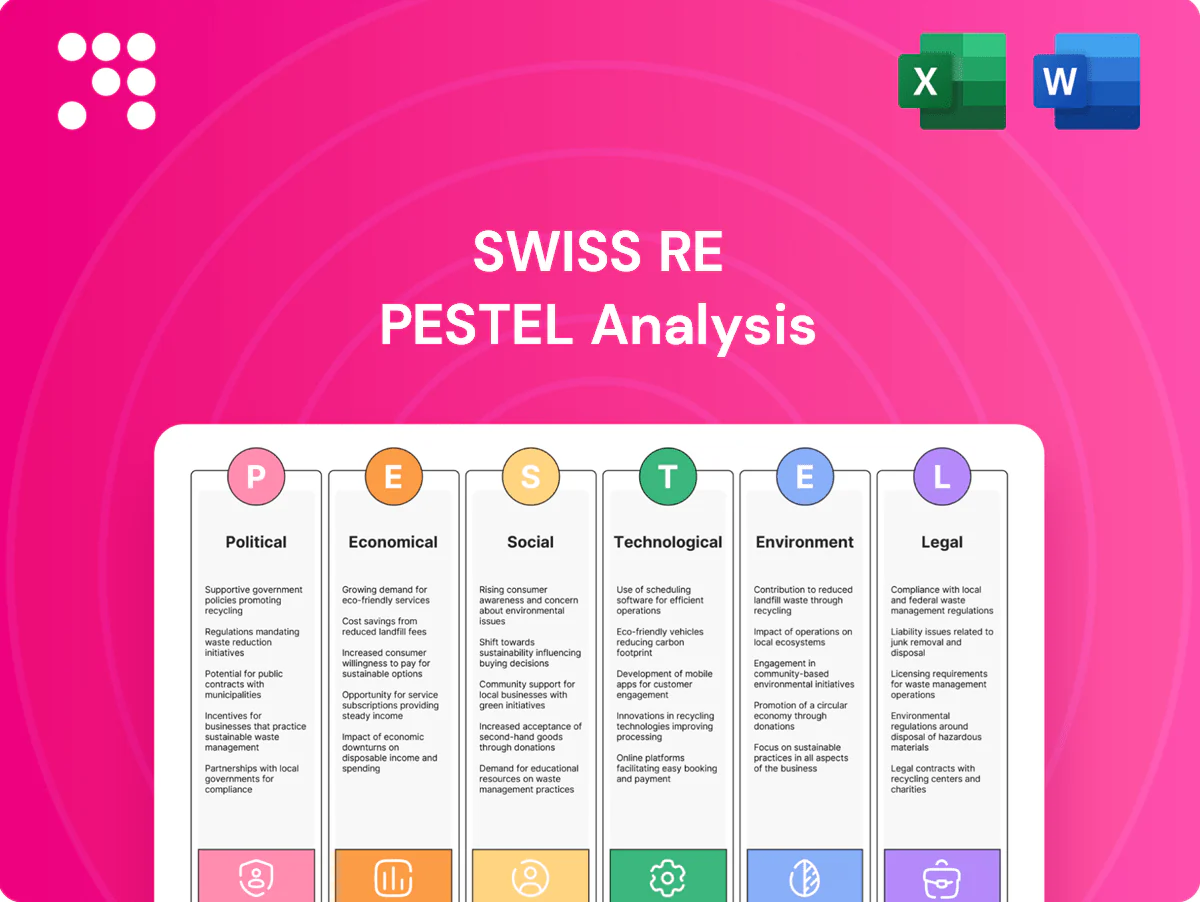

Swiss Re PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE Analysis tailored to Swiss Re—discover how political shifts, economic cycles, and regulatory trends shape its risk profile and growth prospects. This concise, actionable report is ideal for investors and strategists; purchase the full version to unlock detailed insights and ready-to-use recommendations.

Political factors

Regulatory regimes (Solvency II/SST)

Solvency II (99.5% one‑year VaR) and Switzerland’s SST (1‑in‑200‑year stress) materially shape Swiss Re’s capital deployment and pricing, with any upward re‑calibration of risk charges or catastrophe model assumptions tightening capacity and raising return hurdles. Regulatory alignment across jurisdictions permits efficient group capital fungibility; divergence increases compliance costs and risks of trapped capital in local entities.

Geopolitical instability and sanctions

Geopolitical conflicts and sanctions have reshaped risk pools across aviation, marine and political-risk lines, increasing claims volatility and prompting Swiss Re to tighten underwriting in sanctioned markets and on restricted counterparties; sanctions compliance limits capacity in Russia, Iran and select jurisdictions and can void cover on state-linked exposures, creating protection gaps. Trade re-routing alters accumulation patterns and requires updated aggregation models.

Government disaster schemes

Public-private nat-cat and pandemic pools reshape reinsurance demand and terms by shifting risk to state-backed vehicles, often mobilizing billions in capacity and reducing private attachment points. Policy design — backstops and attachment points — reallocates losses between taxpayers and markets, altering Swiss Re’s pricing and capital needs. Swiss Re partners with governments to supply modeling, capital and quota-share capacity. Political will after major events routinely tightens terms and lifts prices.

Tax policy and global minimum tax

OECD Pillar Two sets a 15% global minimum tax and BEPS rules; over 140 jurisdictions have signalled adoption, forcing Swiss Re to rethink group structuring as after-tax ROE and quoted margins face upward pressure. Location of risk, demonstrable substance and intra-group retrocession are under tighter tax and regulatory scrutiny, which can increase effective tax rates and change capital allocation. Regulatory tax stability supports more predictable long-tail reserving assumptions.

- 15% minimum tax floor

- 140+ jurisdictions committed

- Tighter scrutiny on substance and retrocession

- Higher ETR risk, pressure on quoted margins

Trade policy and market access

Trade policy shifts—licensing, local retention rules and data localization—raise frictions for Swiss Re by constraining cross-border placement and forcing treaty localization, which increases operational and treaty amendment costs; liberalization widens accessible premium pools while protectionism fragments risk transfer. Passporting and equivalence decisions (eg post-Brexit arrangements) materially affect market access and capital efficiency for Swiss Re.

- Licensing barriers increase local capital strain

- Local retention/data localization raise compliance costs

- Liberalization expands premium pools; protectionism fragments risks

- Passporting/equivalence decisions determine cross-border capacity

Political rules reshape reinsurance: higher capital, pricing stress and tighter cross-border capacity

Political forces—Solvency II/SST capital regimes, OECD Pillar Two (15% floor, 140+ jurisdictions), sanctions and trade policy shifts—drive Swiss Re’s capital allocation, pricing and market access, increasing compliance costs and trapped-capital risk. Geopolitical conflicts and public-private nat-cat backstops raise claims volatility and alter attachment points, compressing private capacity. Passporting/equivalence and localization rules materially affect cross-border treaty efficiency.

| Factor | Metric | Impact |

|---|---|---|

| OECD Pillar Two | 15% / 140+ juris. | Higher ETR, restructure risk |

| Solvency/SST | 99.5% / 1-in-200 | Tighter capital & pricing |

| Sanctions | Russia/Iran limits | Reduced capacity, higher volatility |

What is included in the product

Explores how macro-environmental factors uniquely affect Swiss Re across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples. Designed for executives and investors, the analysis offers forward-looking insights and scenario-ready guidance to identify risks, opportunities and strategic responses within Swiss Re's markets and regulatory landscape.

A concise, PESTLE-segmented Swiss Re summary that’s easily dropped into presentations, editable for region or business-line notes, and shareable across teams to streamline external risk, market-position and planning discussions.

Economic factors

Interest rates and yield curve

Higher nominal rates and rising developed‑market 10‑year yields near 3–4% lift Swiss Re’s investment income and allow steeper discounting of technical reserves, but can depress bond and equity prices, pressuring asset values. For long‑tail lines, duration management is critical to match liabilities and avoid mark‑to‑market losses. The yield curve shape affects reinvestment rates and present value of future claims; flatter curves limit reinvestment pickup. Higher real yields (~1–2% in 2024–25) improve capital leverage and underwriting economics.

Inflation and social inflation

General inflation (Swiss CPI ~2.1% in 2024) and elevated claims inflation increase loss costs and reserve risk for Swiss Re, while liability lines face social inflation with claim severity rising roughly 8% year-on-year in major markets in 2023–24.

Verdict severity and litigation trends often outpace CPI, forcing faster pricing and indexation clause adjustments; Swiss Re updates model parameters continuously to reflect these dynamics and preserve reserve adequacy.

Cat loss cycles and pricing hard/soft

Frequency of large catastrophes drives reinsurance rate hardening and tighter terms (exclusions, higher attachments), with markets typically seeing double-digit rate increases after major loss years. Post-event capacity tightens and underwriting returns improve as capital reprices and insurers reduce limits. Prolonged benign periods invite capacity inflows, increased competition and margin compression. Swiss Re benefits from disciplined cycle management and selective deployment of capital.

Global growth and insurance penetration

Emerging-market GDP growth (IMF: 4.3% in 2024) widens the protection gap—Swiss Re Institute estimates an uninsured global protection gap of about USD 1.8 trillion—boosting demand for reinsurance and risk-transfer solutions. Corporate investment cycles and rising capex lift commercial-lines exposures, while recessions compress premium bases and underwriting volumes. Swiss Re’s diversified global footprint helps buffer regional downturns and sustain overall ceded premium.

- Emerging markets growth: IMF 4.3% (2024)

- Protection gap: ~USD 1.8 trillion (Swiss Re Institute)

- Corporate investment → higher commercial lines

- Diversification mitigates regional shocks

FX volatility and capital fungibility

Multi-currency claims and assets create translation and mismatch risk for Swiss Re, forcing regular revaluation of reserves and capital across CHF, EUR and USD books.

Robust hedging programs are vital to protect capital ratios measured in CHF or EUR, and pricing must embed currency risk premia to maintain underwriting economics.

Political rules reshape reinsurance: higher capital, pricing stress and tighter cross-border capacity

Higher developed‑market 10y yields (~3–4% in 2024–25) boost Swiss Re’s investment income and allow steeper discounting, but raise mark‑to‑market risk; inflation (Swiss CPI ~2.1% in 2024) and claims inflation (~8% y/y in major markets 2023–24) lift loss costs and reserve risk. Catastrophe frequency drives cyclical rate hardening; emerging‑market GDP (IMF 4.3% 2024) expands protection gap (USD 1.8tn), increasing demand for reinsurance.

| Metric | Value |

|---|---|

| 10y yields | 3–4% |

| Swiss CPI (2024) | 2.1% |

| Claims inflation | ~8% y/y |

| EM GDP (2024) | 4.3% |

| Protection gap | USD 1.8tn |

Full Version Awaits

Swiss Re PESTLE Analysis

The preview shown here is the exact Swiss Re PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; this is the final file. You can download the document immediately after payment.

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE Analysis tailored to Swiss Re—discover how political shifts, economic cycles, and regulatory trends shape its risk profile and growth prospects. This concise, actionable report is ideal for investors and strategists; purchase the full version to unlock detailed insights and ready-to-use recommendations.

Political factors

Regulatory regimes (Solvency II/SST)

Solvency II (99.5% one‑year VaR) and Switzerland’s SST (1‑in‑200‑year stress) materially shape Swiss Re’s capital deployment and pricing, with any upward re‑calibration of risk charges or catastrophe model assumptions tightening capacity and raising return hurdles. Regulatory alignment across jurisdictions permits efficient group capital fungibility; divergence increases compliance costs and risks of trapped capital in local entities.

Geopolitical instability and sanctions

Geopolitical conflicts and sanctions have reshaped risk pools across aviation, marine and political-risk lines, increasing claims volatility and prompting Swiss Re to tighten underwriting in sanctioned markets and on restricted counterparties; sanctions compliance limits capacity in Russia, Iran and select jurisdictions and can void cover on state-linked exposures, creating protection gaps. Trade re-routing alters accumulation patterns and requires updated aggregation models.

Government disaster schemes

Public-private nat-cat and pandemic pools reshape reinsurance demand and terms by shifting risk to state-backed vehicles, often mobilizing billions in capacity and reducing private attachment points. Policy design — backstops and attachment points — reallocates losses between taxpayers and markets, altering Swiss Re’s pricing and capital needs. Swiss Re partners with governments to supply modeling, capital and quota-share capacity. Political will after major events routinely tightens terms and lifts prices.

Tax policy and global minimum tax

OECD Pillar Two sets a 15% global minimum tax and BEPS rules; over 140 jurisdictions have signalled adoption, forcing Swiss Re to rethink group structuring as after-tax ROE and quoted margins face upward pressure. Location of risk, demonstrable substance and intra-group retrocession are under tighter tax and regulatory scrutiny, which can increase effective tax rates and change capital allocation. Regulatory tax stability supports more predictable long-tail reserving assumptions.

- 15% minimum tax floor

- 140+ jurisdictions committed

- Tighter scrutiny on substance and retrocession

- Higher ETR risk, pressure on quoted margins

Trade policy and market access

Trade policy shifts—licensing, local retention rules and data localization—raise frictions for Swiss Re by constraining cross-border placement and forcing treaty localization, which increases operational and treaty amendment costs; liberalization widens accessible premium pools while protectionism fragments risk transfer. Passporting and equivalence decisions (eg post-Brexit arrangements) materially affect market access and capital efficiency for Swiss Re.

- Licensing barriers increase local capital strain

- Local retention/data localization raise compliance costs

- Liberalization expands premium pools; protectionism fragments risks

- Passporting/equivalence decisions determine cross-border capacity

Political rules reshape reinsurance: higher capital, pricing stress and tighter cross-border capacity

Political forces—Solvency II/SST capital regimes, OECD Pillar Two (15% floor, 140+ jurisdictions), sanctions and trade policy shifts—drive Swiss Re’s capital allocation, pricing and market access, increasing compliance costs and trapped-capital risk. Geopolitical conflicts and public-private nat-cat backstops raise claims volatility and alter attachment points, compressing private capacity. Passporting/equivalence and localization rules materially affect cross-border treaty efficiency.

| Factor | Metric | Impact |

|---|---|---|

| OECD Pillar Two | 15% / 140+ juris. | Higher ETR, restructure risk |

| Solvency/SST | 99.5% / 1-in-200 | Tighter capital & pricing |

| Sanctions | Russia/Iran limits | Reduced capacity, higher volatility |

What is included in the product

Explores how macro-environmental factors uniquely affect Swiss Re across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples. Designed for executives and investors, the analysis offers forward-looking insights and scenario-ready guidance to identify risks, opportunities and strategic responses within Swiss Re's markets and regulatory landscape.

A concise, PESTLE-segmented Swiss Re summary that’s easily dropped into presentations, editable for region or business-line notes, and shareable across teams to streamline external risk, market-position and planning discussions.

Economic factors

Interest rates and yield curve

Higher nominal rates and rising developed‑market 10‑year yields near 3–4% lift Swiss Re’s investment income and allow steeper discounting of technical reserves, but can depress bond and equity prices, pressuring asset values. For long‑tail lines, duration management is critical to match liabilities and avoid mark‑to‑market losses. The yield curve shape affects reinvestment rates and present value of future claims; flatter curves limit reinvestment pickup. Higher real yields (~1–2% in 2024–25) improve capital leverage and underwriting economics.

Inflation and social inflation

General inflation (Swiss CPI ~2.1% in 2024) and elevated claims inflation increase loss costs and reserve risk for Swiss Re, while liability lines face social inflation with claim severity rising roughly 8% year-on-year in major markets in 2023–24.

Verdict severity and litigation trends often outpace CPI, forcing faster pricing and indexation clause adjustments; Swiss Re updates model parameters continuously to reflect these dynamics and preserve reserve adequacy.

Cat loss cycles and pricing hard/soft

Frequency of large catastrophes drives reinsurance rate hardening and tighter terms (exclusions, higher attachments), with markets typically seeing double-digit rate increases after major loss years. Post-event capacity tightens and underwriting returns improve as capital reprices and insurers reduce limits. Prolonged benign periods invite capacity inflows, increased competition and margin compression. Swiss Re benefits from disciplined cycle management and selective deployment of capital.

Global growth and insurance penetration

Emerging-market GDP growth (IMF: 4.3% in 2024) widens the protection gap—Swiss Re Institute estimates an uninsured global protection gap of about USD 1.8 trillion—boosting demand for reinsurance and risk-transfer solutions. Corporate investment cycles and rising capex lift commercial-lines exposures, while recessions compress premium bases and underwriting volumes. Swiss Re’s diversified global footprint helps buffer regional downturns and sustain overall ceded premium.

- Emerging markets growth: IMF 4.3% (2024)

- Protection gap: ~USD 1.8 trillion (Swiss Re Institute)

- Corporate investment → higher commercial lines

- Diversification mitigates regional shocks

FX volatility and capital fungibility

Multi-currency claims and assets create translation and mismatch risk for Swiss Re, forcing regular revaluation of reserves and capital across CHF, EUR and USD books.

Robust hedging programs are vital to protect capital ratios measured in CHF or EUR, and pricing must embed currency risk premia to maintain underwriting economics.

Political rules reshape reinsurance: higher capital, pricing stress and tighter cross-border capacity

Higher developed‑market 10y yields (~3–4% in 2024–25) boost Swiss Re’s investment income and allow steeper discounting, but raise mark‑to‑market risk; inflation (Swiss CPI ~2.1% in 2024) and claims inflation (~8% y/y in major markets 2023–24) lift loss costs and reserve risk. Catastrophe frequency drives cyclical rate hardening; emerging‑market GDP (IMF 4.3% 2024) expands protection gap (USD 1.8tn), increasing demand for reinsurance.

| Metric | Value |

|---|---|

| 10y yields | 3–4% |

| Swiss CPI (2024) | 2.1% |

| Claims inflation | ~8% y/y |

| EM GDP (2024) | 4.3% |

| Protection gap | USD 1.8tn |

Full Version Awaits

Swiss Re PESTLE Analysis

The preview shown here is the exact Swiss Re PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; this is the final file. You can download the document immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE Analysis tailored to Swiss Re—discover how political shifts, economic cycles, and regulatory trends shape its risk profile and growth prospects. This concise, actionable report is ideal for investors and strategists; purchase the full version to unlock detailed insights and ready-to-use recommendations.

Political factors

Regulatory regimes (Solvency II/SST)

Solvency II (99.5% one‑year VaR) and Switzerland’s SST (1‑in‑200‑year stress) materially shape Swiss Re’s capital deployment and pricing, with any upward re‑calibration of risk charges or catastrophe model assumptions tightening capacity and raising return hurdles. Regulatory alignment across jurisdictions permits efficient group capital fungibility; divergence increases compliance costs and risks of trapped capital in local entities.

Geopolitical instability and sanctions

Geopolitical conflicts and sanctions have reshaped risk pools across aviation, marine and political-risk lines, increasing claims volatility and prompting Swiss Re to tighten underwriting in sanctioned markets and on restricted counterparties; sanctions compliance limits capacity in Russia, Iran and select jurisdictions and can void cover on state-linked exposures, creating protection gaps. Trade re-routing alters accumulation patterns and requires updated aggregation models.

Government disaster schemes

Public-private nat-cat and pandemic pools reshape reinsurance demand and terms by shifting risk to state-backed vehicles, often mobilizing billions in capacity and reducing private attachment points. Policy design — backstops and attachment points — reallocates losses between taxpayers and markets, altering Swiss Re’s pricing and capital needs. Swiss Re partners with governments to supply modeling, capital and quota-share capacity. Political will after major events routinely tightens terms and lifts prices.

Tax policy and global minimum tax

OECD Pillar Two sets a 15% global minimum tax and BEPS rules; over 140 jurisdictions have signalled adoption, forcing Swiss Re to rethink group structuring as after-tax ROE and quoted margins face upward pressure. Location of risk, demonstrable substance and intra-group retrocession are under tighter tax and regulatory scrutiny, which can increase effective tax rates and change capital allocation. Regulatory tax stability supports more predictable long-tail reserving assumptions.

- 15% minimum tax floor

- 140+ jurisdictions committed

- Tighter scrutiny on substance and retrocession

- Higher ETR risk, pressure on quoted margins

Trade policy and market access

Trade policy shifts—licensing, local retention rules and data localization—raise frictions for Swiss Re by constraining cross-border placement and forcing treaty localization, which increases operational and treaty amendment costs; liberalization widens accessible premium pools while protectionism fragments risk transfer. Passporting and equivalence decisions (eg post-Brexit arrangements) materially affect market access and capital efficiency for Swiss Re.

- Licensing barriers increase local capital strain

- Local retention/data localization raise compliance costs

- Liberalization expands premium pools; protectionism fragments risks

- Passporting/equivalence decisions determine cross-border capacity

Political rules reshape reinsurance: higher capital, pricing stress and tighter cross-border capacity

Political forces—Solvency II/SST capital regimes, OECD Pillar Two (15% floor, 140+ jurisdictions), sanctions and trade policy shifts—drive Swiss Re’s capital allocation, pricing and market access, increasing compliance costs and trapped-capital risk. Geopolitical conflicts and public-private nat-cat backstops raise claims volatility and alter attachment points, compressing private capacity. Passporting/equivalence and localization rules materially affect cross-border treaty efficiency.

| Factor | Metric | Impact |

|---|---|---|

| OECD Pillar Two | 15% / 140+ juris. | Higher ETR, restructure risk |

| Solvency/SST | 99.5% / 1-in-200 | Tighter capital & pricing |

| Sanctions | Russia/Iran limits | Reduced capacity, higher volatility |

What is included in the product

Explores how macro-environmental factors uniquely affect Swiss Re across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and industry-specific examples. Designed for executives and investors, the analysis offers forward-looking insights and scenario-ready guidance to identify risks, opportunities and strategic responses within Swiss Re's markets and regulatory landscape.

A concise, PESTLE-segmented Swiss Re summary that’s easily dropped into presentations, editable for region or business-line notes, and shareable across teams to streamline external risk, market-position and planning discussions.

Economic factors

Interest rates and yield curve

Higher nominal rates and rising developed‑market 10‑year yields near 3–4% lift Swiss Re’s investment income and allow steeper discounting of technical reserves, but can depress bond and equity prices, pressuring asset values. For long‑tail lines, duration management is critical to match liabilities and avoid mark‑to‑market losses. The yield curve shape affects reinvestment rates and present value of future claims; flatter curves limit reinvestment pickup. Higher real yields (~1–2% in 2024–25) improve capital leverage and underwriting economics.

Inflation and social inflation

General inflation (Swiss CPI ~2.1% in 2024) and elevated claims inflation increase loss costs and reserve risk for Swiss Re, while liability lines face social inflation with claim severity rising roughly 8% year-on-year in major markets in 2023–24.

Verdict severity and litigation trends often outpace CPI, forcing faster pricing and indexation clause adjustments; Swiss Re updates model parameters continuously to reflect these dynamics and preserve reserve adequacy.

Cat loss cycles and pricing hard/soft

Frequency of large catastrophes drives reinsurance rate hardening and tighter terms (exclusions, higher attachments), with markets typically seeing double-digit rate increases after major loss years. Post-event capacity tightens and underwriting returns improve as capital reprices and insurers reduce limits. Prolonged benign periods invite capacity inflows, increased competition and margin compression. Swiss Re benefits from disciplined cycle management and selective deployment of capital.

Global growth and insurance penetration

Emerging-market GDP growth (IMF: 4.3% in 2024) widens the protection gap—Swiss Re Institute estimates an uninsured global protection gap of about USD 1.8 trillion—boosting demand for reinsurance and risk-transfer solutions. Corporate investment cycles and rising capex lift commercial-lines exposures, while recessions compress premium bases and underwriting volumes. Swiss Re’s diversified global footprint helps buffer regional downturns and sustain overall ceded premium.

- Emerging markets growth: IMF 4.3% (2024)

- Protection gap: ~USD 1.8 trillion (Swiss Re Institute)

- Corporate investment → higher commercial lines

- Diversification mitigates regional shocks

FX volatility and capital fungibility

Multi-currency claims and assets create translation and mismatch risk for Swiss Re, forcing regular revaluation of reserves and capital across CHF, EUR and USD books.

Robust hedging programs are vital to protect capital ratios measured in CHF or EUR, and pricing must embed currency risk premia to maintain underwriting economics.

Political rules reshape reinsurance: higher capital, pricing stress and tighter cross-border capacity

Higher developed‑market 10y yields (~3–4% in 2024–25) boost Swiss Re’s investment income and allow steeper discounting, but raise mark‑to‑market risk; inflation (Swiss CPI ~2.1% in 2024) and claims inflation (~8% y/y in major markets 2023–24) lift loss costs and reserve risk. Catastrophe frequency drives cyclical rate hardening; emerging‑market GDP (IMF 4.3% 2024) expands protection gap (USD 1.8tn), increasing demand for reinsurance.

| Metric | Value |

|---|---|

| 10y yields | 3–4% |

| Swiss CPI (2024) | 2.1% |

| Claims inflation | ~8% y/y |

| EM GDP (2024) | 4.3% |

| Protection gap | USD 1.8tn |

Full Version Awaits

Swiss Re PESTLE Analysis

The preview shown here is the exact Swiss Re PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; this is the final file. You can download the document immediately after payment.