Shenzhen Sunway Communication PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our focused PESTLE Analysis of Shenzhen Sunway Communication—three to five concise insights reveal how political shifts, economic trends, social change, technological innovation, legal dynamics, and environmental pressures shape its outlook. Ideal for investors and strategists, the full report delivers actionable intelligence and ready-to-use charts; purchase now to access the complete analysis instantly.

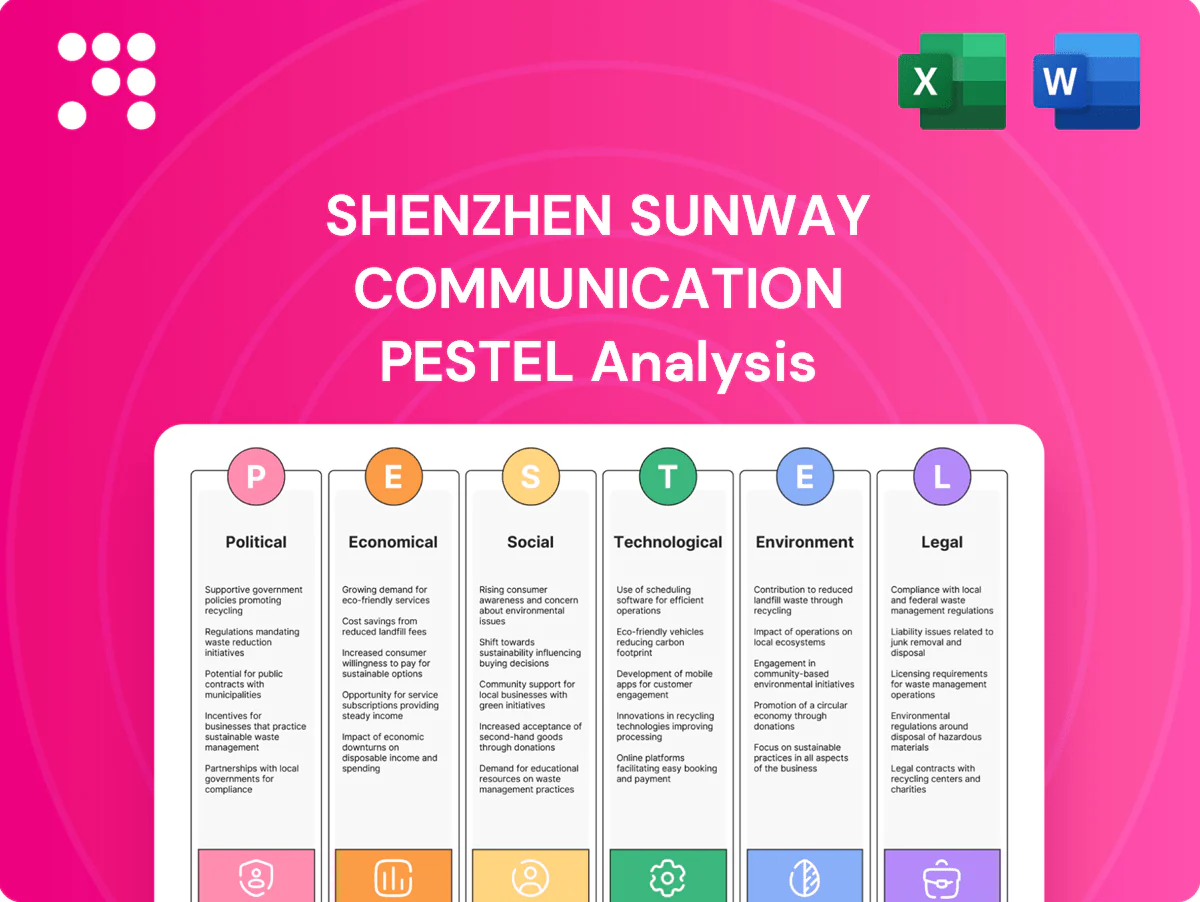

Political factors

US–China trade tensions and export controls

US–China trade tensions threaten Shenzhen Sunway as export controls on advanced semiconductors and RF components tightened in 2022–2024 and tariffs of up to 25% remain on many goods, while bilateral goods trade exceeded $700 billion in 2023. Restrictions and license requirements for certain RF modules and test equipment can limit market access and complicate shipments. Sunway must diversify markets and reconfigure supply chains to mitigate tariff and sanction risks. Active compliance programs and scenario planning help protect revenue continuity.

Industrial policy and subsidies in China

China’s industrial policy under the 14th Five-Year Plan (2021–2025) prioritizes 5G/6G, new energy vehicles and advanced manufacturing, directing central and local incentives that can support Shenzhen Sunway Communication’s capex and R&D. Participation in national standards projects (MIIT-led programs) can shape product roadmaps and market access. Accessing subsidies typically requires meeting localization and technology thresholds set by provincial programs. Rapid policy shifts can quickly redirect funding priorities.

Geopolitical localization of telecom infrastructure

By mid‑2024 over 30 governments had introduced vendor trust or localization policies affecting 5G procurement, pressuring antenna and RF content in base stations and small cells; Shenzhen Sunway may need local partnerships or manufacturing footprints to qualify, potentially adding capex and raising unit costs by an estimated 5–12% in targeted markets; alignment with local certification authorities is a gating factor for contract awards.

Customs, tariffs, and cross-border logistics

Variable tariffs on electronic parts (ranging by HS code from 0% to 25%) materially affect Shenzhen Sunway Communication price competitiveness, while customs delays—commonly adding 2–7 days for high-mix RF components—lengthen lead times and inventory costs. Strategically placed bonded warehouses and FTZ trade-zone usage around Shenzhen can cut clearance friction and financing needs, and proactive tariff classification and full documentation prevent penalties, rework, and shipment holds.

- tariff-range: 0%–25% by HS code

- typical-customs-delay: 2–7 days

- bonded-warehouses: reduce clearance friction & working capital

- classification-compliance: avoids fines and rework

Government spectrum and infrastructure rollouts

National spectrum allocations (eg 3.3–3.6 GHz C‑band for 5G) set antenna and RF design specs; China reported over 1 billion 5G subscribers by 2024, boosting demand for baseband and mmWave modules. Public investment and municipal pilots in 5G, Wi‑Fi offload and V2X (100+ city pilots by 2024) accelerate orders, while auction or rollout delays increase order volatility. Close liaison with carriers and OEMs aligns production cadence and reduces inventory risk.

- Spectrum drives RF design requirements

- Public 5G/V2X funding raises TAM

- Rollout delays = order volatility

- Liaison with carriers/OEMs aligns timing

US-China controls, 0-25%, 30+ local rules squeeze exports

US–China export controls (2022–24) and tariffs (0–25% by HS) threaten Sunway’s export markets and supply chains, while >30 countries imposed vendor-localization rules by 2024. China’s 14th FYP and MIIT incentives boost 5G/6G R&D and capex access; >1bn 5G subs by 2024 expands domestic demand. Customs delays (2–7 days) and spectrum allocations (3.3–3.6 GHz) directly shape production and certification timing.

| Metric | Value |

|---|---|

| Tariff range | 0%–25% |

| Customs delay | 2–7 days |

| 5G subs (China) | >1,000,000,000 (2024) |

| Vendor-localization | 30+ govts (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Shenzhen Sunway Communication, with data-driven trends and region-specific examples to identify risks and growth opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary of Shenzhen Sunway Communication that highlights regulatory, technological, economic and geopolitical risks for quick inclusion in presentations or team planning, editable for local context and easily shareable to align stakeholders during strategy sessions.

Economic factors

Smartphone and consumer electronics cycles

Handset unit volatility—global smartphone shipments ~1.1 billion in 2024—directly swings antenna and RF module volumes, with quarter-to-quarter drops of 5–15% common. Content per device rises as 5G handset share reached ~60% in 2024 and Wi‑Fi 7 adds modules, boosting BOM value roughly 15–25% per device. Inventory digestion in 2023–24 compressed orders and pressured pricing during destocking phases. Flexible capacity and diversified design wins help stabilize Sunway’s revenue streams.

Automotive electronics growth

ADAS, in-vehicle connectivity and EV platforms are driving RF and antenna content higher—average antenna count is rising from ~2 toward 5–6 per vehicle by 2025, significantly raising per-vehicle RF billings. Longer automotive qualification cycles (often 18–36 months) smooth demand but delay volume ramps. Pricing discipline increases under multi-year OEM agreements, while IATF and PPAP compliance unlocks entry to higher-margin programs.

Input costs and FX fluctuations

Input-cost swings—LME copper ~9,500 USD/t and gold ~2,300 USD/oz in mid‑2025, plus volatile ceramics and polymer prices—directly squeeze Sunway’s margins. Yuan around 7.15 per USD and EUR/USD ≈1.08 in mid‑2025 shifts export competitiveness and component import bills. Active FX hedging, multi‑sourcing, design‑for‑manufacturing and material substitution are used to blunt shocks and protect gross margins by several percentage points.

Capex cycles in telecom infrastructure

Carrier spending on 5G/6G—with global 5G subscriptions at ~1.7 billion end-2024—directly drives demand for base station and small-cell components; carrier capex lulls depress infrastructure sales but often redirect spend to private networks and edge deployments. Enterprise Wi‑Fi upgrades (enterprise WLAN market ~$12bn in 2024) produce ancillary pull-through for modules and antennas; aligning Sunway product roadmaps with carrier upgrade cycles cushions cyclicality and stabilizes revenue.

- 5G/6G carrier capex → base station & small-cell demand

- Capex lulls shift spend to private networks

- Enterprise Wi‑Fi upgrades = ancillary pull-through

- Product-roadmap alignment reduces revenue cyclicality

Customer concentration and ASP pressure

Tier-1 OEMs (top five captured ~70% of global smartphone shipments in 2024) exert strong bargaining power that compresses ASPs; multi‑platform design‑ins secure volume but raise dependency when top customers drive >50% of order cycles. Offering value‑added testing and co‑design services has preserved premium ASPs for peers, while diversifying into auto, IoT and enterprise verticals reduces single‑customer exposure.

- OEM concentration ~70% (top 5, 2024)

- Design‑ins = volume vs dependency

- Testing/co‑design defend ASPs

- Vertical diversification cuts single‑customer risk

US-China controls, 0-25%, 30+ local rules squeeze exports

Smartphone shipments ~1.1B (2024) and 5G handset share ~60% raise RF/BOM value 15–25%, while automotive antenna count rises toward 5–6/vehicle by 2025, lengthening qualification but boosting ASPs. Input costs (copper ~9,500 USD/t; gold ~2,300 USD/oz) and FX (CNY ~7.15/USD) pressure margins. Carrier capex and 1.7B 5G subs (end‑2024) drive base‑station and private network demand; top‑5 OEMs ~70% share concentrate pricing power.

| Metric | Value |

|---|---|

| Smartphones (2024) | ~1.1B |

| 5G share | ~60% |

| 5G subs | ~1.7B |

| Copper | ~9,500 USD/t |

Preview Before You Purchase

Shenzhen Sunway Communication PESTLE Analysis

The preview shown here is the exact Shenzhen Sunway Communication PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real file you’re buying, delivered exactly as displayed with no placeholders. The layout, content, and structure are final and downloadable immediately after payment.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our focused PESTLE Analysis of Shenzhen Sunway Communication—three to five concise insights reveal how political shifts, economic trends, social change, technological innovation, legal dynamics, and environmental pressures shape its outlook. Ideal for investors and strategists, the full report delivers actionable intelligence and ready-to-use charts; purchase now to access the complete analysis instantly.

Political factors

US–China trade tensions and export controls

US–China trade tensions threaten Shenzhen Sunway as export controls on advanced semiconductors and RF components tightened in 2022–2024 and tariffs of up to 25% remain on many goods, while bilateral goods trade exceeded $700 billion in 2023. Restrictions and license requirements for certain RF modules and test equipment can limit market access and complicate shipments. Sunway must diversify markets and reconfigure supply chains to mitigate tariff and sanction risks. Active compliance programs and scenario planning help protect revenue continuity.

Industrial policy and subsidies in China

China’s industrial policy under the 14th Five-Year Plan (2021–2025) prioritizes 5G/6G, new energy vehicles and advanced manufacturing, directing central and local incentives that can support Shenzhen Sunway Communication’s capex and R&D. Participation in national standards projects (MIIT-led programs) can shape product roadmaps and market access. Accessing subsidies typically requires meeting localization and technology thresholds set by provincial programs. Rapid policy shifts can quickly redirect funding priorities.

Geopolitical localization of telecom infrastructure

By mid‑2024 over 30 governments had introduced vendor trust or localization policies affecting 5G procurement, pressuring antenna and RF content in base stations and small cells; Shenzhen Sunway may need local partnerships or manufacturing footprints to qualify, potentially adding capex and raising unit costs by an estimated 5–12% in targeted markets; alignment with local certification authorities is a gating factor for contract awards.

Customs, tariffs, and cross-border logistics

Variable tariffs on electronic parts (ranging by HS code from 0% to 25%) materially affect Shenzhen Sunway Communication price competitiveness, while customs delays—commonly adding 2–7 days for high-mix RF components—lengthen lead times and inventory costs. Strategically placed bonded warehouses and FTZ trade-zone usage around Shenzhen can cut clearance friction and financing needs, and proactive tariff classification and full documentation prevent penalties, rework, and shipment holds.

- tariff-range: 0%–25% by HS code

- typical-customs-delay: 2–7 days

- bonded-warehouses: reduce clearance friction & working capital

- classification-compliance: avoids fines and rework

Government spectrum and infrastructure rollouts

National spectrum allocations (eg 3.3–3.6 GHz C‑band for 5G) set antenna and RF design specs; China reported over 1 billion 5G subscribers by 2024, boosting demand for baseband and mmWave modules. Public investment and municipal pilots in 5G, Wi‑Fi offload and V2X (100+ city pilots by 2024) accelerate orders, while auction or rollout delays increase order volatility. Close liaison with carriers and OEMs aligns production cadence and reduces inventory risk.

- Spectrum drives RF design requirements

- Public 5G/V2X funding raises TAM

- Rollout delays = order volatility

- Liaison with carriers/OEMs aligns timing

US-China controls, 0-25%, 30+ local rules squeeze exports

US–China export controls (2022–24) and tariffs (0–25% by HS) threaten Sunway’s export markets and supply chains, while >30 countries imposed vendor-localization rules by 2024. China’s 14th FYP and MIIT incentives boost 5G/6G R&D and capex access; >1bn 5G subs by 2024 expands domestic demand. Customs delays (2–7 days) and spectrum allocations (3.3–3.6 GHz) directly shape production and certification timing.

| Metric | Value |

|---|---|

| Tariff range | 0%–25% |

| Customs delay | 2–7 days |

| 5G subs (China) | >1,000,000,000 (2024) |

| Vendor-localization | 30+ govts (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Shenzhen Sunway Communication, with data-driven trends and region-specific examples to identify risks and growth opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary of Shenzhen Sunway Communication that highlights regulatory, technological, economic and geopolitical risks for quick inclusion in presentations or team planning, editable for local context and easily shareable to align stakeholders during strategy sessions.

Economic factors

Smartphone and consumer electronics cycles

Handset unit volatility—global smartphone shipments ~1.1 billion in 2024—directly swings antenna and RF module volumes, with quarter-to-quarter drops of 5–15% common. Content per device rises as 5G handset share reached ~60% in 2024 and Wi‑Fi 7 adds modules, boosting BOM value roughly 15–25% per device. Inventory digestion in 2023–24 compressed orders and pressured pricing during destocking phases. Flexible capacity and diversified design wins help stabilize Sunway’s revenue streams.

Automotive electronics growth

ADAS, in-vehicle connectivity and EV platforms are driving RF and antenna content higher—average antenna count is rising from ~2 toward 5–6 per vehicle by 2025, significantly raising per-vehicle RF billings. Longer automotive qualification cycles (often 18–36 months) smooth demand but delay volume ramps. Pricing discipline increases under multi-year OEM agreements, while IATF and PPAP compliance unlocks entry to higher-margin programs.

Input costs and FX fluctuations

Input-cost swings—LME copper ~9,500 USD/t and gold ~2,300 USD/oz in mid‑2025, plus volatile ceramics and polymer prices—directly squeeze Sunway’s margins. Yuan around 7.15 per USD and EUR/USD ≈1.08 in mid‑2025 shifts export competitiveness and component import bills. Active FX hedging, multi‑sourcing, design‑for‑manufacturing and material substitution are used to blunt shocks and protect gross margins by several percentage points.

Capex cycles in telecom infrastructure

Carrier spending on 5G/6G—with global 5G subscriptions at ~1.7 billion end-2024—directly drives demand for base station and small-cell components; carrier capex lulls depress infrastructure sales but often redirect spend to private networks and edge deployments. Enterprise Wi‑Fi upgrades (enterprise WLAN market ~$12bn in 2024) produce ancillary pull-through for modules and antennas; aligning Sunway product roadmaps with carrier upgrade cycles cushions cyclicality and stabilizes revenue.

- 5G/6G carrier capex → base station & small-cell demand

- Capex lulls shift spend to private networks

- Enterprise Wi‑Fi upgrades = ancillary pull-through

- Product-roadmap alignment reduces revenue cyclicality

Customer concentration and ASP pressure

Tier-1 OEMs (top five captured ~70% of global smartphone shipments in 2024) exert strong bargaining power that compresses ASPs; multi‑platform design‑ins secure volume but raise dependency when top customers drive >50% of order cycles. Offering value‑added testing and co‑design services has preserved premium ASPs for peers, while diversifying into auto, IoT and enterprise verticals reduces single‑customer exposure.

- OEM concentration ~70% (top 5, 2024)

- Design‑ins = volume vs dependency

- Testing/co‑design defend ASPs

- Vertical diversification cuts single‑customer risk

US-China controls, 0-25%, 30+ local rules squeeze exports

Smartphone shipments ~1.1B (2024) and 5G handset share ~60% raise RF/BOM value 15–25%, while automotive antenna count rises toward 5–6/vehicle by 2025, lengthening qualification but boosting ASPs. Input costs (copper ~9,500 USD/t; gold ~2,300 USD/oz) and FX (CNY ~7.15/USD) pressure margins. Carrier capex and 1.7B 5G subs (end‑2024) drive base‑station and private network demand; top‑5 OEMs ~70% share concentrate pricing power.

| Metric | Value |

|---|---|

| Smartphones (2024) | ~1.1B |

| 5G share | ~60% |

| 5G subs | ~1.7B |

| Copper | ~9,500 USD/t |

Preview Before You Purchase

Shenzhen Sunway Communication PESTLE Analysis

The preview shown here is the exact Shenzhen Sunway Communication PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real file you’re buying, delivered exactly as displayed with no placeholders. The layout, content, and structure are final and downloadable immediately after payment.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our focused PESTLE Analysis of Shenzhen Sunway Communication—three to five concise insights reveal how political shifts, economic trends, social change, technological innovation, legal dynamics, and environmental pressures shape its outlook. Ideal for investors and strategists, the full report delivers actionable intelligence and ready-to-use charts; purchase now to access the complete analysis instantly.

Political factors

US–China trade tensions and export controls

US–China trade tensions threaten Shenzhen Sunway as export controls on advanced semiconductors and RF components tightened in 2022–2024 and tariffs of up to 25% remain on many goods, while bilateral goods trade exceeded $700 billion in 2023. Restrictions and license requirements for certain RF modules and test equipment can limit market access and complicate shipments. Sunway must diversify markets and reconfigure supply chains to mitigate tariff and sanction risks. Active compliance programs and scenario planning help protect revenue continuity.

Industrial policy and subsidies in China

China’s industrial policy under the 14th Five-Year Plan (2021–2025) prioritizes 5G/6G, new energy vehicles and advanced manufacturing, directing central and local incentives that can support Shenzhen Sunway Communication’s capex and R&D. Participation in national standards projects (MIIT-led programs) can shape product roadmaps and market access. Accessing subsidies typically requires meeting localization and technology thresholds set by provincial programs. Rapid policy shifts can quickly redirect funding priorities.

Geopolitical localization of telecom infrastructure

By mid‑2024 over 30 governments had introduced vendor trust or localization policies affecting 5G procurement, pressuring antenna and RF content in base stations and small cells; Shenzhen Sunway may need local partnerships or manufacturing footprints to qualify, potentially adding capex and raising unit costs by an estimated 5–12% in targeted markets; alignment with local certification authorities is a gating factor for contract awards.

Customs, tariffs, and cross-border logistics

Variable tariffs on electronic parts (ranging by HS code from 0% to 25%) materially affect Shenzhen Sunway Communication price competitiveness, while customs delays—commonly adding 2–7 days for high-mix RF components—lengthen lead times and inventory costs. Strategically placed bonded warehouses and FTZ trade-zone usage around Shenzhen can cut clearance friction and financing needs, and proactive tariff classification and full documentation prevent penalties, rework, and shipment holds.

- tariff-range: 0%–25% by HS code

- typical-customs-delay: 2–7 days

- bonded-warehouses: reduce clearance friction & working capital

- classification-compliance: avoids fines and rework

Government spectrum and infrastructure rollouts

National spectrum allocations (eg 3.3–3.6 GHz C‑band for 5G) set antenna and RF design specs; China reported over 1 billion 5G subscribers by 2024, boosting demand for baseband and mmWave modules. Public investment and municipal pilots in 5G, Wi‑Fi offload and V2X (100+ city pilots by 2024) accelerate orders, while auction or rollout delays increase order volatility. Close liaison with carriers and OEMs aligns production cadence and reduces inventory risk.

- Spectrum drives RF design requirements

- Public 5G/V2X funding raises TAM

- Rollout delays = order volatility

- Liaison with carriers/OEMs aligns timing

US-China controls, 0-25%, 30+ local rules squeeze exports

US–China export controls (2022–24) and tariffs (0–25% by HS) threaten Sunway’s export markets and supply chains, while >30 countries imposed vendor-localization rules by 2024. China’s 14th FYP and MIIT incentives boost 5G/6G R&D and capex access; >1bn 5G subs by 2024 expands domestic demand. Customs delays (2–7 days) and spectrum allocations (3.3–3.6 GHz) directly shape production and certification timing.

| Metric | Value |

|---|---|

| Tariff range | 0%–25% |

| Customs delay | 2–7 days |

| 5G subs (China) | >1,000,000,000 (2024) |

| Vendor-localization | 30+ govts (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Shenzhen Sunway Communication, with data-driven trends and region-specific examples to identify risks and growth opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary of Shenzhen Sunway Communication that highlights regulatory, technological, economic and geopolitical risks for quick inclusion in presentations or team planning, editable for local context and easily shareable to align stakeholders during strategy sessions.

Economic factors

Smartphone and consumer electronics cycles

Handset unit volatility—global smartphone shipments ~1.1 billion in 2024—directly swings antenna and RF module volumes, with quarter-to-quarter drops of 5–15% common. Content per device rises as 5G handset share reached ~60% in 2024 and Wi‑Fi 7 adds modules, boosting BOM value roughly 15–25% per device. Inventory digestion in 2023–24 compressed orders and pressured pricing during destocking phases. Flexible capacity and diversified design wins help stabilize Sunway’s revenue streams.

Automotive electronics growth

ADAS, in-vehicle connectivity and EV platforms are driving RF and antenna content higher—average antenna count is rising from ~2 toward 5–6 per vehicle by 2025, significantly raising per-vehicle RF billings. Longer automotive qualification cycles (often 18–36 months) smooth demand but delay volume ramps. Pricing discipline increases under multi-year OEM agreements, while IATF and PPAP compliance unlocks entry to higher-margin programs.

Input costs and FX fluctuations

Input-cost swings—LME copper ~9,500 USD/t and gold ~2,300 USD/oz in mid‑2025, plus volatile ceramics and polymer prices—directly squeeze Sunway’s margins. Yuan around 7.15 per USD and EUR/USD ≈1.08 in mid‑2025 shifts export competitiveness and component import bills. Active FX hedging, multi‑sourcing, design‑for‑manufacturing and material substitution are used to blunt shocks and protect gross margins by several percentage points.

Capex cycles in telecom infrastructure

Carrier spending on 5G/6G—with global 5G subscriptions at ~1.7 billion end-2024—directly drives demand for base station and small-cell components; carrier capex lulls depress infrastructure sales but often redirect spend to private networks and edge deployments. Enterprise Wi‑Fi upgrades (enterprise WLAN market ~$12bn in 2024) produce ancillary pull-through for modules and antennas; aligning Sunway product roadmaps with carrier upgrade cycles cushions cyclicality and stabilizes revenue.

- 5G/6G carrier capex → base station & small-cell demand

- Capex lulls shift spend to private networks

- Enterprise Wi‑Fi upgrades = ancillary pull-through

- Product-roadmap alignment reduces revenue cyclicality

Customer concentration and ASP pressure

Tier-1 OEMs (top five captured ~70% of global smartphone shipments in 2024) exert strong bargaining power that compresses ASPs; multi‑platform design‑ins secure volume but raise dependency when top customers drive >50% of order cycles. Offering value‑added testing and co‑design services has preserved premium ASPs for peers, while diversifying into auto, IoT and enterprise verticals reduces single‑customer exposure.

- OEM concentration ~70% (top 5, 2024)

- Design‑ins = volume vs dependency

- Testing/co‑design defend ASPs

- Vertical diversification cuts single‑customer risk

US-China controls, 0-25%, 30+ local rules squeeze exports

Smartphone shipments ~1.1B (2024) and 5G handset share ~60% raise RF/BOM value 15–25%, while automotive antenna count rises toward 5–6/vehicle by 2025, lengthening qualification but boosting ASPs. Input costs (copper ~9,500 USD/t; gold ~2,300 USD/oz) and FX (CNY ~7.15/USD) pressure margins. Carrier capex and 1.7B 5G subs (end‑2024) drive base‑station and private network demand; top‑5 OEMs ~70% share concentrate pricing power.

| Metric | Value |

|---|---|

| Smartphones (2024) | ~1.1B |

| 5G share | ~60% |

| 5G subs | ~1.7B |

| Copper | ~9,500 USD/t |

Preview Before You Purchase

Shenzhen Sunway Communication PESTLE Analysis

The preview shown here is the exact Shenzhen Sunway Communication PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real file you’re buying, delivered exactly as displayed with no placeholders. The layout, content, and structure are final and downloadable immediately after payment.