Sydbank Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

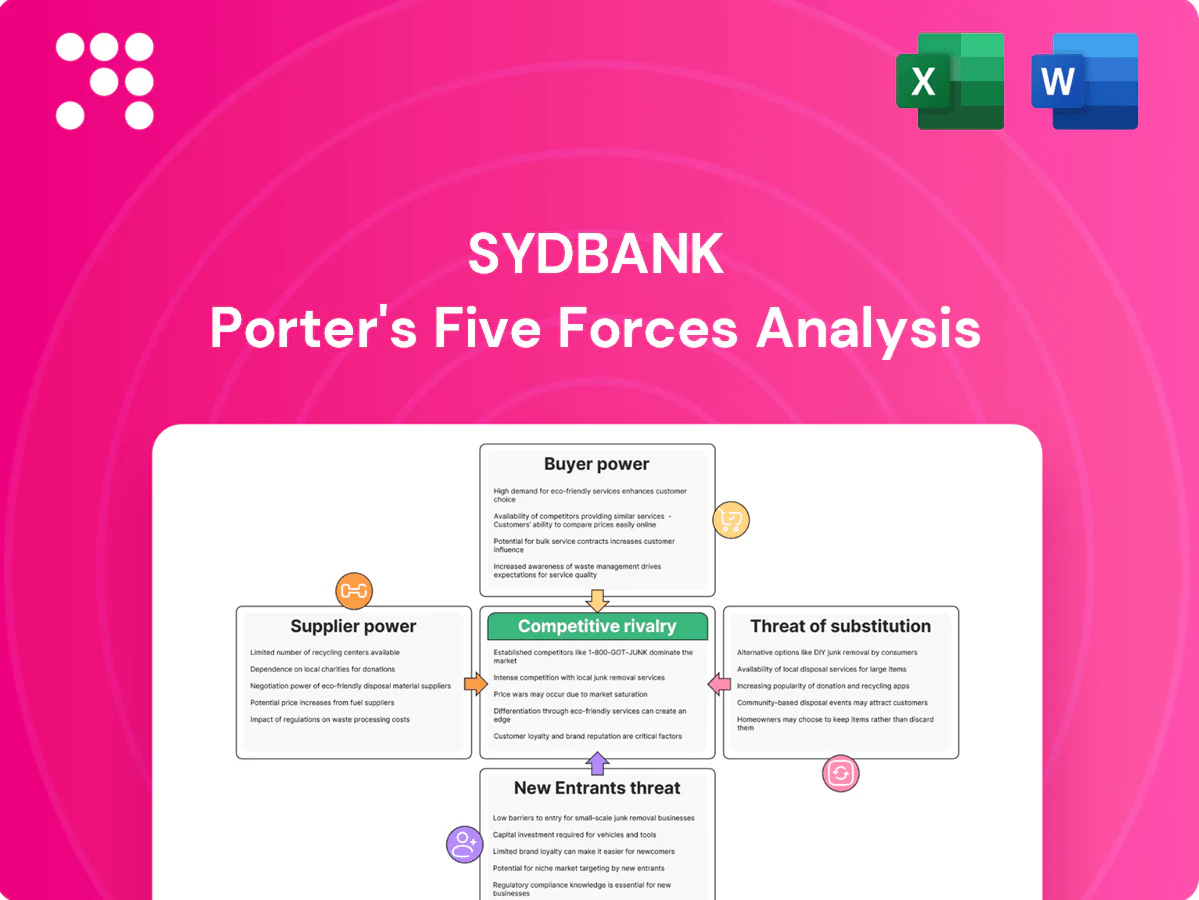

Sydbank’s competitive landscape is shaped by concentrated buyer power, regulatory pressures, and a moderate threat from digital disruptors. Supplier influence is limited but compliance costs compress margins. Regional rivalry and price competition intensify strategic trade-offs. This snapshot scratches the surface—unlock the full Porter's Five Forces for detailed force ratings and actionable strategy.

Suppliers Bargaining Power

Dependence on core IT vendors

Dependence on core banking platforms, cloud providers and cybersecurity firms concentrates supplier power, as the top three cloud vendors hold roughly two-thirds of global market share in 2024, raising switching costs and lock-in risks for Sydbank. Complex integrations and long contracts can increase IT expenditure and reduce leverage, but multi-vendor strategies and EU/Danish outsourcing scrutiny limit worst-case outcomes. Sydbank’s scale across Denmark and Northern Germany strengthens negotiation on SLAs and pricing.

Card and payments networks

Card networks (Visa/Mastercard) and Denmark’s Dankort plus instant rails (MobilePay/real‑time transfers) are essential, giving schemes fee-setting leverage; Visa/Mastercard dominate global scheme volumes (>70%) while EU caps limit interchange to 0.2% (debit) / 0.3% (credit) under Regulation 2015/751. Interchange, scheme fees and compliance pressures materially compress Sydbank’s unit economics; some costs can be passed to merchants/customers but competitive caps and domestic rails like Dankort provide only partial counterbalance.

Wholesale funding providers

Money markets, covered-bond investors and interbank lenders set Sydbank’s funding cost and availability; 3-month EURIBOR averaged about 3.9% in 2024, and covered-bond spreads have moved +/-50–100bp in stress episodes, quickly lifting interest expense and squeezing margins. Sydbank reports diversified funding and liquidity buffers—wholesale funding concentration is limited and LCR remains well above regulatory minimums—reducing single-channel dependence, while deep Nordic/European investor ties secure better terms.

Specialist data and service partners

Specialist suppliers (credit bureaus, KYC/AML utilities, market-data vendors) wield niche power because services are regulatory must-haves; Bloomberg terminals cost about 27,000 USD/yr (2024) and model-validation/supervisory cycles often take 3–6 months, making switching cumbersome, while Nordic consortium KYC projects have cut unit fees roughly 15–20% and volume commitments unlock better pricing tiers.

- Credit bureaus: regulatory dependency

- KYC/AML: validation 3–6 months

- Market data: Bloomberg ~27,000 USD/yr (2024)

- Consortiums: ~15–20% fee dilution

- Volume: secures lower pricing tiers

Skilled labor and compliance talent

Competition for engineers, risk and AML specialists is tight in 2024, lifting wage pressure and making skilled talent a supplier-like constraint for Sydbank; Statistics Denmark reported unemployment at about 3.8% in 2024, tightening labor availability. Talent scarcity increases bargaining power of the labor market, while hybrid work and nearshoring can expand candidate pools and help dampen costs; Sydbank’s strong Danish employer brand aids attraction and retention.

- Labor tightness: 2024 unemployment ~3.8% (Statistics Denmark)

- Supplier power: higher for AML/risk/engineers due to scarcity

- Mitigants: hybrid work, nearshoring, and strong Danish employer brand

Top‑3 cloud~66%|cards>70%|funding3.9%

Supplier power is elevated: top‑3 cloud vendors ~66% share (2024), Visa/Mastercard >70% global scheme volume, EU interchange caps 0.2%/0.3%. Funding cost pressure: 3m EURIBOR ~3.9% (2024). Specialist tools costly (Bloomberg ~27,000 USD/yr) and labor tight (Denmark unemployment ~3.8%).

| Item | 2024 |

|---|---|

| Top‑3 cloud share | ~66% |

| Card networks | >70% |

| 3m EURIBOR | ~3.9% |

| Bloomberg | ~27,000 USD/yr |

| Denmark unemployment | ~3.8% |

What is included in the product

Tailored exclusively for Sydbank, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and disruptive forces that shape pricing, profitability and market entry risks—ideal for strategic planning and investor materials.

A concise one-sheet Porter's Five Forces for Sydbank that visualizes competitive pressure with a radar chart and customizable force levels—ready to drop into decks, adapt for regulatory shifts, or integrate into broader Excel dashboards without macros.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors now compare deposit and mortgage rates instantly via aggregators, forcing Sydbank to react quickly as market rates rose through 2024 and buyer betas climbed, increasing demanded yields. Sydbank must balance retention pricing against net interest margin protection by using targeted loyalty programs and bundled services to reduce pure price-driven churn.

Corporate clients’ negotiating clout

Corporate clients, especially mid-cap and larger firms, routinely run multibank RFPs that compress fees and lending margins, often using FX and cash-management services to negotiate tighter credit spreads; Sydbank mitigates this by leveraging deep product suites and relationship banking, while cross-border requirements in Northern Germany increase clients’ switching options in 2024.

Low switching frictions digitally

Low switching frictions mean account opening and payment portability sharply reduce retail client lock-in; in 2024 about 85% of Danish retail customers used digital banking channels. Open Banking and PSD2 boost price transparency and product comparison, enabling buyers to cherry-pick best-in-class offers. Differentiated UX and advisory services can restore stickiness by delivering personalized, hard-to-replicate value.

Wealth and insurance customers

Wealth and insurance customers increasingly benchmark performance and fees; by 2024 passive ETFs made up roughly half of US fund assets and robo-advisor AUM surpassed about 1.6 trillion USD, anchoring pricing downward.

Sydbank must justify active alpha and holistic planning to retain clients; bundling banking, wealth, and insurance raises perceived value and stickiness.

- Benchmarking: fees vs returns

- Passive pressure: ETFs ~50%

- Robo AUM: ~1.6T USD

- Value: bundled propositions

SME segment expectations

SME customers demand integrated banking-POS-accounting solutions at competitive prices and will shift to fintech bundles if service or integration lags; fintechs captured significant SME wallet share in 2024, intensifying price sensitivity. Relationship managers and fast credit decisions at Sydbank help retain clients and counter price pressure. Data-driven underwriting (faster decisions, better pricing) improves offer quality and retention.

- Integrated services demanded

- Fintech bundle threat (2024: higher SME fintech uptake)

- RM + quick credit = retention

- Data underwriting boosts speed/price

Customers wield pricing power — 85% digital, ~50% passive ETFs, 1.6T USD robo AUM

Customers exert strong bargaining power: 85% of Danish retail clients used digital banking in 2024, boosting price transparency; passive ETFs held ~50% of US fund assets and robo-advisors reached ~1.6T USD AUM in 2024, compressing wealth fees; SMEs shifted toward fintech bundles, increasing price sensitivity and multibank RFPs.

| Metric | 2024 |

|---|---|

| Danish retail digital use | 85% |

| Passive ETFs share (US) | ~50% |

| Robo-advisor AUM | ~1.6T USD |

| SME fintech uptake | notable increase |

What You See Is What You Get

Sydbank Porter's Five Forces Analysis

This preview shows the exact Sydbank Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or edits. The document displayed is the final, fully formatted file, ready for download and use the moment you buy. Instant access is granted upon payment, with the same professional deliverable shown here.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sydbank’s competitive landscape is shaped by concentrated buyer power, regulatory pressures, and a moderate threat from digital disruptors. Supplier influence is limited but compliance costs compress margins. Regional rivalry and price competition intensify strategic trade-offs. This snapshot scratches the surface—unlock the full Porter's Five Forces for detailed force ratings and actionable strategy.

Suppliers Bargaining Power

Dependence on core IT vendors

Dependence on core banking platforms, cloud providers and cybersecurity firms concentrates supplier power, as the top three cloud vendors hold roughly two-thirds of global market share in 2024, raising switching costs and lock-in risks for Sydbank. Complex integrations and long contracts can increase IT expenditure and reduce leverage, but multi-vendor strategies and EU/Danish outsourcing scrutiny limit worst-case outcomes. Sydbank’s scale across Denmark and Northern Germany strengthens negotiation on SLAs and pricing.

Card and payments networks

Card networks (Visa/Mastercard) and Denmark’s Dankort plus instant rails (MobilePay/real‑time transfers) are essential, giving schemes fee-setting leverage; Visa/Mastercard dominate global scheme volumes (>70%) while EU caps limit interchange to 0.2% (debit) / 0.3% (credit) under Regulation 2015/751. Interchange, scheme fees and compliance pressures materially compress Sydbank’s unit economics; some costs can be passed to merchants/customers but competitive caps and domestic rails like Dankort provide only partial counterbalance.

Wholesale funding providers

Money markets, covered-bond investors and interbank lenders set Sydbank’s funding cost and availability; 3-month EURIBOR averaged about 3.9% in 2024, and covered-bond spreads have moved +/-50–100bp in stress episodes, quickly lifting interest expense and squeezing margins. Sydbank reports diversified funding and liquidity buffers—wholesale funding concentration is limited and LCR remains well above regulatory minimums—reducing single-channel dependence, while deep Nordic/European investor ties secure better terms.

Specialist data and service partners

Specialist suppliers (credit bureaus, KYC/AML utilities, market-data vendors) wield niche power because services are regulatory must-haves; Bloomberg terminals cost about 27,000 USD/yr (2024) and model-validation/supervisory cycles often take 3–6 months, making switching cumbersome, while Nordic consortium KYC projects have cut unit fees roughly 15–20% and volume commitments unlock better pricing tiers.

- Credit bureaus: regulatory dependency

- KYC/AML: validation 3–6 months

- Market data: Bloomberg ~27,000 USD/yr (2024)

- Consortiums: ~15–20% fee dilution

- Volume: secures lower pricing tiers

Skilled labor and compliance talent

Competition for engineers, risk and AML specialists is tight in 2024, lifting wage pressure and making skilled talent a supplier-like constraint for Sydbank; Statistics Denmark reported unemployment at about 3.8% in 2024, tightening labor availability. Talent scarcity increases bargaining power of the labor market, while hybrid work and nearshoring can expand candidate pools and help dampen costs; Sydbank’s strong Danish employer brand aids attraction and retention.

- Labor tightness: 2024 unemployment ~3.8% (Statistics Denmark)

- Supplier power: higher for AML/risk/engineers due to scarcity

- Mitigants: hybrid work, nearshoring, and strong Danish employer brand

Top‑3 cloud~66%|cards>70%|funding3.9%

Supplier power is elevated: top‑3 cloud vendors ~66% share (2024), Visa/Mastercard >70% global scheme volume, EU interchange caps 0.2%/0.3%. Funding cost pressure: 3m EURIBOR ~3.9% (2024). Specialist tools costly (Bloomberg ~27,000 USD/yr) and labor tight (Denmark unemployment ~3.8%).

| Item | 2024 |

|---|---|

| Top‑3 cloud share | ~66% |

| Card networks | >70% |

| 3m EURIBOR | ~3.9% |

| Bloomberg | ~27,000 USD/yr |

| Denmark unemployment | ~3.8% |

What is included in the product

Tailored exclusively for Sydbank, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and disruptive forces that shape pricing, profitability and market entry risks—ideal for strategic planning and investor materials.

A concise one-sheet Porter's Five Forces for Sydbank that visualizes competitive pressure with a radar chart and customizable force levels—ready to drop into decks, adapt for regulatory shifts, or integrate into broader Excel dashboards without macros.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors now compare deposit and mortgage rates instantly via aggregators, forcing Sydbank to react quickly as market rates rose through 2024 and buyer betas climbed, increasing demanded yields. Sydbank must balance retention pricing against net interest margin protection by using targeted loyalty programs and bundled services to reduce pure price-driven churn.

Corporate clients’ negotiating clout

Corporate clients, especially mid-cap and larger firms, routinely run multibank RFPs that compress fees and lending margins, often using FX and cash-management services to negotiate tighter credit spreads; Sydbank mitigates this by leveraging deep product suites and relationship banking, while cross-border requirements in Northern Germany increase clients’ switching options in 2024.

Low switching frictions digitally

Low switching frictions mean account opening and payment portability sharply reduce retail client lock-in; in 2024 about 85% of Danish retail customers used digital banking channels. Open Banking and PSD2 boost price transparency and product comparison, enabling buyers to cherry-pick best-in-class offers. Differentiated UX and advisory services can restore stickiness by delivering personalized, hard-to-replicate value.

Wealth and insurance customers

Wealth and insurance customers increasingly benchmark performance and fees; by 2024 passive ETFs made up roughly half of US fund assets and robo-advisor AUM surpassed about 1.6 trillion USD, anchoring pricing downward.

Sydbank must justify active alpha and holistic planning to retain clients; bundling banking, wealth, and insurance raises perceived value and stickiness.

- Benchmarking: fees vs returns

- Passive pressure: ETFs ~50%

- Robo AUM: ~1.6T USD

- Value: bundled propositions

SME segment expectations

SME customers demand integrated banking-POS-accounting solutions at competitive prices and will shift to fintech bundles if service or integration lags; fintechs captured significant SME wallet share in 2024, intensifying price sensitivity. Relationship managers and fast credit decisions at Sydbank help retain clients and counter price pressure. Data-driven underwriting (faster decisions, better pricing) improves offer quality and retention.

- Integrated services demanded

- Fintech bundle threat (2024: higher SME fintech uptake)

- RM + quick credit = retention

- Data underwriting boosts speed/price

Customers wield pricing power — 85% digital, ~50% passive ETFs, 1.6T USD robo AUM

Customers exert strong bargaining power: 85% of Danish retail clients used digital banking in 2024, boosting price transparency; passive ETFs held ~50% of US fund assets and robo-advisors reached ~1.6T USD AUM in 2024, compressing wealth fees; SMEs shifted toward fintech bundles, increasing price sensitivity and multibank RFPs.

| Metric | 2024 |

|---|---|

| Danish retail digital use | 85% |

| Passive ETFs share (US) | ~50% |

| Robo-advisor AUM | ~1.6T USD |

| SME fintech uptake | notable increase |

What You See Is What You Get

Sydbank Porter's Five Forces Analysis

This preview shows the exact Sydbank Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or edits. The document displayed is the final, fully formatted file, ready for download and use the moment you buy. Instant access is granted upon payment, with the same professional deliverable shown here.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sydbank’s competitive landscape is shaped by concentrated buyer power, regulatory pressures, and a moderate threat from digital disruptors. Supplier influence is limited but compliance costs compress margins. Regional rivalry and price competition intensify strategic trade-offs. This snapshot scratches the surface—unlock the full Porter's Five Forces for detailed force ratings and actionable strategy.

Suppliers Bargaining Power

Dependence on core IT vendors

Dependence on core banking platforms, cloud providers and cybersecurity firms concentrates supplier power, as the top three cloud vendors hold roughly two-thirds of global market share in 2024, raising switching costs and lock-in risks for Sydbank. Complex integrations and long contracts can increase IT expenditure and reduce leverage, but multi-vendor strategies and EU/Danish outsourcing scrutiny limit worst-case outcomes. Sydbank’s scale across Denmark and Northern Germany strengthens negotiation on SLAs and pricing.

Card and payments networks

Card networks (Visa/Mastercard) and Denmark’s Dankort plus instant rails (MobilePay/real‑time transfers) are essential, giving schemes fee-setting leverage; Visa/Mastercard dominate global scheme volumes (>70%) while EU caps limit interchange to 0.2% (debit) / 0.3% (credit) under Regulation 2015/751. Interchange, scheme fees and compliance pressures materially compress Sydbank’s unit economics; some costs can be passed to merchants/customers but competitive caps and domestic rails like Dankort provide only partial counterbalance.

Wholesale funding providers

Money markets, covered-bond investors and interbank lenders set Sydbank’s funding cost and availability; 3-month EURIBOR averaged about 3.9% in 2024, and covered-bond spreads have moved +/-50–100bp in stress episodes, quickly lifting interest expense and squeezing margins. Sydbank reports diversified funding and liquidity buffers—wholesale funding concentration is limited and LCR remains well above regulatory minimums—reducing single-channel dependence, while deep Nordic/European investor ties secure better terms.

Specialist data and service partners

Specialist suppliers (credit bureaus, KYC/AML utilities, market-data vendors) wield niche power because services are regulatory must-haves; Bloomberg terminals cost about 27,000 USD/yr (2024) and model-validation/supervisory cycles often take 3–6 months, making switching cumbersome, while Nordic consortium KYC projects have cut unit fees roughly 15–20% and volume commitments unlock better pricing tiers.

- Credit bureaus: regulatory dependency

- KYC/AML: validation 3–6 months

- Market data: Bloomberg ~27,000 USD/yr (2024)

- Consortiums: ~15–20% fee dilution

- Volume: secures lower pricing tiers

Skilled labor and compliance talent

Competition for engineers, risk and AML specialists is tight in 2024, lifting wage pressure and making skilled talent a supplier-like constraint for Sydbank; Statistics Denmark reported unemployment at about 3.8% in 2024, tightening labor availability. Talent scarcity increases bargaining power of the labor market, while hybrid work and nearshoring can expand candidate pools and help dampen costs; Sydbank’s strong Danish employer brand aids attraction and retention.

- Labor tightness: 2024 unemployment ~3.8% (Statistics Denmark)

- Supplier power: higher for AML/risk/engineers due to scarcity

- Mitigants: hybrid work, nearshoring, and strong Danish employer brand

Top‑3 cloud~66%|cards>70%|funding3.9%

Supplier power is elevated: top‑3 cloud vendors ~66% share (2024), Visa/Mastercard >70% global scheme volume, EU interchange caps 0.2%/0.3%. Funding cost pressure: 3m EURIBOR ~3.9% (2024). Specialist tools costly (Bloomberg ~27,000 USD/yr) and labor tight (Denmark unemployment ~3.8%).

| Item | 2024 |

|---|---|

| Top‑3 cloud share | ~66% |

| Card networks | >70% |

| 3m EURIBOR | ~3.9% |

| Bloomberg | ~27,000 USD/yr |

| Denmark unemployment | ~3.8% |

What is included in the product

Tailored exclusively for Sydbank, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and disruptive forces that shape pricing, profitability and market entry risks—ideal for strategic planning and investor materials.

A concise one-sheet Porter's Five Forces for Sydbank that visualizes competitive pressure with a radar chart and customizable force levels—ready to drop into decks, adapt for regulatory shifts, or integrate into broader Excel dashboards without macros.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors now compare deposit and mortgage rates instantly via aggregators, forcing Sydbank to react quickly as market rates rose through 2024 and buyer betas climbed, increasing demanded yields. Sydbank must balance retention pricing against net interest margin protection by using targeted loyalty programs and bundled services to reduce pure price-driven churn.

Corporate clients’ negotiating clout

Corporate clients, especially mid-cap and larger firms, routinely run multibank RFPs that compress fees and lending margins, often using FX and cash-management services to negotiate tighter credit spreads; Sydbank mitigates this by leveraging deep product suites and relationship banking, while cross-border requirements in Northern Germany increase clients’ switching options in 2024.

Low switching frictions digitally

Low switching frictions mean account opening and payment portability sharply reduce retail client lock-in; in 2024 about 85% of Danish retail customers used digital banking channels. Open Banking and PSD2 boost price transparency and product comparison, enabling buyers to cherry-pick best-in-class offers. Differentiated UX and advisory services can restore stickiness by delivering personalized, hard-to-replicate value.

Wealth and insurance customers

Wealth and insurance customers increasingly benchmark performance and fees; by 2024 passive ETFs made up roughly half of US fund assets and robo-advisor AUM surpassed about 1.6 trillion USD, anchoring pricing downward.

Sydbank must justify active alpha and holistic planning to retain clients; bundling banking, wealth, and insurance raises perceived value and stickiness.

- Benchmarking: fees vs returns

- Passive pressure: ETFs ~50%

- Robo AUM: ~1.6T USD

- Value: bundled propositions

SME segment expectations

SME customers demand integrated banking-POS-accounting solutions at competitive prices and will shift to fintech bundles if service or integration lags; fintechs captured significant SME wallet share in 2024, intensifying price sensitivity. Relationship managers and fast credit decisions at Sydbank help retain clients and counter price pressure. Data-driven underwriting (faster decisions, better pricing) improves offer quality and retention.

- Integrated services demanded

- Fintech bundle threat (2024: higher SME fintech uptake)

- RM + quick credit = retention

- Data underwriting boosts speed/price

Customers wield pricing power — 85% digital, ~50% passive ETFs, 1.6T USD robo AUM

Customers exert strong bargaining power: 85% of Danish retail clients used digital banking in 2024, boosting price transparency; passive ETFs held ~50% of US fund assets and robo-advisors reached ~1.6T USD AUM in 2024, compressing wealth fees; SMEs shifted toward fintech bundles, increasing price sensitivity and multibank RFPs.

| Metric | 2024 |

|---|---|

| Danish retail digital use | 85% |

| Passive ETFs share (US) | ~50% |

| Robo-advisor AUM | ~1.6T USD |

| SME fintech uptake | notable increase |

What You See Is What You Get

Sydbank Porter's Five Forces Analysis

This preview shows the exact Sydbank Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or edits. The document displayed is the final, fully formatted file, ready for download and use the moment you buy. Instant access is granted upon payment, with the same professional deliverable shown here.