Taiheiyo Cement Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Taiheiyo Cement faces moderate supplier power due to raw material concentration, high buyer scrutiny from large construction clients, and steady rivalry in a mature domestic market, while new entrants are limited by scale and capital intensity and substitutes (e.g., alternative binders) pose emerging but manageable threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Taiheiyo Cement’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials

Core inputs such as limestone, gypsum and clinker additives are supplied by a limited set of qualified quarries and traders, and strict quality specs plus geographic proximity make switching difficult for Taiheiyo Cement.

Taiheiyo’s mineral resources segment provides partial self-supply that reduces supplier leverage, but depletion of reserves and tightening permit regimes can quickly increase supplier bargaining power.

Energy and fuel dependence

Cement production is highly energy-intensive, relying on coal, petcoke, alternative fuels and grid power; Japan imports over 90% of its fossil fuels, exposing Taiheiyo Cement to global price and FX volatility seen in the 2022–24 coal/LNG price shocks. Long-term fuel contracts mitigate but could not fully hedge 2022 spikes; during tight energy markets suppliers gain measurable bargaining power, pressuring margins and prompting fuel-switching and efficiency investments.

Specialized equipment and spares

Kilns, mills and emission-control systems depend on OEM parts and certified services, and 2024 industry data show critical spare lead times commonly span 6–9 months, creating tangible downtime exposure for Taiheiyo Cement. Limited qualified vendors produce switching frictions and concentrated supplier leverage, with OEMs retaining pricing power on high-value components. Predictive maintenance programs and selective multi-sourcing have reduced unplanned outages by an estimated 15–25% in 2024 case studies, yet critical spares remain high-bargain items for suppliers.

Waste-derived and SCM feedstocks

Waste-derived fuels and SCMs (slag, fly ash) depend heavily on upstream industrial output and policy; as decarbonization accelerates competition for high-quality SCMs rises, increasing supplier leverage over pricing and availability. Taiheiyo Cement’s environmental services and waste-processing footprint improve feedstock access but do not eliminate market tightness or regional logistics constraints. Tight supplies can force repricing of cement blends and raise CO2 abatement costs.

- Supply dependence: upstream industrial output + policy

- Supplier clout: rising with decarbonization-driven demand

- Taiheiyo edge: improved access via environmental services, not full control

- Risk: blend repricing and higher logistics/abatement costs

Logistics and maritime capacity

Domestic coastal shipping, barges and terminals are essential for cement’s bulk distribution; port slots, vessel availability and freight rates materially affect delivered cost and margins, with logistics partners gaining leverage during peak construction seasons or capacity shortages.

- Port slots pressure

- Vessel availability

- Freight-rate exposure

- Vertical logistics lowers but not removes risk

Supply concentration, 6–9 months spare lead times, >90% fuel import risk; outages cut 15–25%

Core inputs and OEM parts are concentrated, creating switching frictions; spare lead times of 6–9 months in 2024 give suppliers pricing power. Japan imports over 90% of fossil fuels, exposing Taiheiyo to global fuel/FX shocks; long-term contracts helped but could not fully hedge 2022–24 price spikes. Self-supply and predictive maintenance cut unplanned outages by 15–25% in 2024 but do not eliminate supplier leverage.

| Metric | 2024 value |

|---|---|

| Fossil fuel import dependency | >90% |

| Spare lead times | 6–9 months |

| Unplanned outage reduction | 15–25% |

What is included in the product

Tailored Porter’s Five Forces analysis for Taiheiyo Cement, uncovering competitive intensity, supplier and buyer power, threats from new entrants and substitutes, and regulatory/market dynamics that shape pricing and profitability.

Clear, one-sheet Porter's Five Forces for Taiheiyo Cement—instantly visualizes competitive pressure and supplier/buyer risks to ease board-level decisions. Customize force levels or swap in your own data to model scenarios (infrastructure demand, regulations, imports) and drop the chart straight into pitch decks or strategic reports.

Customers Bargaining Power

Concentrated B2B customers

Major buyers—ready-mix firms, contractors and public works agencies—drive demand for Taiheiyo Cement; Japan’s FY2024 public works budget stood at ¥6.7 trillion, concentrating volume in large projects that enhance buyer leverage over price and service. Framework agreements with volume discounts reduce short-term price volatility but lock in concessions tied to scale. Ongoing consolidation among contractors and RMC suppliers increases comparative shopping power and negotiation intensity.

Price sensitivity and commoditization

Cement grades are highly standardized, so price becomes the primary battleground for Taiheiyo Cement as product differentiation is limited. Delivery reliability and technical support offer some premium potential but only partially offset commoditization. Buyers intensify discount demands during demand slowdowns, while indexation clauses in contracts help partly pass rising fuel and raw material costs back to customers.

Switching costs and local stickiness

While products are broadly comparable, switching requires re-qualification, re-routing logistics and contract amendments, raising real switching costs for buyers in 2024 and preserving local customer stickiness for Taiheiyo Cement.

Proximity to plants and terminals amplifies delivered-cost gaps, creating quasi-captive local pockets where Taiheiyo’s nearby supply is materially cheaper for end users.

However, in overlapping service areas with multiple nearby suppliers, buyers can and do switch readily, keeping customer bargaining power significant.

Project cycles and timing power

Infrastructure and housing cycles drive batch purchases and tender timing, letting buyers concentrate orders during slow periods to pressure prices. Buyers exploit overcapacity by timing orders when plants run below optimal utilization, forcing producers to offer concessions as project backlogs thin. Conversely, tight markets and low inventories sharply reduce buyer leverage, shifting negotiation power to Taiheiyo Cement.

- Buyer timing: batch orders affect leverage

- Overcapacity: increases concessions

- Thin backlogs: higher discounts

- Tight market: reduced buyer power

Sustainability and spec pressure

Buyers increasingly demand low-clinker/low-CO2 cement as the cement sector causes about 7% of global CO2 emissions; meeting tighter specs shifts bargaining power toward suppliers of scarce SCMs and verified green supply chains. Taiheiyo Cement can defend margins by branding and certifying eco-products and sourcing SCMs, but large buyers may still push prices down using sustainability targets and scale purchasing power.

- Buyers: demand low-CO2, leverage scale

- Suppliers: control of SCMs raises bargaining power

- Taiheiyo: certified eco-products = margin defense

- Risk: buyers negotiate lower premiums

Buyers wield leverage; Japan FY24 ¥6.7T, cement ≈7%

Major buyers (RMC, contractors, public works) exert strong price and service pressure—Japan FY2024 public works budget ¥6.7 trillion concentrates volume and leverage. Standardized product limits differentiation; delivery, reliability and eco-certification provide partial premium. Consolidation among buyers and demand cyclicality raise negotiation intensity, while local proximity and re-qualification costs preserve pockets of stickiness; cement sector ≈7% of global CO2.

| Metric | Buyer Impact | Data |

|---|---|---|

| Public works | Concentrates demand | ¥6.7 trillion (FY2024) |

| Product commoditization | Price pressure | High |

| CO2 focus | Shifts premium to green suppliers | ≈7% global CO2 |

Preview the Actual Deliverable

Taiheiyo Cement Porter's Five Forces Analysis

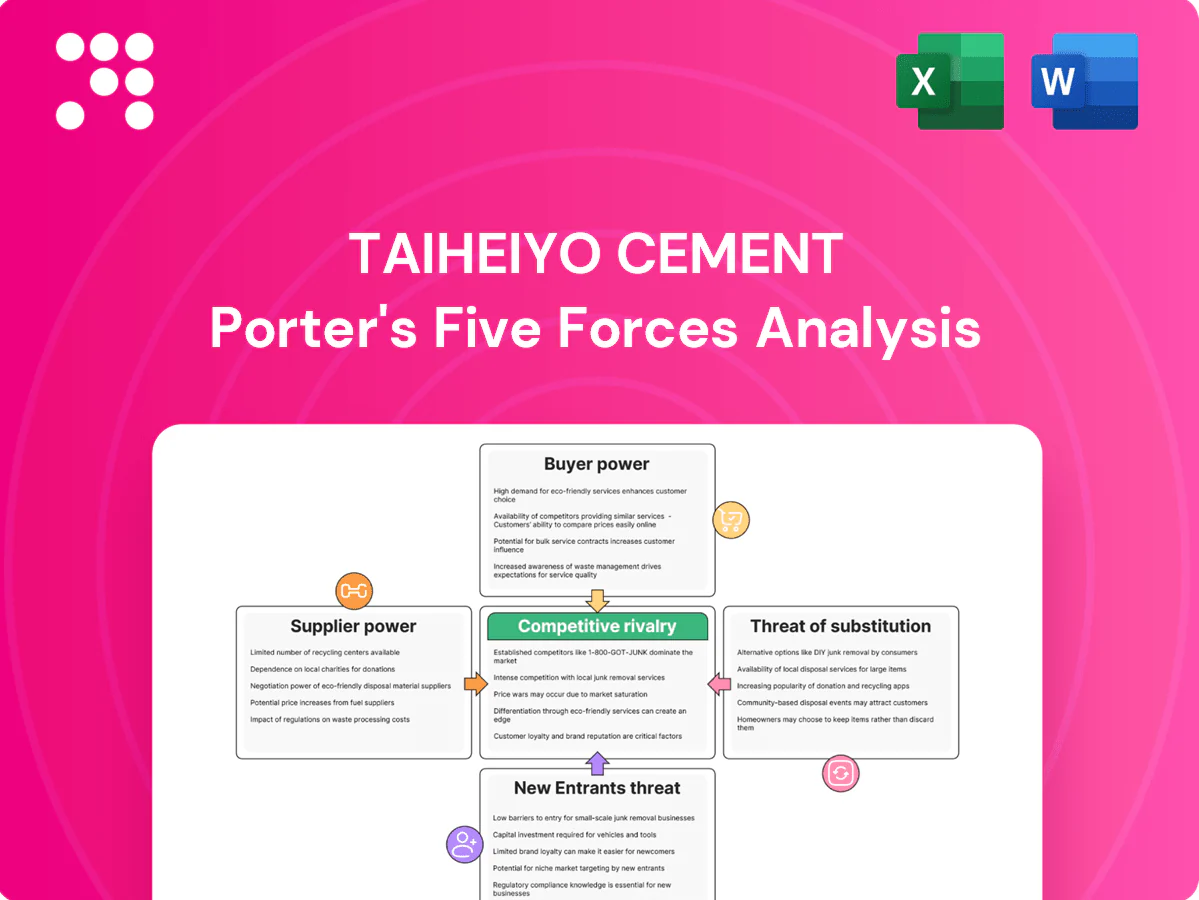

This preview shows the exact Taiheiyo Cement Porter's Five Forces Analysis you'll receive after purchase—fully formatted, complete and ready for immediate download. The assessment covers competitive rivalry, supplier and buyer power, and threats of substitutes and new entry, with clear, actionable insights. No placeholders or samples; this is the final deliverable.

Go Beyond the Preview—Access the Full Strategic Report

Taiheiyo Cement faces moderate supplier power due to raw material concentration, high buyer scrutiny from large construction clients, and steady rivalry in a mature domestic market, while new entrants are limited by scale and capital intensity and substitutes (e.g., alternative binders) pose emerging but manageable threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Taiheiyo Cement’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials

Core inputs such as limestone, gypsum and clinker additives are supplied by a limited set of qualified quarries and traders, and strict quality specs plus geographic proximity make switching difficult for Taiheiyo Cement.

Taiheiyo’s mineral resources segment provides partial self-supply that reduces supplier leverage, but depletion of reserves and tightening permit regimes can quickly increase supplier bargaining power.

Energy and fuel dependence

Cement production is highly energy-intensive, relying on coal, petcoke, alternative fuels and grid power; Japan imports over 90% of its fossil fuels, exposing Taiheiyo Cement to global price and FX volatility seen in the 2022–24 coal/LNG price shocks. Long-term fuel contracts mitigate but could not fully hedge 2022 spikes; during tight energy markets suppliers gain measurable bargaining power, pressuring margins and prompting fuel-switching and efficiency investments.

Specialized equipment and spares

Kilns, mills and emission-control systems depend on OEM parts and certified services, and 2024 industry data show critical spare lead times commonly span 6–9 months, creating tangible downtime exposure for Taiheiyo Cement. Limited qualified vendors produce switching frictions and concentrated supplier leverage, with OEMs retaining pricing power on high-value components. Predictive maintenance programs and selective multi-sourcing have reduced unplanned outages by an estimated 15–25% in 2024 case studies, yet critical spares remain high-bargain items for suppliers.

Waste-derived and SCM feedstocks

Waste-derived fuels and SCMs (slag, fly ash) depend heavily on upstream industrial output and policy; as decarbonization accelerates competition for high-quality SCMs rises, increasing supplier leverage over pricing and availability. Taiheiyo Cement’s environmental services and waste-processing footprint improve feedstock access but do not eliminate market tightness or regional logistics constraints. Tight supplies can force repricing of cement blends and raise CO2 abatement costs.

- Supply dependence: upstream industrial output + policy

- Supplier clout: rising with decarbonization-driven demand

- Taiheiyo edge: improved access via environmental services, not full control

- Risk: blend repricing and higher logistics/abatement costs

Logistics and maritime capacity

Domestic coastal shipping, barges and terminals are essential for cement’s bulk distribution; port slots, vessel availability and freight rates materially affect delivered cost and margins, with logistics partners gaining leverage during peak construction seasons or capacity shortages.

- Port slots pressure

- Vessel availability

- Freight-rate exposure

- Vertical logistics lowers but not removes risk

Supply concentration, 6–9 months spare lead times, >90% fuel import risk; outages cut 15–25%

Core inputs and OEM parts are concentrated, creating switching frictions; spare lead times of 6–9 months in 2024 give suppliers pricing power. Japan imports over 90% of fossil fuels, exposing Taiheiyo to global fuel/FX shocks; long-term contracts helped but could not fully hedge 2022–24 price spikes. Self-supply and predictive maintenance cut unplanned outages by 15–25% in 2024 but do not eliminate supplier leverage.

| Metric | 2024 value |

|---|---|

| Fossil fuel import dependency | >90% |

| Spare lead times | 6–9 months |

| Unplanned outage reduction | 15–25% |

What is included in the product

Tailored Porter’s Five Forces analysis for Taiheiyo Cement, uncovering competitive intensity, supplier and buyer power, threats from new entrants and substitutes, and regulatory/market dynamics that shape pricing and profitability.

Clear, one-sheet Porter's Five Forces for Taiheiyo Cement—instantly visualizes competitive pressure and supplier/buyer risks to ease board-level decisions. Customize force levels or swap in your own data to model scenarios (infrastructure demand, regulations, imports) and drop the chart straight into pitch decks or strategic reports.

Customers Bargaining Power

Concentrated B2B customers

Major buyers—ready-mix firms, contractors and public works agencies—drive demand for Taiheiyo Cement; Japan’s FY2024 public works budget stood at ¥6.7 trillion, concentrating volume in large projects that enhance buyer leverage over price and service. Framework agreements with volume discounts reduce short-term price volatility but lock in concessions tied to scale. Ongoing consolidation among contractors and RMC suppliers increases comparative shopping power and negotiation intensity.

Price sensitivity and commoditization

Cement grades are highly standardized, so price becomes the primary battleground for Taiheiyo Cement as product differentiation is limited. Delivery reliability and technical support offer some premium potential but only partially offset commoditization. Buyers intensify discount demands during demand slowdowns, while indexation clauses in contracts help partly pass rising fuel and raw material costs back to customers.

Switching costs and local stickiness

While products are broadly comparable, switching requires re-qualification, re-routing logistics and contract amendments, raising real switching costs for buyers in 2024 and preserving local customer stickiness for Taiheiyo Cement.

Proximity to plants and terminals amplifies delivered-cost gaps, creating quasi-captive local pockets where Taiheiyo’s nearby supply is materially cheaper for end users.

However, in overlapping service areas with multiple nearby suppliers, buyers can and do switch readily, keeping customer bargaining power significant.

Project cycles and timing power

Infrastructure and housing cycles drive batch purchases and tender timing, letting buyers concentrate orders during slow periods to pressure prices. Buyers exploit overcapacity by timing orders when plants run below optimal utilization, forcing producers to offer concessions as project backlogs thin. Conversely, tight markets and low inventories sharply reduce buyer leverage, shifting negotiation power to Taiheiyo Cement.

- Buyer timing: batch orders affect leverage

- Overcapacity: increases concessions

- Thin backlogs: higher discounts

- Tight market: reduced buyer power

Sustainability and spec pressure

Buyers increasingly demand low-clinker/low-CO2 cement as the cement sector causes about 7% of global CO2 emissions; meeting tighter specs shifts bargaining power toward suppliers of scarce SCMs and verified green supply chains. Taiheiyo Cement can defend margins by branding and certifying eco-products and sourcing SCMs, but large buyers may still push prices down using sustainability targets and scale purchasing power.

- Buyers: demand low-CO2, leverage scale

- Suppliers: control of SCMs raises bargaining power

- Taiheiyo: certified eco-products = margin defense

- Risk: buyers negotiate lower premiums

Buyers wield leverage; Japan FY24 ¥6.7T, cement ≈7%

Major buyers (RMC, contractors, public works) exert strong price and service pressure—Japan FY2024 public works budget ¥6.7 trillion concentrates volume and leverage. Standardized product limits differentiation; delivery, reliability and eco-certification provide partial premium. Consolidation among buyers and demand cyclicality raise negotiation intensity, while local proximity and re-qualification costs preserve pockets of stickiness; cement sector ≈7% of global CO2.

| Metric | Buyer Impact | Data |

|---|---|---|

| Public works | Concentrates demand | ¥6.7 trillion (FY2024) |

| Product commoditization | Price pressure | High |

| CO2 focus | Shifts premium to green suppliers | ≈7% global CO2 |

Preview the Actual Deliverable

Taiheiyo Cement Porter's Five Forces Analysis

This preview shows the exact Taiheiyo Cement Porter's Five Forces Analysis you'll receive after purchase—fully formatted, complete and ready for immediate download. The assessment covers competitive rivalry, supplier and buyer power, and threats of substitutes and new entry, with clear, actionable insights. No placeholders or samples; this is the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Taiheiyo Cement faces moderate supplier power due to raw material concentration, high buyer scrutiny from large construction clients, and steady rivalry in a mature domestic market, while new entrants are limited by scale and capital intensity and substitutes (e.g., alternative binders) pose emerging but manageable threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Taiheiyo Cement’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials

Core inputs such as limestone, gypsum and clinker additives are supplied by a limited set of qualified quarries and traders, and strict quality specs plus geographic proximity make switching difficult for Taiheiyo Cement.

Taiheiyo’s mineral resources segment provides partial self-supply that reduces supplier leverage, but depletion of reserves and tightening permit regimes can quickly increase supplier bargaining power.

Energy and fuel dependence

Cement production is highly energy-intensive, relying on coal, petcoke, alternative fuels and grid power; Japan imports over 90% of its fossil fuels, exposing Taiheiyo Cement to global price and FX volatility seen in the 2022–24 coal/LNG price shocks. Long-term fuel contracts mitigate but could not fully hedge 2022 spikes; during tight energy markets suppliers gain measurable bargaining power, pressuring margins and prompting fuel-switching and efficiency investments.

Specialized equipment and spares

Kilns, mills and emission-control systems depend on OEM parts and certified services, and 2024 industry data show critical spare lead times commonly span 6–9 months, creating tangible downtime exposure for Taiheiyo Cement. Limited qualified vendors produce switching frictions and concentrated supplier leverage, with OEMs retaining pricing power on high-value components. Predictive maintenance programs and selective multi-sourcing have reduced unplanned outages by an estimated 15–25% in 2024 case studies, yet critical spares remain high-bargain items for suppliers.

Waste-derived and SCM feedstocks

Waste-derived fuels and SCMs (slag, fly ash) depend heavily on upstream industrial output and policy; as decarbonization accelerates competition for high-quality SCMs rises, increasing supplier leverage over pricing and availability. Taiheiyo Cement’s environmental services and waste-processing footprint improve feedstock access but do not eliminate market tightness or regional logistics constraints. Tight supplies can force repricing of cement blends and raise CO2 abatement costs.

- Supply dependence: upstream industrial output + policy

- Supplier clout: rising with decarbonization-driven demand

- Taiheiyo edge: improved access via environmental services, not full control

- Risk: blend repricing and higher logistics/abatement costs

Logistics and maritime capacity

Domestic coastal shipping, barges and terminals are essential for cement’s bulk distribution; port slots, vessel availability and freight rates materially affect delivered cost and margins, with logistics partners gaining leverage during peak construction seasons or capacity shortages.

- Port slots pressure

- Vessel availability

- Freight-rate exposure

- Vertical logistics lowers but not removes risk

Supply concentration, 6–9 months spare lead times, >90% fuel import risk; outages cut 15–25%

Core inputs and OEM parts are concentrated, creating switching frictions; spare lead times of 6–9 months in 2024 give suppliers pricing power. Japan imports over 90% of fossil fuels, exposing Taiheiyo to global fuel/FX shocks; long-term contracts helped but could not fully hedge 2022–24 price spikes. Self-supply and predictive maintenance cut unplanned outages by 15–25% in 2024 but do not eliminate supplier leverage.

| Metric | 2024 value |

|---|---|

| Fossil fuel import dependency | >90% |

| Spare lead times | 6–9 months |

| Unplanned outage reduction | 15–25% |

What is included in the product

Tailored Porter’s Five Forces analysis for Taiheiyo Cement, uncovering competitive intensity, supplier and buyer power, threats from new entrants and substitutes, and regulatory/market dynamics that shape pricing and profitability.

Clear, one-sheet Porter's Five Forces for Taiheiyo Cement—instantly visualizes competitive pressure and supplier/buyer risks to ease board-level decisions. Customize force levels or swap in your own data to model scenarios (infrastructure demand, regulations, imports) and drop the chart straight into pitch decks or strategic reports.

Customers Bargaining Power

Concentrated B2B customers

Major buyers—ready-mix firms, contractors and public works agencies—drive demand for Taiheiyo Cement; Japan’s FY2024 public works budget stood at ¥6.7 trillion, concentrating volume in large projects that enhance buyer leverage over price and service. Framework agreements with volume discounts reduce short-term price volatility but lock in concessions tied to scale. Ongoing consolidation among contractors and RMC suppliers increases comparative shopping power and negotiation intensity.

Price sensitivity and commoditization

Cement grades are highly standardized, so price becomes the primary battleground for Taiheiyo Cement as product differentiation is limited. Delivery reliability and technical support offer some premium potential but only partially offset commoditization. Buyers intensify discount demands during demand slowdowns, while indexation clauses in contracts help partly pass rising fuel and raw material costs back to customers.

Switching costs and local stickiness

While products are broadly comparable, switching requires re-qualification, re-routing logistics and contract amendments, raising real switching costs for buyers in 2024 and preserving local customer stickiness for Taiheiyo Cement.

Proximity to plants and terminals amplifies delivered-cost gaps, creating quasi-captive local pockets where Taiheiyo’s nearby supply is materially cheaper for end users.

However, in overlapping service areas with multiple nearby suppliers, buyers can and do switch readily, keeping customer bargaining power significant.

Project cycles and timing power

Infrastructure and housing cycles drive batch purchases and tender timing, letting buyers concentrate orders during slow periods to pressure prices. Buyers exploit overcapacity by timing orders when plants run below optimal utilization, forcing producers to offer concessions as project backlogs thin. Conversely, tight markets and low inventories sharply reduce buyer leverage, shifting negotiation power to Taiheiyo Cement.

- Buyer timing: batch orders affect leverage

- Overcapacity: increases concessions

- Thin backlogs: higher discounts

- Tight market: reduced buyer power

Sustainability and spec pressure

Buyers increasingly demand low-clinker/low-CO2 cement as the cement sector causes about 7% of global CO2 emissions; meeting tighter specs shifts bargaining power toward suppliers of scarce SCMs and verified green supply chains. Taiheiyo Cement can defend margins by branding and certifying eco-products and sourcing SCMs, but large buyers may still push prices down using sustainability targets and scale purchasing power.

- Buyers: demand low-CO2, leverage scale

- Suppliers: control of SCMs raises bargaining power

- Taiheiyo: certified eco-products = margin defense

- Risk: buyers negotiate lower premiums

Buyers wield leverage; Japan FY24 ¥6.7T, cement ≈7%

Major buyers (RMC, contractors, public works) exert strong price and service pressure—Japan FY2024 public works budget ¥6.7 trillion concentrates volume and leverage. Standardized product limits differentiation; delivery, reliability and eco-certification provide partial premium. Consolidation among buyers and demand cyclicality raise negotiation intensity, while local proximity and re-qualification costs preserve pockets of stickiness; cement sector ≈7% of global CO2.

| Metric | Buyer Impact | Data |

|---|---|---|

| Public works | Concentrates demand | ¥6.7 trillion (FY2024) |

| Product commoditization | Price pressure | High |

| CO2 focus | Shifts premium to green suppliers | ≈7% global CO2 |

Preview the Actual Deliverable

Taiheiyo Cement Porter's Five Forces Analysis

This preview shows the exact Taiheiyo Cement Porter's Five Forces Analysis you'll receive after purchase—fully formatted, complete and ready for immediate download. The assessment covers competitive rivalry, supplier and buyer power, and threats of substitutes and new entry, with clear, actionable insights. No placeholders or samples; this is the final deliverable.