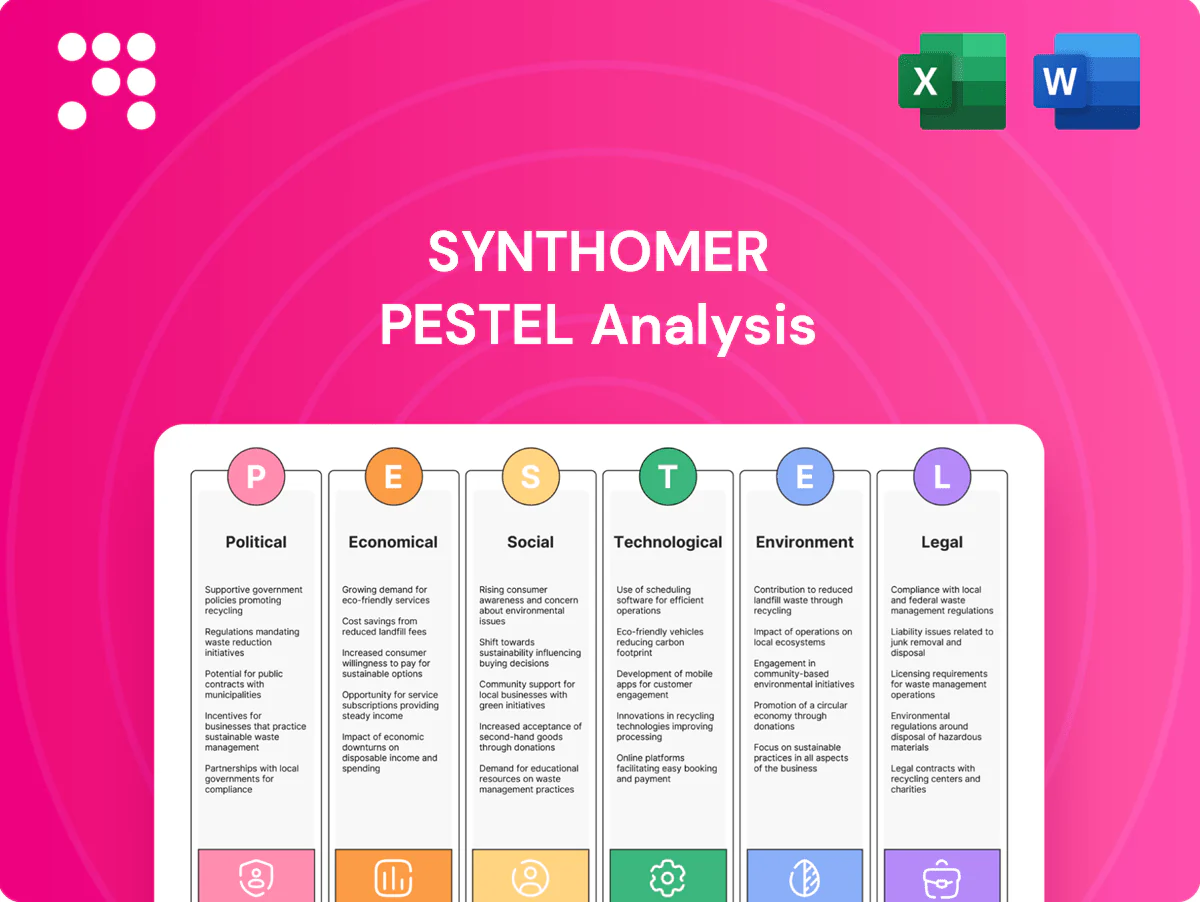

Synthomer PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political shifts, regulatory pressure, economic cycles and environmental trends are influencing Synthomer’s strategy and risk profile in our concise PESTLE snapshot. Use these insights to refine forecasts, spot growth pockets, and stress-test assumptions. Ideal for investors, strategists, and advisors seeking clarity. Purchase the full PESTLE for the complete, actionable breakdown—ready to download now.

Political factors

Trade policies and tariffs

Shifts in tariffs on chemicals, such as US Section 301 measures of up to 25%, directly raise Synthomer’s input costs and compress margins, forcing pass-through pricing or margin erosion. Trade tensions between major blocs have already disrupted polymer supply chains, increasing lead times and spot prices. Proactive sourcing and regional diversification reduce exposure, while government export incentives and subsidies in 2024 can open new markets for specialty binders.

Regulatory stability in key regions

Consistency in EU, UK and US industrial policies underpins investment decisions; Horizon Europe carries a €95.5bn R&D budget (2021–27) while the UK RDEC rate is about 20%, directly affecting project returns. Political turnover can shift funding for green chemistry, altering expected IRRs on 5–10 year plant capex. Stable frameworks enable long-horizon capex and R&D; monitoring policy pipelines aligns product roadmaps early.

Industrial strategy and subsidies

Government grants for decarbonization and advanced materials lower project hurdles; global fiscal support such as the US Inflation Reduction Act allocates about $369bn for energy and climate over a decade and EU NextGenerationEU totals €806.9bn, shaping investment flows. Competing subsidy regimes and IPCEIs influence site selection and cost of capital. Public-private partnerships accelerate scale-up of sustainable polymers while transparent eligibility criteria guide portfolio prioritization.

Geopolitical supply risk

- Tags: supply-risk

- Tags: lead-times

- Tags: multi-source

- Tags: scenario-planning

Public procurement preferences

Green public purchasing favors low-VOC and bio-based dispersions, and EU public procurement is worth about €2 trillion annually, creating sizable demand for certified products; meeting EU Ecolabel/GPP criteria unlocks infrastructure and healthcare contracts often reserved for compliant suppliers. Policy-driven demand has accelerated premium product adoption, and early certification provides clear competitive differentiation for Synthomer.

- Tag: public-procurement

- Tag: low-VOC

- Tag: bio-based

- Tag: EU-ecolabel

- Tag: €2T-market

Tariff shocks, 80% Russian gas drop and green funding spur demand for low-VOC bio inputs

Shifts in tariffs (up to 25%) and trade tensions raise input costs and add lead times (+20–30 days); EU pipeline gas imports from Russia fell ~80% in 2022, tightening feedstock. Policy funding (Horizon €95.5bn, UK RDEC ~20%, IRA $369bn, NextGenerationEU €806.9bn) steers decarbonization capex. EU public procurement (€2T) boosts demand for low-VOC/bio-based products.

| Indicator | Value |

|---|---|

| Tariff cap | 25% |

| Russian gas fall | ~80% (2022) |

| Horizon | €95.5bn (2021–27) |

| IRA | $369bn |

| Public procurement | €2T |

What is included in the product

Explores how external macro-environmental factors uniquely affect Synthomer across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and region-specific trends. Designed for executives and investors, the analysis maps threats and opportunities, offers forward-looking scenarios, and is formatted for direct use in plans, decks, and reports.

A concise, visually segmented Synthomer PESTLE summary that eases stakeholder alignment, supports external risk discussions in planning sessions, and can be dropped into presentations or shared across teams for quick decision-making.

Economic factors

Cyclical end-market demand

Construction and coatings volumes for Synthomer closely follow GDP — IMF put global growth near 3.0% in 2024 — and housing starts (US ~1.5m annualised in 2024), so demand slowdowns compress plant utilization and margins. Broad end-market exposure (industrial, construction, adhesives) partially smooths cycles, while agile production planning and inventory cuts preserve cash during downturns.

Input cost volatility

Petrochemical feedstocks and energy track global markets—Brent crude averaged around $80–90/bbl in 2024–H1 2025, driving naphtha and gas cost swings that feed into Synthomer’s raw-material bills. Cost pass-through lags of roughly 2–3 months can compress realised margins and pressure EBITDA during rapid price moves. Hedging programmes and formula-linked customer pricing materially reduce exposure to spot spikes. Ongoing process-efficiency gains and yield improvements gradually offset margin erosion over time.

Currency fluctuations

Multi-currency revenues and costs expose Synthomer to translation and transaction risk across USD, EUR and other markets, affecting reported margins and cashflow. A stronger US dollar can erode export competitiveness from non-dollar plants and shift regional pricing dynamics. The group uses natural hedges in local sourcing and selective FX derivatives to stabilise earnings. Pricing governance is adjusted to align selling prices with material FX movements.

Interest rates and financing

Higher policy rates (~5% in major markets in 2024) raise borrowing costs for Synthomer’s capex and working capital, compressing margins and lengthening payback periods. A conservative debt structure and <1.5–2.5x net debt/EBITDA target improve flexibility through cycles; prioritising high-IRR, quick-payback projects protects returns while cash discipline enables opportunistic M&A or deleveraging.

- Higher rates ~5% (2024)

- Focus: high IRR, quick payback

- Target leverage: ~1.5–2.5x ND/EBITDA

- Cash discipline → M&A or deleveraging optionality

Customer consolidation

Larger coatings and adhesives customers raise bargaining power; top 10 global coatings firms account for around 45% of the market (2023), intensifying buyer leverage. Long-term contracts give volume visibility but compress pricing. Differentiated performance grades protect margins, while technical service and specification support secure repeat business.

- Customer consolidation: ↑ buyer leverage (~45% top-10 share)

- Contracts: volume visibility vs price squeeze

- Performance grades: margin defense

- Technical service: specification lock-in

Tariff shocks, 80% Russian gas drop and green funding spur demand for low-VOC bio inputs

Global GDP ~3.0% (IMF 2024) and US housing starts ~1.5m (2024) drive demand; cycles hit utilisation and margins. Brent ~$80–90/bbl (2024–H1 2025) and 5% policy rates (major markets, 2024) raise feedstock and financing costs. Top-10 coatings ~45% share (2023) increases buyer power; net debt/EBITDA target ~1.5–2.5x cushions risk.

| Metric | Value |

|---|---|

| Global GDP (2024) | ~3.0% |

| Brent (2024–H1 2025) | $80–90/bbl |

| US housing starts (2024) | ~1.5m |

| Policy rates (2024) | ~5% |

| Top-10 coatings (2023) | ~45% |

| ND/EBITDA target | 1.5–2.5x |

Preview the Actual Deliverable

Synthomer PESTLE Analysis

This Synthomer PESTLE Analysis examines political, economic, social, technological, legal and environmental factors shaping the company's operating environment. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content, structure and layout visible are the final file you'll download immediately after payment.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political shifts, regulatory pressure, economic cycles and environmental trends are influencing Synthomer’s strategy and risk profile in our concise PESTLE snapshot. Use these insights to refine forecasts, spot growth pockets, and stress-test assumptions. Ideal for investors, strategists, and advisors seeking clarity. Purchase the full PESTLE for the complete, actionable breakdown—ready to download now.

Political factors

Trade policies and tariffs

Shifts in tariffs on chemicals, such as US Section 301 measures of up to 25%, directly raise Synthomer’s input costs and compress margins, forcing pass-through pricing or margin erosion. Trade tensions between major blocs have already disrupted polymer supply chains, increasing lead times and spot prices. Proactive sourcing and regional diversification reduce exposure, while government export incentives and subsidies in 2024 can open new markets for specialty binders.

Regulatory stability in key regions

Consistency in EU, UK and US industrial policies underpins investment decisions; Horizon Europe carries a €95.5bn R&D budget (2021–27) while the UK RDEC rate is about 20%, directly affecting project returns. Political turnover can shift funding for green chemistry, altering expected IRRs on 5–10 year plant capex. Stable frameworks enable long-horizon capex and R&D; monitoring policy pipelines aligns product roadmaps early.

Industrial strategy and subsidies

Government grants for decarbonization and advanced materials lower project hurdles; global fiscal support such as the US Inflation Reduction Act allocates about $369bn for energy and climate over a decade and EU NextGenerationEU totals €806.9bn, shaping investment flows. Competing subsidy regimes and IPCEIs influence site selection and cost of capital. Public-private partnerships accelerate scale-up of sustainable polymers while transparent eligibility criteria guide portfolio prioritization.

Geopolitical supply risk

- Tags: supply-risk

- Tags: lead-times

- Tags: multi-source

- Tags: scenario-planning

Public procurement preferences

Green public purchasing favors low-VOC and bio-based dispersions, and EU public procurement is worth about €2 trillion annually, creating sizable demand for certified products; meeting EU Ecolabel/GPP criteria unlocks infrastructure and healthcare contracts often reserved for compliant suppliers. Policy-driven demand has accelerated premium product adoption, and early certification provides clear competitive differentiation for Synthomer.

- Tag: public-procurement

- Tag: low-VOC

- Tag: bio-based

- Tag: EU-ecolabel

- Tag: €2T-market

Tariff shocks, 80% Russian gas drop and green funding spur demand for low-VOC bio inputs

Shifts in tariffs (up to 25%) and trade tensions raise input costs and add lead times (+20–30 days); EU pipeline gas imports from Russia fell ~80% in 2022, tightening feedstock. Policy funding (Horizon €95.5bn, UK RDEC ~20%, IRA $369bn, NextGenerationEU €806.9bn) steers decarbonization capex. EU public procurement (€2T) boosts demand for low-VOC/bio-based products.

| Indicator | Value |

|---|---|

| Tariff cap | 25% |

| Russian gas fall | ~80% (2022) |

| Horizon | €95.5bn (2021–27) |

| IRA | $369bn |

| Public procurement | €2T |

What is included in the product

Explores how external macro-environmental factors uniquely affect Synthomer across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and region-specific trends. Designed for executives and investors, the analysis maps threats and opportunities, offers forward-looking scenarios, and is formatted for direct use in plans, decks, and reports.

A concise, visually segmented Synthomer PESTLE summary that eases stakeholder alignment, supports external risk discussions in planning sessions, and can be dropped into presentations or shared across teams for quick decision-making.

Economic factors

Cyclical end-market demand

Construction and coatings volumes for Synthomer closely follow GDP — IMF put global growth near 3.0% in 2024 — and housing starts (US ~1.5m annualised in 2024), so demand slowdowns compress plant utilization and margins. Broad end-market exposure (industrial, construction, adhesives) partially smooths cycles, while agile production planning and inventory cuts preserve cash during downturns.

Input cost volatility

Petrochemical feedstocks and energy track global markets—Brent crude averaged around $80–90/bbl in 2024–H1 2025, driving naphtha and gas cost swings that feed into Synthomer’s raw-material bills. Cost pass-through lags of roughly 2–3 months can compress realised margins and pressure EBITDA during rapid price moves. Hedging programmes and formula-linked customer pricing materially reduce exposure to spot spikes. Ongoing process-efficiency gains and yield improvements gradually offset margin erosion over time.

Currency fluctuations

Multi-currency revenues and costs expose Synthomer to translation and transaction risk across USD, EUR and other markets, affecting reported margins and cashflow. A stronger US dollar can erode export competitiveness from non-dollar plants and shift regional pricing dynamics. The group uses natural hedges in local sourcing and selective FX derivatives to stabilise earnings. Pricing governance is adjusted to align selling prices with material FX movements.

Interest rates and financing

Higher policy rates (~5% in major markets in 2024) raise borrowing costs for Synthomer’s capex and working capital, compressing margins and lengthening payback periods. A conservative debt structure and <1.5–2.5x net debt/EBITDA target improve flexibility through cycles; prioritising high-IRR, quick-payback projects protects returns while cash discipline enables opportunistic M&A or deleveraging.

- Higher rates ~5% (2024)

- Focus: high IRR, quick payback

- Target leverage: ~1.5–2.5x ND/EBITDA

- Cash discipline → M&A or deleveraging optionality

Customer consolidation

Larger coatings and adhesives customers raise bargaining power; top 10 global coatings firms account for around 45% of the market (2023), intensifying buyer leverage. Long-term contracts give volume visibility but compress pricing. Differentiated performance grades protect margins, while technical service and specification support secure repeat business.

- Customer consolidation: ↑ buyer leverage (~45% top-10 share)

- Contracts: volume visibility vs price squeeze

- Performance grades: margin defense

- Technical service: specification lock-in

Tariff shocks, 80% Russian gas drop and green funding spur demand for low-VOC bio inputs

Global GDP ~3.0% (IMF 2024) and US housing starts ~1.5m (2024) drive demand; cycles hit utilisation and margins. Brent ~$80–90/bbl (2024–H1 2025) and 5% policy rates (major markets, 2024) raise feedstock and financing costs. Top-10 coatings ~45% share (2023) increases buyer power; net debt/EBITDA target ~1.5–2.5x cushions risk.

| Metric | Value |

|---|---|

| Global GDP (2024) | ~3.0% |

| Brent (2024–H1 2025) | $80–90/bbl |

| US housing starts (2024) | ~1.5m |

| Policy rates (2024) | ~5% |

| Top-10 coatings (2023) | ~45% |

| ND/EBITDA target | 1.5–2.5x |

Preview the Actual Deliverable

Synthomer PESTLE Analysis

This Synthomer PESTLE Analysis examines political, economic, social, technological, legal and environmental factors shaping the company's operating environment. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content, structure and layout visible are the final file you'll download immediately after payment.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political shifts, regulatory pressure, economic cycles and environmental trends are influencing Synthomer’s strategy and risk profile in our concise PESTLE snapshot. Use these insights to refine forecasts, spot growth pockets, and stress-test assumptions. Ideal for investors, strategists, and advisors seeking clarity. Purchase the full PESTLE for the complete, actionable breakdown—ready to download now.

Political factors

Trade policies and tariffs

Shifts in tariffs on chemicals, such as US Section 301 measures of up to 25%, directly raise Synthomer’s input costs and compress margins, forcing pass-through pricing or margin erosion. Trade tensions between major blocs have already disrupted polymer supply chains, increasing lead times and spot prices. Proactive sourcing and regional diversification reduce exposure, while government export incentives and subsidies in 2024 can open new markets for specialty binders.

Regulatory stability in key regions

Consistency in EU, UK and US industrial policies underpins investment decisions; Horizon Europe carries a €95.5bn R&D budget (2021–27) while the UK RDEC rate is about 20%, directly affecting project returns. Political turnover can shift funding for green chemistry, altering expected IRRs on 5–10 year plant capex. Stable frameworks enable long-horizon capex and R&D; monitoring policy pipelines aligns product roadmaps early.

Industrial strategy and subsidies

Government grants for decarbonization and advanced materials lower project hurdles; global fiscal support such as the US Inflation Reduction Act allocates about $369bn for energy and climate over a decade and EU NextGenerationEU totals €806.9bn, shaping investment flows. Competing subsidy regimes and IPCEIs influence site selection and cost of capital. Public-private partnerships accelerate scale-up of sustainable polymers while transparent eligibility criteria guide portfolio prioritization.

Geopolitical supply risk

- Tags: supply-risk

- Tags: lead-times

- Tags: multi-source

- Tags: scenario-planning

Public procurement preferences

Green public purchasing favors low-VOC and bio-based dispersions, and EU public procurement is worth about €2 trillion annually, creating sizable demand for certified products; meeting EU Ecolabel/GPP criteria unlocks infrastructure and healthcare contracts often reserved for compliant suppliers. Policy-driven demand has accelerated premium product adoption, and early certification provides clear competitive differentiation for Synthomer.

- Tag: public-procurement

- Tag: low-VOC

- Tag: bio-based

- Tag: EU-ecolabel

- Tag: €2T-market

Tariff shocks, 80% Russian gas drop and green funding spur demand for low-VOC bio inputs

Shifts in tariffs (up to 25%) and trade tensions raise input costs and add lead times (+20–30 days); EU pipeline gas imports from Russia fell ~80% in 2022, tightening feedstock. Policy funding (Horizon €95.5bn, UK RDEC ~20%, IRA $369bn, NextGenerationEU €806.9bn) steers decarbonization capex. EU public procurement (€2T) boosts demand for low-VOC/bio-based products.

| Indicator | Value |

|---|---|

| Tariff cap | 25% |

| Russian gas fall | ~80% (2022) |

| Horizon | €95.5bn (2021–27) |

| IRA | $369bn |

| Public procurement | €2T |

What is included in the product

Explores how external macro-environmental factors uniquely affect Synthomer across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and region-specific trends. Designed for executives and investors, the analysis maps threats and opportunities, offers forward-looking scenarios, and is formatted for direct use in plans, decks, and reports.

A concise, visually segmented Synthomer PESTLE summary that eases stakeholder alignment, supports external risk discussions in planning sessions, and can be dropped into presentations or shared across teams for quick decision-making.

Economic factors

Cyclical end-market demand

Construction and coatings volumes for Synthomer closely follow GDP — IMF put global growth near 3.0% in 2024 — and housing starts (US ~1.5m annualised in 2024), so demand slowdowns compress plant utilization and margins. Broad end-market exposure (industrial, construction, adhesives) partially smooths cycles, while agile production planning and inventory cuts preserve cash during downturns.

Input cost volatility

Petrochemical feedstocks and energy track global markets—Brent crude averaged around $80–90/bbl in 2024–H1 2025, driving naphtha and gas cost swings that feed into Synthomer’s raw-material bills. Cost pass-through lags of roughly 2–3 months can compress realised margins and pressure EBITDA during rapid price moves. Hedging programmes and formula-linked customer pricing materially reduce exposure to spot spikes. Ongoing process-efficiency gains and yield improvements gradually offset margin erosion over time.

Currency fluctuations

Multi-currency revenues and costs expose Synthomer to translation and transaction risk across USD, EUR and other markets, affecting reported margins and cashflow. A stronger US dollar can erode export competitiveness from non-dollar plants and shift regional pricing dynamics. The group uses natural hedges in local sourcing and selective FX derivatives to stabilise earnings. Pricing governance is adjusted to align selling prices with material FX movements.

Interest rates and financing

Higher policy rates (~5% in major markets in 2024) raise borrowing costs for Synthomer’s capex and working capital, compressing margins and lengthening payback periods. A conservative debt structure and <1.5–2.5x net debt/EBITDA target improve flexibility through cycles; prioritising high-IRR, quick-payback projects protects returns while cash discipline enables opportunistic M&A or deleveraging.

- Higher rates ~5% (2024)

- Focus: high IRR, quick payback

- Target leverage: ~1.5–2.5x ND/EBITDA

- Cash discipline → M&A or deleveraging optionality

Customer consolidation

Larger coatings and adhesives customers raise bargaining power; top 10 global coatings firms account for around 45% of the market (2023), intensifying buyer leverage. Long-term contracts give volume visibility but compress pricing. Differentiated performance grades protect margins, while technical service and specification support secure repeat business.

- Customer consolidation: ↑ buyer leverage (~45% top-10 share)

- Contracts: volume visibility vs price squeeze

- Performance grades: margin defense

- Technical service: specification lock-in

Tariff shocks, 80% Russian gas drop and green funding spur demand for low-VOC bio inputs

Global GDP ~3.0% (IMF 2024) and US housing starts ~1.5m (2024) drive demand; cycles hit utilisation and margins. Brent ~$80–90/bbl (2024–H1 2025) and 5% policy rates (major markets, 2024) raise feedstock and financing costs. Top-10 coatings ~45% share (2023) increases buyer power; net debt/EBITDA target ~1.5–2.5x cushions risk.

| Metric | Value |

|---|---|

| Global GDP (2024) | ~3.0% |

| Brent (2024–H1 2025) | $80–90/bbl |

| US housing starts (2024) | ~1.5m |

| Policy rates (2024) | ~5% |

| Top-10 coatings (2023) | ~45% |

| ND/EBITDA target | 1.5–2.5x |

Preview the Actual Deliverable

Synthomer PESTLE Analysis

This Synthomer PESTLE Analysis examines political, economic, social, technological, legal and environmental factors shaping the company's operating environment. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content, structure and layout visible are the final file you'll download immediately after payment.