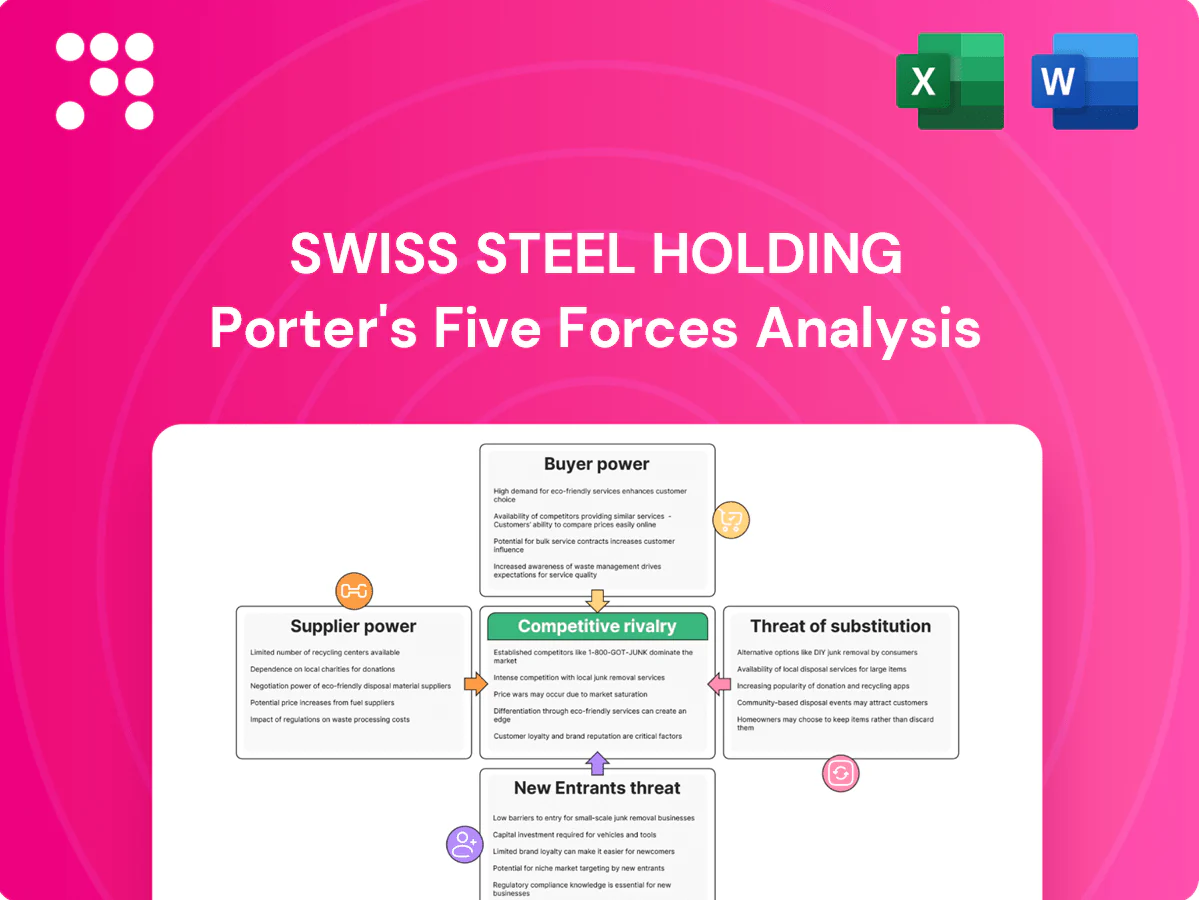

Swiss Steel Holding Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Swiss Steel Holding faces moderate bargaining power from buyers due to industry fragmentation, but intense rivalry among existing players exerts significant pressure. The threat of substitutes, while present, is somewhat mitigated by the specialized nature of steel products.

The complete report reveals the real forces shaping Swiss Steel Holding’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Reliance on Key Raw Materials

Swiss Steel Holding AG's reliance on steel scrap as its primary input for its 100% electric arc furnace (EAF) operations significantly amplifies supplier bargaining power. The global scrap market is inherently volatile, and any disruptions or increased demand can lead to price surges, directly impacting Swiss Steel's cost of goods sold.

Beyond scrap, the availability and pricing of critical alloying elements such as nickel and chromium are also key determinants of supplier leverage. These materials are essential for producing specialized steel grades, and limited global supply or concentrated production can give suppliers considerable pricing power, squeezing margins for Swiss Steel.

Furthermore, energy costs, specifically electricity for the EAF process, represent another substantial input cost. In 2024, European energy markets remained susceptible to geopolitical factors and supply chain issues, allowing electricity providers to exert significant influence over Swiss Steel's operational expenses and overall profitability.

Concentration of Specialized Alloy Suppliers

The production of specialized steels, like those Swiss Steel Holding focuses on, relies heavily on specific alloying materials. When only a few suppliers can provide these crucial, often niche, alloys, their leverage grows significantly. This concentration means Swiss Steel, and similar manufacturers, face a higher risk of increased input costs as these specialized suppliers can dictate terms.

For instance, the global market for certain high-performance alloys used in demanding applications can be quite limited. If Swiss Steel needs a particular vanadium or molybdenum alloy that only a handful of companies produce, those suppliers hold considerable sway. This directly impacts Swiss Steel’s cost structure and profitability, making supplier relationships critical.

In response to this, Swiss Steel Holding is strategically investing in vertical integration, particularly in alloy recycling. By developing its own capabilities to recover and reuse valuable alloys, the company aims to lessen its dependence on external, concentrated suppliers. This move not only strengthens its bargaining position but also enhances supply chain resilience and potentially lowers material costs over the long term.

Influence of Decarbonization Technology Providers

Swiss Steel's drive towards climate-neutral steel production, a key part of its 2024 strategy, significantly boosts the bargaining power of suppliers offering advanced decarbonization technologies. The company's substantial investments in areas like electric arc furnaces and hydrogen solutions mean these specialized providers are essential partners in achieving ambitious environmental goals.

Availability of Skilled Labor

The manufacturing of special long steel products by Swiss Steel Holding relies heavily on a workforce possessing specialized metallurgical knowledge and advanced production skills. A shortage of these highly qualified individuals in key operating regions can significantly amplify the bargaining power of employees. This scarcity translates into potential upward pressure on wages and complicates the process of finding and retaining talent, directly impacting operational costs and the ability to innovate.

The availability of skilled labor is a crucial factor influencing the bargaining power of suppliers in the special long steel sector. For Swiss Steel, this relates to the human capital required for intricate manufacturing and processing.

- Specialized Expertise: The production of special long steel demands deep knowledge in metallurgy, advanced manufacturing, and stringent quality control, making skilled labor a unique input.

- Labor Scarcity Impact: A limited pool of qualified workers in operational areas enhances employee leverage, potentially driving up labor costs for Swiss Steel.

- Human Capital Value: This skilled workforce is indispensable for ensuring high product quality and fostering innovation within the company.

- Recruitment Challenges: Difficulty in sourcing and retaining such specialized personnel can create significant operational hurdles and increase recruitment expenses.

Logistics and Transportation Service Providers

Swiss Steel Holding, with its extensive global footprint of 69 locations across 26 countries, is significantly dependent on logistics and transportation service providers. These providers hold considerable bargaining power, especially when facing volatile fuel prices or disruptions in global supply chains. For instance, the International Monetary Fund (IMF) projected that global shipping costs saw a notable increase in early 2024 due to geopolitical tensions and rising insurance premiums, directly impacting companies like Swiss Steel.

The ability of logistics firms to dictate terms, pricing, and service levels can directly influence Swiss Steel's operational costs and the timely delivery of its products. In 2024, the trucking industry in many regions experienced driver shortages and increased labor costs, further strengthening the hand of established logistics companies. This situation forces Swiss Steel to potentially absorb higher transportation expenses or negotiate more complex contracts to ensure supply chain continuity.

- Increased Fuel Costs: Fluctuations in global oil prices directly impact transportation expenses, giving fuel-efficient or strategically located providers more leverage.

- Supply Chain Disruptions: Events like port congestion or geopolitical instability can reduce the availability of shipping capacity, empowering remaining providers.

- Specialized Handling Needs: If Swiss Steel requires specialized transport for certain steel products, providers with that expertise gain stronger bargaining power.

- Limited Provider Options: In specific geographic regions, a limited number of qualified logistics providers can consolidate power.

Suppliers' Strong Hand: Shaping Steel's Costs and Future

The bargaining power of suppliers for Swiss Steel Holding is notably high due to its reliance on essential raw materials like steel scrap and specialized alloys. The global nature of these markets, coupled with potential supply chain vulnerabilities, allows suppliers to influence pricing and terms. Furthermore, the increasing demand for decarbonization technologies in 2024 places significant leverage with providers of these advanced solutions, impacting Swiss Steel's strategic investments and operational costs.

The company's extensive global operations mean that logistics and transportation providers also wield substantial influence. Factors such as fluctuating fuel costs, driver shortages in 2024, and geopolitical disruptions can empower these service providers to dictate terms, directly affecting Swiss Steel's delivery timelines and overall expenses.

| Input Material/Service | Supplier Bargaining Power Factor | Impact on Swiss Steel | 2024 Data Point/Trend |

|---|---|---|---|

| Steel Scrap | Concentration of suppliers, market volatility | Increased cost of goods sold | Global scrap prices experienced fluctuations driven by demand and supply imbalances. |

| Alloying Elements (Nickel, Chromium) | Limited global supply, concentrated production | Higher input costs, potential margin squeeze | Prices for key alloys remained sensitive to geopolitical events and industrial demand. |

| Electricity | Geopolitical factors, energy market dynamics | Elevated operational expenses | European electricity prices remained volatile in 2024, influenced by energy security concerns. |

| Decarbonization Technologies | Essential for climate goals, specialized providers | Supplier leverage in strategic investments | Demand for green steel technologies surged, increasing the negotiating power of technology providers. |

| Logistics & Transportation | Fuel price volatility, driver shortages, supply chain disruptions | Higher transportation costs, delivery risks | Global shipping costs saw increases in early 2024 due to geopolitical tensions and insurance premiums. |

What is included in the product

This analysis uncovers key drivers of competition, customer influence, and market entry risks tailored to Swiss Steel Holding's position in the steel industry.

Instantly grasp the competitive landscape of Swiss Steel Holding with a visual breakdown of Porter's Five Forces, simplifying complex strategic pressures.

Customers Bargaining Power

Criticality of Special Steel Products

Swiss Steel Holding's special steel products, like tool steel, engineering steel, and stainless long steel, are vital for high-demand sectors such as automotive and mechanical engineering. These materials are essential for performance-critical applications, meaning customers often cannot easily switch to inferior alternatives. This inherent criticality significantly limits the bargaining power of customers.

Customer Base Segmentation and Volume

Swiss Steel serves over 20,000 customers worldwide, with a significant portion of its revenue coming from high-volume buyers in demanding sectors like automotive and mechanical engineering. These large clients, often representing substantial portions of Swiss Steel's order books, wield considerable power to negotiate favorable pricing, delivery schedules, and even product customizations. For instance, a major automotive manufacturer might represent 5-10% of a specific steel product's annual output, giving them considerable leverage.

Despite this potential for customer power, the highly specialized nature of Swiss Steel's product portfolio, particularly in areas like high-performance alloys and precision steel, often cultivates deeper, more strategic relationships. These partnerships can mitigate some of the price-based bargaining power, as customers value the unique technical expertise and tailored solutions provided, rather than solely focusing on commodity pricing. This specialization can shift the negotiation focus from pure price to value-added services and product performance.

High Switching Costs for Specialized Applications

For specialized applications, customers often encounter significant switching costs when considering a change in steel suppliers. These costs can encompass rigorous qualification procedures, extensive technical validation, and even the potential need for re-engineering of their own components to accommodate different material specifications. For example, in the automotive sector, a supplier of critical engine parts might need to recertify their entire production line and re-run crash tests if they switch from a specific steel grade, a process that can easily run into hundreds of thousands of euros and months of delay.

Sensitivity to Demand Fluctuations in End Markets

The bargaining power of customers for Swiss Steel Holding is significantly influenced by how sensitive demand for special long steel is to fluctuations in its end markets, particularly automotive and construction. These sectors are crucial for steel consumption.

Recent analyses for 2024 highlight a challenging environment for European steel demand, marked by a downturn and considerable uncertainty. Projections suggest a subdued recovery extending into 2025.

This weak demand environment directly amplifies customer bargaining power. As steel producers face fewer orders, they tend to compete more fiercely for the business that is available, often resulting in downward pressure on prices.

- End Market Sensitivity: Demand for special long steel is highly dependent on the health of the automotive and construction industries.

- 2024 Demand Outlook: European steel consumption experienced a downturn in 2024, with significant uncertainty persisting.

- 2025 Recovery Forecast: Projections indicate a slower-than-expected recovery in steel demand for 2025.

- Impact on Bargaining Power: Weak demand forces producers into aggressive competition, increasing customer leverage and potentially lowering prices.

Growing Demand for Sustainable Products

Customers are increasingly prioritizing sustainability, driving demand for 'Green Steel' with a significantly reduced carbon footprint. This trend directly impacts the bargaining power of customers, as those seeking environmentally responsible materials may be willing to pay a premium or exert pressure on suppliers to meet these criteria.

Swiss Steel Holding is well-positioned to address this growing demand. Their production process, utilizing a 100% Electric Arc Furnace (EAF) route, results in up to 83% lower emissions compared to industry averages. This strong differentiator allows them to cater to a segment of the market that values and actively seeks out sustainable material solutions.

- Growing customer preference for sustainable products

- Swiss Steel's 100% EAF route offers up to 83% lower emissions

- Potential for premium pricing due to reduced carbon footprint

- Ability to mitigate price pressure from environmentally conscious buyers

Swiss Steel Customer Leverage: Specialization vs. 2024 Demand Downturn

The bargaining power of customers for Swiss Steel Holding is a key consideration, influenced by market conditions and product specialization. While the highly specialized nature of their steel products limits customer options, the current economic climate in 2024 presents challenges.

European steel demand saw a downturn in 2024, with projections indicating a subdued recovery into 2025. This weak demand environment increases customer leverage, as producers compete more intensely for available business, potentially driving down prices.

| Factor | Impact on Bargaining Power | Relevant Data/Context |

|---|---|---|

| Product Specialization | Lowers bargaining power due to high switching costs and unique technical value. | Critical applications in automotive and mechanical engineering limit easy substitution. |

| Market Demand (2024) | Increases bargaining power due to weak demand. | European steel demand experienced a downturn in 2024, with slow recovery expected in 2025. |

| Sustainability Focus | Can increase bargaining power for those demanding 'Green Steel'. | Swiss Steel's 100% EAF route offers up to 83% lower emissions, potentially mitigating this. |

Preview the Actual Deliverable

Swiss Steel Holding Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It details the Swiss Steel Holding Porter's Five Forces Analysis, offering a comprehensive examination of industry rivalry, the threat of new entrants, the bargaining power of buyers, the bargaining power of suppliers, and the threat of substitute products. This in-depth analysis provides actionable insights into the competitive landscape of the steel industry.

Don't Miss the Bigger Picture

Swiss Steel Holding faces moderate bargaining power from buyers due to industry fragmentation, but intense rivalry among existing players exerts significant pressure. The threat of substitutes, while present, is somewhat mitigated by the specialized nature of steel products.

The complete report reveals the real forces shaping Swiss Steel Holding’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Reliance on Key Raw Materials

Swiss Steel Holding AG's reliance on steel scrap as its primary input for its 100% electric arc furnace (EAF) operations significantly amplifies supplier bargaining power. The global scrap market is inherently volatile, and any disruptions or increased demand can lead to price surges, directly impacting Swiss Steel's cost of goods sold.

Beyond scrap, the availability and pricing of critical alloying elements such as nickel and chromium are also key determinants of supplier leverage. These materials are essential for producing specialized steel grades, and limited global supply or concentrated production can give suppliers considerable pricing power, squeezing margins for Swiss Steel.

Furthermore, energy costs, specifically electricity for the EAF process, represent another substantial input cost. In 2024, European energy markets remained susceptible to geopolitical factors and supply chain issues, allowing electricity providers to exert significant influence over Swiss Steel's operational expenses and overall profitability.

Concentration of Specialized Alloy Suppliers

The production of specialized steels, like those Swiss Steel Holding focuses on, relies heavily on specific alloying materials. When only a few suppliers can provide these crucial, often niche, alloys, their leverage grows significantly. This concentration means Swiss Steel, and similar manufacturers, face a higher risk of increased input costs as these specialized suppliers can dictate terms.

For instance, the global market for certain high-performance alloys used in demanding applications can be quite limited. If Swiss Steel needs a particular vanadium or molybdenum alloy that only a handful of companies produce, those suppliers hold considerable sway. This directly impacts Swiss Steel’s cost structure and profitability, making supplier relationships critical.

In response to this, Swiss Steel Holding is strategically investing in vertical integration, particularly in alloy recycling. By developing its own capabilities to recover and reuse valuable alloys, the company aims to lessen its dependence on external, concentrated suppliers. This move not only strengthens its bargaining position but also enhances supply chain resilience and potentially lowers material costs over the long term.

Influence of Decarbonization Technology Providers

Swiss Steel's drive towards climate-neutral steel production, a key part of its 2024 strategy, significantly boosts the bargaining power of suppliers offering advanced decarbonization technologies. The company's substantial investments in areas like electric arc furnaces and hydrogen solutions mean these specialized providers are essential partners in achieving ambitious environmental goals.

Availability of Skilled Labor

The manufacturing of special long steel products by Swiss Steel Holding relies heavily on a workforce possessing specialized metallurgical knowledge and advanced production skills. A shortage of these highly qualified individuals in key operating regions can significantly amplify the bargaining power of employees. This scarcity translates into potential upward pressure on wages and complicates the process of finding and retaining talent, directly impacting operational costs and the ability to innovate.

The availability of skilled labor is a crucial factor influencing the bargaining power of suppliers in the special long steel sector. For Swiss Steel, this relates to the human capital required for intricate manufacturing and processing.

- Specialized Expertise: The production of special long steel demands deep knowledge in metallurgy, advanced manufacturing, and stringent quality control, making skilled labor a unique input.

- Labor Scarcity Impact: A limited pool of qualified workers in operational areas enhances employee leverage, potentially driving up labor costs for Swiss Steel.

- Human Capital Value: This skilled workforce is indispensable for ensuring high product quality and fostering innovation within the company.

- Recruitment Challenges: Difficulty in sourcing and retaining such specialized personnel can create significant operational hurdles and increase recruitment expenses.

Logistics and Transportation Service Providers

Swiss Steel Holding, with its extensive global footprint of 69 locations across 26 countries, is significantly dependent on logistics and transportation service providers. These providers hold considerable bargaining power, especially when facing volatile fuel prices or disruptions in global supply chains. For instance, the International Monetary Fund (IMF) projected that global shipping costs saw a notable increase in early 2024 due to geopolitical tensions and rising insurance premiums, directly impacting companies like Swiss Steel.

The ability of logistics firms to dictate terms, pricing, and service levels can directly influence Swiss Steel's operational costs and the timely delivery of its products. In 2024, the trucking industry in many regions experienced driver shortages and increased labor costs, further strengthening the hand of established logistics companies. This situation forces Swiss Steel to potentially absorb higher transportation expenses or negotiate more complex contracts to ensure supply chain continuity.

- Increased Fuel Costs: Fluctuations in global oil prices directly impact transportation expenses, giving fuel-efficient or strategically located providers more leverage.

- Supply Chain Disruptions: Events like port congestion or geopolitical instability can reduce the availability of shipping capacity, empowering remaining providers.

- Specialized Handling Needs: If Swiss Steel requires specialized transport for certain steel products, providers with that expertise gain stronger bargaining power.

- Limited Provider Options: In specific geographic regions, a limited number of qualified logistics providers can consolidate power.

Suppliers' Strong Hand: Shaping Steel's Costs and Future

The bargaining power of suppliers for Swiss Steel Holding is notably high due to its reliance on essential raw materials like steel scrap and specialized alloys. The global nature of these markets, coupled with potential supply chain vulnerabilities, allows suppliers to influence pricing and terms. Furthermore, the increasing demand for decarbonization technologies in 2024 places significant leverage with providers of these advanced solutions, impacting Swiss Steel's strategic investments and operational costs.

The company's extensive global operations mean that logistics and transportation providers also wield substantial influence. Factors such as fluctuating fuel costs, driver shortages in 2024, and geopolitical disruptions can empower these service providers to dictate terms, directly affecting Swiss Steel's delivery timelines and overall expenses.

| Input Material/Service | Supplier Bargaining Power Factor | Impact on Swiss Steel | 2024 Data Point/Trend |

|---|---|---|---|

| Steel Scrap | Concentration of suppliers, market volatility | Increased cost of goods sold | Global scrap prices experienced fluctuations driven by demand and supply imbalances. |

| Alloying Elements (Nickel, Chromium) | Limited global supply, concentrated production | Higher input costs, potential margin squeeze | Prices for key alloys remained sensitive to geopolitical events and industrial demand. |

| Electricity | Geopolitical factors, energy market dynamics | Elevated operational expenses | European electricity prices remained volatile in 2024, influenced by energy security concerns. |

| Decarbonization Technologies | Essential for climate goals, specialized providers | Supplier leverage in strategic investments | Demand for green steel technologies surged, increasing the negotiating power of technology providers. |

| Logistics & Transportation | Fuel price volatility, driver shortages, supply chain disruptions | Higher transportation costs, delivery risks | Global shipping costs saw increases in early 2024 due to geopolitical tensions and insurance premiums. |

What is included in the product

This analysis uncovers key drivers of competition, customer influence, and market entry risks tailored to Swiss Steel Holding's position in the steel industry.

Instantly grasp the competitive landscape of Swiss Steel Holding with a visual breakdown of Porter's Five Forces, simplifying complex strategic pressures.

Customers Bargaining Power

Criticality of Special Steel Products

Swiss Steel Holding's special steel products, like tool steel, engineering steel, and stainless long steel, are vital for high-demand sectors such as automotive and mechanical engineering. These materials are essential for performance-critical applications, meaning customers often cannot easily switch to inferior alternatives. This inherent criticality significantly limits the bargaining power of customers.

Customer Base Segmentation and Volume

Swiss Steel serves over 20,000 customers worldwide, with a significant portion of its revenue coming from high-volume buyers in demanding sectors like automotive and mechanical engineering. These large clients, often representing substantial portions of Swiss Steel's order books, wield considerable power to negotiate favorable pricing, delivery schedules, and even product customizations. For instance, a major automotive manufacturer might represent 5-10% of a specific steel product's annual output, giving them considerable leverage.

Despite this potential for customer power, the highly specialized nature of Swiss Steel's product portfolio, particularly in areas like high-performance alloys and precision steel, often cultivates deeper, more strategic relationships. These partnerships can mitigate some of the price-based bargaining power, as customers value the unique technical expertise and tailored solutions provided, rather than solely focusing on commodity pricing. This specialization can shift the negotiation focus from pure price to value-added services and product performance.

High Switching Costs for Specialized Applications

For specialized applications, customers often encounter significant switching costs when considering a change in steel suppliers. These costs can encompass rigorous qualification procedures, extensive technical validation, and even the potential need for re-engineering of their own components to accommodate different material specifications. For example, in the automotive sector, a supplier of critical engine parts might need to recertify their entire production line and re-run crash tests if they switch from a specific steel grade, a process that can easily run into hundreds of thousands of euros and months of delay.

Sensitivity to Demand Fluctuations in End Markets

The bargaining power of customers for Swiss Steel Holding is significantly influenced by how sensitive demand for special long steel is to fluctuations in its end markets, particularly automotive and construction. These sectors are crucial for steel consumption.

Recent analyses for 2024 highlight a challenging environment for European steel demand, marked by a downturn and considerable uncertainty. Projections suggest a subdued recovery extending into 2025.

This weak demand environment directly amplifies customer bargaining power. As steel producers face fewer orders, they tend to compete more fiercely for the business that is available, often resulting in downward pressure on prices.

- End Market Sensitivity: Demand for special long steel is highly dependent on the health of the automotive and construction industries.

- 2024 Demand Outlook: European steel consumption experienced a downturn in 2024, with significant uncertainty persisting.

- 2025 Recovery Forecast: Projections indicate a slower-than-expected recovery in steel demand for 2025.

- Impact on Bargaining Power: Weak demand forces producers into aggressive competition, increasing customer leverage and potentially lowering prices.

Growing Demand for Sustainable Products

Customers are increasingly prioritizing sustainability, driving demand for 'Green Steel' with a significantly reduced carbon footprint. This trend directly impacts the bargaining power of customers, as those seeking environmentally responsible materials may be willing to pay a premium or exert pressure on suppliers to meet these criteria.

Swiss Steel Holding is well-positioned to address this growing demand. Their production process, utilizing a 100% Electric Arc Furnace (EAF) route, results in up to 83% lower emissions compared to industry averages. This strong differentiator allows them to cater to a segment of the market that values and actively seeks out sustainable material solutions.

- Growing customer preference for sustainable products

- Swiss Steel's 100% EAF route offers up to 83% lower emissions

- Potential for premium pricing due to reduced carbon footprint

- Ability to mitigate price pressure from environmentally conscious buyers

Swiss Steel Customer Leverage: Specialization vs. 2024 Demand Downturn

The bargaining power of customers for Swiss Steel Holding is a key consideration, influenced by market conditions and product specialization. While the highly specialized nature of their steel products limits customer options, the current economic climate in 2024 presents challenges.

European steel demand saw a downturn in 2024, with projections indicating a subdued recovery into 2025. This weak demand environment increases customer leverage, as producers compete more intensely for available business, potentially driving down prices.

| Factor | Impact on Bargaining Power | Relevant Data/Context |

|---|---|---|

| Product Specialization | Lowers bargaining power due to high switching costs and unique technical value. | Critical applications in automotive and mechanical engineering limit easy substitution. |

| Market Demand (2024) | Increases bargaining power due to weak demand. | European steel demand experienced a downturn in 2024, with slow recovery expected in 2025. |

| Sustainability Focus | Can increase bargaining power for those demanding 'Green Steel'. | Swiss Steel's 100% EAF route offers up to 83% lower emissions, potentially mitigating this. |

Preview the Actual Deliverable

Swiss Steel Holding Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It details the Swiss Steel Holding Porter's Five Forces Analysis, offering a comprehensive examination of industry rivalry, the threat of new entrants, the bargaining power of buyers, the bargaining power of suppliers, and the threat of substitute products. This in-depth analysis provides actionable insights into the competitive landscape of the steel industry.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Swiss Steel Holding faces moderate bargaining power from buyers due to industry fragmentation, but intense rivalry among existing players exerts significant pressure. The threat of substitutes, while present, is somewhat mitigated by the specialized nature of steel products.

The complete report reveals the real forces shaping Swiss Steel Holding’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Reliance on Key Raw Materials

Swiss Steel Holding AG's reliance on steel scrap as its primary input for its 100% electric arc furnace (EAF) operations significantly amplifies supplier bargaining power. The global scrap market is inherently volatile, and any disruptions or increased demand can lead to price surges, directly impacting Swiss Steel's cost of goods sold.

Beyond scrap, the availability and pricing of critical alloying elements such as nickel and chromium are also key determinants of supplier leverage. These materials are essential for producing specialized steel grades, and limited global supply or concentrated production can give suppliers considerable pricing power, squeezing margins for Swiss Steel.

Furthermore, energy costs, specifically electricity for the EAF process, represent another substantial input cost. In 2024, European energy markets remained susceptible to geopolitical factors and supply chain issues, allowing electricity providers to exert significant influence over Swiss Steel's operational expenses and overall profitability.

Concentration of Specialized Alloy Suppliers

The production of specialized steels, like those Swiss Steel Holding focuses on, relies heavily on specific alloying materials. When only a few suppliers can provide these crucial, often niche, alloys, their leverage grows significantly. This concentration means Swiss Steel, and similar manufacturers, face a higher risk of increased input costs as these specialized suppliers can dictate terms.

For instance, the global market for certain high-performance alloys used in demanding applications can be quite limited. If Swiss Steel needs a particular vanadium or molybdenum alloy that only a handful of companies produce, those suppliers hold considerable sway. This directly impacts Swiss Steel’s cost structure and profitability, making supplier relationships critical.

In response to this, Swiss Steel Holding is strategically investing in vertical integration, particularly in alloy recycling. By developing its own capabilities to recover and reuse valuable alloys, the company aims to lessen its dependence on external, concentrated suppliers. This move not only strengthens its bargaining position but also enhances supply chain resilience and potentially lowers material costs over the long term.

Influence of Decarbonization Technology Providers

Swiss Steel's drive towards climate-neutral steel production, a key part of its 2024 strategy, significantly boosts the bargaining power of suppliers offering advanced decarbonization technologies. The company's substantial investments in areas like electric arc furnaces and hydrogen solutions mean these specialized providers are essential partners in achieving ambitious environmental goals.

Availability of Skilled Labor

The manufacturing of special long steel products by Swiss Steel Holding relies heavily on a workforce possessing specialized metallurgical knowledge and advanced production skills. A shortage of these highly qualified individuals in key operating regions can significantly amplify the bargaining power of employees. This scarcity translates into potential upward pressure on wages and complicates the process of finding and retaining talent, directly impacting operational costs and the ability to innovate.

The availability of skilled labor is a crucial factor influencing the bargaining power of suppliers in the special long steel sector. For Swiss Steel, this relates to the human capital required for intricate manufacturing and processing.

- Specialized Expertise: The production of special long steel demands deep knowledge in metallurgy, advanced manufacturing, and stringent quality control, making skilled labor a unique input.

- Labor Scarcity Impact: A limited pool of qualified workers in operational areas enhances employee leverage, potentially driving up labor costs for Swiss Steel.

- Human Capital Value: This skilled workforce is indispensable for ensuring high product quality and fostering innovation within the company.

- Recruitment Challenges: Difficulty in sourcing and retaining such specialized personnel can create significant operational hurdles and increase recruitment expenses.

Logistics and Transportation Service Providers

Swiss Steel Holding, with its extensive global footprint of 69 locations across 26 countries, is significantly dependent on logistics and transportation service providers. These providers hold considerable bargaining power, especially when facing volatile fuel prices or disruptions in global supply chains. For instance, the International Monetary Fund (IMF) projected that global shipping costs saw a notable increase in early 2024 due to geopolitical tensions and rising insurance premiums, directly impacting companies like Swiss Steel.

The ability of logistics firms to dictate terms, pricing, and service levels can directly influence Swiss Steel's operational costs and the timely delivery of its products. In 2024, the trucking industry in many regions experienced driver shortages and increased labor costs, further strengthening the hand of established logistics companies. This situation forces Swiss Steel to potentially absorb higher transportation expenses or negotiate more complex contracts to ensure supply chain continuity.

- Increased Fuel Costs: Fluctuations in global oil prices directly impact transportation expenses, giving fuel-efficient or strategically located providers more leverage.

- Supply Chain Disruptions: Events like port congestion or geopolitical instability can reduce the availability of shipping capacity, empowering remaining providers.

- Specialized Handling Needs: If Swiss Steel requires specialized transport for certain steel products, providers with that expertise gain stronger bargaining power.

- Limited Provider Options: In specific geographic regions, a limited number of qualified logistics providers can consolidate power.

Suppliers' Strong Hand: Shaping Steel's Costs and Future

The bargaining power of suppliers for Swiss Steel Holding is notably high due to its reliance on essential raw materials like steel scrap and specialized alloys. The global nature of these markets, coupled with potential supply chain vulnerabilities, allows suppliers to influence pricing and terms. Furthermore, the increasing demand for decarbonization technologies in 2024 places significant leverage with providers of these advanced solutions, impacting Swiss Steel's strategic investments and operational costs.

The company's extensive global operations mean that logistics and transportation providers also wield substantial influence. Factors such as fluctuating fuel costs, driver shortages in 2024, and geopolitical disruptions can empower these service providers to dictate terms, directly affecting Swiss Steel's delivery timelines and overall expenses.

| Input Material/Service | Supplier Bargaining Power Factor | Impact on Swiss Steel | 2024 Data Point/Trend |

|---|---|---|---|

| Steel Scrap | Concentration of suppliers, market volatility | Increased cost of goods sold | Global scrap prices experienced fluctuations driven by demand and supply imbalances. |

| Alloying Elements (Nickel, Chromium) | Limited global supply, concentrated production | Higher input costs, potential margin squeeze | Prices for key alloys remained sensitive to geopolitical events and industrial demand. |

| Electricity | Geopolitical factors, energy market dynamics | Elevated operational expenses | European electricity prices remained volatile in 2024, influenced by energy security concerns. |

| Decarbonization Technologies | Essential for climate goals, specialized providers | Supplier leverage in strategic investments | Demand for green steel technologies surged, increasing the negotiating power of technology providers. |

| Logistics & Transportation | Fuel price volatility, driver shortages, supply chain disruptions | Higher transportation costs, delivery risks | Global shipping costs saw increases in early 2024 due to geopolitical tensions and insurance premiums. |

What is included in the product

This analysis uncovers key drivers of competition, customer influence, and market entry risks tailored to Swiss Steel Holding's position in the steel industry.

Instantly grasp the competitive landscape of Swiss Steel Holding with a visual breakdown of Porter's Five Forces, simplifying complex strategic pressures.

Customers Bargaining Power

Criticality of Special Steel Products

Swiss Steel Holding's special steel products, like tool steel, engineering steel, and stainless long steel, are vital for high-demand sectors such as automotive and mechanical engineering. These materials are essential for performance-critical applications, meaning customers often cannot easily switch to inferior alternatives. This inherent criticality significantly limits the bargaining power of customers.

Customer Base Segmentation and Volume

Swiss Steel serves over 20,000 customers worldwide, with a significant portion of its revenue coming from high-volume buyers in demanding sectors like automotive and mechanical engineering. These large clients, often representing substantial portions of Swiss Steel's order books, wield considerable power to negotiate favorable pricing, delivery schedules, and even product customizations. For instance, a major automotive manufacturer might represent 5-10% of a specific steel product's annual output, giving them considerable leverage.

Despite this potential for customer power, the highly specialized nature of Swiss Steel's product portfolio, particularly in areas like high-performance alloys and precision steel, often cultivates deeper, more strategic relationships. These partnerships can mitigate some of the price-based bargaining power, as customers value the unique technical expertise and tailored solutions provided, rather than solely focusing on commodity pricing. This specialization can shift the negotiation focus from pure price to value-added services and product performance.

High Switching Costs for Specialized Applications

For specialized applications, customers often encounter significant switching costs when considering a change in steel suppliers. These costs can encompass rigorous qualification procedures, extensive technical validation, and even the potential need for re-engineering of their own components to accommodate different material specifications. For example, in the automotive sector, a supplier of critical engine parts might need to recertify their entire production line and re-run crash tests if they switch from a specific steel grade, a process that can easily run into hundreds of thousands of euros and months of delay.

Sensitivity to Demand Fluctuations in End Markets

The bargaining power of customers for Swiss Steel Holding is significantly influenced by how sensitive demand for special long steel is to fluctuations in its end markets, particularly automotive and construction. These sectors are crucial for steel consumption.

Recent analyses for 2024 highlight a challenging environment for European steel demand, marked by a downturn and considerable uncertainty. Projections suggest a subdued recovery extending into 2025.

This weak demand environment directly amplifies customer bargaining power. As steel producers face fewer orders, they tend to compete more fiercely for the business that is available, often resulting in downward pressure on prices.

- End Market Sensitivity: Demand for special long steel is highly dependent on the health of the automotive and construction industries.

- 2024 Demand Outlook: European steel consumption experienced a downturn in 2024, with significant uncertainty persisting.

- 2025 Recovery Forecast: Projections indicate a slower-than-expected recovery in steel demand for 2025.

- Impact on Bargaining Power: Weak demand forces producers into aggressive competition, increasing customer leverage and potentially lowering prices.

Growing Demand for Sustainable Products

Customers are increasingly prioritizing sustainability, driving demand for 'Green Steel' with a significantly reduced carbon footprint. This trend directly impacts the bargaining power of customers, as those seeking environmentally responsible materials may be willing to pay a premium or exert pressure on suppliers to meet these criteria.

Swiss Steel Holding is well-positioned to address this growing demand. Their production process, utilizing a 100% Electric Arc Furnace (EAF) route, results in up to 83% lower emissions compared to industry averages. This strong differentiator allows them to cater to a segment of the market that values and actively seeks out sustainable material solutions.

- Growing customer preference for sustainable products

- Swiss Steel's 100% EAF route offers up to 83% lower emissions

- Potential for premium pricing due to reduced carbon footprint

- Ability to mitigate price pressure from environmentally conscious buyers

Swiss Steel Customer Leverage: Specialization vs. 2024 Demand Downturn

The bargaining power of customers for Swiss Steel Holding is a key consideration, influenced by market conditions and product specialization. While the highly specialized nature of their steel products limits customer options, the current economic climate in 2024 presents challenges.

European steel demand saw a downturn in 2024, with projections indicating a subdued recovery into 2025. This weak demand environment increases customer leverage, as producers compete more intensely for available business, potentially driving down prices.

| Factor | Impact on Bargaining Power | Relevant Data/Context |

|---|---|---|

| Product Specialization | Lowers bargaining power due to high switching costs and unique technical value. | Critical applications in automotive and mechanical engineering limit easy substitution. |

| Market Demand (2024) | Increases bargaining power due to weak demand. | European steel demand experienced a downturn in 2024, with slow recovery expected in 2025. |

| Sustainability Focus | Can increase bargaining power for those demanding 'Green Steel'. | Swiss Steel's 100% EAF route offers up to 83% lower emissions, potentially mitigating this. |

Preview the Actual Deliverable

Swiss Steel Holding Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It details the Swiss Steel Holding Porter's Five Forces Analysis, offering a comprehensive examination of industry rivalry, the threat of new entrants, the bargaining power of buyers, the bargaining power of suppliers, and the threat of substitute products. This in-depth analysis provides actionable insights into the competitive landscape of the steel industry.