Synchrony Financial PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political, economic, social, technological, legal, and environmental forces are shaping Synchrony Financial’s strategic outlook in our concise PESTLE analysis. Packed with actionable insights for investors and strategists, it reveals risks and growth levers you can use today. Purchase the full report to access the complete, ready-to-use breakdown.

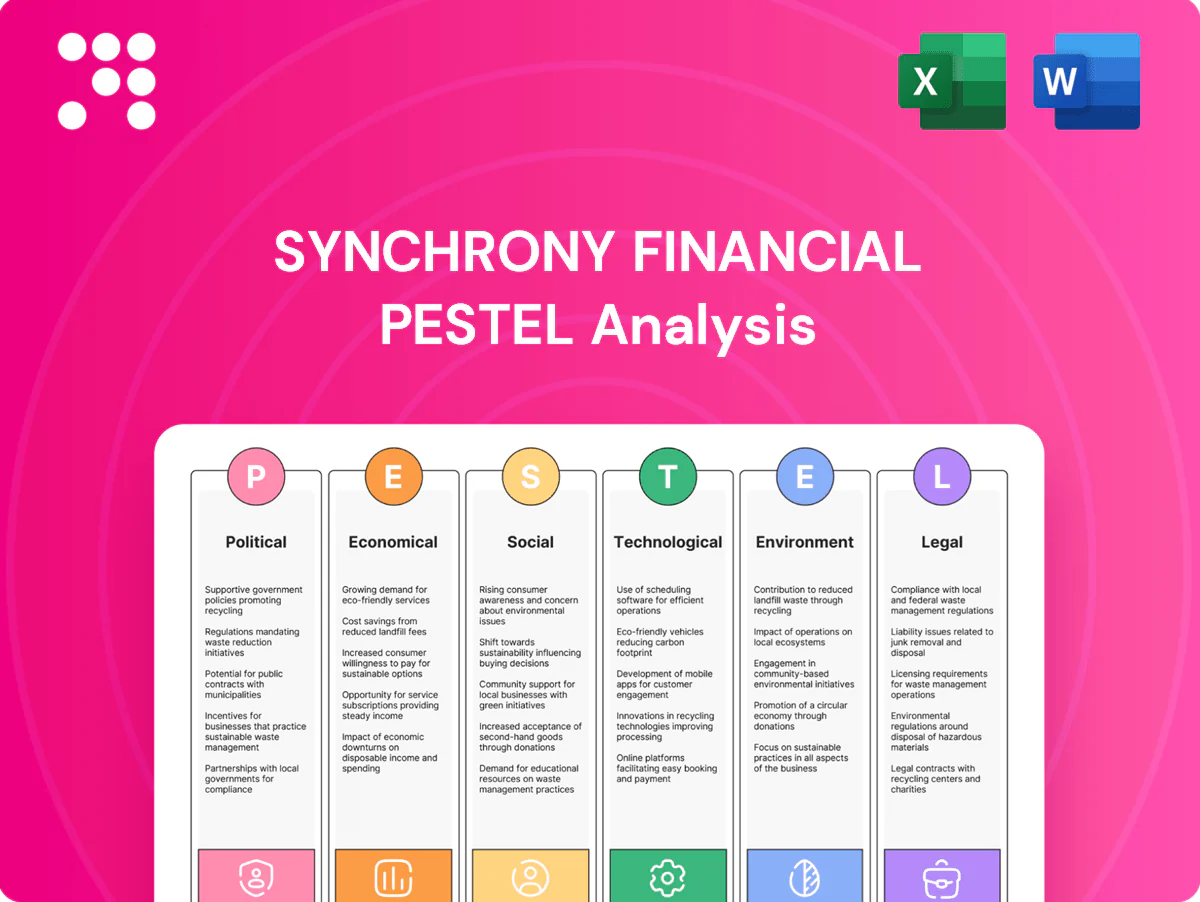

Political factors

Regulatory posture

Shifts in U.S. administration priorities can tighten or loosen consumer finance oversight; an activist stance empowers agencies like the CFPB to increase examinations and enforcement, affecting credit practices, fees and collections strategies. With the fed funds target near 5.25–5.50% in mid‑2025, Synchrony must align policies and capital planning to evolving supervisory expectations.

CFPB agenda

CFPB rulemaking shifts since 2021, intensified in 2024 under Director Rohit Chopra, affect credit card terms, late fees and dispute-resolution policies, forcing issuers like Synchrony to adjust pricing and disclosures. Guidance and proposed actions on junk fees and add-on products threaten fee revenue streams and interchange-related income. Heightened fair lending scrutiny alters allowable underwriting model inputs and increases review frequency. Proactive compliance investment reduces enforcement and remediation risk.

State actions

State attorneys general and regulators impose divergent rules on rates, fees and collections across all 50 states, complicating Synchrony’s nationwide servicing of roughly $58 billion in receivables (2024). Patchwork rules increase compliance complexity and monitoring costs; varying data privacy and servicing standards add operational friction. A harmonized federal framework or preemption would materially shift compliance costs and capital allocation.

Election cycles

Elections (presidential every 4 years, midterms every 2 years) reshape leadership at financial agencies and committee chairs, driving swings in interchange fee debates, BNPL oversight, and credit-access initiatives. Policy and budget shifts determine enforcement capacity; scenario planning stabilizes Synchrony strategy through 2024–25 policy volatility.

- 2024/25: election-driven agency turnover

- Focus: interchange, BNPL, credit access

- Mitigation: scenario planning for enforcement/budget shifts

Geopolitics & trade

Geopolitical tensions and tariffs disrupt retail supply chains and can compress partner sales volumes, which in turn slows Synchrony’s receivables growth and raises credit risk; currency swings and import cost shifts also alter partner promotional intensity and consumer demand, pressuring financing needs, so Synchrony must diversify partner exposure across categories and regions to stabilize originations.

- Supply-chain risk: reduces partner sales

- Lower merchant activity: slows receivables growth

- Currency/imports: change promotions, demand

- Strategy: diversify partners by category/region

CFPB crackdown raises compliance costs on $58bn receivables

U.S. regulatory activism under CFPB Director Rohit Chopra since 2021 intensified in 2024 forcing Synchrony to revise pricing, disclosures and collections; federal rule proposals target junk fees and BNPL. State patchwork compliance across 50 states raises monitoring costs against $58bn receivables (2024). Election cycles through 2025 increase supervisory uncertainty and enforcement funding risk.

| Metric | 2024/25 |

|---|---|

| Receivables | $58bn (2024) |

| Fed funds target | 5.25–5.50% (mid‑2025) |

What is included in the product

Explores how macro-environmental forces uniquely affect Synchrony Financial across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities; designed for executives, advisors, and investors and formatted for direct insertion into plans, decks, or reports.

The Synchrony Financial PESTLE Analysis delivers a concise, visually segmented summary that’s easily dropped into presentations or shared across teams, helping stakeholders quickly assess external risks and market positioning; users can annotate or localize insights for their specific region or business line.

Economic factors

Interest rates

Interest rate levels directly drive Synchrony Financials net interest margin and consumer APRs, with the federal funds target near 5.25%-5.50% in mid-2025 increasing yield on receivables while raising funding costs. Higher funding costs can compress spreads if liabilities cannot be fully repriced, pressuring margin-sensitive credit portfolios. Rate volatility also alters securitization economics and investor demand for ABS, affecting capital costs. Robust asset-liability management is therefore critical to protect margins.

Credit cycle

U.S. unemployment held near 3.7% in 2024, and wage growth moderation has begun to pressure consumer payment performance, lifting card delinquencies and charge-offs across the industry. Synchrony saw provisioning and ACL builds accelerate in 2024, with provisions rising into the high hundreds of millions to protect against higher loss content. Tight labor markets still support current performance, but underwriting must adjust quickly as macro outlooks flip to avoid sharp reserve shortfalls.

Consumer spending

Retail sales, which exceeded $7.5 trillion annualized in 2024, and rising healthcare out-of-pocket costs (US patient OOP roughly $430B in 2023) drive Synchrony loan growth as consumers lean on promotional financing. Uptake of promotional offers and BNPL rose amid constrained budgets, lifting receivables and average ticket sizes for durables versus smaller discretionary buys. Category mix shifts change revolve behavior; balanced partner portfolios across retail, healthcare and travel help smooth cycles.

Inflation pressure

Inflation erodes consumer purchasing power and repayment capacity, with US annual CPI averaging 3.4% in 2024; sustained above-target inflation and Fed funds near 5.25-5.50% into 2025 raise delinquencies risk and funding costs for Synchrony. Rising input and marketing costs lift operating expenses, compressing margins. Promotional APR economics may shift as funding and loss assumptions increase, so careful pricing and credit-line management mitigate pressure.

- US CPI 2024: 3.4%

- Fed funds 2024–25: ~5.25–5.50%

- Mitigants: dynamic pricing, tighter credit-line adjustments

Capital markets

Capital markets for Synchrony depend on securitization and deposit funding to manage liquidity and cost of funds; with the federal funds target at 5.25–5.50% in 2024–25, funding costs remain elevated. Spreads in risk-off periods can widen materially, constraining originations and balance-sheet growth. Ratings outlooks directly affect ABS and unsecured access, so maintaining strong credit metrics preserves funding flexibility.

- Funding mix: securitization + deposits

- Fed funds: 5.25–5.50% (2024–25)

- Risk-off: wider spreads limit growth

- Strong credit = preserved access

CFPB crackdown raises compliance costs on $58bn receivables

Higher rates (Fed funds ~5.25–5.50% mid-2025) lift yield on receivables but raise funding costs, compressing NIM if liabilities lag. CPI 2024: 3.4% and unemployment ~3.7% pressure repayment capacity, boosting delinquencies and provisions. Strong retail ($7.5T+ 2024) and healthcare OOP ~$430B (2023) support loan growth via promotional financing, while ABS/deposit funding and ratings drive access.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| CPI 2024 | 3.4% |

| Unemployment 2024 | 3.7% |

| Retail sales 2024 | $7.5T+ |

| Healthcare OOP 2023 | $430B |

What You See Is What You Get

Synchrony Financial PESTLE Analysis

The Synchrony Financial PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers: the content, layout, and structure visible now are what you’ll download immediately after checkout. This is the real, finished file you’ll own upon payment.

Your Shortcut to Market Insight Starts Here

Discover how political, economic, social, technological, legal, and environmental forces are shaping Synchrony Financial’s strategic outlook in our concise PESTLE analysis. Packed with actionable insights for investors and strategists, it reveals risks and growth levers you can use today. Purchase the full report to access the complete, ready-to-use breakdown.

Political factors

Regulatory posture

Shifts in U.S. administration priorities can tighten or loosen consumer finance oversight; an activist stance empowers agencies like the CFPB to increase examinations and enforcement, affecting credit practices, fees and collections strategies. With the fed funds target near 5.25–5.50% in mid‑2025, Synchrony must align policies and capital planning to evolving supervisory expectations.

CFPB agenda

CFPB rulemaking shifts since 2021, intensified in 2024 under Director Rohit Chopra, affect credit card terms, late fees and dispute-resolution policies, forcing issuers like Synchrony to adjust pricing and disclosures. Guidance and proposed actions on junk fees and add-on products threaten fee revenue streams and interchange-related income. Heightened fair lending scrutiny alters allowable underwriting model inputs and increases review frequency. Proactive compliance investment reduces enforcement and remediation risk.

State actions

State attorneys general and regulators impose divergent rules on rates, fees and collections across all 50 states, complicating Synchrony’s nationwide servicing of roughly $58 billion in receivables (2024). Patchwork rules increase compliance complexity and monitoring costs; varying data privacy and servicing standards add operational friction. A harmonized federal framework or preemption would materially shift compliance costs and capital allocation.

Election cycles

Elections (presidential every 4 years, midterms every 2 years) reshape leadership at financial agencies and committee chairs, driving swings in interchange fee debates, BNPL oversight, and credit-access initiatives. Policy and budget shifts determine enforcement capacity; scenario planning stabilizes Synchrony strategy through 2024–25 policy volatility.

- 2024/25: election-driven agency turnover

- Focus: interchange, BNPL, credit access

- Mitigation: scenario planning for enforcement/budget shifts

Geopolitics & trade

Geopolitical tensions and tariffs disrupt retail supply chains and can compress partner sales volumes, which in turn slows Synchrony’s receivables growth and raises credit risk; currency swings and import cost shifts also alter partner promotional intensity and consumer demand, pressuring financing needs, so Synchrony must diversify partner exposure across categories and regions to stabilize originations.

- Supply-chain risk: reduces partner sales

- Lower merchant activity: slows receivables growth

- Currency/imports: change promotions, demand

- Strategy: diversify partners by category/region

CFPB crackdown raises compliance costs on $58bn receivables

U.S. regulatory activism under CFPB Director Rohit Chopra since 2021 intensified in 2024 forcing Synchrony to revise pricing, disclosures and collections; federal rule proposals target junk fees and BNPL. State patchwork compliance across 50 states raises monitoring costs against $58bn receivables (2024). Election cycles through 2025 increase supervisory uncertainty and enforcement funding risk.

| Metric | 2024/25 |

|---|---|

| Receivables | $58bn (2024) |

| Fed funds target | 5.25–5.50% (mid‑2025) |

What is included in the product

Explores how macro-environmental forces uniquely affect Synchrony Financial across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities; designed for executives, advisors, and investors and formatted for direct insertion into plans, decks, or reports.

The Synchrony Financial PESTLE Analysis delivers a concise, visually segmented summary that’s easily dropped into presentations or shared across teams, helping stakeholders quickly assess external risks and market positioning; users can annotate or localize insights for their specific region or business line.

Economic factors

Interest rates

Interest rate levels directly drive Synchrony Financials net interest margin and consumer APRs, with the federal funds target near 5.25%-5.50% in mid-2025 increasing yield on receivables while raising funding costs. Higher funding costs can compress spreads if liabilities cannot be fully repriced, pressuring margin-sensitive credit portfolios. Rate volatility also alters securitization economics and investor demand for ABS, affecting capital costs. Robust asset-liability management is therefore critical to protect margins.

Credit cycle

U.S. unemployment held near 3.7% in 2024, and wage growth moderation has begun to pressure consumer payment performance, lifting card delinquencies and charge-offs across the industry. Synchrony saw provisioning and ACL builds accelerate in 2024, with provisions rising into the high hundreds of millions to protect against higher loss content. Tight labor markets still support current performance, but underwriting must adjust quickly as macro outlooks flip to avoid sharp reserve shortfalls.

Consumer spending

Retail sales, which exceeded $7.5 trillion annualized in 2024, and rising healthcare out-of-pocket costs (US patient OOP roughly $430B in 2023) drive Synchrony loan growth as consumers lean on promotional financing. Uptake of promotional offers and BNPL rose amid constrained budgets, lifting receivables and average ticket sizes for durables versus smaller discretionary buys. Category mix shifts change revolve behavior; balanced partner portfolios across retail, healthcare and travel help smooth cycles.

Inflation pressure

Inflation erodes consumer purchasing power and repayment capacity, with US annual CPI averaging 3.4% in 2024; sustained above-target inflation and Fed funds near 5.25-5.50% into 2025 raise delinquencies risk and funding costs for Synchrony. Rising input and marketing costs lift operating expenses, compressing margins. Promotional APR economics may shift as funding and loss assumptions increase, so careful pricing and credit-line management mitigate pressure.

- US CPI 2024: 3.4%

- Fed funds 2024–25: ~5.25–5.50%

- Mitigants: dynamic pricing, tighter credit-line adjustments

Capital markets

Capital markets for Synchrony depend on securitization and deposit funding to manage liquidity and cost of funds; with the federal funds target at 5.25–5.50% in 2024–25, funding costs remain elevated. Spreads in risk-off periods can widen materially, constraining originations and balance-sheet growth. Ratings outlooks directly affect ABS and unsecured access, so maintaining strong credit metrics preserves funding flexibility.

- Funding mix: securitization + deposits

- Fed funds: 5.25–5.50% (2024–25)

- Risk-off: wider spreads limit growth

- Strong credit = preserved access

CFPB crackdown raises compliance costs on $58bn receivables

Higher rates (Fed funds ~5.25–5.50% mid-2025) lift yield on receivables but raise funding costs, compressing NIM if liabilities lag. CPI 2024: 3.4% and unemployment ~3.7% pressure repayment capacity, boosting delinquencies and provisions. Strong retail ($7.5T+ 2024) and healthcare OOP ~$430B (2023) support loan growth via promotional financing, while ABS/deposit funding and ratings drive access.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| CPI 2024 | 3.4% |

| Unemployment 2024 | 3.7% |

| Retail sales 2024 | $7.5T+ |

| Healthcare OOP 2023 | $430B |

What You See Is What You Get

Synchrony Financial PESTLE Analysis

The Synchrony Financial PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers: the content, layout, and structure visible now are what you’ll download immediately after checkout. This is the real, finished file you’ll own upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Discover how political, economic, social, technological, legal, and environmental forces are shaping Synchrony Financial’s strategic outlook in our concise PESTLE analysis. Packed with actionable insights for investors and strategists, it reveals risks and growth levers you can use today. Purchase the full report to access the complete, ready-to-use breakdown.

Political factors

Regulatory posture

Shifts in U.S. administration priorities can tighten or loosen consumer finance oversight; an activist stance empowers agencies like the CFPB to increase examinations and enforcement, affecting credit practices, fees and collections strategies. With the fed funds target near 5.25–5.50% in mid‑2025, Synchrony must align policies and capital planning to evolving supervisory expectations.

CFPB agenda

CFPB rulemaking shifts since 2021, intensified in 2024 under Director Rohit Chopra, affect credit card terms, late fees and dispute-resolution policies, forcing issuers like Synchrony to adjust pricing and disclosures. Guidance and proposed actions on junk fees and add-on products threaten fee revenue streams and interchange-related income. Heightened fair lending scrutiny alters allowable underwriting model inputs and increases review frequency. Proactive compliance investment reduces enforcement and remediation risk.

State actions

State attorneys general and regulators impose divergent rules on rates, fees and collections across all 50 states, complicating Synchrony’s nationwide servicing of roughly $58 billion in receivables (2024). Patchwork rules increase compliance complexity and monitoring costs; varying data privacy and servicing standards add operational friction. A harmonized federal framework or preemption would materially shift compliance costs and capital allocation.

Election cycles

Elections (presidential every 4 years, midterms every 2 years) reshape leadership at financial agencies and committee chairs, driving swings in interchange fee debates, BNPL oversight, and credit-access initiatives. Policy and budget shifts determine enforcement capacity; scenario planning stabilizes Synchrony strategy through 2024–25 policy volatility.

- 2024/25: election-driven agency turnover

- Focus: interchange, BNPL, credit access

- Mitigation: scenario planning for enforcement/budget shifts

Geopolitics & trade

Geopolitical tensions and tariffs disrupt retail supply chains and can compress partner sales volumes, which in turn slows Synchrony’s receivables growth and raises credit risk; currency swings and import cost shifts also alter partner promotional intensity and consumer demand, pressuring financing needs, so Synchrony must diversify partner exposure across categories and regions to stabilize originations.

- Supply-chain risk: reduces partner sales

- Lower merchant activity: slows receivables growth

- Currency/imports: change promotions, demand

- Strategy: diversify partners by category/region

CFPB crackdown raises compliance costs on $58bn receivables

U.S. regulatory activism under CFPB Director Rohit Chopra since 2021 intensified in 2024 forcing Synchrony to revise pricing, disclosures and collections; federal rule proposals target junk fees and BNPL. State patchwork compliance across 50 states raises monitoring costs against $58bn receivables (2024). Election cycles through 2025 increase supervisory uncertainty and enforcement funding risk.

| Metric | 2024/25 |

|---|---|

| Receivables | $58bn (2024) |

| Fed funds target | 5.25–5.50% (mid‑2025) |

What is included in the product

Explores how macro-environmental forces uniquely affect Synchrony Financial across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities; designed for executives, advisors, and investors and formatted for direct insertion into plans, decks, or reports.

The Synchrony Financial PESTLE Analysis delivers a concise, visually segmented summary that’s easily dropped into presentations or shared across teams, helping stakeholders quickly assess external risks and market positioning; users can annotate or localize insights for their specific region or business line.

Economic factors

Interest rates

Interest rate levels directly drive Synchrony Financials net interest margin and consumer APRs, with the federal funds target near 5.25%-5.50% in mid-2025 increasing yield on receivables while raising funding costs. Higher funding costs can compress spreads if liabilities cannot be fully repriced, pressuring margin-sensitive credit portfolios. Rate volatility also alters securitization economics and investor demand for ABS, affecting capital costs. Robust asset-liability management is therefore critical to protect margins.

Credit cycle

U.S. unemployment held near 3.7% in 2024, and wage growth moderation has begun to pressure consumer payment performance, lifting card delinquencies and charge-offs across the industry. Synchrony saw provisioning and ACL builds accelerate in 2024, with provisions rising into the high hundreds of millions to protect against higher loss content. Tight labor markets still support current performance, but underwriting must adjust quickly as macro outlooks flip to avoid sharp reserve shortfalls.

Consumer spending

Retail sales, which exceeded $7.5 trillion annualized in 2024, and rising healthcare out-of-pocket costs (US patient OOP roughly $430B in 2023) drive Synchrony loan growth as consumers lean on promotional financing. Uptake of promotional offers and BNPL rose amid constrained budgets, lifting receivables and average ticket sizes for durables versus smaller discretionary buys. Category mix shifts change revolve behavior; balanced partner portfolios across retail, healthcare and travel help smooth cycles.

Inflation pressure

Inflation erodes consumer purchasing power and repayment capacity, with US annual CPI averaging 3.4% in 2024; sustained above-target inflation and Fed funds near 5.25-5.50% into 2025 raise delinquencies risk and funding costs for Synchrony. Rising input and marketing costs lift operating expenses, compressing margins. Promotional APR economics may shift as funding and loss assumptions increase, so careful pricing and credit-line management mitigate pressure.

- US CPI 2024: 3.4%

- Fed funds 2024–25: ~5.25–5.50%

- Mitigants: dynamic pricing, tighter credit-line adjustments

Capital markets

Capital markets for Synchrony depend on securitization and deposit funding to manage liquidity and cost of funds; with the federal funds target at 5.25–5.50% in 2024–25, funding costs remain elevated. Spreads in risk-off periods can widen materially, constraining originations and balance-sheet growth. Ratings outlooks directly affect ABS and unsecured access, so maintaining strong credit metrics preserves funding flexibility.

- Funding mix: securitization + deposits

- Fed funds: 5.25–5.50% (2024–25)

- Risk-off: wider spreads limit growth

- Strong credit = preserved access

CFPB crackdown raises compliance costs on $58bn receivables

Higher rates (Fed funds ~5.25–5.50% mid-2025) lift yield on receivables but raise funding costs, compressing NIM if liabilities lag. CPI 2024: 3.4% and unemployment ~3.7% pressure repayment capacity, boosting delinquencies and provisions. Strong retail ($7.5T+ 2024) and healthcare OOP ~$430B (2023) support loan growth via promotional financing, while ABS/deposit funding and ratings drive access.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| CPI 2024 | 3.4% |

| Unemployment 2024 | 3.7% |

| Retail sales 2024 | $7.5T+ |

| Healthcare OOP 2023 | $430B |

What You See Is What You Get

Synchrony Financial PESTLE Analysis

The Synchrony Financial PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers: the content, layout, and structure visible now are what you’ll download immediately after checkout. This is the real, finished file you’ll own upon payment.