Synthomer Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

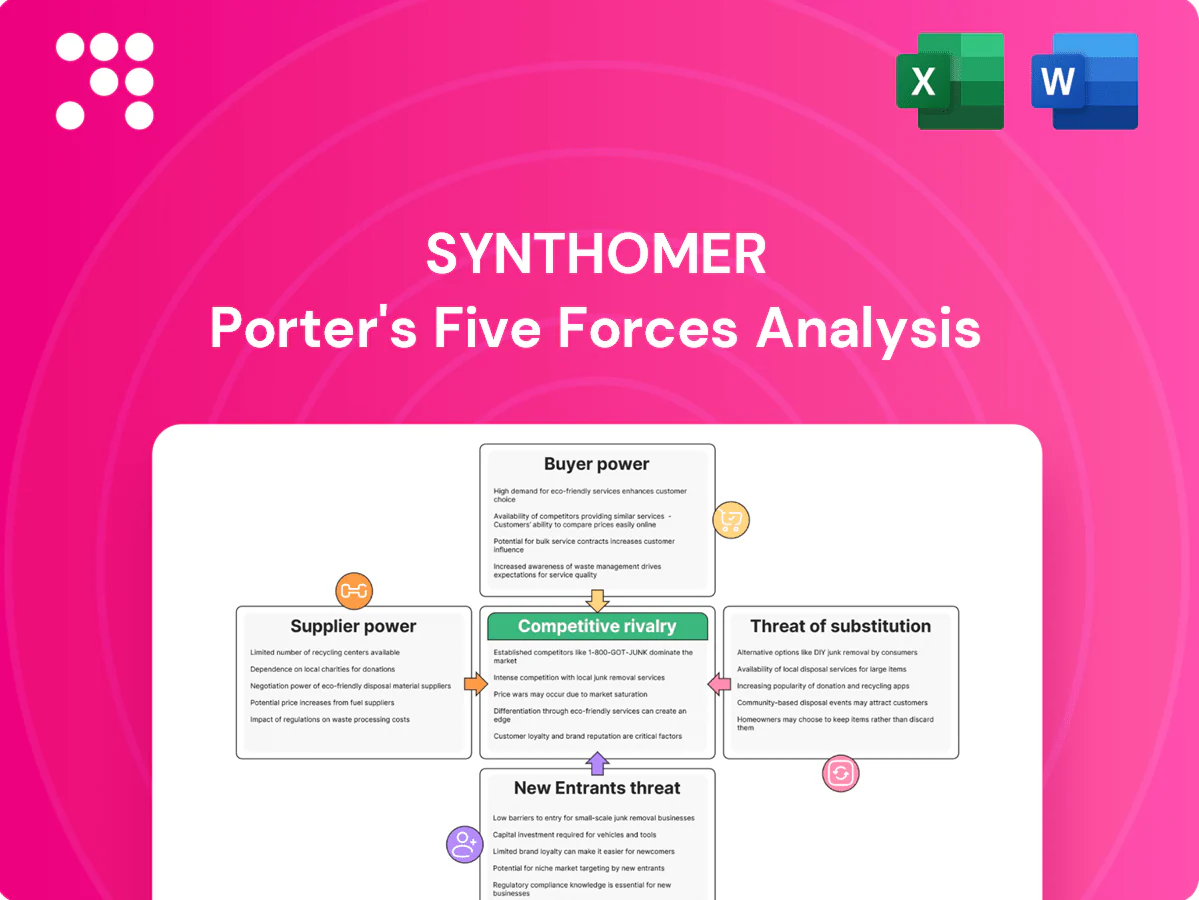

Synthomer's Porter's Five Forces snapshot highlights moderate supplier power, high buyer pressure in commoditised segments, rising substitute threats and regulatory/input-cost headwinds; competitive rivalry is intense across specialty and commodity markets, with entry barriers varying by segment. This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Synthomer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated petrochemical feedstocks

Core monomers (butadiene, styrene, acrylates, VAM) originate from a concentrated petrochemical base, giving upstream suppliers measurable leverage; in 2024 supply tightness and regional outages repeatedly pushed spot markets higher. Synthomer reduces exposure through multisourcing and regional diversification and uses strategic inventory and hedging, but supplier concentration still elevates bargaining power. Structural leverage from feedstock concentration cannot be fully offset.

Price volatility and energy linkage

Feedstock and energy prices are tightly linked to polymer costs, with Brent crude averaging about $86/bbl in 2024 transmitting volatility into Synthomer's raw-material base; rapid pass-through is constrained by customer contracts, compressing margins during spikes. Long-term supply agreements with indexation smooth some swings, but supplier leverage rises sharply in tight cycles when feedstock-driven costs outpace contract repricing.

Logistics and specialty additives

Specialty additives, surfactants and functional monomers are often single- or few-source, raising supplier leverage; qualification of alternatives typically takes 6–12 months, slowing switching. Port congestion and hazardous‑materials routing constraints create logistical friction suppliers can monetize. Nearshoring and dual sourcing mitigate risk where feasible but remain limited by technical qualification and CAPEX.

Sustainability-grade inputs

- Narrow supplier pool: higher switching costs and supply risk

- Price premium: c.10–25% for certified/mass-balance feedstocks (industry range)

- Bottleneck risk: limits growth of sustainable product lines

- Mitigation: early partnerships, long-term contracts, certification programs

Switching costs and specifications

Changing a critical monomer or additive often forces requalification of Synthomer formulations because technical performance and REACH/registration dossiers are tied to specific inputs, raising buyer switching costs while simultaneously locking Synthomer to those suppliers, sustaining moderate-to-high supplier power.

- Requalification timelines: laboratory and regulatory steps

- Regulatory linkage: REACH dossiers bind inputs

- Mutual lock-in: supplier dependency raises supplier leverage

Upstream petrochemical concentration boosts supplier leverage after 2024 feed tightness

Upstream petrochemical concentration gives suppliers measurable leverage; 2024 feed tightness raised spot prices and kept supplier power moderate-to-high. Brent averaged about $86/bbl in 2024, transmitting volatility into polymer costs; certified/mass‑balance feedstocks carried premiums of c.10–25%. Requalification of critical monomers/additives typically takes 6–12 months, raising switching costs.

| Metric | 2024 / Note |

|---|---|

| Brent crude | $86/bbl (2024 avg) |

| Certified feedstock premium | c.10–25% (industry) |

| Requalification time | 6–12 months |

| Supplier structure | Concentrated petrochemical base |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Synthomer, uncovering key drivers of competition, supplier and buyer power, substitutes and entry risks, and identifying disruptive threats to its market share and profitability.

Relieves analysis bottlenecks with a concise, one-sheet Synthomer Porter's Five Forces summary—customize pressure levels, view instant spider-chart visuals, and copy slide-ready layouts for fast, boardroom-ready decisions.

Customers Bargaining Power

Consolidated downstream customers

Large coatings, adhesives, construction and healthcare OEMs with global procurement teams push Synthomer for price concessions and higher service levels; in 2024 Synthomer reported revenue of about £2.7bn, exposing margin sensitivity to volume discounts. Volume leverage and multi-year tenders from OEMs amplify customer bargaining power, while Synthomer mitigates pressure by embedding application support and tailored polymer formulations to increase switching costs and retain contracts.

High qualification and reformulation costs

End-use criticality and regulatory approvals (REACH, FDA) in 2024 create strong switching frictions for Synthomer customers, as alternative polymers often require fresh certification and validation. Reformulation risks product performance, project timelines, and compliance, raising technical and commercial barriers. These frictions curb immediate price-driven switching and temper buyer power, although large buyers can gradually dual-source to restore leverage.

Demand cyclicality and inventory swings

Construction and industrial cycles drive sharp volume swings for Synthomer, with downturns prompting buyers to press for discounts and extended payment terms. In upcycles allocation tightness reduces customer leverage but raises expectations on reliability of supply and lead times. This cyclical pattern produces variable buyer power that fluctuates with sector demand and inventory swings.

Specification and sustainability pull

In 2024 buyers increasingly demand low-VOC, water-borne and bio-based solutions, creating specification-driven leverage that pressures premium pricing. Meeting those specs differentiates Synthomer but invites tougher price negotiations as buyers compare peer offers, compressing premiums. Strong performance data and third-party LCA proofs materially help defend value and retention.

- Specification pull: low-VOC/water-borne/bio-based

- Price pressure: cross-peer comparisons compress premiums

- Defense: performance data + LCA

Limited forward integration risk

Most customers lack incentives to backward integrate into emulsion polymers/latices due to high capital intensity, specialized R&D know-how and heavy 2024 EHS/regulatory burdens, which curbs a major source of buyer power; nevertheless large buyers can sponsor alternate toll or merchant suppliers to sustain pricing pressure.

- Barriers: capex, EHS, technical know-how

- Effect: limited forward integration risk

- Counter: buyer-sponsored alternative suppliers

Global OEM buyer power, regulatory friction and multi-year tenders boost negotiating leverage

Large OEMs with global procurement and Synthomer's £2.7bn 2024 revenue drive strong price/service demands; multi-year tenders and volume leverage increase buyer power. Regulatory approvals (REACH/FDA) and reformulation costs limit switching, but large buyers can dual-source or sponsor toll suppliers to press prices.

| Metric | 2024 |

|---|---|

| Revenue | £2.7bn |

| Buyer leverage | High |

| Switching friction | Strong |

Same Document Delivered

Synthomer Porter's Five Forces Analysis

This preview shows the exact Synthomer Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. Instant access to the same complete file is granted upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Synthomer's Porter's Five Forces snapshot highlights moderate supplier power, high buyer pressure in commoditised segments, rising substitute threats and regulatory/input-cost headwinds; competitive rivalry is intense across specialty and commodity markets, with entry barriers varying by segment. This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Synthomer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated petrochemical feedstocks

Core monomers (butadiene, styrene, acrylates, VAM) originate from a concentrated petrochemical base, giving upstream suppliers measurable leverage; in 2024 supply tightness and regional outages repeatedly pushed spot markets higher. Synthomer reduces exposure through multisourcing and regional diversification and uses strategic inventory and hedging, but supplier concentration still elevates bargaining power. Structural leverage from feedstock concentration cannot be fully offset.

Price volatility and energy linkage

Feedstock and energy prices are tightly linked to polymer costs, with Brent crude averaging about $86/bbl in 2024 transmitting volatility into Synthomer's raw-material base; rapid pass-through is constrained by customer contracts, compressing margins during spikes. Long-term supply agreements with indexation smooth some swings, but supplier leverage rises sharply in tight cycles when feedstock-driven costs outpace contract repricing.

Logistics and specialty additives

Specialty additives, surfactants and functional monomers are often single- or few-source, raising supplier leverage; qualification of alternatives typically takes 6–12 months, slowing switching. Port congestion and hazardous‑materials routing constraints create logistical friction suppliers can monetize. Nearshoring and dual sourcing mitigate risk where feasible but remain limited by technical qualification and CAPEX.

Sustainability-grade inputs

- Narrow supplier pool: higher switching costs and supply risk

- Price premium: c.10–25% for certified/mass-balance feedstocks (industry range)

- Bottleneck risk: limits growth of sustainable product lines

- Mitigation: early partnerships, long-term contracts, certification programs

Switching costs and specifications

Changing a critical monomer or additive often forces requalification of Synthomer formulations because technical performance and REACH/registration dossiers are tied to specific inputs, raising buyer switching costs while simultaneously locking Synthomer to those suppliers, sustaining moderate-to-high supplier power.

- Requalification timelines: laboratory and regulatory steps

- Regulatory linkage: REACH dossiers bind inputs

- Mutual lock-in: supplier dependency raises supplier leverage

Upstream petrochemical concentration boosts supplier leverage after 2024 feed tightness

Upstream petrochemical concentration gives suppliers measurable leverage; 2024 feed tightness raised spot prices and kept supplier power moderate-to-high. Brent averaged about $86/bbl in 2024, transmitting volatility into polymer costs; certified/mass‑balance feedstocks carried premiums of c.10–25%. Requalification of critical monomers/additives typically takes 6–12 months, raising switching costs.

| Metric | 2024 / Note |

|---|---|

| Brent crude | $86/bbl (2024 avg) |

| Certified feedstock premium | c.10–25% (industry) |

| Requalification time | 6–12 months |

| Supplier structure | Concentrated petrochemical base |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Synthomer, uncovering key drivers of competition, supplier and buyer power, substitutes and entry risks, and identifying disruptive threats to its market share and profitability.

Relieves analysis bottlenecks with a concise, one-sheet Synthomer Porter's Five Forces summary—customize pressure levels, view instant spider-chart visuals, and copy slide-ready layouts for fast, boardroom-ready decisions.

Customers Bargaining Power

Consolidated downstream customers

Large coatings, adhesives, construction and healthcare OEMs with global procurement teams push Synthomer for price concessions and higher service levels; in 2024 Synthomer reported revenue of about £2.7bn, exposing margin sensitivity to volume discounts. Volume leverage and multi-year tenders from OEMs amplify customer bargaining power, while Synthomer mitigates pressure by embedding application support and tailored polymer formulations to increase switching costs and retain contracts.

High qualification and reformulation costs

End-use criticality and regulatory approvals (REACH, FDA) in 2024 create strong switching frictions for Synthomer customers, as alternative polymers often require fresh certification and validation. Reformulation risks product performance, project timelines, and compliance, raising technical and commercial barriers. These frictions curb immediate price-driven switching and temper buyer power, although large buyers can gradually dual-source to restore leverage.

Demand cyclicality and inventory swings

Construction and industrial cycles drive sharp volume swings for Synthomer, with downturns prompting buyers to press for discounts and extended payment terms. In upcycles allocation tightness reduces customer leverage but raises expectations on reliability of supply and lead times. This cyclical pattern produces variable buyer power that fluctuates with sector demand and inventory swings.

Specification and sustainability pull

In 2024 buyers increasingly demand low-VOC, water-borne and bio-based solutions, creating specification-driven leverage that pressures premium pricing. Meeting those specs differentiates Synthomer but invites tougher price negotiations as buyers compare peer offers, compressing premiums. Strong performance data and third-party LCA proofs materially help defend value and retention.

- Specification pull: low-VOC/water-borne/bio-based

- Price pressure: cross-peer comparisons compress premiums

- Defense: performance data + LCA

Limited forward integration risk

Most customers lack incentives to backward integrate into emulsion polymers/latices due to high capital intensity, specialized R&D know-how and heavy 2024 EHS/regulatory burdens, which curbs a major source of buyer power; nevertheless large buyers can sponsor alternate toll or merchant suppliers to sustain pricing pressure.

- Barriers: capex, EHS, technical know-how

- Effect: limited forward integration risk

- Counter: buyer-sponsored alternative suppliers

Global OEM buyer power, regulatory friction and multi-year tenders boost negotiating leverage

Large OEMs with global procurement and Synthomer's £2.7bn 2024 revenue drive strong price/service demands; multi-year tenders and volume leverage increase buyer power. Regulatory approvals (REACH/FDA) and reformulation costs limit switching, but large buyers can dual-source or sponsor toll suppliers to press prices.

| Metric | 2024 |

|---|---|

| Revenue | £2.7bn |

| Buyer leverage | High |

| Switching friction | Strong |

Same Document Delivered

Synthomer Porter's Five Forces Analysis

This preview shows the exact Synthomer Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. Instant access to the same complete file is granted upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Synthomer's Porter's Five Forces snapshot highlights moderate supplier power, high buyer pressure in commoditised segments, rising substitute threats and regulatory/input-cost headwinds; competitive rivalry is intense across specialty and commodity markets, with entry barriers varying by segment. This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Synthomer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated petrochemical feedstocks

Core monomers (butadiene, styrene, acrylates, VAM) originate from a concentrated petrochemical base, giving upstream suppliers measurable leverage; in 2024 supply tightness and regional outages repeatedly pushed spot markets higher. Synthomer reduces exposure through multisourcing and regional diversification and uses strategic inventory and hedging, but supplier concentration still elevates bargaining power. Structural leverage from feedstock concentration cannot be fully offset.

Price volatility and energy linkage

Feedstock and energy prices are tightly linked to polymer costs, with Brent crude averaging about $86/bbl in 2024 transmitting volatility into Synthomer's raw-material base; rapid pass-through is constrained by customer contracts, compressing margins during spikes. Long-term supply agreements with indexation smooth some swings, but supplier leverage rises sharply in tight cycles when feedstock-driven costs outpace contract repricing.

Logistics and specialty additives

Specialty additives, surfactants and functional monomers are often single- or few-source, raising supplier leverage; qualification of alternatives typically takes 6–12 months, slowing switching. Port congestion and hazardous‑materials routing constraints create logistical friction suppliers can monetize. Nearshoring and dual sourcing mitigate risk where feasible but remain limited by technical qualification and CAPEX.

Sustainability-grade inputs

- Narrow supplier pool: higher switching costs and supply risk

- Price premium: c.10–25% for certified/mass-balance feedstocks (industry range)

- Bottleneck risk: limits growth of sustainable product lines

- Mitigation: early partnerships, long-term contracts, certification programs

Switching costs and specifications

Changing a critical monomer or additive often forces requalification of Synthomer formulations because technical performance and REACH/registration dossiers are tied to specific inputs, raising buyer switching costs while simultaneously locking Synthomer to those suppliers, sustaining moderate-to-high supplier power.

- Requalification timelines: laboratory and regulatory steps

- Regulatory linkage: REACH dossiers bind inputs

- Mutual lock-in: supplier dependency raises supplier leverage

Upstream petrochemical concentration boosts supplier leverage after 2024 feed tightness

Upstream petrochemical concentration gives suppliers measurable leverage; 2024 feed tightness raised spot prices and kept supplier power moderate-to-high. Brent averaged about $86/bbl in 2024, transmitting volatility into polymer costs; certified/mass‑balance feedstocks carried premiums of c.10–25%. Requalification of critical monomers/additives typically takes 6–12 months, raising switching costs.

| Metric | 2024 / Note |

|---|---|

| Brent crude | $86/bbl (2024 avg) |

| Certified feedstock premium | c.10–25% (industry) |

| Requalification time | 6–12 months |

| Supplier structure | Concentrated petrochemical base |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Synthomer, uncovering key drivers of competition, supplier and buyer power, substitutes and entry risks, and identifying disruptive threats to its market share and profitability.

Relieves analysis bottlenecks with a concise, one-sheet Synthomer Porter's Five Forces summary—customize pressure levels, view instant spider-chart visuals, and copy slide-ready layouts for fast, boardroom-ready decisions.

Customers Bargaining Power

Consolidated downstream customers

Large coatings, adhesives, construction and healthcare OEMs with global procurement teams push Synthomer for price concessions and higher service levels; in 2024 Synthomer reported revenue of about £2.7bn, exposing margin sensitivity to volume discounts. Volume leverage and multi-year tenders from OEMs amplify customer bargaining power, while Synthomer mitigates pressure by embedding application support and tailored polymer formulations to increase switching costs and retain contracts.

High qualification and reformulation costs

End-use criticality and regulatory approvals (REACH, FDA) in 2024 create strong switching frictions for Synthomer customers, as alternative polymers often require fresh certification and validation. Reformulation risks product performance, project timelines, and compliance, raising technical and commercial barriers. These frictions curb immediate price-driven switching and temper buyer power, although large buyers can gradually dual-source to restore leverage.

Demand cyclicality and inventory swings

Construction and industrial cycles drive sharp volume swings for Synthomer, with downturns prompting buyers to press for discounts and extended payment terms. In upcycles allocation tightness reduces customer leverage but raises expectations on reliability of supply and lead times. This cyclical pattern produces variable buyer power that fluctuates with sector demand and inventory swings.

Specification and sustainability pull

In 2024 buyers increasingly demand low-VOC, water-borne and bio-based solutions, creating specification-driven leverage that pressures premium pricing. Meeting those specs differentiates Synthomer but invites tougher price negotiations as buyers compare peer offers, compressing premiums. Strong performance data and third-party LCA proofs materially help defend value and retention.

- Specification pull: low-VOC/water-borne/bio-based

- Price pressure: cross-peer comparisons compress premiums

- Defense: performance data + LCA

Limited forward integration risk

Most customers lack incentives to backward integrate into emulsion polymers/latices due to high capital intensity, specialized R&D know-how and heavy 2024 EHS/regulatory burdens, which curbs a major source of buyer power; nevertheless large buyers can sponsor alternate toll or merchant suppliers to sustain pricing pressure.

- Barriers: capex, EHS, technical know-how

- Effect: limited forward integration risk

- Counter: buyer-sponsored alternative suppliers

Global OEM buyer power, regulatory friction and multi-year tenders boost negotiating leverage

Large OEMs with global procurement and Synthomer's £2.7bn 2024 revenue drive strong price/service demands; multi-year tenders and volume leverage increase buyer power. Regulatory approvals (REACH/FDA) and reformulation costs limit switching, but large buyers can dual-source or sponsor toll suppliers to press prices.

| Metric | 2024 |

|---|---|

| Revenue | £2.7bn |

| Buyer leverage | High |

| Switching friction | Strong |

Same Document Delivered

Synthomer Porter's Five Forces Analysis

This preview shows the exact Synthomer Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. Instant access to the same complete file is granted upon payment.