver both advantage and disruption risk. This snapshot highlights key friction points but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to explore SWARCO AG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component dependence

SWARCO depends on six niche inputs — LEDs, controllers, resins, glass beads, sensors and certified electronics — that few suppliers make at scale, elevating supplier power through limited alternatives and high qualification costs. Global sourcing and volume bundling mitigate leverage by aggregating demand across regions. Long-term contracts and dual-sourcing lower disruption risk and preserve continuity of supply.

Standards and certifications

Safety-critical ISO/EN standards in traffic systems strongly limit supplier substitution, reinforcing approved vendors’ leverage. Requalifying components typically requires 6–12 months and can incur €20k–€200k in testing and certification costs. SWARCO leverages stringent performance/lifecycle requirements to negotiate total-cost terms. Compliance-driven stickiness reduces short-term price volatility for core components.

Software and cloud dependencies

Reliance on cloud/IoT platforms, cybersecurity tools and mapping data gives digital vendors leverage, especially as the global public cloud market reached roughly 600 billion USD in 2024 and ~80% of firms report multi-cloud use. Interoperability and API standards reduce lock-in, while SWARCO’s proprietary software stack and modular architectures curtail single-vendor power; multi-cloud and on-premise options provide practical fallback resilience.

Commodity inputs volatility

Commodity inputs such as metals, chemicals and electronics face cyclical price swings and periodic supply shocks that allow suppliers to pass costs through and pressure SWARCO margins. SWARCO mitigates exposure via hedging programs, product redesigns and value engineering while using inventory planning and regionalization to buffer lead‑time risk. These measures reduce but do not eliminate supplier leverage.

- Supplier pass-through pressure

- Hedging and redesigns

- Inventory & regionalization buffers

Potential for backward/forward moves

Large component makers could move downstream with smart roadside units, raising supplier power, yet SWARCO’s in-house formulation and assembly for markings and controllers (supporting 2024 installations) reduce dependence; co-development and JV models align incentives and enable IP-sharing, keeping bargaining power moderate.

- Downstream threat: rising from smart roadside unit makers

- In-house capability: lowers supplier reliance

- Co-development/JV: aligns incentives, shares IP

- Overall: supplier power moderate

High supplier power for niche safety parts; requalify costly, multi-sourcing limits risk

SWARCO faces elevated supplier power for six niche inputs and safety‑certified components (requalification €20k–€200k, 6–12 months), partly offset by global sourcing, long‑term contracts and dual‑sourcing. Cloud vendors add leverage (public cloud ≈600B USD in 2024) but modular software and multi‑cloud reduce lock‑in. Commodity swings persist; hedging, redesigns and inventory buffers keep overall supplier power moderate.

| Metric | Value |

|---|---|

| Requalify cost | €20k–€200k |

| Requalify time | 6–12 months |

| Cloud market 2024 | ≈600B USD |

| Supplier power | Moderate |

What is included in the product

Tailored Porter's Five Forces analysis for SWARCO AG, uncovering the intensity of competition, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive technologies and regulatory factors that influence pricing, margins, and strategic positioning.

Concise one-sheet Porter's Five Forces for SWARCO AG—instantly highlights competitive pressures, customizable pressure levels for evolving traffic-tech markets, and a clean layout ready for pitch decks or boardroom slides.

Customers Bargaining Power

Public sector procurement

Core customers—municipalities, DOTs, transit agencies and concessions—procure via competitive tenders where public procurement typically represents about 10–15% of GDP, strengthening buyer leverage on price. High transparency and standardised bid comparisons push margins down; framework agreements and multi-year cycles (commonly 3–7 years) further compress margins. References and operational performance remain decisive alongside price.

High switching costs

Integrated traffic management platforms create data, training, and maintenance lock-in, tying municipalities to vendor-specific stacks. Buyers hesitate to switch because interoperability gaps, certification hurdles, and downtime risks raise migration costs and operational exposure. Post-deployment this materially reduces buyer bargaining power. Gradual adoption of open standards is lowering switching barriers over time.

Outcome and SLA focus

Buyers demand uptime and safety gains with congestion reduction targets, commonly specifying 99.9–99.99% availability (≈8.76 hours vs ≈52.6 minutes downtime/year), and attach penalties for misses, increasing buyer leverage. Performance‑based contracts shift operational and financial risk to vendors, tightening procurement bargaining. SWARCO counters with analytics, remote monitoring, and a broad service network, using demonstrable ROI to boost retention.

Budget constraints and funding cycles

Public budgets, grants and 4-5 year political cycles create stop-start demand and hard caps; EU cohesion policy allocates €373 billion for 2021–27 as an example of constrained but earmarked funding. Buyers push lowest TCO, extended warranties and phased rollouts; value-engineered, modular options match budget realities. Multi-year service contracts, typically 5–10 years, smooth revenue volatility.

- Political cycles: 4-5 year procurement cliffs

- Public funding scale: EU cohesion fund €373bn (2021–27)

- Buyer demands: lowest TCO, extended warranties, phased rollouts

- Seller responses: modular/value-engineered options, 5–10 year service contracts

Global competition in tenders

Global tendering lets buyers solicit 3–8 international bids, raising bargaining power as standardized specs make offerings directly comparable. SWARCO counters through a local footprint, regulatory compliance expertise and end-to-end project scope, shifting negotiations from price to value. Bundled lifecycle services further reduce pure price focus by linking maintenance and upgrades to contract value.

- 3–8 bids

- standardized specs → comparability

- local footprint & compliance

- end-to-end + lifecycle bundling

Buyers use 3–8 bids and strict 99.9–99.99% SLAs; EU funds (€373bn) push TCO focus

Buyers wield high price leverage via competitive tenders (3–8 bids) and public procurement norms (≈10–15% GDP), pushing margins. Performance clauses (99.9–99.99% uptime) and penalties strengthen buyer demands, while vendor lock‑in from integrated platforms raises switching costs and lowers bargaining power post-deployment. Multi‑year contracts (3–10 yrs) and EU funds (€373bn 2021–27) moderate volatility and shift focus to TCO.

| Metric | Value |

|---|---|

| Competitive bids | 3–8 |

| Procurement share | 10–15% GDP |

| Uptime SLAs | 99.9–99.99% |

| EU funding | €373bn (2021–27) |

Same Document Delivered

SWARCO AG Porter's Five Forces Analysis

This preview shows the exact SWARCO AG Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the full, professionally formatted file, ready for download and use the moment you buy. You're looking at the actual deliverable; once payment is complete, you’ll get instant access to this identical document.

From Overview to Strategy Blueprint

SWARCO AG operates in a technologically driven transport-systems market where buyer power, supplier specialization, and regulatory barriers shape competitive intensity; digital innovation and scale deliver both advantage and disruption risk. This snapshot highlights key friction points but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to explore SWARCO AG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component dependence

SWARCO depends on six niche inputs — LEDs, controllers, resins, glass beads, sensors and certified electronics — that few suppliers make at scale, elevating supplier power through limited alternatives and high qualification costs. Global sourcing and volume bundling mitigate leverage by aggregating demand across regions. Long-term contracts and dual-sourcing lower disruption risk and preserve continuity of supply.

Standards and certifications

Safety-critical ISO/EN standards in traffic systems strongly limit supplier substitution, reinforcing approved vendors’ leverage. Requalifying components typically requires 6–12 months and can incur €20k–€200k in testing and certification costs. SWARCO leverages stringent performance/lifecycle requirements to negotiate total-cost terms. Compliance-driven stickiness reduces short-term price volatility for core components.

Software and cloud dependencies

Reliance on cloud/IoT platforms, cybersecurity tools and mapping data gives digital vendors leverage, especially as the global public cloud market reached roughly 600 billion USD in 2024 and ~80% of firms report multi-cloud use. Interoperability and API standards reduce lock-in, while SWARCO’s proprietary software stack and modular architectures curtail single-vendor power; multi-cloud and on-premise options provide practical fallback resilience.

Commodity inputs volatility

Commodity inputs such as metals, chemicals and electronics face cyclical price swings and periodic supply shocks that allow suppliers to pass costs through and pressure SWARCO margins. SWARCO mitigates exposure via hedging programs, product redesigns and value engineering while using inventory planning and regionalization to buffer lead‑time risk. These measures reduce but do not eliminate supplier leverage.

- Supplier pass-through pressure

- Hedging and redesigns

- Inventory & regionalization buffers

Potential for backward/forward moves

Large component makers could move downstream with smart roadside units, raising supplier power, yet SWARCO’s in-house formulation and assembly for markings and controllers (supporting 2024 installations) reduce dependence; co-development and JV models align incentives and enable IP-sharing, keeping bargaining power moderate.

- Downstream threat: rising from smart roadside unit makers

- In-house capability: lowers supplier reliance

- Co-development/JV: aligns incentives, shares IP

- Overall: supplier power moderate

High supplier power for niche safety parts; requalify costly, multi-sourcing limits risk

SWARCO faces elevated supplier power for six niche inputs and safety‑certified components (requalification €20k–€200k, 6–12 months), partly offset by global sourcing, long‑term contracts and dual‑sourcing. Cloud vendors add leverage (public cloud ≈600B USD in 2024) but modular software and multi‑cloud reduce lock‑in. Commodity swings persist; hedging, redesigns and inventory buffers keep overall supplier power moderate.

| Metric | Value |

|---|---|

| Requalify cost | €20k–€200k |

| Requalify time | 6–12 months |

| Cloud market 2024 | ≈600B USD |

| Supplier power | Moderate |

What is included in the product

Tailored Porter's Five Forces analysis for SWARCO AG, uncovering the intensity of competition, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive technologies and regulatory factors that influence pricing, margins, and strategic positioning.

Concise one-sheet Porter's Five Forces for SWARCO AG—instantly highlights competitive pressures, customizable pressure levels for evolving traffic-tech markets, and a clean layout ready for pitch decks or boardroom slides.

Customers Bargaining Power

Public sector procurement

Core customers—municipalities, DOTs, transit agencies and concessions—procure via competitive tenders where public procurement typically represents about 10–15% of GDP, strengthening buyer leverage on price. High transparency and standardised bid comparisons push margins down; framework agreements and multi-year cycles (commonly 3–7 years) further compress margins. References and operational performance remain decisive alongside price.

High switching costs

Integrated traffic management platforms create data, training, and maintenance lock-in, tying municipalities to vendor-specific stacks. Buyers hesitate to switch because interoperability gaps, certification hurdles, and downtime risks raise migration costs and operational exposure. Post-deployment this materially reduces buyer bargaining power. Gradual adoption of open standards is lowering switching barriers over time.

Outcome and SLA focus

Buyers demand uptime and safety gains with congestion reduction targets, commonly specifying 99.9–99.99% availability (≈8.76 hours vs ≈52.6 minutes downtime/year), and attach penalties for misses, increasing buyer leverage. Performance‑based contracts shift operational and financial risk to vendors, tightening procurement bargaining. SWARCO counters with analytics, remote monitoring, and a broad service network, using demonstrable ROI to boost retention.

Budget constraints and funding cycles

Public budgets, grants and 4-5 year political cycles create stop-start demand and hard caps; EU cohesion policy allocates €373 billion for 2021–27 as an example of constrained but earmarked funding. Buyers push lowest TCO, extended warranties and phased rollouts; value-engineered, modular options match budget realities. Multi-year service contracts, typically 5–10 years, smooth revenue volatility.

- Political cycles: 4-5 year procurement cliffs

- Public funding scale: EU cohesion fund €373bn (2021–27)

- Buyer demands: lowest TCO, extended warranties, phased rollouts

- Seller responses: modular/value-engineered options, 5–10 year service contracts

Global competition in tenders

Global tendering lets buyers solicit 3–8 international bids, raising bargaining power as standardized specs make offerings directly comparable. SWARCO counters through a local footprint, regulatory compliance expertise and end-to-end project scope, shifting negotiations from price to value. Bundled lifecycle services further reduce pure price focus by linking maintenance and upgrades to contract value.

- 3–8 bids

- standardized specs → comparability

- local footprint & compliance

- end-to-end + lifecycle bundling

Buyers use 3–8 bids and strict 99.9–99.99% SLAs; EU funds (€373bn) push TCO focus

Buyers wield high price leverage via competitive tenders (3–8 bids) and public procurement norms (≈10–15% GDP), pushing margins. Performance clauses (99.9–99.99% uptime) and penalties strengthen buyer demands, while vendor lock‑in from integrated platforms raises switching costs and lowers bargaining power post-deployment. Multi‑year contracts (3–10 yrs) and EU funds (€373bn 2021–27) moderate volatility and shift focus to TCO.

| Metric | Value |

|---|---|

| Competitive bids | 3–8 |

| Procurement share | 10–15% GDP |

| Uptime SLAs | 99.9–99.99% |

| EU funding | €373bn (2021–27) |

Same Document Delivered

SWARCO AG Porter's Five Forces Analysis

This preview shows the exact SWARCO AG Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the full, professionally formatted file, ready for download and use the moment you buy. You're looking at the actual deliverable; once payment is complete, you’ll get instant access to this identical document.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

SWARCO AG operates in a technologically driven transport-systems market where buyer power, supplier specialization, and regulatory barriers shape competitive intensity; digital innovation and scale deliver both advantage and disruption risk. This snapshot highlights key friction points but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to explore SWARCO AG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component dependence

SWARCO depends on six niche inputs — LEDs, controllers, resins, glass beads, sensors and certified electronics — that few suppliers make at scale, elevating supplier power through limited alternatives and high qualification costs. Global sourcing and volume bundling mitigate leverage by aggregating demand across regions. Long-term contracts and dual-sourcing lower disruption risk and preserve continuity of supply.

Standards and certifications

Safety-critical ISO/EN standards in traffic systems strongly limit supplier substitution, reinforcing approved vendors’ leverage. Requalifying components typically requires 6–12 months and can incur €20k–€200k in testing and certification costs. SWARCO leverages stringent performance/lifecycle requirements to negotiate total-cost terms. Compliance-driven stickiness reduces short-term price volatility for core components.

Software and cloud dependencies

Reliance on cloud/IoT platforms, cybersecurity tools and mapping data gives digital vendors leverage, especially as the global public cloud market reached roughly 600 billion USD in 2024 and ~80% of firms report multi-cloud use. Interoperability and API standards reduce lock-in, while SWARCO’s proprietary software stack and modular architectures curtail single-vendor power; multi-cloud and on-premise options provide practical fallback resilience.

Commodity inputs volatility

Commodity inputs such as metals, chemicals and electronics face cyclical price swings and periodic supply shocks that allow suppliers to pass costs through and pressure SWARCO margins. SWARCO mitigates exposure via hedging programs, product redesigns and value engineering while using inventory planning and regionalization to buffer lead‑time risk. These measures reduce but do not eliminate supplier leverage.

- Supplier pass-through pressure

- Hedging and redesigns

- Inventory & regionalization buffers

Potential for backward/forward moves

Large component makers could move downstream with smart roadside units, raising supplier power, yet SWARCO’s in-house formulation and assembly for markings and controllers (supporting 2024 installations) reduce dependence; co-development and JV models align incentives and enable IP-sharing, keeping bargaining power moderate.

- Downstream threat: rising from smart roadside unit makers

- In-house capability: lowers supplier reliance

- Co-development/JV: aligns incentives, shares IP

- Overall: supplier power moderate

High supplier power for niche safety parts; requalify costly, multi-sourcing limits risk

SWARCO faces elevated supplier power for six niche inputs and safety‑certified components (requalification €20k–€200k, 6–12 months), partly offset by global sourcing, long‑term contracts and dual‑sourcing. Cloud vendors add leverage (public cloud ≈600B USD in 2024) but modular software and multi‑cloud reduce lock‑in. Commodity swings persist; hedging, redesigns and inventory buffers keep overall supplier power moderate.

| Metric | Value |

|---|---|

| Requalify cost | €20k–€200k |

| Requalify time | 6–12 months |

| Cloud market 2024 | ≈600B USD |

| Supplier power | Moderate |

What is included in the product

Tailored Porter's Five Forces analysis for SWARCO AG, uncovering the intensity of competition, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive technologies and regulatory factors that influence pricing, margins, and strategic positioning.

Concise one-sheet Porter's Five Forces for SWARCO AG—instantly highlights competitive pressures, customizable pressure levels for evolving traffic-tech markets, and a clean layout ready for pitch decks or boardroom slides.

Customers Bargaining Power

Public sector procurement

Core customers—municipalities, DOTs, transit agencies and concessions—procure via competitive tenders where public procurement typically represents about 10–15% of GDP, strengthening buyer leverage on price. High transparency and standardised bid comparisons push margins down; framework agreements and multi-year cycles (commonly 3–7 years) further compress margins. References and operational performance remain decisive alongside price.

High switching costs

Integrated traffic management platforms create data, training, and maintenance lock-in, tying municipalities to vendor-specific stacks. Buyers hesitate to switch because interoperability gaps, certification hurdles, and downtime risks raise migration costs and operational exposure. Post-deployment this materially reduces buyer bargaining power. Gradual adoption of open standards is lowering switching barriers over time.

Outcome and SLA focus

Buyers demand uptime and safety gains with congestion reduction targets, commonly specifying 99.9–99.99% availability (≈8.76 hours vs ≈52.6 minutes downtime/year), and attach penalties for misses, increasing buyer leverage. Performance‑based contracts shift operational and financial risk to vendors, tightening procurement bargaining. SWARCO counters with analytics, remote monitoring, and a broad service network, using demonstrable ROI to boost retention.

Budget constraints and funding cycles

Public budgets, grants and 4-5 year political cycles create stop-start demand and hard caps; EU cohesion policy allocates €373 billion for 2021–27 as an example of constrained but earmarked funding. Buyers push lowest TCO, extended warranties and phased rollouts; value-engineered, modular options match budget realities. Multi-year service contracts, typically 5–10 years, smooth revenue volatility.

- Political cycles: 4-5 year procurement cliffs

- Public funding scale: EU cohesion fund €373bn (2021–27)

- Buyer demands: lowest TCO, extended warranties, phased rollouts

- Seller responses: modular/value-engineered options, 5–10 year service contracts

Global competition in tenders

Global tendering lets buyers solicit 3–8 international bids, raising bargaining power as standardized specs make offerings directly comparable. SWARCO counters through a local footprint, regulatory compliance expertise and end-to-end project scope, shifting negotiations from price to value. Bundled lifecycle services further reduce pure price focus by linking maintenance and upgrades to contract value.

- 3–8 bids

- standardized specs → comparability

- local footprint & compliance

- end-to-end + lifecycle bundling

Buyers use 3–8 bids and strict 99.9–99.99% SLAs; EU funds (€373bn) push TCO focus

Buyers wield high price leverage via competitive tenders (3–8 bids) and public procurement norms (≈10–15% GDP), pushing margins. Performance clauses (99.9–99.99% uptime) and penalties strengthen buyer demands, while vendor lock‑in from integrated platforms raises switching costs and lowers bargaining power post-deployment. Multi‑year contracts (3–10 yrs) and EU funds (€373bn 2021–27) moderate volatility and shift focus to TCO.

| Metric | Value |

|---|---|

| Competitive bids | 3–8 |

| Procurement share | 10–15% GDP |

| Uptime SLAs | 99.9–99.99% |

| EU funding | €373bn (2021–27) |

Same Document Delivered

SWARCO AG Porter's Five Forces Analysis

This preview shows the exact SWARCO AG Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the full, professionally formatted file, ready for download and use the moment you buy. You're looking at the actual deliverable; once payment is complete, you’ll get instant access to this identical document.