Takara Bio PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Takara Bio PESTLE Analysis—concise, expertly researched insight into political, economic, social, technological, legal, and environmental forces shaping the company. Ideal for investors and strategists; buy the full report now to access actionable, editable findings and immediate download.

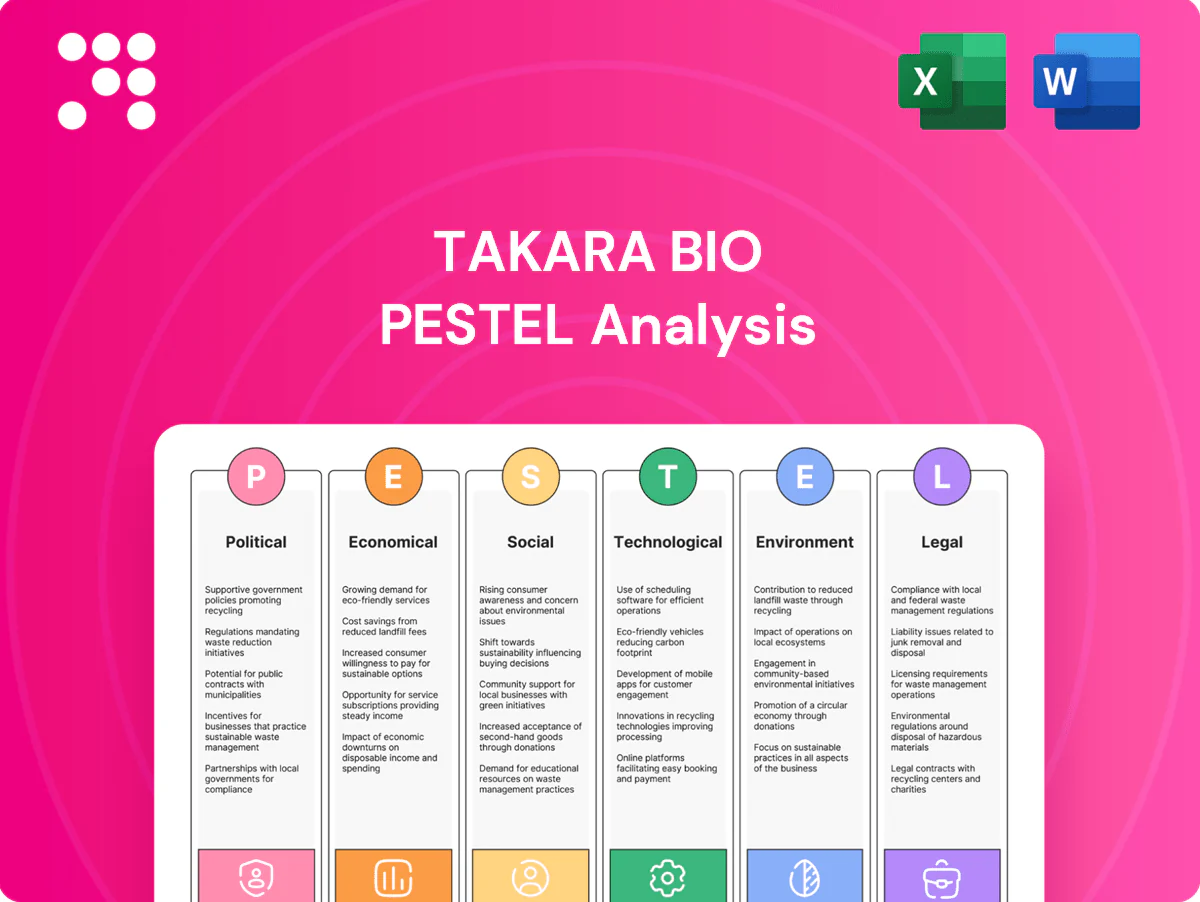

Political factors

Global regulatory alignment

Gene and cell therapy tools face divergent regulatory frameworks across the US, EU, Japan and China, complicating global rollouts. ICH, established in 1990, and PIC/S harmonization efforts can smooth approvals for GMP-grade reagents and services. Regulatory misalignment increases compliance costs and delays market entry. Continuous monitoring of FDA, EMA and PMDA guidance is critical for kit labeling, validation and QC expectations.

Government R&D funding

Public grants—NIH funding above $50B (FY2024–25), Horizon Europe budget €95.5B (2021–27) and AMED allocations near ¥300B in 2024—drive demand for genomics and cell‑biology reagents. Budget cycles and priorities (pandemic readiness, rare‑disease programs) shift Takara Bio’s product mix. Funding cuts or freezes measurably slow orders from academic cores. Strategic alignment with funded programs stabilizes revenue streams.

Health policy and biomanufacturing

National strategies to localize biomanufacturing in 2024 shifted CDMO selection toward partners with in-country facilities and regulatory experience, reshaping supplier lists. Targeted incentives for advanced therapies in 2024 accelerated uptake of viral vector and cell-processing tools. Conversely, medicine price controls continue to squeeze pharma budgets, and many public procurements now mandate local presence for eligibility.

Geopolitics and trade

Export controls tightened in 2023–24 complicate shipments of enzymes, instruments and software and US tariffs on China-origin goods can reach up to 25%, raising landed costs; US–China supply-chain tensions risk disrupting sourcing of electronic and reagent components, while sanctions screening increases administrative and KYC burden for global shipments. Takara Bio mitigates risk through diversified logistics and dual-sourcing strategies.

- Export controls tightened 2023–24

- US tariffs on China up to 25%

- Supply-chain disruption risk from US–China tensions

- Sanctions screening raises compliance workload

- Diversified logistics and dual-sourcing mitigate shocks

Pandemic preparedness

Policy-led stockpiles and surveillance programs drive cyclical PCR/NGS demand, supporting a global reagent and consumables market estimated over USD 10B by 2024; post‑pandemic normalization has reduced routine test volumes but sustains baseline sequencing and PCR capacity. Readiness funding prioritizes validated, scalable kits and Takara Bio's participation in public‑private consortia increases procurement visibility and contract access.

- cyclical demand: policy stockpiles

- baseline capacity: sustained post‑pandemic

- funding: favors validated kits

- visibility: consortia boost procurement

Regulatory divergence, public funding and trade frictions raise costs and delay launches

Regulatory divergence across US/EU/Japan/China raises compliance costs and delays global launches; FDA/EMA/PMDA guidance monitoring is essential. Public grants (NIH >$50B FY2024–25, Horizon €95.5B, AMED ≈¥300B 2024) underpin reagent demand. Trade frictions (US tariffs up to 25%, tightened export controls 2023–24) increase landed costs and supply‑chain risk.

| Factor | Impact | Key data |

|---|---|---|

| Regulation | Higher compliance | FDA/EMA/PMDA guidance |

| Public funding | Demand driver | NIH>$50B; Horizon €95.5B; AMED≈¥300B |

| Trade | Cost/supply risk | Tariffs up to 25%; export controls 2023–24 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Takara Bio across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and sector-specific examples.

Designed for executives, consultants and investors, it provides detailed sub-points, forward-looking insights and ready-to-use formatting to support scenario planning, risk mitigation and funding discussions.

A concise, visually segmented PESTLE summary of Takara Bio that simplifies external risk and market positioning for quick integration into presentations and team planning; editable notes let users localize insights by region or business line for fast alignment across teams.

Economic factors

Currency volatility (JPY)

Yen depreciation (USD/JPY ~150 in 2024) lifts Takara Bio's translated overseas revenue but raises import costs for reagents and components sourced abroad. Pricing power in USD/EUR is required to offset COGS inflation to protect gross margins. Active FX hedging programs smooth quarter-to-quarter margin variability. Regional price corridors and segmented pricing help maintain competitiveness across APAC, Europe and North America.

Biotech funding cycle

Risk-on equity markets have historically lifted startup lab spend on discovery reagents and services, but biotech VC funding cooled after the 2021–22 peak, weakening order growth in 2024 and lengthening sales cycles. Tight VC and IPO windows in 2024 curtailed new program starts, extending purchasing decisions and increasing churn. Enterprise contracts with big pharma and opex-friendly subscriptions (recurring revenue) have buffered cyclicality and stabilized cash flow for Takara Bio.

Input inflation and logistics

Enzymes, plastics and semiconductor parts show volatile pricing and lead times—semiconductor lead times peaked above 20 weeks in 2021–22 and averaged ~12–14 weeks by 2024—while cold-chain and hazmat shipping can add roughly 20–40% to freight costs. Lean inventory reduces carrying costs but raises stockout risk; buffers can inflate working capital needs by ~10–25%. Supplier partnerships and VMI have cut stockout rates by up to ~50% in industry cases.

Customer consolidation

Customer consolidation in pharma M&A concentrates purchasing power and standardizes vendor lists, forcing suppliers into competitive preferred‑supplier processes; academic cores increasingly centralize procurement—NIH funding was about 49.6 billion USD in FY2024, underpinning large institutional tenders. Winning preferred status scales volumes but compresses margins, while differentiation through demonstrable quality and customer support helps defend pricing and limit commoditization.

- Pharma M&A: concentrated purchasing

- Academic tenders: NIH ~49.6B FY2024

- Preferred supplier: higher volume, lower margins

- Differentiation: quality + support preserves price

Growth in APAC markets

APAC R&D expansion—notably China (R&D intensity ~2.4–2.8% of GDP), South Korea (~4.6% of GDP) and India (~0.7% of GDP)—is enlarging Takara Bio’s addressable market as regional biotech funding and clinical activity rise in 2024–25. Intensifying local suppliers compress margins on commoditized reagents, while strict compliance and higher service quality support premium pricing. Regional manufacturing reduces landed costs and shortens lead times.

- Rising R&D: China/Korea/India funding up

- Price pressure: local competitors

- Premium: compliance & service

- Cost: regional manufacturing lowers landed cost

Regulatory divergence, public funding and trade frictions raise costs and delay launches

Yen ~150 (2024) boosts translated overseas revenue but raises imported COGS; FX hedges used to stabilize margins. Biotech VC funding retrenched after 2022, softening orders; enterprise contracts/recurring revenue improved cash stability. Supply‑chain lead times ~12–14 weeks (2024) raise working capital needs; regional manufacturing cuts landed costs.

| Metric | 2024 |

|---|---|

| USD/JPY | ~150 |

| NIH budget | 49.6B USD |

| Semi lead time | 12–14 wks |

Preview Before You Purchase

Takara Bio PESTLE Analysis

The preview shown here is the exact Takara Bio PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors with actionable insights and source notes. No placeholders or teasers—this is the final file available for immediate download.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Takara Bio PESTLE Analysis—concise, expertly researched insight into political, economic, social, technological, legal, and environmental forces shaping the company. Ideal for investors and strategists; buy the full report now to access actionable, editable findings and immediate download.

Political factors

Global regulatory alignment

Gene and cell therapy tools face divergent regulatory frameworks across the US, EU, Japan and China, complicating global rollouts. ICH, established in 1990, and PIC/S harmonization efforts can smooth approvals for GMP-grade reagents and services. Regulatory misalignment increases compliance costs and delays market entry. Continuous monitoring of FDA, EMA and PMDA guidance is critical for kit labeling, validation and QC expectations.

Government R&D funding

Public grants—NIH funding above $50B (FY2024–25), Horizon Europe budget €95.5B (2021–27) and AMED allocations near ¥300B in 2024—drive demand for genomics and cell‑biology reagents. Budget cycles and priorities (pandemic readiness, rare‑disease programs) shift Takara Bio’s product mix. Funding cuts or freezes measurably slow orders from academic cores. Strategic alignment with funded programs stabilizes revenue streams.

Health policy and biomanufacturing

National strategies to localize biomanufacturing in 2024 shifted CDMO selection toward partners with in-country facilities and regulatory experience, reshaping supplier lists. Targeted incentives for advanced therapies in 2024 accelerated uptake of viral vector and cell-processing tools. Conversely, medicine price controls continue to squeeze pharma budgets, and many public procurements now mandate local presence for eligibility.

Geopolitics and trade

Export controls tightened in 2023–24 complicate shipments of enzymes, instruments and software and US tariffs on China-origin goods can reach up to 25%, raising landed costs; US–China supply-chain tensions risk disrupting sourcing of electronic and reagent components, while sanctions screening increases administrative and KYC burden for global shipments. Takara Bio mitigates risk through diversified logistics and dual-sourcing strategies.

- Export controls tightened 2023–24

- US tariffs on China up to 25%

- Supply-chain disruption risk from US–China tensions

- Sanctions screening raises compliance workload

- Diversified logistics and dual-sourcing mitigate shocks

Pandemic preparedness

Policy-led stockpiles and surveillance programs drive cyclical PCR/NGS demand, supporting a global reagent and consumables market estimated over USD 10B by 2024; post‑pandemic normalization has reduced routine test volumes but sustains baseline sequencing and PCR capacity. Readiness funding prioritizes validated, scalable kits and Takara Bio's participation in public‑private consortia increases procurement visibility and contract access.

- cyclical demand: policy stockpiles

- baseline capacity: sustained post‑pandemic

- funding: favors validated kits

- visibility: consortia boost procurement

Regulatory divergence, public funding and trade frictions raise costs and delay launches

Regulatory divergence across US/EU/Japan/China raises compliance costs and delays global launches; FDA/EMA/PMDA guidance monitoring is essential. Public grants (NIH >$50B FY2024–25, Horizon €95.5B, AMED ≈¥300B 2024) underpin reagent demand. Trade frictions (US tariffs up to 25%, tightened export controls 2023–24) increase landed costs and supply‑chain risk.

| Factor | Impact | Key data |

|---|---|---|

| Regulation | Higher compliance | FDA/EMA/PMDA guidance |

| Public funding | Demand driver | NIH>$50B; Horizon €95.5B; AMED≈¥300B |

| Trade | Cost/supply risk | Tariffs up to 25%; export controls 2023–24 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Takara Bio across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and sector-specific examples.

Designed for executives, consultants and investors, it provides detailed sub-points, forward-looking insights and ready-to-use formatting to support scenario planning, risk mitigation and funding discussions.

A concise, visually segmented PESTLE summary of Takara Bio that simplifies external risk and market positioning for quick integration into presentations and team planning; editable notes let users localize insights by region or business line for fast alignment across teams.

Economic factors

Currency volatility (JPY)

Yen depreciation (USD/JPY ~150 in 2024) lifts Takara Bio's translated overseas revenue but raises import costs for reagents and components sourced abroad. Pricing power in USD/EUR is required to offset COGS inflation to protect gross margins. Active FX hedging programs smooth quarter-to-quarter margin variability. Regional price corridors and segmented pricing help maintain competitiveness across APAC, Europe and North America.

Biotech funding cycle

Risk-on equity markets have historically lifted startup lab spend on discovery reagents and services, but biotech VC funding cooled after the 2021–22 peak, weakening order growth in 2024 and lengthening sales cycles. Tight VC and IPO windows in 2024 curtailed new program starts, extending purchasing decisions and increasing churn. Enterprise contracts with big pharma and opex-friendly subscriptions (recurring revenue) have buffered cyclicality and stabilized cash flow for Takara Bio.

Input inflation and logistics

Enzymes, plastics and semiconductor parts show volatile pricing and lead times—semiconductor lead times peaked above 20 weeks in 2021–22 and averaged ~12–14 weeks by 2024—while cold-chain and hazmat shipping can add roughly 20–40% to freight costs. Lean inventory reduces carrying costs but raises stockout risk; buffers can inflate working capital needs by ~10–25%. Supplier partnerships and VMI have cut stockout rates by up to ~50% in industry cases.

Customer consolidation

Customer consolidation in pharma M&A concentrates purchasing power and standardizes vendor lists, forcing suppliers into competitive preferred‑supplier processes; academic cores increasingly centralize procurement—NIH funding was about 49.6 billion USD in FY2024, underpinning large institutional tenders. Winning preferred status scales volumes but compresses margins, while differentiation through demonstrable quality and customer support helps defend pricing and limit commoditization.

- Pharma M&A: concentrated purchasing

- Academic tenders: NIH ~49.6B FY2024

- Preferred supplier: higher volume, lower margins

- Differentiation: quality + support preserves price

Growth in APAC markets

APAC R&D expansion—notably China (R&D intensity ~2.4–2.8% of GDP), South Korea (~4.6% of GDP) and India (~0.7% of GDP)—is enlarging Takara Bio’s addressable market as regional biotech funding and clinical activity rise in 2024–25. Intensifying local suppliers compress margins on commoditized reagents, while strict compliance and higher service quality support premium pricing. Regional manufacturing reduces landed costs and shortens lead times.

- Rising R&D: China/Korea/India funding up

- Price pressure: local competitors

- Premium: compliance & service

- Cost: regional manufacturing lowers landed cost

Regulatory divergence, public funding and trade frictions raise costs and delay launches

Yen ~150 (2024) boosts translated overseas revenue but raises imported COGS; FX hedges used to stabilize margins. Biotech VC funding retrenched after 2022, softening orders; enterprise contracts/recurring revenue improved cash stability. Supply‑chain lead times ~12–14 weeks (2024) raise working capital needs; regional manufacturing cuts landed costs.

| Metric | 2024 |

|---|---|

| USD/JPY | ~150 |

| NIH budget | 49.6B USD |

| Semi lead time | 12–14 wks |

Preview Before You Purchase

Takara Bio PESTLE Analysis

The preview shown here is the exact Takara Bio PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors with actionable insights and source notes. No placeholders or teasers—this is the final file available for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Takara Bio PESTLE Analysis—concise, expertly researched insight into political, economic, social, technological, legal, and environmental forces shaping the company. Ideal for investors and strategists; buy the full report now to access actionable, editable findings and immediate download.

Political factors

Global regulatory alignment

Gene and cell therapy tools face divergent regulatory frameworks across the US, EU, Japan and China, complicating global rollouts. ICH, established in 1990, and PIC/S harmonization efforts can smooth approvals for GMP-grade reagents and services. Regulatory misalignment increases compliance costs and delays market entry. Continuous monitoring of FDA, EMA and PMDA guidance is critical for kit labeling, validation and QC expectations.

Government R&D funding

Public grants—NIH funding above $50B (FY2024–25), Horizon Europe budget €95.5B (2021–27) and AMED allocations near ¥300B in 2024—drive demand for genomics and cell‑biology reagents. Budget cycles and priorities (pandemic readiness, rare‑disease programs) shift Takara Bio’s product mix. Funding cuts or freezes measurably slow orders from academic cores. Strategic alignment with funded programs stabilizes revenue streams.

Health policy and biomanufacturing

National strategies to localize biomanufacturing in 2024 shifted CDMO selection toward partners with in-country facilities and regulatory experience, reshaping supplier lists. Targeted incentives for advanced therapies in 2024 accelerated uptake of viral vector and cell-processing tools. Conversely, medicine price controls continue to squeeze pharma budgets, and many public procurements now mandate local presence for eligibility.

Geopolitics and trade

Export controls tightened in 2023–24 complicate shipments of enzymes, instruments and software and US tariffs on China-origin goods can reach up to 25%, raising landed costs; US–China supply-chain tensions risk disrupting sourcing of electronic and reagent components, while sanctions screening increases administrative and KYC burden for global shipments. Takara Bio mitigates risk through diversified logistics and dual-sourcing strategies.

- Export controls tightened 2023–24

- US tariffs on China up to 25%

- Supply-chain disruption risk from US–China tensions

- Sanctions screening raises compliance workload

- Diversified logistics and dual-sourcing mitigate shocks

Pandemic preparedness

Policy-led stockpiles and surveillance programs drive cyclical PCR/NGS demand, supporting a global reagent and consumables market estimated over USD 10B by 2024; post‑pandemic normalization has reduced routine test volumes but sustains baseline sequencing and PCR capacity. Readiness funding prioritizes validated, scalable kits and Takara Bio's participation in public‑private consortia increases procurement visibility and contract access.

- cyclical demand: policy stockpiles

- baseline capacity: sustained post‑pandemic

- funding: favors validated kits

- visibility: consortia boost procurement

Regulatory divergence, public funding and trade frictions raise costs and delay launches

Regulatory divergence across US/EU/Japan/China raises compliance costs and delays global launches; FDA/EMA/PMDA guidance monitoring is essential. Public grants (NIH >$50B FY2024–25, Horizon €95.5B, AMED ≈¥300B 2024) underpin reagent demand. Trade frictions (US tariffs up to 25%, tightened export controls 2023–24) increase landed costs and supply‑chain risk.

| Factor | Impact | Key data |

|---|---|---|

| Regulation | Higher compliance | FDA/EMA/PMDA guidance |

| Public funding | Demand driver | NIH>$50B; Horizon €95.5B; AMED≈¥300B |

| Trade | Cost/supply risk | Tariffs up to 25%; export controls 2023–24 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Takara Bio across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and sector-specific examples.

Designed for executives, consultants and investors, it provides detailed sub-points, forward-looking insights and ready-to-use formatting to support scenario planning, risk mitigation and funding discussions.

A concise, visually segmented PESTLE summary of Takara Bio that simplifies external risk and market positioning for quick integration into presentations and team planning; editable notes let users localize insights by region or business line for fast alignment across teams.

Economic factors

Currency volatility (JPY)

Yen depreciation (USD/JPY ~150 in 2024) lifts Takara Bio's translated overseas revenue but raises import costs for reagents and components sourced abroad. Pricing power in USD/EUR is required to offset COGS inflation to protect gross margins. Active FX hedging programs smooth quarter-to-quarter margin variability. Regional price corridors and segmented pricing help maintain competitiveness across APAC, Europe and North America.

Biotech funding cycle

Risk-on equity markets have historically lifted startup lab spend on discovery reagents and services, but biotech VC funding cooled after the 2021–22 peak, weakening order growth in 2024 and lengthening sales cycles. Tight VC and IPO windows in 2024 curtailed new program starts, extending purchasing decisions and increasing churn. Enterprise contracts with big pharma and opex-friendly subscriptions (recurring revenue) have buffered cyclicality and stabilized cash flow for Takara Bio.

Input inflation and logistics

Enzymes, plastics and semiconductor parts show volatile pricing and lead times—semiconductor lead times peaked above 20 weeks in 2021–22 and averaged ~12–14 weeks by 2024—while cold-chain and hazmat shipping can add roughly 20–40% to freight costs. Lean inventory reduces carrying costs but raises stockout risk; buffers can inflate working capital needs by ~10–25%. Supplier partnerships and VMI have cut stockout rates by up to ~50% in industry cases.

Customer consolidation

Customer consolidation in pharma M&A concentrates purchasing power and standardizes vendor lists, forcing suppliers into competitive preferred‑supplier processes; academic cores increasingly centralize procurement—NIH funding was about 49.6 billion USD in FY2024, underpinning large institutional tenders. Winning preferred status scales volumes but compresses margins, while differentiation through demonstrable quality and customer support helps defend pricing and limit commoditization.

- Pharma M&A: concentrated purchasing

- Academic tenders: NIH ~49.6B FY2024

- Preferred supplier: higher volume, lower margins

- Differentiation: quality + support preserves price

Growth in APAC markets

APAC R&D expansion—notably China (R&D intensity ~2.4–2.8% of GDP), South Korea (~4.6% of GDP) and India (~0.7% of GDP)—is enlarging Takara Bio’s addressable market as regional biotech funding and clinical activity rise in 2024–25. Intensifying local suppliers compress margins on commoditized reagents, while strict compliance and higher service quality support premium pricing. Regional manufacturing reduces landed costs and shortens lead times.

- Rising R&D: China/Korea/India funding up

- Price pressure: local competitors

- Premium: compliance & service

- Cost: regional manufacturing lowers landed cost

Regulatory divergence, public funding and trade frictions raise costs and delay launches

Yen ~150 (2024) boosts translated overseas revenue but raises imported COGS; FX hedges used to stabilize margins. Biotech VC funding retrenched after 2022, softening orders; enterprise contracts/recurring revenue improved cash stability. Supply‑chain lead times ~12–14 weeks (2024) raise working capital needs; regional manufacturing cuts landed costs.

| Metric | 2024 |

|---|---|

| USD/JPY | ~150 |

| NIH budget | 49.6B USD |

| Semi lead time | 12–14 wks |

Preview Before You Purchase

Takara Bio PESTLE Analysis

The preview shown here is the exact Takara Bio PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors with actionable insights and source notes. No placeholders or teasers—this is the final file available for immediate download.