Synergie Porter's Five Forces Analysis

Don't Miss the Bigger Picture

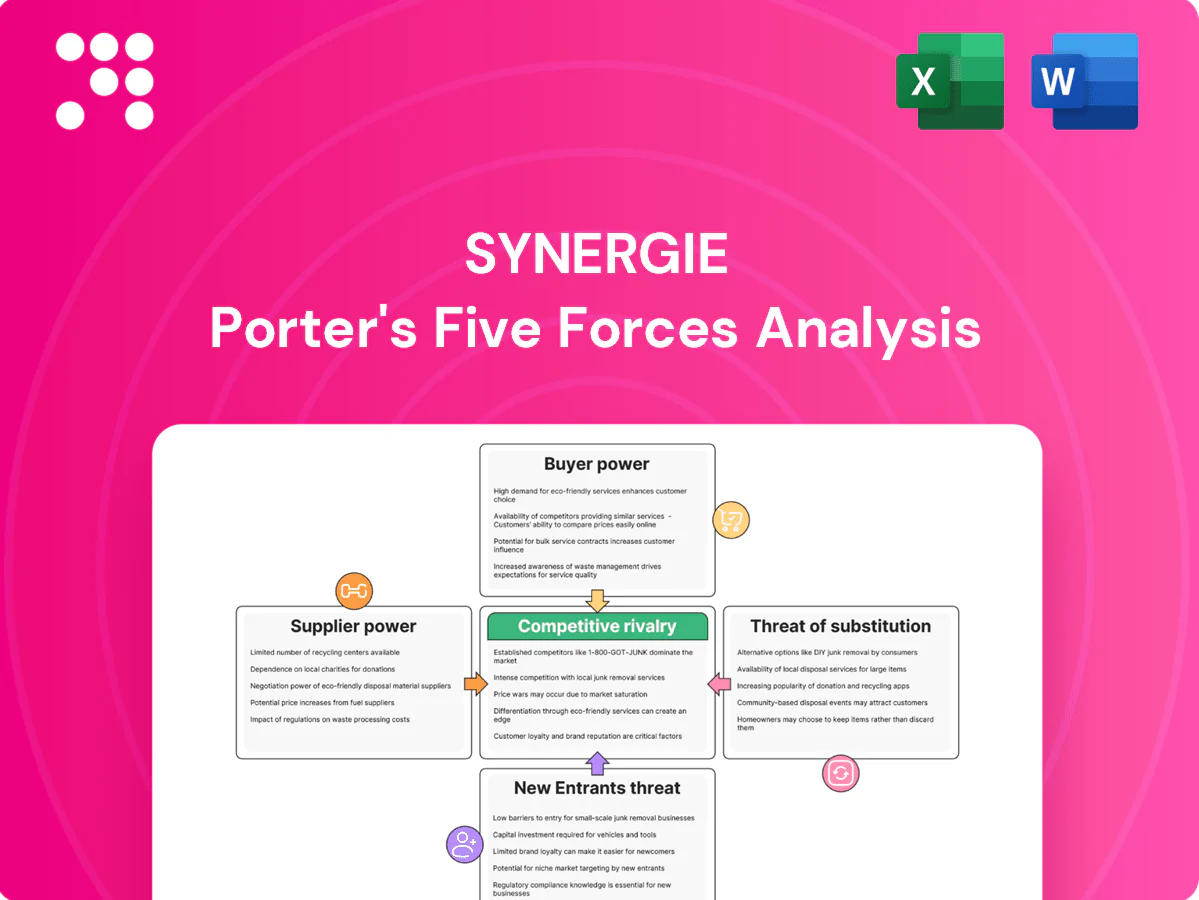

Synergie faces moderate buyer power, fragmented suppliers with niche leverage, and looming threats from digital disruptors that intensify rivalry and substitution risks; regulatory shifts also shape entry barriers and cost structures. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Synergie’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of qualified talent

In staffing, workers are the primary suppliers and scarcity of high‑demand skills increases their leverage; tight labor markets (U.S. unemployment ~3.9% in 2024, BLS) drive higher pay and faster fill expectations. Synergie must invest in proactive sourcing and upskilling to secure scarce profiles; supplier power peaks in niche sectors but falls in commoditized roles, with computer/IT occupations projected to grow ~15% 2022–32 (BLS).

Multi-channel sourcing dependence

Synergie relies on job boards, social platforms and recruiters for sourcing; LinkedIn surpassed 1 billion members by 2024, concentrating candidate flows and pricing power. Algorithm and pricing shifts on platforms can raise acquisition costs, sometimes by double-digit percentages for ad-driven campaigns. Diversifying channels and building proprietary talent pools reduces this dependency. Strong employer branding cuts paid sourcing needs and CPC/CPA spend.

Training and certification partners

External training vendors and accrediting bodies shape upskilling pipelines; 2024 industry reports value the corporate training market near $440B and show 62% of employers cite persistent skills gaps. Limited certified programs can delay candidate readiness and extend time-to-hire. Co-developing curricula and launching in-house academies reduces supplier power and can cut onboarding time up to 40%, while volume commitments often unlock 10–25% better terms.

Payroll and workforce tech vendors

ATS, VMS, payroll and compliance platforms are core infrastructure for Synergie, with 54% of enterprises in 2024 citing integration complexity as a primary barrier to switching; high implementation and data-migration costs entrench vendor power. Negotiating multi-country contracts and standardized APIs lowers lock-in and can cut total vendor spend by double-digit percentages in procurement scenarios. Open architectures and modular stacks preserve flexibility and reduce future switching friction.

Regulatory and compliance gatekeepers

Regulators and labor authorities function as non-traditional suppliers by granting licenses and permissions; the 2024 transposition of EU platform work rules has directly altered engagement models and contract compliance for staffing firms. Changes in labor law shift cost structures and can slow speed to market, while proactive compliance and audit readiness cut legal uncertainty. Participation in industry bodies helps firms influence evolving standards.

- Regulators = gatekeepers of licenses/permits

- Compliance/audits reduce time/cost volatility

- Industry bodies shape standards

Supplier power rising: scarce skills, $440B training market

Suppliers (workers, platforms, training vendors, tech providers, regulators) hold variable power: high for scarce skills and dominant platforms; 2024 signals—US unemployment ~3.9%, LinkedIn >1B, corporate training ~$440B, 54% cite integration complexity. Diversify channels, build academies, negotiate multi-country contracts and open APIs to reduce supplier leverage.

| Supplier | 2024 metric |

|---|---|

| Labor market | Unemp ~3.9% |

| Platforms | LinkedIn >1B |

| Training | $440B market |

| Tech vendors | 54% integration issue |

What is included in the product

Comprehensive Porter’s Five Forces for Synergie, uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitutes and emerging threats, with strategic commentary and editable findings for reports.

One-sheet Porter’s Five Forces from Synergie simplifies strategic pressure into a clean, customizable spider chart—ideal for quick decisions and slide-ready summaries, with no macros so non-finance teams can update scenarios and integrate results into reports or dashboards.

Customers Bargaining Power

Large enterprise clients with VMS/MSP

Enterprises using VMS/MSP centralize buying and routinely squeeze supplier margins, with Staffing Industry Analysts reporting the global MSP market exceeded $28 billion in 2024 and consolidation driving tougher pricing. They demand SLAs, rebates, and global rate cards, pressuring suppliers on compliance and scale. Synergie must compete on scale, regulatory compliance, and specialty coverage to retain contracts. Differentiation via faster delivery and niche capabilities can preserve pricing power.

Low switching costs between agencies

Clients increasingly onboard multiple agencies and can rebalance spend quickly—2024 industry surveys show over 50% of brands use two or more agency partners, heightening price sensitivity and shortening contract terms to typically 6–12 months. Real-time performance dashboards make cross-agency comparisons transparent, lowering barriers to reallocation. However, sticky value-adds and embedded teams raise switching frictions and preserve wallet share.

Demand cyclicality and budget pressures

Economic slowdowns cut requisitions and raise rate pressure; IMF projected global growth at 3.1% in 2024, tightening corporate hiring budgets. Clients increasingly demand temp-to-perm discounts and longer payment terms, squeezing margins. Synergie needs flexible, variable-cost models to defend profitability, while productivity-boosting workforce solutions can justify premium pricing.

Sector-specific compliance demands

Sector-specific compliance demands in finance, healthcare and defense force stringent screening and onboarding, with buyers leveraging regulatory risk to require tailored processes at no additional fee. As of 2024, demonstrated compliance maturity (eg ISO/IEC 27001, SOC 2) shifts negotiations from price to value. Certifications increasingly act as procurement differentiators.

- Buyers require tailored onboarding at no extra charge

- Compliance maturity redirects talks to value, not price

- ISO/IEC 27001 and SOC 2 cited as key differentiators in 2024

Preference for outcome-based models

Clients increasingly shift to RPO, SOW and output-linked pricing, moving risk to providers and compressing unit rates; the global RPO market was valued at about $5.8 billion in 2022 with a 7.4% CAGR per Grand View Research, underscoring demand for outcome models. Synergie can win by proving measurable productivity and faster time-to-fill; clear KPIs align incentives and defend fees.

- Tag: outcome-based adoption

- Tag: risk transfer

- Tag: unit-rate pressure

- Tag: KPI alignment

MSP consolidation tightens margins as brands demand outcome KPIs and shorter contracts

Enterprises centralize VMS/MSP procurement, squeezing margins; global MSP market >28 billion USD in 2024 with consolidation increasing buyer leverage. Over 50% of brands use 2+ agencies in 2024, shortening contracts to 6–12 months and raising price sensitivity. Compliance certifications (ISO/IEC 27001, SOC 2) and outcome KPIs shift talks toward value, but IMF 2024 growth 3.1% tightens hiring budgets.

| Metric | Value |

|---|---|

| Global MSP market (2024) | >28B USD |

| Brands using 2+ agencies (2024) | >50% |

| Typical contract length | 6–12 months |

| IMF global growth (2024) | 3.1% |

Preview Before You Purchase

Synergie Porter's Five Forces Analysis

This preview displays the exact Synergie Porter's Five Forces Analysis you will receive upon purchase—fully written, formatted, and ready to download. No samples or placeholders are included; the file shown is the deliverable. Buy and get instant access to this precise document for immediate use.

Don't Miss the Bigger Picture

Synergie faces moderate buyer power, fragmented suppliers with niche leverage, and looming threats from digital disruptors that intensify rivalry and substitution risks; regulatory shifts also shape entry barriers and cost structures. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Synergie’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of qualified talent

In staffing, workers are the primary suppliers and scarcity of high‑demand skills increases their leverage; tight labor markets (U.S. unemployment ~3.9% in 2024, BLS) drive higher pay and faster fill expectations. Synergie must invest in proactive sourcing and upskilling to secure scarce profiles; supplier power peaks in niche sectors but falls in commoditized roles, with computer/IT occupations projected to grow ~15% 2022–32 (BLS).

Multi-channel sourcing dependence

Synergie relies on job boards, social platforms and recruiters for sourcing; LinkedIn surpassed 1 billion members by 2024, concentrating candidate flows and pricing power. Algorithm and pricing shifts on platforms can raise acquisition costs, sometimes by double-digit percentages for ad-driven campaigns. Diversifying channels and building proprietary talent pools reduces this dependency. Strong employer branding cuts paid sourcing needs and CPC/CPA spend.

Training and certification partners

External training vendors and accrediting bodies shape upskilling pipelines; 2024 industry reports value the corporate training market near $440B and show 62% of employers cite persistent skills gaps. Limited certified programs can delay candidate readiness and extend time-to-hire. Co-developing curricula and launching in-house academies reduces supplier power and can cut onboarding time up to 40%, while volume commitments often unlock 10–25% better terms.

Payroll and workforce tech vendors

ATS, VMS, payroll and compliance platforms are core infrastructure for Synergie, with 54% of enterprises in 2024 citing integration complexity as a primary barrier to switching; high implementation and data-migration costs entrench vendor power. Negotiating multi-country contracts and standardized APIs lowers lock-in and can cut total vendor spend by double-digit percentages in procurement scenarios. Open architectures and modular stacks preserve flexibility and reduce future switching friction.

Regulatory and compliance gatekeepers

Regulators and labor authorities function as non-traditional suppliers by granting licenses and permissions; the 2024 transposition of EU platform work rules has directly altered engagement models and contract compliance for staffing firms. Changes in labor law shift cost structures and can slow speed to market, while proactive compliance and audit readiness cut legal uncertainty. Participation in industry bodies helps firms influence evolving standards.

- Regulators = gatekeepers of licenses/permits

- Compliance/audits reduce time/cost volatility

- Industry bodies shape standards

Supplier power rising: scarce skills, $440B training market

Suppliers (workers, platforms, training vendors, tech providers, regulators) hold variable power: high for scarce skills and dominant platforms; 2024 signals—US unemployment ~3.9%, LinkedIn >1B, corporate training ~$440B, 54% cite integration complexity. Diversify channels, build academies, negotiate multi-country contracts and open APIs to reduce supplier leverage.

| Supplier | 2024 metric |

|---|---|

| Labor market | Unemp ~3.9% |

| Platforms | LinkedIn >1B |

| Training | $440B market |

| Tech vendors | 54% integration issue |

What is included in the product

Comprehensive Porter’s Five Forces for Synergie, uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitutes and emerging threats, with strategic commentary and editable findings for reports.

One-sheet Porter’s Five Forces from Synergie simplifies strategic pressure into a clean, customizable spider chart—ideal for quick decisions and slide-ready summaries, with no macros so non-finance teams can update scenarios and integrate results into reports or dashboards.

Customers Bargaining Power

Large enterprise clients with VMS/MSP

Enterprises using VMS/MSP centralize buying and routinely squeeze supplier margins, with Staffing Industry Analysts reporting the global MSP market exceeded $28 billion in 2024 and consolidation driving tougher pricing. They demand SLAs, rebates, and global rate cards, pressuring suppliers on compliance and scale. Synergie must compete on scale, regulatory compliance, and specialty coverage to retain contracts. Differentiation via faster delivery and niche capabilities can preserve pricing power.

Low switching costs between agencies

Clients increasingly onboard multiple agencies and can rebalance spend quickly—2024 industry surveys show over 50% of brands use two or more agency partners, heightening price sensitivity and shortening contract terms to typically 6–12 months. Real-time performance dashboards make cross-agency comparisons transparent, lowering barriers to reallocation. However, sticky value-adds and embedded teams raise switching frictions and preserve wallet share.

Demand cyclicality and budget pressures

Economic slowdowns cut requisitions and raise rate pressure; IMF projected global growth at 3.1% in 2024, tightening corporate hiring budgets. Clients increasingly demand temp-to-perm discounts and longer payment terms, squeezing margins. Synergie needs flexible, variable-cost models to defend profitability, while productivity-boosting workforce solutions can justify premium pricing.

Sector-specific compliance demands

Sector-specific compliance demands in finance, healthcare and defense force stringent screening and onboarding, with buyers leveraging regulatory risk to require tailored processes at no additional fee. As of 2024, demonstrated compliance maturity (eg ISO/IEC 27001, SOC 2) shifts negotiations from price to value. Certifications increasingly act as procurement differentiators.

- Buyers require tailored onboarding at no extra charge

- Compliance maturity redirects talks to value, not price

- ISO/IEC 27001 and SOC 2 cited as key differentiators in 2024

Preference for outcome-based models

Clients increasingly shift to RPO, SOW and output-linked pricing, moving risk to providers and compressing unit rates; the global RPO market was valued at about $5.8 billion in 2022 with a 7.4% CAGR per Grand View Research, underscoring demand for outcome models. Synergie can win by proving measurable productivity and faster time-to-fill; clear KPIs align incentives and defend fees.

- Tag: outcome-based adoption

- Tag: risk transfer

- Tag: unit-rate pressure

- Tag: KPI alignment

MSP consolidation tightens margins as brands demand outcome KPIs and shorter contracts

Enterprises centralize VMS/MSP procurement, squeezing margins; global MSP market >28 billion USD in 2024 with consolidation increasing buyer leverage. Over 50% of brands use 2+ agencies in 2024, shortening contracts to 6–12 months and raising price sensitivity. Compliance certifications (ISO/IEC 27001, SOC 2) and outcome KPIs shift talks toward value, but IMF 2024 growth 3.1% tightens hiring budgets.

| Metric | Value |

|---|---|

| Global MSP market (2024) | >28B USD |

| Brands using 2+ agencies (2024) | >50% |

| Typical contract length | 6–12 months |

| IMF global growth (2024) | 3.1% |

Preview Before You Purchase

Synergie Porter's Five Forces Analysis

This preview displays the exact Synergie Porter's Five Forces Analysis you will receive upon purchase—fully written, formatted, and ready to download. No samples or placeholders are included; the file shown is the deliverable. Buy and get instant access to this precise document for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Synergie faces moderate buyer power, fragmented suppliers with niche leverage, and looming threats from digital disruptors that intensify rivalry and substitution risks; regulatory shifts also shape entry barriers and cost structures. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Synergie’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of qualified talent

In staffing, workers are the primary suppliers and scarcity of high‑demand skills increases their leverage; tight labor markets (U.S. unemployment ~3.9% in 2024, BLS) drive higher pay and faster fill expectations. Synergie must invest in proactive sourcing and upskilling to secure scarce profiles; supplier power peaks in niche sectors but falls in commoditized roles, with computer/IT occupations projected to grow ~15% 2022–32 (BLS).

Multi-channel sourcing dependence

Synergie relies on job boards, social platforms and recruiters for sourcing; LinkedIn surpassed 1 billion members by 2024, concentrating candidate flows and pricing power. Algorithm and pricing shifts on platforms can raise acquisition costs, sometimes by double-digit percentages for ad-driven campaigns. Diversifying channels and building proprietary talent pools reduces this dependency. Strong employer branding cuts paid sourcing needs and CPC/CPA spend.

Training and certification partners

External training vendors and accrediting bodies shape upskilling pipelines; 2024 industry reports value the corporate training market near $440B and show 62% of employers cite persistent skills gaps. Limited certified programs can delay candidate readiness and extend time-to-hire. Co-developing curricula and launching in-house academies reduces supplier power and can cut onboarding time up to 40%, while volume commitments often unlock 10–25% better terms.

Payroll and workforce tech vendors

ATS, VMS, payroll and compliance platforms are core infrastructure for Synergie, with 54% of enterprises in 2024 citing integration complexity as a primary barrier to switching; high implementation and data-migration costs entrench vendor power. Negotiating multi-country contracts and standardized APIs lowers lock-in and can cut total vendor spend by double-digit percentages in procurement scenarios. Open architectures and modular stacks preserve flexibility and reduce future switching friction.

Regulatory and compliance gatekeepers

Regulators and labor authorities function as non-traditional suppliers by granting licenses and permissions; the 2024 transposition of EU platform work rules has directly altered engagement models and contract compliance for staffing firms. Changes in labor law shift cost structures and can slow speed to market, while proactive compliance and audit readiness cut legal uncertainty. Participation in industry bodies helps firms influence evolving standards.

- Regulators = gatekeepers of licenses/permits

- Compliance/audits reduce time/cost volatility

- Industry bodies shape standards

Supplier power rising: scarce skills, $440B training market

Suppliers (workers, platforms, training vendors, tech providers, regulators) hold variable power: high for scarce skills and dominant platforms; 2024 signals—US unemployment ~3.9%, LinkedIn >1B, corporate training ~$440B, 54% cite integration complexity. Diversify channels, build academies, negotiate multi-country contracts and open APIs to reduce supplier leverage.

| Supplier | 2024 metric |

|---|---|

| Labor market | Unemp ~3.9% |

| Platforms | LinkedIn >1B |

| Training | $440B market |

| Tech vendors | 54% integration issue |

What is included in the product

Comprehensive Porter’s Five Forces for Synergie, uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitutes and emerging threats, with strategic commentary and editable findings for reports.

One-sheet Porter’s Five Forces from Synergie simplifies strategic pressure into a clean, customizable spider chart—ideal for quick decisions and slide-ready summaries, with no macros so non-finance teams can update scenarios and integrate results into reports or dashboards.

Customers Bargaining Power

Large enterprise clients with VMS/MSP

Enterprises using VMS/MSP centralize buying and routinely squeeze supplier margins, with Staffing Industry Analysts reporting the global MSP market exceeded $28 billion in 2024 and consolidation driving tougher pricing. They demand SLAs, rebates, and global rate cards, pressuring suppliers on compliance and scale. Synergie must compete on scale, regulatory compliance, and specialty coverage to retain contracts. Differentiation via faster delivery and niche capabilities can preserve pricing power.

Low switching costs between agencies

Clients increasingly onboard multiple agencies and can rebalance spend quickly—2024 industry surveys show over 50% of brands use two or more agency partners, heightening price sensitivity and shortening contract terms to typically 6–12 months. Real-time performance dashboards make cross-agency comparisons transparent, lowering barriers to reallocation. However, sticky value-adds and embedded teams raise switching frictions and preserve wallet share.

Demand cyclicality and budget pressures

Economic slowdowns cut requisitions and raise rate pressure; IMF projected global growth at 3.1% in 2024, tightening corporate hiring budgets. Clients increasingly demand temp-to-perm discounts and longer payment terms, squeezing margins. Synergie needs flexible, variable-cost models to defend profitability, while productivity-boosting workforce solutions can justify premium pricing.

Sector-specific compliance demands

Sector-specific compliance demands in finance, healthcare and defense force stringent screening and onboarding, with buyers leveraging regulatory risk to require tailored processes at no additional fee. As of 2024, demonstrated compliance maturity (eg ISO/IEC 27001, SOC 2) shifts negotiations from price to value. Certifications increasingly act as procurement differentiators.

- Buyers require tailored onboarding at no extra charge

- Compliance maturity redirects talks to value, not price

- ISO/IEC 27001 and SOC 2 cited as key differentiators in 2024

Preference for outcome-based models

Clients increasingly shift to RPO, SOW and output-linked pricing, moving risk to providers and compressing unit rates; the global RPO market was valued at about $5.8 billion in 2022 with a 7.4% CAGR per Grand View Research, underscoring demand for outcome models. Synergie can win by proving measurable productivity and faster time-to-fill; clear KPIs align incentives and defend fees.

- Tag: outcome-based adoption

- Tag: risk transfer

- Tag: unit-rate pressure

- Tag: KPI alignment

MSP consolidation tightens margins as brands demand outcome KPIs and shorter contracts

Enterprises centralize VMS/MSP procurement, squeezing margins; global MSP market >28 billion USD in 2024 with consolidation increasing buyer leverage. Over 50% of brands use 2+ agencies in 2024, shortening contracts to 6–12 months and raising price sensitivity. Compliance certifications (ISO/IEC 27001, SOC 2) and outcome KPIs shift talks toward value, but IMF 2024 growth 3.1% tightens hiring budgets.

| Metric | Value |

|---|---|

| Global MSP market (2024) | >28B USD |

| Brands using 2+ agencies (2024) | >50% |

| Typical contract length | 6–12 months |

| IMF global growth (2024) | 3.1% |

Preview Before You Purchase

Synergie Porter's Five Forces Analysis

This preview displays the exact Synergie Porter's Five Forces Analysis you will receive upon purchase—fully written, formatted, and ready to download. No samples or placeholders are included; the file shown is the deliverable. Buy and get instant access to this precise document for immediate use.