Synopsys Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

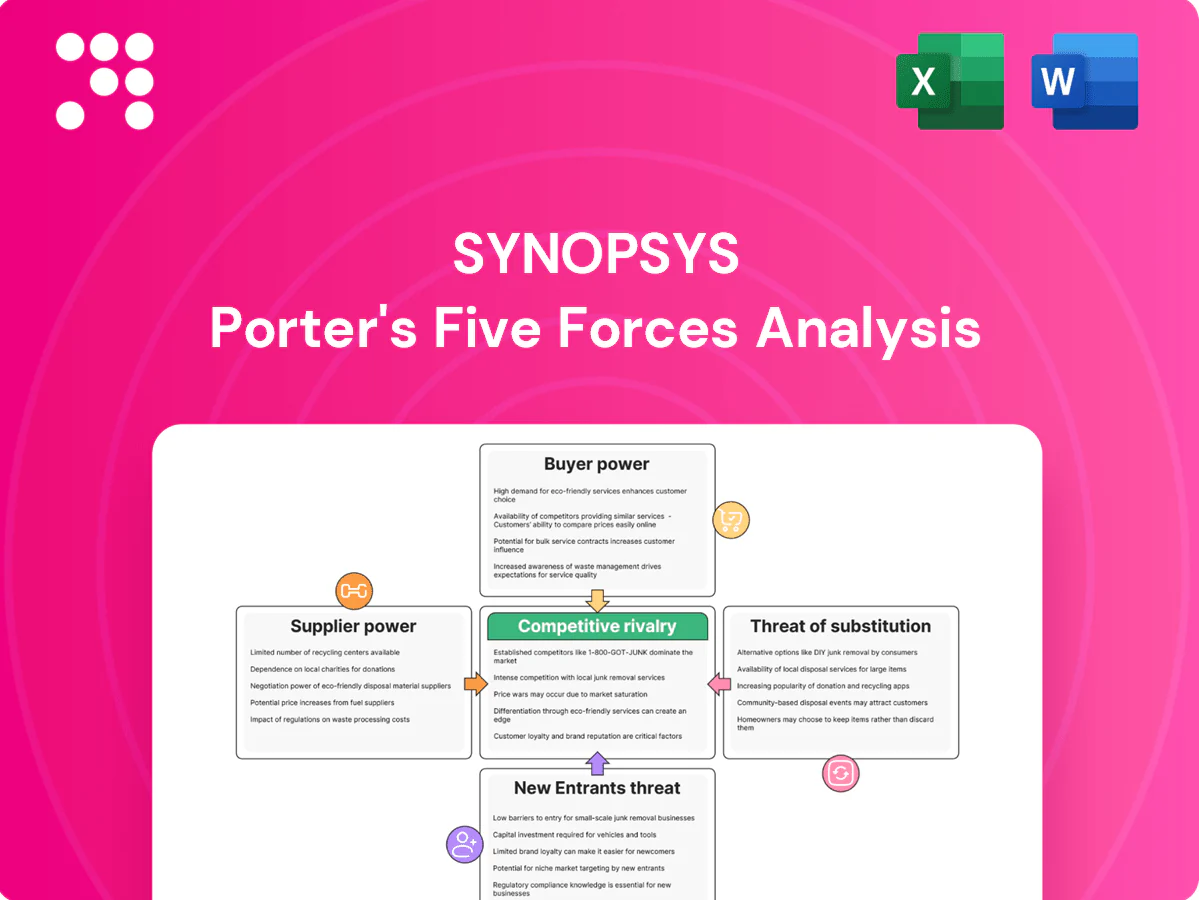

Synopsys's Porter's Five Forces Analysis highlights intense rivalry from established EDA competitors, high supplier specialization, strong buyer leverage in chip design cycles, moderate threat of new entrants due to scale barriers, and evolving substitute risks from open-source tools. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Synopsys’s competitive dynamics in detail.

Suppliers Bargaining Power

PDK and foundry rule-deck dependence

Access to up-to-date PDKs and sign-off rule decks from leading foundries is essential for Synopsys to keep tools tape-out ready and accurate. Only a handful of advanced-node foundries exist—TSMC, Samsung, Intel—TSMC alone holds roughly 50% of advanced-node capacity, concentrating supplier influence. Synopsys’s scale (>$5B revenue range) and deep co-optimization programs temper unilateral power, while joint development roadmaps reduce surprise rule changes and align incentives.

Compute, cloud, and EDA infrastructure inputs

High-performance compute, GPUs, and cloud capacity are critical for AI-driven and large-scale verification, with hyperscalers AWS, Azure, and GCP commanding roughly 64% of cloud infrastructure in 2024 and NVIDIA holding about 80%+ of datacenter GPU share in 2024, elevating input cost exposure.

Concentration among hyperscalers and chip vendors increases supplier leverage, but long-term enterprise agreements and multicloud adoption blunt pricing shocks.

Synopsys and peers report tool optimizations and hardware-aware runtimes that can cut compute intensity materially, with vendor claims of up to ~30% runtime reductions, further diluting supplier power.

Specialized algorithmic talent and academia

EDA innovation depends on scarce PhD-level algorithm and ML talent clustered at top universities, driving wage inflation and retention risk; with Synopsys investing roughly $1.6B in R&D in 2024 to compete for this pool, its brand, competitive compensation and research partnerships (many tied to leading universities) sustain pipeline access, while internal training programs and targeted acquisitions broaden the talent base to reduce single-source risk.

Standards bodies and ecosystem IP libraries

Standards conformance (IEEE, Accellera) and access to interface specs drive tool interoperability; evolving specs force rework and timing pressure, but Synopsys mitigates risk through active standards participation and influence. Synopsys reported fiscal 2024 revenue of about $5.46B, supporting broad VIP and DesignWare IP portfolios that reduce supplier leverage.

- Standards influence

- Rework/timing risk

- Standards participation

- Broad VIP/IP cushion

Third-party datasets and tool components

Certain flows rely on external solvers, parsers, or datasets to accelerate development, creating concentration risks and switching frictions that can pass costs upstream; Synopsys’ 2024 public filings emphasize greater internalization of critical components and proprietary datasets to reduce that dependence. This strategic shift lowers suppliers’ bargaining power over time and mitigates cost pass-through for customers while protecting time-to-market. The move aligns with industry trends toward vertical integration in EDA and IP.

Foundry and GPU/cloud concentration vs scale and R&D resilience

Access to foundry PDKs (TSMC ~50% advanced capacity) and hyperscaler compute (AWS/Azure/GCP ~64% cloud; NVIDIA ~80% datacenter GPUs) concentrates supplier power, but Synopsys scale (revenue ~$5.46B in 2024) and long-term partnerships lower risk. Internalization of datasets/IP and R&D spend (~$1.6B in 2024) reduces upstream leverage and switching costs.

| Supplier | Concentration | Impact | Synopsys mitigation |

|---|---|---|---|

| Foundries | TSMC ~50% | High | JVs/PDK access |

| Cloud/GPU | AWS/Azure/GCP ~64%; NVIDIA ~80% | Medium-High | Multicloud, optimizations |

| Talent/IP | Top universities scarce | Medium | $1.6B R&D, partnerships |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Synopsys, assessing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive risks and strategic advantages.

A concise, one-sheet Porter's Five Forces for Synopsys that distills competitive pressure and strategic risks into board-ready insight for faster decision-making. Customizable force levels and a visual spider chart make it easy to update for new technologies, M&A or regulation shifts.

Customers Bargaining Power

Concentrated global semiconductor customers

Large fabless and IDM customers negotiate sizable, multi-year (typically 3–5 year) enterprise deals, increasing price sensitivity and demands for favorable terms; customer concentration among a handful of hyperscale buyers raises negotiation leverage. Mission-criticality of EDA and verified sign-off status at leading foundries (TSMC, Samsung) constrain aggressive discounting. Wins at advanced nodes (5nm/3nm sign-offs) strengthen Synopsys’s negotiating position.

High switching costs and workflow lock-in

Design flows span many tools, scripts, and IP, creating deep integration lock-in that ties Synopsys tools into multi-stage toolchains and verification environments. Switching jeopardizes time-to-market and yield, elevating operational risk and often adding months to delivery timelines and significant validation cost. This dampens buyer power despite procurement scale, making incremental displacement more common than wholesale swaps.

Performance at leading nodes drives willingness to pay

At 3nm and beyond, measurable PPA and time-to-tape-out gains drive buyer willingness to pay, with customers in 2024 tolerating premium licensing when flows cut tape-out risk. Benchmarking and silicon-proven results are decisive in negotiations, shifting leverage to vendors that can demonstrate real-world node enablement. Strong node enablement reduces pricing pressure by making tool choice functionally indispensable.

Bundling and enterprise licensing dynamics

Synopsys' portfolio breadth across front-end, back-end and verification enables bundled enterprise licensing that trades lower effective per-tool price for standardized flows and premium support; buyers gain volume discounts and simplified procurement but concede flexibility to substitute best-of-breed point tools. Vendor-managed flows reduce buyers' multi-vendor leverage and increase switching costs.

- Bundling: standardization vs flexibility

- Discounts: volume pricing, less point-tool leverage

- Switching costs: vendor-managed flows raise lock-in

Compliance, security, and support expectations

Enterprise customers demand robust security, strict SLAs, and global support, which raise switching costs and make product quality and compliance primary buying criteria; superior 24/7 support and security certifications reduce customers ability to extract price concessions, while lapses in support or breaches would rapidly amplify buyer power and churn risk.

- security-first procurement

- high switching costs

- support lowers price leverage

- poor support increases churn

Buyer leverage vs toolchain lock-in: 5nm/3nm sign-offs and 24/7 SLAs limit discounts

Large fabless/IDM customers (3–5 year enterprise deals) and hyperscaler concentration increase buyer leverage, but mission-critical EDA sign-offs at TSMC/Samsung and deep toolchain lock-in limit aggressive price pressure. Proven 5nm/3nm node enablement and bundled enterprise licensing shift negotiating power toward Synopsys, while security, SLAs and 24/7 support raise switching costs and reduce discounting.

| Metric | 2024 |

|---|---|

| Synopsys FY revenue | ~$5.0B (FY2024) |

| Typical enterprise deal | 3–5 years |

Preview the Actual Deliverable

Synopsys Porter's Five Forces Analysis

This Synopsys Porter's Five Forces Analysis preview is the exact document you'll receive immediately after purchase—no placeholders or mockups. It is professionally written, fully formatted, and ready for immediate download and use. No customization or setup required.

A Must-Have Tool for Decision-Makers

Synopsys's Porter's Five Forces Analysis highlights intense rivalry from established EDA competitors, high supplier specialization, strong buyer leverage in chip design cycles, moderate threat of new entrants due to scale barriers, and evolving substitute risks from open-source tools. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Synopsys’s competitive dynamics in detail.

Suppliers Bargaining Power

PDK and foundry rule-deck dependence

Access to up-to-date PDKs and sign-off rule decks from leading foundries is essential for Synopsys to keep tools tape-out ready and accurate. Only a handful of advanced-node foundries exist—TSMC, Samsung, Intel—TSMC alone holds roughly 50% of advanced-node capacity, concentrating supplier influence. Synopsys’s scale (>$5B revenue range) and deep co-optimization programs temper unilateral power, while joint development roadmaps reduce surprise rule changes and align incentives.

Compute, cloud, and EDA infrastructure inputs

High-performance compute, GPUs, and cloud capacity are critical for AI-driven and large-scale verification, with hyperscalers AWS, Azure, and GCP commanding roughly 64% of cloud infrastructure in 2024 and NVIDIA holding about 80%+ of datacenter GPU share in 2024, elevating input cost exposure.

Concentration among hyperscalers and chip vendors increases supplier leverage, but long-term enterprise agreements and multicloud adoption blunt pricing shocks.

Synopsys and peers report tool optimizations and hardware-aware runtimes that can cut compute intensity materially, with vendor claims of up to ~30% runtime reductions, further diluting supplier power.

Specialized algorithmic talent and academia

EDA innovation depends on scarce PhD-level algorithm and ML talent clustered at top universities, driving wage inflation and retention risk; with Synopsys investing roughly $1.6B in R&D in 2024 to compete for this pool, its brand, competitive compensation and research partnerships (many tied to leading universities) sustain pipeline access, while internal training programs and targeted acquisitions broaden the talent base to reduce single-source risk.

Standards bodies and ecosystem IP libraries

Standards conformance (IEEE, Accellera) and access to interface specs drive tool interoperability; evolving specs force rework and timing pressure, but Synopsys mitigates risk through active standards participation and influence. Synopsys reported fiscal 2024 revenue of about $5.46B, supporting broad VIP and DesignWare IP portfolios that reduce supplier leverage.

- Standards influence

- Rework/timing risk

- Standards participation

- Broad VIP/IP cushion

Third-party datasets and tool components

Certain flows rely on external solvers, parsers, or datasets to accelerate development, creating concentration risks and switching frictions that can pass costs upstream; Synopsys’ 2024 public filings emphasize greater internalization of critical components and proprietary datasets to reduce that dependence. This strategic shift lowers suppliers’ bargaining power over time and mitigates cost pass-through for customers while protecting time-to-market. The move aligns with industry trends toward vertical integration in EDA and IP.

Foundry and GPU/cloud concentration vs scale and R&D resilience

Access to foundry PDKs (TSMC ~50% advanced capacity) and hyperscaler compute (AWS/Azure/GCP ~64% cloud; NVIDIA ~80% datacenter GPUs) concentrates supplier power, but Synopsys scale (revenue ~$5.46B in 2024) and long-term partnerships lower risk. Internalization of datasets/IP and R&D spend (~$1.6B in 2024) reduces upstream leverage and switching costs.

| Supplier | Concentration | Impact | Synopsys mitigation |

|---|---|---|---|

| Foundries | TSMC ~50% | High | JVs/PDK access |

| Cloud/GPU | AWS/Azure/GCP ~64%; NVIDIA ~80% | Medium-High | Multicloud, optimizations |

| Talent/IP | Top universities scarce | Medium | $1.6B R&D, partnerships |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Synopsys, assessing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive risks and strategic advantages.

A concise, one-sheet Porter's Five Forces for Synopsys that distills competitive pressure and strategic risks into board-ready insight for faster decision-making. Customizable force levels and a visual spider chart make it easy to update for new technologies, M&A or regulation shifts.

Customers Bargaining Power

Concentrated global semiconductor customers

Large fabless and IDM customers negotiate sizable, multi-year (typically 3–5 year) enterprise deals, increasing price sensitivity and demands for favorable terms; customer concentration among a handful of hyperscale buyers raises negotiation leverage. Mission-criticality of EDA and verified sign-off status at leading foundries (TSMC, Samsung) constrain aggressive discounting. Wins at advanced nodes (5nm/3nm sign-offs) strengthen Synopsys’s negotiating position.

High switching costs and workflow lock-in

Design flows span many tools, scripts, and IP, creating deep integration lock-in that ties Synopsys tools into multi-stage toolchains and verification environments. Switching jeopardizes time-to-market and yield, elevating operational risk and often adding months to delivery timelines and significant validation cost. This dampens buyer power despite procurement scale, making incremental displacement more common than wholesale swaps.

Performance at leading nodes drives willingness to pay

At 3nm and beyond, measurable PPA and time-to-tape-out gains drive buyer willingness to pay, with customers in 2024 tolerating premium licensing when flows cut tape-out risk. Benchmarking and silicon-proven results are decisive in negotiations, shifting leverage to vendors that can demonstrate real-world node enablement. Strong node enablement reduces pricing pressure by making tool choice functionally indispensable.

Bundling and enterprise licensing dynamics

Synopsys' portfolio breadth across front-end, back-end and verification enables bundled enterprise licensing that trades lower effective per-tool price for standardized flows and premium support; buyers gain volume discounts and simplified procurement but concede flexibility to substitute best-of-breed point tools. Vendor-managed flows reduce buyers' multi-vendor leverage and increase switching costs.

- Bundling: standardization vs flexibility

- Discounts: volume pricing, less point-tool leverage

- Switching costs: vendor-managed flows raise lock-in

Compliance, security, and support expectations

Enterprise customers demand robust security, strict SLAs, and global support, which raise switching costs and make product quality and compliance primary buying criteria; superior 24/7 support and security certifications reduce customers ability to extract price concessions, while lapses in support or breaches would rapidly amplify buyer power and churn risk.

- security-first procurement

- high switching costs

- support lowers price leverage

- poor support increases churn

Buyer leverage vs toolchain lock-in: 5nm/3nm sign-offs and 24/7 SLAs limit discounts

Large fabless/IDM customers (3–5 year enterprise deals) and hyperscaler concentration increase buyer leverage, but mission-critical EDA sign-offs at TSMC/Samsung and deep toolchain lock-in limit aggressive price pressure. Proven 5nm/3nm node enablement and bundled enterprise licensing shift negotiating power toward Synopsys, while security, SLAs and 24/7 support raise switching costs and reduce discounting.

| Metric | 2024 |

|---|---|

| Synopsys FY revenue | ~$5.0B (FY2024) |

| Typical enterprise deal | 3–5 years |

Preview the Actual Deliverable

Synopsys Porter's Five Forces Analysis

This Synopsys Porter's Five Forces Analysis preview is the exact document you'll receive immediately after purchase—no placeholders or mockups. It is professionally written, fully formatted, and ready for immediate download and use. No customization or setup required.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Synopsys's Porter's Five Forces Analysis highlights intense rivalry from established EDA competitors, high supplier specialization, strong buyer leverage in chip design cycles, moderate threat of new entrants due to scale barriers, and evolving substitute risks from open-source tools. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Synopsys’s competitive dynamics in detail.

Suppliers Bargaining Power

PDK and foundry rule-deck dependence

Access to up-to-date PDKs and sign-off rule decks from leading foundries is essential for Synopsys to keep tools tape-out ready and accurate. Only a handful of advanced-node foundries exist—TSMC, Samsung, Intel—TSMC alone holds roughly 50% of advanced-node capacity, concentrating supplier influence. Synopsys’s scale (>$5B revenue range) and deep co-optimization programs temper unilateral power, while joint development roadmaps reduce surprise rule changes and align incentives.

Compute, cloud, and EDA infrastructure inputs

High-performance compute, GPUs, and cloud capacity are critical for AI-driven and large-scale verification, with hyperscalers AWS, Azure, and GCP commanding roughly 64% of cloud infrastructure in 2024 and NVIDIA holding about 80%+ of datacenter GPU share in 2024, elevating input cost exposure.

Concentration among hyperscalers and chip vendors increases supplier leverage, but long-term enterprise agreements and multicloud adoption blunt pricing shocks.

Synopsys and peers report tool optimizations and hardware-aware runtimes that can cut compute intensity materially, with vendor claims of up to ~30% runtime reductions, further diluting supplier power.

Specialized algorithmic talent and academia

EDA innovation depends on scarce PhD-level algorithm and ML talent clustered at top universities, driving wage inflation and retention risk; with Synopsys investing roughly $1.6B in R&D in 2024 to compete for this pool, its brand, competitive compensation and research partnerships (many tied to leading universities) sustain pipeline access, while internal training programs and targeted acquisitions broaden the talent base to reduce single-source risk.

Standards bodies and ecosystem IP libraries

Standards conformance (IEEE, Accellera) and access to interface specs drive tool interoperability; evolving specs force rework and timing pressure, but Synopsys mitigates risk through active standards participation and influence. Synopsys reported fiscal 2024 revenue of about $5.46B, supporting broad VIP and DesignWare IP portfolios that reduce supplier leverage.

- Standards influence

- Rework/timing risk

- Standards participation

- Broad VIP/IP cushion

Third-party datasets and tool components

Certain flows rely on external solvers, parsers, or datasets to accelerate development, creating concentration risks and switching frictions that can pass costs upstream; Synopsys’ 2024 public filings emphasize greater internalization of critical components and proprietary datasets to reduce that dependence. This strategic shift lowers suppliers’ bargaining power over time and mitigates cost pass-through for customers while protecting time-to-market. The move aligns with industry trends toward vertical integration in EDA and IP.

Foundry and GPU/cloud concentration vs scale and R&D resilience

Access to foundry PDKs (TSMC ~50% advanced capacity) and hyperscaler compute (AWS/Azure/GCP ~64% cloud; NVIDIA ~80% datacenter GPUs) concentrates supplier power, but Synopsys scale (revenue ~$5.46B in 2024) and long-term partnerships lower risk. Internalization of datasets/IP and R&D spend (~$1.6B in 2024) reduces upstream leverage and switching costs.

| Supplier | Concentration | Impact | Synopsys mitigation |

|---|---|---|---|

| Foundries | TSMC ~50% | High | JVs/PDK access |

| Cloud/GPU | AWS/Azure/GCP ~64%; NVIDIA ~80% | Medium-High | Multicloud, optimizations |

| Talent/IP | Top universities scarce | Medium | $1.6B R&D, partnerships |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Synopsys, assessing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive risks and strategic advantages.

A concise, one-sheet Porter's Five Forces for Synopsys that distills competitive pressure and strategic risks into board-ready insight for faster decision-making. Customizable force levels and a visual spider chart make it easy to update for new technologies, M&A or regulation shifts.

Customers Bargaining Power

Concentrated global semiconductor customers

Large fabless and IDM customers negotiate sizable, multi-year (typically 3–5 year) enterprise deals, increasing price sensitivity and demands for favorable terms; customer concentration among a handful of hyperscale buyers raises negotiation leverage. Mission-criticality of EDA and verified sign-off status at leading foundries (TSMC, Samsung) constrain aggressive discounting. Wins at advanced nodes (5nm/3nm sign-offs) strengthen Synopsys’s negotiating position.

High switching costs and workflow lock-in

Design flows span many tools, scripts, and IP, creating deep integration lock-in that ties Synopsys tools into multi-stage toolchains and verification environments. Switching jeopardizes time-to-market and yield, elevating operational risk and often adding months to delivery timelines and significant validation cost. This dampens buyer power despite procurement scale, making incremental displacement more common than wholesale swaps.

Performance at leading nodes drives willingness to pay

At 3nm and beyond, measurable PPA and time-to-tape-out gains drive buyer willingness to pay, with customers in 2024 tolerating premium licensing when flows cut tape-out risk. Benchmarking and silicon-proven results are decisive in negotiations, shifting leverage to vendors that can demonstrate real-world node enablement. Strong node enablement reduces pricing pressure by making tool choice functionally indispensable.

Bundling and enterprise licensing dynamics

Synopsys' portfolio breadth across front-end, back-end and verification enables bundled enterprise licensing that trades lower effective per-tool price for standardized flows and premium support; buyers gain volume discounts and simplified procurement but concede flexibility to substitute best-of-breed point tools. Vendor-managed flows reduce buyers' multi-vendor leverage and increase switching costs.

- Bundling: standardization vs flexibility

- Discounts: volume pricing, less point-tool leverage

- Switching costs: vendor-managed flows raise lock-in

Compliance, security, and support expectations

Enterprise customers demand robust security, strict SLAs, and global support, which raise switching costs and make product quality and compliance primary buying criteria; superior 24/7 support and security certifications reduce customers ability to extract price concessions, while lapses in support or breaches would rapidly amplify buyer power and churn risk.

- security-first procurement

- high switching costs

- support lowers price leverage

- poor support increases churn

Buyer leverage vs toolchain lock-in: 5nm/3nm sign-offs and 24/7 SLAs limit discounts

Large fabless/IDM customers (3–5 year enterprise deals) and hyperscaler concentration increase buyer leverage, but mission-critical EDA sign-offs at TSMC/Samsung and deep toolchain lock-in limit aggressive price pressure. Proven 5nm/3nm node enablement and bundled enterprise licensing shift negotiating power toward Synopsys, while security, SLAs and 24/7 support raise switching costs and reduce discounting.

| Metric | 2024 |

|---|---|

| Synopsys FY revenue | ~$5.0B (FY2024) |

| Typical enterprise deal | 3–5 years |

Preview the Actual Deliverable

Synopsys Porter's Five Forces Analysis

This Synopsys Porter's Five Forces Analysis preview is the exact document you'll receive immediately after purchase—no placeholders or mockups. It is professionally written, fully formatted, and ready for immediate download and use. No customization or setup required.