Tabcorp Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Tabcorp’s Porter's Five Forces snapshot highlights intense competitive rivalry, regulated barriers to entry, and evolving substitute threats from digital gaming, while buyer and supplier power remain moderate; strategic positioning and risk levers are clearer at a glance. This brief teases key dynamics—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy tailored to Tabcorp.

Suppliers Bargaining Power

Racing content rights

Australian racing content rights are controlled by three major codes—thoroughbred, harness and greyhound—whose clubs gate race fields, broadcast and wagering access; long-duration contracts commonly exceed five years, concentrating supplier leverage. Consolidation of rights holders and exclusive premium-meet rights enable multi‑million‑dollar fee extraction and limit operator flexibility. Tabcorp’s Sky Racing vertically integrates broadcast capabilities to mitigate exposure but remains dependent on external codes for core content.

Sports data and integrity feeds

Official sports data and integrity feeds are dominated by a small set of accredited vendors — notably Sportradar, Genius Sports and Stats Perform — giving roughly three providers most league partnerships and pricing power.

Exclusive league arrangements and limited vendor count lift fees and reduce switching options, while sub-second latency and high reliability requirements increase dependence on top-tier suppliers.

Multi-year contracts are common, providing revenue certainty for suppliers but locking Tabcorp into fixed cost structures and renewal price risk.

Venue partners and retail footprint

Pubs, clubs and agencies supply the bulk of TAB and Sky Racing retail distribution, with Tabcorp reporting a retail network of c.5,000 outlets in FY2024 and group revenue of about A$3.7bn that year, making venue access critical. Prime venue screens are scarce and secured through negotiated commissions, fit-outs and media fees, while competing bookmakers routinely bid for visibility, increasing supplier leverage. Long-term site agreements lower churn but lock Tabcorp into revenue-sharing obligations that compress margins.

Technology platforms and payments

Technology platforms — betting engines, risk tools, cloud and payment gateways — are mission critical for Tabcorp; 99.95–99.99% availability SLAs, PCI DSS and AML controls concentrate vendor choice and raise supplier bargaining power, while certification and migration costs create high switching barriers.

- High-availability SLAs: 99.95–99.99%

- Compliance: PCI DSS, AML, ISO 27001

- Switching barriers: certification + migration risk

- Cost mitigation: volume discounts, redundancy contracts

Broadcast production and satellite capacity

Outside broadcast crews, satellite capacity and CDN providers are critical to Sky Racing distribution and wield pricing power, especially for premium race times and specialist OB teams; outages historically cause immediate revenue loss and brand damage. In 2024 the global CDN market was ~USD30bn, underscoring supplier scale, while Tabcorp’s partial in‑house production and multi‑provider sourcing moderate that clout.

- High supplier clout: premium timeslot capacity

- Operational risk: outages → immediate revenue loss

- Mitigation: multi‑provider mix + in‑house capabilities

High supplier power: racing codes, data vendors and retail scale lock in customers

Supplier power is high: three racing codes and three major data vendors concentrate rights and feeds, enabling multi‑year (>5y) contracts and fee escalation. Tabcorp’s retail reliance (c.5,000 outlets, group revenue A$3.7bn FY2024) and 99.95–99.99% tech SLAs raise switching costs. CDN market scale (~USD30bn 2024) and premium OB capacity further amplify supplier leverage.

| Supplier | Concentration | Key metric |

|---|---|---|

| Racing codes | High (3) | Contracts >5y |

| Data vendors | High (≈3) | Latency/reliability |

| Retail venues | Moderate | 5,000 outlets (FY2024) |

What is included in the product

Concise Porter's Five Forces analysis of Tabcorp identifying competitive rivalry, buyer/supplier power, threats from new entrants and substitutes, plus regulatory and technological disruptors to its wagering and entertainment markets.

Concise Porter's Five Forces for Tabcorp that maps regulatory, competitor, supplier and tech pressures into a single-sheet view—ideal for fast strategic decisions, board decks, and scenario comparison without complex setup.

Customers Bargaining Power

Multi-homing bettors

As of 2024 multi-homing is widespread: punters commonly hold accounts with Sportsbet, Ladbrokes, bet365 and TAB, raising buyer power and price sensitivity. Low switching costs driven by frequent price boosts and promotions make customers nimble and margin-sensitive. Loyalty programs and omnichannel features (retail+digital) are deployed to damp churn but have limited power against aggressive short-term offers.

Price and promo sensitivity

Customers exert strong bargaining power as odds competitiveness, bonus bets and same-game multis drive rapid acquisition; apps and odds aggregators allow buyers to compare offers instantly. Regulatory curbs on inducements in some states moderate deal-seeking but do not eliminate it. Sustained promo wars compress operator margins and elevate buyer leverage, forcing continuous spend to defend market share.

Omnichannel expectations

Customers demand seamless app, web and retail experiences with fast in-play; in 2024 mobile channels accounted for over 70% of Australian wagering traffic, raising expectations. Friction in IDV, payments or bet settlement triggers immediate switching and higher churn. Superior UX reduces perceived buyer power by increasing stickiness, while lagging digital features amplify customer bargaining leverage.

Venue and corporate clients

Venue and corporate clients wield strong leverage over Tabcorp, negotiating commissions, screen rights and exclusivity for TAB terminals and Sky content; in FY2024 Tabcorp reported group revenue of about AUD 4.2bn, making these deals material to margins. Rival bookmakers and digital media alternatives raised venue bargaining power in 2024, while large venue groups extract multi-site bundles for lower fees. Performance-linked remuneration partially aligns incentives but concedes margin, shifting risk to Tabcorp.

- venues: commission, screen rights, exclusivity

- rivals/media: increase alternatives

- large groups: bundle leverage

- pay-for-performance: aligns but reduces margin

Keno players’ alternatives

Keno appeals to casual retail players with low stakes and rapid draws, but close substitutes such as EGMs and lotteries keep customers highly price- and payout-sensitive, limiting Tabcorp’s buyer leverage.

- Minimal switching costs at venue level

- Progressive jackpots and variants lower perceived buyer power

- Casual play drives volume, not loyalty

Mobile bettors (>70%) promos spur churn; venue deals sway margins

Customers hold multiple bookmaker accounts, driving high price sensitivity and low switching costs; omnichannel loyalty partially reduces churn but cannot match short-term promos. Mobile accounted for over 70% of wagering traffic in 2024, raising UX expectations and rapid switching on friction. Tabcorp’s FY2024 group revenue ~AUD 4.2bn makes venue and corporate client deals materially influential on margins.

| Metric | 2024 |

|---|---|

| Mobile share | >70% |

| Tabcorp revenue | AUD 4.2bn |

| Customer behavior | Multi-homing, promo-driven |

What You See Is What You Get

Tabcorp Porter's Five Forces Analysis

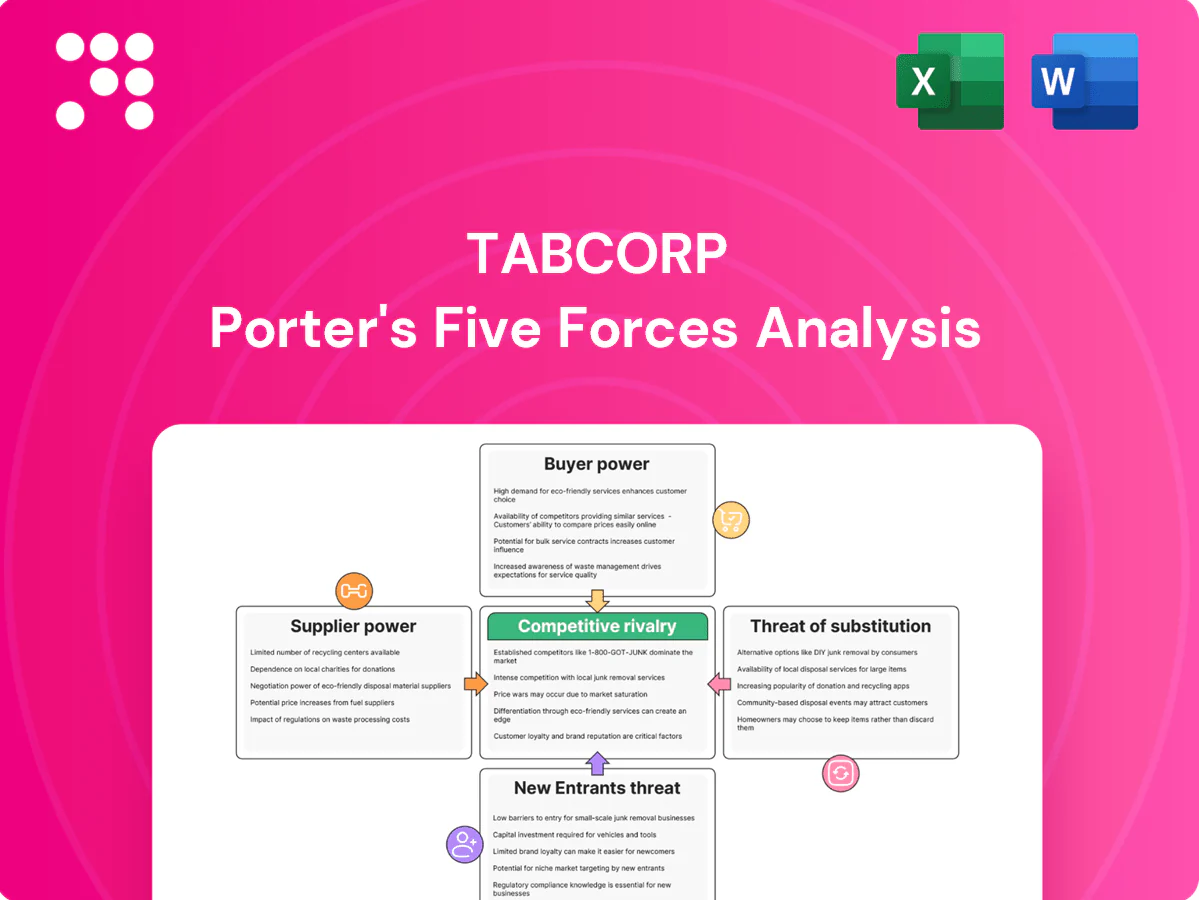

This preview shows the Tabcorp Porter’s Five Forces Analysis in full; what you see is the exact, professionally formatted document you'll receive immediately after purchase. It covers competitive rivalry, supplier and buyer power, and the threats of entry and substitutes. No placeholders or mockups—ready for instant download and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Tabcorp’s Porter's Five Forces snapshot highlights intense competitive rivalry, regulated barriers to entry, and evolving substitute threats from digital gaming, while buyer and supplier power remain moderate; strategic positioning and risk levers are clearer at a glance. This brief teases key dynamics—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy tailored to Tabcorp.

Suppliers Bargaining Power

Racing content rights

Australian racing content rights are controlled by three major codes—thoroughbred, harness and greyhound—whose clubs gate race fields, broadcast and wagering access; long-duration contracts commonly exceed five years, concentrating supplier leverage. Consolidation of rights holders and exclusive premium-meet rights enable multi‑million‑dollar fee extraction and limit operator flexibility. Tabcorp’s Sky Racing vertically integrates broadcast capabilities to mitigate exposure but remains dependent on external codes for core content.

Sports data and integrity feeds

Official sports data and integrity feeds are dominated by a small set of accredited vendors — notably Sportradar, Genius Sports and Stats Perform — giving roughly three providers most league partnerships and pricing power.

Exclusive league arrangements and limited vendor count lift fees and reduce switching options, while sub-second latency and high reliability requirements increase dependence on top-tier suppliers.

Multi-year contracts are common, providing revenue certainty for suppliers but locking Tabcorp into fixed cost structures and renewal price risk.

Venue partners and retail footprint

Pubs, clubs and agencies supply the bulk of TAB and Sky Racing retail distribution, with Tabcorp reporting a retail network of c.5,000 outlets in FY2024 and group revenue of about A$3.7bn that year, making venue access critical. Prime venue screens are scarce and secured through negotiated commissions, fit-outs and media fees, while competing bookmakers routinely bid for visibility, increasing supplier leverage. Long-term site agreements lower churn but lock Tabcorp into revenue-sharing obligations that compress margins.

Technology platforms and payments

Technology platforms — betting engines, risk tools, cloud and payment gateways — are mission critical for Tabcorp; 99.95–99.99% availability SLAs, PCI DSS and AML controls concentrate vendor choice and raise supplier bargaining power, while certification and migration costs create high switching barriers.

- High-availability SLAs: 99.95–99.99%

- Compliance: PCI DSS, AML, ISO 27001

- Switching barriers: certification + migration risk

- Cost mitigation: volume discounts, redundancy contracts

Broadcast production and satellite capacity

Outside broadcast crews, satellite capacity and CDN providers are critical to Sky Racing distribution and wield pricing power, especially for premium race times and specialist OB teams; outages historically cause immediate revenue loss and brand damage. In 2024 the global CDN market was ~USD30bn, underscoring supplier scale, while Tabcorp’s partial in‑house production and multi‑provider sourcing moderate that clout.

- High supplier clout: premium timeslot capacity

- Operational risk: outages → immediate revenue loss

- Mitigation: multi‑provider mix + in‑house capabilities

High supplier power: racing codes, data vendors and retail scale lock in customers

Supplier power is high: three racing codes and three major data vendors concentrate rights and feeds, enabling multi‑year (>5y) contracts and fee escalation. Tabcorp’s retail reliance (c.5,000 outlets, group revenue A$3.7bn FY2024) and 99.95–99.99% tech SLAs raise switching costs. CDN market scale (~USD30bn 2024) and premium OB capacity further amplify supplier leverage.

| Supplier | Concentration | Key metric |

|---|---|---|

| Racing codes | High (3) | Contracts >5y |

| Data vendors | High (≈3) | Latency/reliability |

| Retail venues | Moderate | 5,000 outlets (FY2024) |

What is included in the product

Concise Porter's Five Forces analysis of Tabcorp identifying competitive rivalry, buyer/supplier power, threats from new entrants and substitutes, plus regulatory and technological disruptors to its wagering and entertainment markets.

Concise Porter's Five Forces for Tabcorp that maps regulatory, competitor, supplier and tech pressures into a single-sheet view—ideal for fast strategic decisions, board decks, and scenario comparison without complex setup.

Customers Bargaining Power

Multi-homing bettors

As of 2024 multi-homing is widespread: punters commonly hold accounts with Sportsbet, Ladbrokes, bet365 and TAB, raising buyer power and price sensitivity. Low switching costs driven by frequent price boosts and promotions make customers nimble and margin-sensitive. Loyalty programs and omnichannel features (retail+digital) are deployed to damp churn but have limited power against aggressive short-term offers.

Price and promo sensitivity

Customers exert strong bargaining power as odds competitiveness, bonus bets and same-game multis drive rapid acquisition; apps and odds aggregators allow buyers to compare offers instantly. Regulatory curbs on inducements in some states moderate deal-seeking but do not eliminate it. Sustained promo wars compress operator margins and elevate buyer leverage, forcing continuous spend to defend market share.

Omnichannel expectations

Customers demand seamless app, web and retail experiences with fast in-play; in 2024 mobile channels accounted for over 70% of Australian wagering traffic, raising expectations. Friction in IDV, payments or bet settlement triggers immediate switching and higher churn. Superior UX reduces perceived buyer power by increasing stickiness, while lagging digital features amplify customer bargaining leverage.

Venue and corporate clients

Venue and corporate clients wield strong leverage over Tabcorp, negotiating commissions, screen rights and exclusivity for TAB terminals and Sky content; in FY2024 Tabcorp reported group revenue of about AUD 4.2bn, making these deals material to margins. Rival bookmakers and digital media alternatives raised venue bargaining power in 2024, while large venue groups extract multi-site bundles for lower fees. Performance-linked remuneration partially aligns incentives but concedes margin, shifting risk to Tabcorp.

- venues: commission, screen rights, exclusivity

- rivals/media: increase alternatives

- large groups: bundle leverage

- pay-for-performance: aligns but reduces margin

Keno players’ alternatives

Keno appeals to casual retail players with low stakes and rapid draws, but close substitutes such as EGMs and lotteries keep customers highly price- and payout-sensitive, limiting Tabcorp’s buyer leverage.

- Minimal switching costs at venue level

- Progressive jackpots and variants lower perceived buyer power

- Casual play drives volume, not loyalty

Mobile bettors (>70%) promos spur churn; venue deals sway margins

Customers hold multiple bookmaker accounts, driving high price sensitivity and low switching costs; omnichannel loyalty partially reduces churn but cannot match short-term promos. Mobile accounted for over 70% of wagering traffic in 2024, raising UX expectations and rapid switching on friction. Tabcorp’s FY2024 group revenue ~AUD 4.2bn makes venue and corporate client deals materially influential on margins.

| Metric | 2024 |

|---|---|

| Mobile share | >70% |

| Tabcorp revenue | AUD 4.2bn |

| Customer behavior | Multi-homing, promo-driven |

What You See Is What You Get

Tabcorp Porter's Five Forces Analysis

This preview shows the Tabcorp Porter’s Five Forces Analysis in full; what you see is the exact, professionally formatted document you'll receive immediately after purchase. It covers competitive rivalry, supplier and buyer power, and the threats of entry and substitutes. No placeholders or mockups—ready for instant download and use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Tabcorp’s Porter's Five Forces snapshot highlights intense competitive rivalry, regulated barriers to entry, and evolving substitute threats from digital gaming, while buyer and supplier power remain moderate; strategic positioning and risk levers are clearer at a glance. This brief teases key dynamics—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy tailored to Tabcorp.

Suppliers Bargaining Power

Racing content rights

Australian racing content rights are controlled by three major codes—thoroughbred, harness and greyhound—whose clubs gate race fields, broadcast and wagering access; long-duration contracts commonly exceed five years, concentrating supplier leverage. Consolidation of rights holders and exclusive premium-meet rights enable multi‑million‑dollar fee extraction and limit operator flexibility. Tabcorp’s Sky Racing vertically integrates broadcast capabilities to mitigate exposure but remains dependent on external codes for core content.

Sports data and integrity feeds

Official sports data and integrity feeds are dominated by a small set of accredited vendors — notably Sportradar, Genius Sports and Stats Perform — giving roughly three providers most league partnerships and pricing power.

Exclusive league arrangements and limited vendor count lift fees and reduce switching options, while sub-second latency and high reliability requirements increase dependence on top-tier suppliers.

Multi-year contracts are common, providing revenue certainty for suppliers but locking Tabcorp into fixed cost structures and renewal price risk.

Venue partners and retail footprint

Pubs, clubs and agencies supply the bulk of TAB and Sky Racing retail distribution, with Tabcorp reporting a retail network of c.5,000 outlets in FY2024 and group revenue of about A$3.7bn that year, making venue access critical. Prime venue screens are scarce and secured through negotiated commissions, fit-outs and media fees, while competing bookmakers routinely bid for visibility, increasing supplier leverage. Long-term site agreements lower churn but lock Tabcorp into revenue-sharing obligations that compress margins.

Technology platforms and payments

Technology platforms — betting engines, risk tools, cloud and payment gateways — are mission critical for Tabcorp; 99.95–99.99% availability SLAs, PCI DSS and AML controls concentrate vendor choice and raise supplier bargaining power, while certification and migration costs create high switching barriers.

- High-availability SLAs: 99.95–99.99%

- Compliance: PCI DSS, AML, ISO 27001

- Switching barriers: certification + migration risk

- Cost mitigation: volume discounts, redundancy contracts

Broadcast production and satellite capacity

Outside broadcast crews, satellite capacity and CDN providers are critical to Sky Racing distribution and wield pricing power, especially for premium race times and specialist OB teams; outages historically cause immediate revenue loss and brand damage. In 2024 the global CDN market was ~USD30bn, underscoring supplier scale, while Tabcorp’s partial in‑house production and multi‑provider sourcing moderate that clout.

- High supplier clout: premium timeslot capacity

- Operational risk: outages → immediate revenue loss

- Mitigation: multi‑provider mix + in‑house capabilities

High supplier power: racing codes, data vendors and retail scale lock in customers

Supplier power is high: three racing codes and three major data vendors concentrate rights and feeds, enabling multi‑year (>5y) contracts and fee escalation. Tabcorp’s retail reliance (c.5,000 outlets, group revenue A$3.7bn FY2024) and 99.95–99.99% tech SLAs raise switching costs. CDN market scale (~USD30bn 2024) and premium OB capacity further amplify supplier leverage.

| Supplier | Concentration | Key metric |

|---|---|---|

| Racing codes | High (3) | Contracts >5y |

| Data vendors | High (≈3) | Latency/reliability |

| Retail venues | Moderate | 5,000 outlets (FY2024) |

What is included in the product

Concise Porter's Five Forces analysis of Tabcorp identifying competitive rivalry, buyer/supplier power, threats from new entrants and substitutes, plus regulatory and technological disruptors to its wagering and entertainment markets.

Concise Porter's Five Forces for Tabcorp that maps regulatory, competitor, supplier and tech pressures into a single-sheet view—ideal for fast strategic decisions, board decks, and scenario comparison without complex setup.

Customers Bargaining Power

Multi-homing bettors

As of 2024 multi-homing is widespread: punters commonly hold accounts with Sportsbet, Ladbrokes, bet365 and TAB, raising buyer power and price sensitivity. Low switching costs driven by frequent price boosts and promotions make customers nimble and margin-sensitive. Loyalty programs and omnichannel features (retail+digital) are deployed to damp churn but have limited power against aggressive short-term offers.

Price and promo sensitivity

Customers exert strong bargaining power as odds competitiveness, bonus bets and same-game multis drive rapid acquisition; apps and odds aggregators allow buyers to compare offers instantly. Regulatory curbs on inducements in some states moderate deal-seeking but do not eliminate it. Sustained promo wars compress operator margins and elevate buyer leverage, forcing continuous spend to defend market share.

Omnichannel expectations

Customers demand seamless app, web and retail experiences with fast in-play; in 2024 mobile channels accounted for over 70% of Australian wagering traffic, raising expectations. Friction in IDV, payments or bet settlement triggers immediate switching and higher churn. Superior UX reduces perceived buyer power by increasing stickiness, while lagging digital features amplify customer bargaining leverage.

Venue and corporate clients

Venue and corporate clients wield strong leverage over Tabcorp, negotiating commissions, screen rights and exclusivity for TAB terminals and Sky content; in FY2024 Tabcorp reported group revenue of about AUD 4.2bn, making these deals material to margins. Rival bookmakers and digital media alternatives raised venue bargaining power in 2024, while large venue groups extract multi-site bundles for lower fees. Performance-linked remuneration partially aligns incentives but concedes margin, shifting risk to Tabcorp.

- venues: commission, screen rights, exclusivity

- rivals/media: increase alternatives

- large groups: bundle leverage

- pay-for-performance: aligns but reduces margin

Keno players’ alternatives

Keno appeals to casual retail players with low stakes and rapid draws, but close substitutes such as EGMs and lotteries keep customers highly price- and payout-sensitive, limiting Tabcorp’s buyer leverage.

- Minimal switching costs at venue level

- Progressive jackpots and variants lower perceived buyer power

- Casual play drives volume, not loyalty

Mobile bettors (>70%) promos spur churn; venue deals sway margins

Customers hold multiple bookmaker accounts, driving high price sensitivity and low switching costs; omnichannel loyalty partially reduces churn but cannot match short-term promos. Mobile accounted for over 70% of wagering traffic in 2024, raising UX expectations and rapid switching on friction. Tabcorp’s FY2024 group revenue ~AUD 4.2bn makes venue and corporate client deals materially influential on margins.

| Metric | 2024 |

|---|---|

| Mobile share | >70% |

| Tabcorp revenue | AUD 4.2bn |

| Customer behavior | Multi-homing, promo-driven |

What You See Is What You Get

Tabcorp Porter's Five Forces Analysis

This preview shows the Tabcorp Porter’s Five Forces Analysis in full; what you see is the exact, professionally formatted document you'll receive immediately after purchase. It covers competitive rivalry, supplier and buyer power, and the threats of entry and substitutes. No placeholders or mockups—ready for instant download and use.