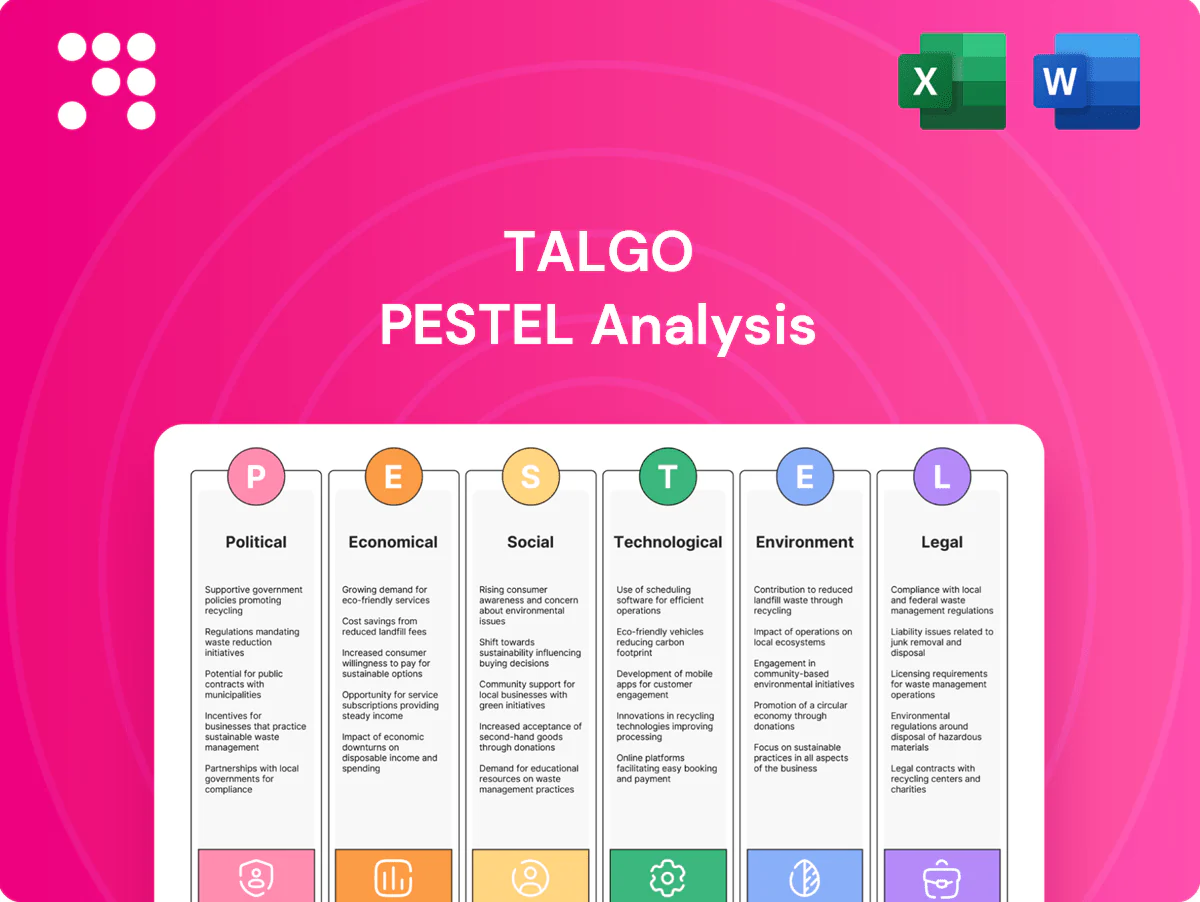

Talgo PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological change are shaping Talgo's prospects in our concise PESTLE overview. This snapshot highlights key risks and opportunities to inform your strategy. Purchase the full, downloadable PESTLE for a detailed, actionable briefing now.

Political factors

EU rail policy and funding

EU rail policy channels priority via TEN-T (core network targets 2030, comprehensive 2050) and Green Deal goals (at least 55% GHG reduction by 2030), boosting high-speed and intercity tenders where Talgo competes. Harmonization initiatives simplify cross-border rolling stock approvals, underpinning a stable European pipeline for Talgo. A reallocation of EU budget priorities could delay project starts and cash flows.

Government procurement dynamics

National rail operators award multi-year contracts often worth €500m–€2bn and tied to policy goals and election cycles, with tender timing affecting delivery windows of 7–15 years. Specifications frequently mandate 30–60% local content or preferred technologies, so Talgo must align bids with national strategic plans and localization targets. Political turnover can abruptly reset priorities and pipeline forecasts, delaying or reshaping committed spend.

Geopolitical risk and sanctions

Talgo’s export markets can be constrained by sanctions and diplomatic tensions, notably since the 2022 EU/US measures that tightened controls on technology and transport-sector goods. Rolling stock and critical parts may face export controls to jurisdictions under embargo, forcing reroutes or cancelled sales. Talgo’s global maintenance footprint requires rigorous compliance screening to avoid fines and frozen receivables. Sudden sanctions can halt deliveries and delay payments across contracts.

Public-private partnership models

Many rail projects use public-private partnerships that require political sponsorship and state guarantees; EU Connecting Europe Facility II allocates €33.7 billion to transport (2021–2027), shaping bankability and timelines for suppliers like Talgo. Talgo benefits when governments de-risk rolling-stock availability schemes; policy reversals can delay financial close and production schedules.

- PPPs need political guarantees

- CEF II €33.7bn influences project funding

- De-risking boosts Talgo order certainty

- Policy reversals stall financial close/production

Industrial policy and localization

Buy-local rules and industrial strategies strongly influence Talgos factory siting and supplier choices, with EU public procurement estimated at about 14% of GDP shaping tender conditions. Spain and several markets offer grants and tax incentives for domestic manufacturing and R&D, raising chances for local content requirements. To win larger tenders Talgo may need joint ventures or local assembly, increasing complexity but deepening market access.

- Buy-local pressure: alters supplier mix

- EU procurement ~14% GDP: high stakes

- Incentives: boost local R&D/manufacturing

- JV/local assembly: higher complexity, better access

EU TEN-T and Fit for 55 expand high-speed rail tenders; CEF II €33.7bn boosts bankability

EU TEN-T and Green Deal (Fit for 55: -55% GHG by 2030) prioritize high-speed/intercity tenders, enlarging Talgo’s EU pipeline; CEF II transport budget €33.7bn (2021–27) improves bankability. National buy-local rules and public procurement (~14% GDP) force localization/JV strategies. Export controls since 2022 raise compliance risk and can suspend deliveries.

| Factor | Impact | 2024/25 data |

|---|---|---|

| EU policy | More tenders | TEN-T core 2030 |

| Funding | De-risking | CEF II €33.7bn |

| Procurement | Localization | ~14% GDP |

What is included in the product

Explores how macro-environmental factors uniquely affect Talgo across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by current data and trends. Designed for executives and investors, the analysis reflects regional market and regulatory dynamics, includes forward-looking insights for scenario planning, and is formatted for direct use in reports and pitch decks.

Talgo PESTLE condenses geopolitical, regulatory, economic, social, technological and environmental factors into a clean, visually segmented summary for quick reference in meetings or presentations, easing external risk assessment and alignment across teams.

Economic factors

Interest rates and capex cycles

Higher interest rates (ECB deposit rate ~4.00% in mid‑2024) raise project financing costs and can delay fleet renewals, while rail capex is cyclical and sensitive to sovereign budgets and EU funding cycles; the Connecting Europe Facility allocates €33.7bn for 2021–2027 transport projects. Talgo’s long lead times (often 18–24 months) make resilient order backlogs critical. Lower rates would accelerate high‑speed corridor investments.

Commodity and energy costs

Steel (HRC ~€900/ton) and aluminum (LME ~€2,200/ton) plus EU industrial electricity (~€0.14/kWh) materially affect Talgo’s unit economics and margins, with raw materials and energy forming a major share of rolling-stock cost.

Talgo’s lightweight articulared designs can cut operator energy use by roughly 20–25%, strengthening its value proposition against rising fuel/electricity costs.

Hedging metal exposure and locking long-term supply contracts are critical to stabilize input costs and margin forecasts.

Commodity and energy volatility forces tighter pricing, higher warranty contingencies and more frequent contract renegotiations.

Exchange-rate exposure

Euro-based production and maintenance costs versus multi-currency revenues expose Talgo to FX risk, with over half of sales derived from exports to non-euro markets. Large export contracts (rolling stock and long-term maintenance) require hedging across production and lifecycle phases to protect margins. 2024 saw roughly 4–6% EUR swings versus major currencies, altering Talgo competitiveness in non-euro markets. Strategic localization of assembly and after-sales can partially offset FX mismatches.

Post-pandemic mobility demand

Passenger volumes are rebounding with a clear modal shift toward sustainable rail as EU policy targets moving 30% of road freight over 300 km to rail by 2030, bolstering demand for intercity and high-speed fleets. Intercity corridors show resilience versus short-haul air, supporting fleet expansions and refurbishments, though economic slowdowns could temper premium high-speed uptake.

- Trend: modal shift to rail

- Policy: 30% freight-to-rail by 2030

- Opportunity: fleet expansion/refurb

- Risk: slower premium HSR demand in downturns

Aftermarket and service annuities

Aftermarket and service annuities deliver stable, long-duration cash flows through multiyear maintenance contracts (commonly 10–20 years) that smooth Talgo's revenue between new-build cycles. Tight public budgets raise refurbishment demand as operators opt for mid-life over replacement. Growing digital monitoring increases service intensity and predictive-maintenance upsells, boosting recurring margins.

- Maintenance contracts: long-duration cash flows

- Refurbishment demand: rises in tight budgets

- Digital monitoring: increases service intensity

EU TEN-T and Fit for 55 expand high-speed rail tenders; CEF II €33.7bn boosts bankability

Higher ECB rates (~4.00% mid‑2024) raise financing costs; CEF transport funding €33.7bn (2021–27) supports orders. Steel HRC ~€900/t, Al ~€2,200/t and EU power ~€0.14/kWh compress margins; Talgo saves ~20–25% energy vs rivals. Exports >50% of sales; EUR moved ~4–6% in 2024, raising FX risk. Aftermarket annuities (10–20yr) and refurbishment demand cushion revenue.

| Metric | Value |

|---|---|

| ECB rate (mid‑2024) | ~4.00% |

| CEF transport (2021–27) | €33.7bn |

| HRC / Al / Power | €900/t • €2,200/t • €0.14/kWh |

| Energy saving | 20–25% |

| Export share | >50% |

| EUR volatility (2024) | 4–6% |

What You See Is What You Get

Talgo PESTLE Analysis

The Talgo PESTLE Analysis provides concise political, economic, social, technological, legal, and environmental insights specific to Talgo and its markets; the content and structure shown in the preview is the same document you’ll download after payment. It is fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological change are shaping Talgo's prospects in our concise PESTLE overview. This snapshot highlights key risks and opportunities to inform your strategy. Purchase the full, downloadable PESTLE for a detailed, actionable briefing now.

Political factors

EU rail policy and funding

EU rail policy channels priority via TEN-T (core network targets 2030, comprehensive 2050) and Green Deal goals (at least 55% GHG reduction by 2030), boosting high-speed and intercity tenders where Talgo competes. Harmonization initiatives simplify cross-border rolling stock approvals, underpinning a stable European pipeline for Talgo. A reallocation of EU budget priorities could delay project starts and cash flows.

Government procurement dynamics

National rail operators award multi-year contracts often worth €500m–€2bn and tied to policy goals and election cycles, with tender timing affecting delivery windows of 7–15 years. Specifications frequently mandate 30–60% local content or preferred technologies, so Talgo must align bids with national strategic plans and localization targets. Political turnover can abruptly reset priorities and pipeline forecasts, delaying or reshaping committed spend.

Geopolitical risk and sanctions

Talgo’s export markets can be constrained by sanctions and diplomatic tensions, notably since the 2022 EU/US measures that tightened controls on technology and transport-sector goods. Rolling stock and critical parts may face export controls to jurisdictions under embargo, forcing reroutes or cancelled sales. Talgo’s global maintenance footprint requires rigorous compliance screening to avoid fines and frozen receivables. Sudden sanctions can halt deliveries and delay payments across contracts.

Public-private partnership models

Many rail projects use public-private partnerships that require political sponsorship and state guarantees; EU Connecting Europe Facility II allocates €33.7 billion to transport (2021–2027), shaping bankability and timelines for suppliers like Talgo. Talgo benefits when governments de-risk rolling-stock availability schemes; policy reversals can delay financial close and production schedules.

- PPPs need political guarantees

- CEF II €33.7bn influences project funding

- De-risking boosts Talgo order certainty

- Policy reversals stall financial close/production

Industrial policy and localization

Buy-local rules and industrial strategies strongly influence Talgos factory siting and supplier choices, with EU public procurement estimated at about 14% of GDP shaping tender conditions. Spain and several markets offer grants and tax incentives for domestic manufacturing and R&D, raising chances for local content requirements. To win larger tenders Talgo may need joint ventures or local assembly, increasing complexity but deepening market access.

- Buy-local pressure: alters supplier mix

- EU procurement ~14% GDP: high stakes

- Incentives: boost local R&D/manufacturing

- JV/local assembly: higher complexity, better access

EU TEN-T and Fit for 55 expand high-speed rail tenders; CEF II €33.7bn boosts bankability

EU TEN-T and Green Deal (Fit for 55: -55% GHG by 2030) prioritize high-speed/intercity tenders, enlarging Talgo’s EU pipeline; CEF II transport budget €33.7bn (2021–27) improves bankability. National buy-local rules and public procurement (~14% GDP) force localization/JV strategies. Export controls since 2022 raise compliance risk and can suspend deliveries.

| Factor | Impact | 2024/25 data |

|---|---|---|

| EU policy | More tenders | TEN-T core 2030 |

| Funding | De-risking | CEF II €33.7bn |

| Procurement | Localization | ~14% GDP |

What is included in the product

Explores how macro-environmental factors uniquely affect Talgo across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by current data and trends. Designed for executives and investors, the analysis reflects regional market and regulatory dynamics, includes forward-looking insights for scenario planning, and is formatted for direct use in reports and pitch decks.

Talgo PESTLE condenses geopolitical, regulatory, economic, social, technological and environmental factors into a clean, visually segmented summary for quick reference in meetings or presentations, easing external risk assessment and alignment across teams.

Economic factors

Interest rates and capex cycles

Higher interest rates (ECB deposit rate ~4.00% in mid‑2024) raise project financing costs and can delay fleet renewals, while rail capex is cyclical and sensitive to sovereign budgets and EU funding cycles; the Connecting Europe Facility allocates €33.7bn for 2021–2027 transport projects. Talgo’s long lead times (often 18–24 months) make resilient order backlogs critical. Lower rates would accelerate high‑speed corridor investments.

Commodity and energy costs

Steel (HRC ~€900/ton) and aluminum (LME ~€2,200/ton) plus EU industrial electricity (~€0.14/kWh) materially affect Talgo’s unit economics and margins, with raw materials and energy forming a major share of rolling-stock cost.

Talgo’s lightweight articulared designs can cut operator energy use by roughly 20–25%, strengthening its value proposition against rising fuel/electricity costs.

Hedging metal exposure and locking long-term supply contracts are critical to stabilize input costs and margin forecasts.

Commodity and energy volatility forces tighter pricing, higher warranty contingencies and more frequent contract renegotiations.

Exchange-rate exposure

Euro-based production and maintenance costs versus multi-currency revenues expose Talgo to FX risk, with over half of sales derived from exports to non-euro markets. Large export contracts (rolling stock and long-term maintenance) require hedging across production and lifecycle phases to protect margins. 2024 saw roughly 4–6% EUR swings versus major currencies, altering Talgo competitiveness in non-euro markets. Strategic localization of assembly and after-sales can partially offset FX mismatches.

Post-pandemic mobility demand

Passenger volumes are rebounding with a clear modal shift toward sustainable rail as EU policy targets moving 30% of road freight over 300 km to rail by 2030, bolstering demand for intercity and high-speed fleets. Intercity corridors show resilience versus short-haul air, supporting fleet expansions and refurbishments, though economic slowdowns could temper premium high-speed uptake.

- Trend: modal shift to rail

- Policy: 30% freight-to-rail by 2030

- Opportunity: fleet expansion/refurb

- Risk: slower premium HSR demand in downturns

Aftermarket and service annuities

Aftermarket and service annuities deliver stable, long-duration cash flows through multiyear maintenance contracts (commonly 10–20 years) that smooth Talgo's revenue between new-build cycles. Tight public budgets raise refurbishment demand as operators opt for mid-life over replacement. Growing digital monitoring increases service intensity and predictive-maintenance upsells, boosting recurring margins.

- Maintenance contracts: long-duration cash flows

- Refurbishment demand: rises in tight budgets

- Digital monitoring: increases service intensity

EU TEN-T and Fit for 55 expand high-speed rail tenders; CEF II €33.7bn boosts bankability

Higher ECB rates (~4.00% mid‑2024) raise financing costs; CEF transport funding €33.7bn (2021–27) supports orders. Steel HRC ~€900/t, Al ~€2,200/t and EU power ~€0.14/kWh compress margins; Talgo saves ~20–25% energy vs rivals. Exports >50% of sales; EUR moved ~4–6% in 2024, raising FX risk. Aftermarket annuities (10–20yr) and refurbishment demand cushion revenue.

| Metric | Value |

|---|---|

| ECB rate (mid‑2024) | ~4.00% |

| CEF transport (2021–27) | €33.7bn |

| HRC / Al / Power | €900/t • €2,200/t • €0.14/kWh |

| Energy saving | 20–25% |

| Export share | >50% |

| EUR volatility (2024) | 4–6% |

What You See Is What You Get

Talgo PESTLE Analysis

The Talgo PESTLE Analysis provides concise political, economic, social, technological, legal, and environmental insights specific to Talgo and its markets; the content and structure shown in the preview is the same document you’ll download after payment. It is fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological change are shaping Talgo's prospects in our concise PESTLE overview. This snapshot highlights key risks and opportunities to inform your strategy. Purchase the full, downloadable PESTLE for a detailed, actionable briefing now.

Political factors

EU rail policy and funding

EU rail policy channels priority via TEN-T (core network targets 2030, comprehensive 2050) and Green Deal goals (at least 55% GHG reduction by 2030), boosting high-speed and intercity tenders where Talgo competes. Harmonization initiatives simplify cross-border rolling stock approvals, underpinning a stable European pipeline for Talgo. A reallocation of EU budget priorities could delay project starts and cash flows.

Government procurement dynamics

National rail operators award multi-year contracts often worth €500m–€2bn and tied to policy goals and election cycles, with tender timing affecting delivery windows of 7–15 years. Specifications frequently mandate 30–60% local content or preferred technologies, so Talgo must align bids with national strategic plans and localization targets. Political turnover can abruptly reset priorities and pipeline forecasts, delaying or reshaping committed spend.

Geopolitical risk and sanctions

Talgo’s export markets can be constrained by sanctions and diplomatic tensions, notably since the 2022 EU/US measures that tightened controls on technology and transport-sector goods. Rolling stock and critical parts may face export controls to jurisdictions under embargo, forcing reroutes or cancelled sales. Talgo’s global maintenance footprint requires rigorous compliance screening to avoid fines and frozen receivables. Sudden sanctions can halt deliveries and delay payments across contracts.

Public-private partnership models

Many rail projects use public-private partnerships that require political sponsorship and state guarantees; EU Connecting Europe Facility II allocates €33.7 billion to transport (2021–2027), shaping bankability and timelines for suppliers like Talgo. Talgo benefits when governments de-risk rolling-stock availability schemes; policy reversals can delay financial close and production schedules.

- PPPs need political guarantees

- CEF II €33.7bn influences project funding

- De-risking boosts Talgo order certainty

- Policy reversals stall financial close/production

Industrial policy and localization

Buy-local rules and industrial strategies strongly influence Talgos factory siting and supplier choices, with EU public procurement estimated at about 14% of GDP shaping tender conditions. Spain and several markets offer grants and tax incentives for domestic manufacturing and R&D, raising chances for local content requirements. To win larger tenders Talgo may need joint ventures or local assembly, increasing complexity but deepening market access.

- Buy-local pressure: alters supplier mix

- EU procurement ~14% GDP: high stakes

- Incentives: boost local R&D/manufacturing

- JV/local assembly: higher complexity, better access

EU TEN-T and Fit for 55 expand high-speed rail tenders; CEF II €33.7bn boosts bankability

EU TEN-T and Green Deal (Fit for 55: -55% GHG by 2030) prioritize high-speed/intercity tenders, enlarging Talgo’s EU pipeline; CEF II transport budget €33.7bn (2021–27) improves bankability. National buy-local rules and public procurement (~14% GDP) force localization/JV strategies. Export controls since 2022 raise compliance risk and can suspend deliveries.

| Factor | Impact | 2024/25 data |

|---|---|---|

| EU policy | More tenders | TEN-T core 2030 |

| Funding | De-risking | CEF II €33.7bn |

| Procurement | Localization | ~14% GDP |

What is included in the product

Explores how macro-environmental factors uniquely affect Talgo across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by current data and trends. Designed for executives and investors, the analysis reflects regional market and regulatory dynamics, includes forward-looking insights for scenario planning, and is formatted for direct use in reports and pitch decks.

Talgo PESTLE condenses geopolitical, regulatory, economic, social, technological and environmental factors into a clean, visually segmented summary for quick reference in meetings or presentations, easing external risk assessment and alignment across teams.

Economic factors

Interest rates and capex cycles

Higher interest rates (ECB deposit rate ~4.00% in mid‑2024) raise project financing costs and can delay fleet renewals, while rail capex is cyclical and sensitive to sovereign budgets and EU funding cycles; the Connecting Europe Facility allocates €33.7bn for 2021–2027 transport projects. Talgo’s long lead times (often 18–24 months) make resilient order backlogs critical. Lower rates would accelerate high‑speed corridor investments.

Commodity and energy costs

Steel (HRC ~€900/ton) and aluminum (LME ~€2,200/ton) plus EU industrial electricity (~€0.14/kWh) materially affect Talgo’s unit economics and margins, with raw materials and energy forming a major share of rolling-stock cost.

Talgo’s lightweight articulared designs can cut operator energy use by roughly 20–25%, strengthening its value proposition against rising fuel/electricity costs.

Hedging metal exposure and locking long-term supply contracts are critical to stabilize input costs and margin forecasts.

Commodity and energy volatility forces tighter pricing, higher warranty contingencies and more frequent contract renegotiations.

Exchange-rate exposure

Euro-based production and maintenance costs versus multi-currency revenues expose Talgo to FX risk, with over half of sales derived from exports to non-euro markets. Large export contracts (rolling stock and long-term maintenance) require hedging across production and lifecycle phases to protect margins. 2024 saw roughly 4–6% EUR swings versus major currencies, altering Talgo competitiveness in non-euro markets. Strategic localization of assembly and after-sales can partially offset FX mismatches.

Post-pandemic mobility demand

Passenger volumes are rebounding with a clear modal shift toward sustainable rail as EU policy targets moving 30% of road freight over 300 km to rail by 2030, bolstering demand for intercity and high-speed fleets. Intercity corridors show resilience versus short-haul air, supporting fleet expansions and refurbishments, though economic slowdowns could temper premium high-speed uptake.

- Trend: modal shift to rail

- Policy: 30% freight-to-rail by 2030

- Opportunity: fleet expansion/refurb

- Risk: slower premium HSR demand in downturns

Aftermarket and service annuities

Aftermarket and service annuities deliver stable, long-duration cash flows through multiyear maintenance contracts (commonly 10–20 years) that smooth Talgo's revenue between new-build cycles. Tight public budgets raise refurbishment demand as operators opt for mid-life over replacement. Growing digital monitoring increases service intensity and predictive-maintenance upsells, boosting recurring margins.

- Maintenance contracts: long-duration cash flows

- Refurbishment demand: rises in tight budgets

- Digital monitoring: increases service intensity

EU TEN-T and Fit for 55 expand high-speed rail tenders; CEF II €33.7bn boosts bankability

Higher ECB rates (~4.00% mid‑2024) raise financing costs; CEF transport funding €33.7bn (2021–27) supports orders. Steel HRC ~€900/t, Al ~€2,200/t and EU power ~€0.14/kWh compress margins; Talgo saves ~20–25% energy vs rivals. Exports >50% of sales; EUR moved ~4–6% in 2024, raising FX risk. Aftermarket annuities (10–20yr) and refurbishment demand cushion revenue.

| Metric | Value |

|---|---|

| ECB rate (mid‑2024) | ~4.00% |

| CEF transport (2021–27) | €33.7bn |

| HRC / Al / Power | €900/t • €2,200/t • €0.14/kWh |

| Energy saving | 20–25% |

| Export share | >50% |

| EUR volatility (2024) | 4–6% |

What You See Is What You Get

Talgo PESTLE Analysis

The Talgo PESTLE Analysis provides concise political, economic, social, technological, legal, and environmental insights specific to Talgo and its markets; the content and structure shown in the preview is the same document you’ll download after payment. It is fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.