Tata Consumer Products Porter's Five Forces Analysis

From Overview to Strategy Blueprint

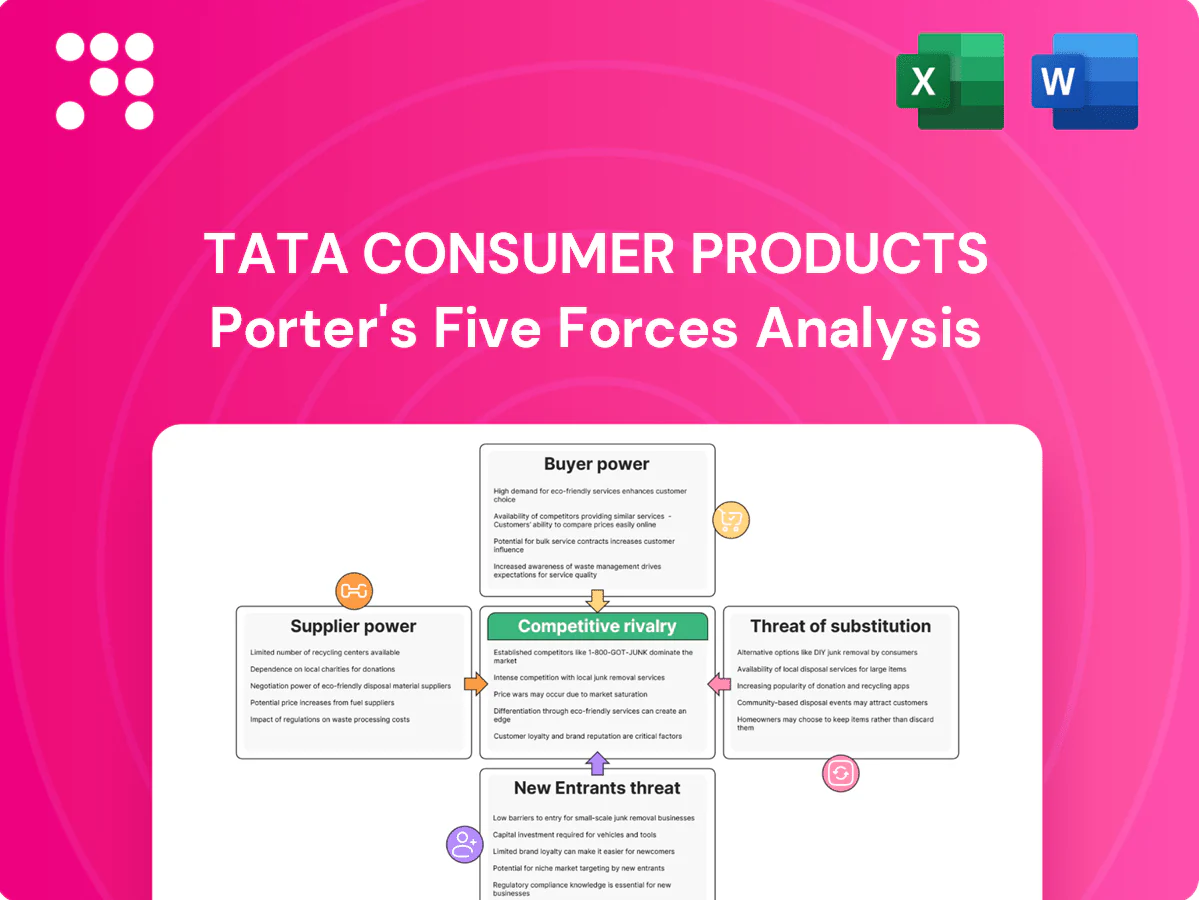

Tata Consumer Products faces moderate supplier power, strong buyer expectations, and competitive rivalry across tea, coffee, and branded foods; this snapshot uncovers key pressure points and strategic levers. Want the full picture? Purchase the complete Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Commodity input concentration

Tea, coffee and spices for Tata Consumer Products come from limited agro-climatic zones such as Assam, Nilgiris, Darjeeling and select coffee belts, with Darjeeling contributing under 1% of India’s tea volume; weather volatility (floods/droughts in 2023–24) and geopolitical shocks tighten availability and lift auction/prices, while certified and specialty grades (organic, single-origin) shrink supplier pools, increasing supplier leverage during crop shortages.

Farmer fragmentation vs aggregator influence

Millions of smallholders—over 1.2 million tea smallholders in India and roughly 400,000 coffee growers nationally—supply crops but often sell via auctions, estates and traders. Intermediaries and organized estates can coordinate pricing and quality, raising supplier bargaining power. Tea auction mechanisms compress transparency and pass price volatility to buyers. Long-term direct-procurement and agronomy programs can partly offset this power.

Switching costs on quality and provenance

Blends rely on origin, leaf grade and flavor profile, so rapid supplier switching risks noticeable taste shifts that can erode brand equity. Reformulating with new sources to maintain consistency is costly and time-consuming, constraining procurement flexibility. Certification requirements like Rainforest Alliance or Fairtrade further narrow eligible suppliers, strengthening suppliers' bargaining power.

Packaging and logistics dependencies

Packaging and logistics dependencies give suppliers episodic but material power: resins, paperboard, glass and aluminum supply chains remain cyclical and at times consolidated, amplifying price pass-through to Tata Consumer Products; freight and container market volatility drives cost spikes on export lanes; changing packaging specs requires revalidation and tooling, raising switching barriers.

Mitigants via scale and integration

Tata Consumer Products leverages scale and multi-origin sourcing plus hedging to dampen spot shocks; FY24 consolidated revenue ~₹13,000 crore supports purchasing leverage and diversification. Backward linkages via Tata Coffee, long-term contracts and supplier development improve availability and resilience. Dual-sourcing and localized packing reduce bottlenecks, lowering average supplier power across cycles.

- Scale: diversified procurement across origins

- Integration: Tata Coffee backward linkages

- Contracts: long-term agreements improve availability

- Operations: dual-sourcing and local packing cut bottlenecks

Concentrated origins, weather shocks vs scale: FY24 revenue ₹13,000 crore

Suppliers hold episodic power due to concentrated origins, weather shocks (2023–24 floods/droughts) and certified/specialty supply limits; millions of smallholders (tea 1.2M, coffee 400k) sell via auctions/intermediaries, raising price transmission; TataCP scale (FY24 revenue ~₹13,000 crore), Tata Coffee integration, long-term contracts and dual-sourcing reduce net supplier leverage.

| Metric | 2024 value |

|---|---|

| FY24 revenue | ₹13,000 crore |

| Tea smallholders | 1.2M |

| Coffee growers | 400k |

| Darjeeling share | <1% |

What is included in the product

Concise Porter's Five Forces assessment of Tata Consumer Products, highlighting competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying strategic levers and emerging disruptors shaping its market position.

One-sheet Porter's Five Forces for Tata Consumer Products that pinpoints supplier/buyer power, competitive rivalry, and threats of entry/substitution—perfect for quick strategic decisions, pitch decks, and boardroom clarity.

Customers Bargaining Power

Retailer and e-commerce gatekeepers

Modern trade, quick-commerce and marketplaces extract margins, promo funding and shelf fees—platform commissions commonly range 8–27%—giving buyers leverage and enabling private-label expansion using superior shopper data. Delisting or loss of visibility can slash category sales, increasing dependence on gatekeepers, while strong Tata Consumer brands retain pricing power but must spend heavily on activation and platform promo funding to secure space.

Highly price-sensitive end consumers

Staples like salt, pulses and tea show high price elasticity; during 2023-24 inflationary pressure (food CPI ~8% in 2023) consumers downtrade to lower tiers, squeezing Tata Consumer Products price realization. Unit-size engineering and value packs mitigate losses but do not fully offset elasticity. Promotions and trade packs, often involving 5-7% effective discounts, are frequently used to defend share.

Low switching costs across brands

Comparable taste profiles and ubiquitous retail and online availability make brand switching easy for Tata Consumer Products consumers, while e-commerce and modern trade—accounting for roughly 6–8% of FMCG sales in India in 2024—amplify assortment visibility.

Online reviews and social proof accelerate trial and reduce search frictions; even with loyalty programs and heritage brands, loyalty is fragile in commoditized tea/coffee segments.

These dynamics keep buyer bargaining power structurally high for TCP, pressuring pricing and margin resilience.

Private label alternatives

Retailers increasingly push private labels in tea, coffee, bottled water and staples at lower price points, narrowing perceived gaps with national brands through improved formulations and packaging; Euromonitor estimated Indian FMCG private label share near 6% in 2024. Shelf prioritization and algorithmic e-commerce placement favor own brands, expanding buyer choice and strengthening customer bargaining power against Tata Consumer Products.

- Private label share ~6% (2024)

- Higher shelf/algorithmic visibility

- Price-driven switching increases buyer leverage

Mitigants from brand equity and portfolios

Iconic brands like Tata Tea and Tetley, health credentials and consistent quality curb switching; Tata Consumer reported consolidated revenue of INR 10,108 crore in FY2024, supporting premium pricing and moderating buyer leverage.

- Brand strength: ~27% branded tea market share (India)

- Portfolio bundling: strengthens trade negotiation

- D2C & loyalty: direct consumer relationships

- Impact: lowers buyer power in premium/differentiated segments

Platform fees force promos; staples pressured; INR 10,108

Buyers have high leverage: platform commissions 8–27% and delisting risks force heavy promo spend despite Tata Consumer’s premium positioning. Staples show high elasticity (food CPI ~8% in 2023), e-comm share 6–8% (2024) and private-label ~6% (2024), pressuring pricing. Tata Consumer revenue INR 10,108 crore (FY2024) and ~27% branded tea share sustain some pricing power.

| Metric | 2023–24 |

|---|---|

| Platform commissions | 8–27% |

| Food CPI | ~8% |

| E‑commerce FMCG share | 6–8% |

| Private label share | ~6% |

| Tata Consumer rev | INR 10,108 crore |

| Branded tea share | ~27% |

Preview the Actual Deliverable

Tata Consumer Products Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces Analysis of Tata Consumer Products you’ll receive—no samples or placeholders. The document is fully formatted and ready for use, covering competitive rivalry, supplier and buyer power, threats of entry and substitutes. Once purchased, you get this same file instantly.

From Overview to Strategy Blueprint

Tata Consumer Products faces moderate supplier power, strong buyer expectations, and competitive rivalry across tea, coffee, and branded foods; this snapshot uncovers key pressure points and strategic levers. Want the full picture? Purchase the complete Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Commodity input concentration

Tea, coffee and spices for Tata Consumer Products come from limited agro-climatic zones such as Assam, Nilgiris, Darjeeling and select coffee belts, with Darjeeling contributing under 1% of India’s tea volume; weather volatility (floods/droughts in 2023–24) and geopolitical shocks tighten availability and lift auction/prices, while certified and specialty grades (organic, single-origin) shrink supplier pools, increasing supplier leverage during crop shortages.

Farmer fragmentation vs aggregator influence

Millions of smallholders—over 1.2 million tea smallholders in India and roughly 400,000 coffee growers nationally—supply crops but often sell via auctions, estates and traders. Intermediaries and organized estates can coordinate pricing and quality, raising supplier bargaining power. Tea auction mechanisms compress transparency and pass price volatility to buyers. Long-term direct-procurement and agronomy programs can partly offset this power.

Switching costs on quality and provenance

Blends rely on origin, leaf grade and flavor profile, so rapid supplier switching risks noticeable taste shifts that can erode brand equity. Reformulating with new sources to maintain consistency is costly and time-consuming, constraining procurement flexibility. Certification requirements like Rainforest Alliance or Fairtrade further narrow eligible suppliers, strengthening suppliers' bargaining power.

Packaging and logistics dependencies

Packaging and logistics dependencies give suppliers episodic but material power: resins, paperboard, glass and aluminum supply chains remain cyclical and at times consolidated, amplifying price pass-through to Tata Consumer Products; freight and container market volatility drives cost spikes on export lanes; changing packaging specs requires revalidation and tooling, raising switching barriers.

Mitigants via scale and integration

Tata Consumer Products leverages scale and multi-origin sourcing plus hedging to dampen spot shocks; FY24 consolidated revenue ~₹13,000 crore supports purchasing leverage and diversification. Backward linkages via Tata Coffee, long-term contracts and supplier development improve availability and resilience. Dual-sourcing and localized packing reduce bottlenecks, lowering average supplier power across cycles.

- Scale: diversified procurement across origins

- Integration: Tata Coffee backward linkages

- Contracts: long-term agreements improve availability

- Operations: dual-sourcing and local packing cut bottlenecks

Concentrated origins, weather shocks vs scale: FY24 revenue ₹13,000 crore

Suppliers hold episodic power due to concentrated origins, weather shocks (2023–24 floods/droughts) and certified/specialty supply limits; millions of smallholders (tea 1.2M, coffee 400k) sell via auctions/intermediaries, raising price transmission; TataCP scale (FY24 revenue ~₹13,000 crore), Tata Coffee integration, long-term contracts and dual-sourcing reduce net supplier leverage.

| Metric | 2024 value |

|---|---|

| FY24 revenue | ₹13,000 crore |

| Tea smallholders | 1.2M |

| Coffee growers | 400k |

| Darjeeling share | <1% |

What is included in the product

Concise Porter's Five Forces assessment of Tata Consumer Products, highlighting competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying strategic levers and emerging disruptors shaping its market position.

One-sheet Porter's Five Forces for Tata Consumer Products that pinpoints supplier/buyer power, competitive rivalry, and threats of entry/substitution—perfect for quick strategic decisions, pitch decks, and boardroom clarity.

Customers Bargaining Power

Retailer and e-commerce gatekeepers

Modern trade, quick-commerce and marketplaces extract margins, promo funding and shelf fees—platform commissions commonly range 8–27%—giving buyers leverage and enabling private-label expansion using superior shopper data. Delisting or loss of visibility can slash category sales, increasing dependence on gatekeepers, while strong Tata Consumer brands retain pricing power but must spend heavily on activation and platform promo funding to secure space.

Highly price-sensitive end consumers

Staples like salt, pulses and tea show high price elasticity; during 2023-24 inflationary pressure (food CPI ~8% in 2023) consumers downtrade to lower tiers, squeezing Tata Consumer Products price realization. Unit-size engineering and value packs mitigate losses but do not fully offset elasticity. Promotions and trade packs, often involving 5-7% effective discounts, are frequently used to defend share.

Low switching costs across brands

Comparable taste profiles and ubiquitous retail and online availability make brand switching easy for Tata Consumer Products consumers, while e-commerce and modern trade—accounting for roughly 6–8% of FMCG sales in India in 2024—amplify assortment visibility.

Online reviews and social proof accelerate trial and reduce search frictions; even with loyalty programs and heritage brands, loyalty is fragile in commoditized tea/coffee segments.

These dynamics keep buyer bargaining power structurally high for TCP, pressuring pricing and margin resilience.

Private label alternatives

Retailers increasingly push private labels in tea, coffee, bottled water and staples at lower price points, narrowing perceived gaps with national brands through improved formulations and packaging; Euromonitor estimated Indian FMCG private label share near 6% in 2024. Shelf prioritization and algorithmic e-commerce placement favor own brands, expanding buyer choice and strengthening customer bargaining power against Tata Consumer Products.

- Private label share ~6% (2024)

- Higher shelf/algorithmic visibility

- Price-driven switching increases buyer leverage

Mitigants from brand equity and portfolios

Iconic brands like Tata Tea and Tetley, health credentials and consistent quality curb switching; Tata Consumer reported consolidated revenue of INR 10,108 crore in FY2024, supporting premium pricing and moderating buyer leverage.

- Brand strength: ~27% branded tea market share (India)

- Portfolio bundling: strengthens trade negotiation

- D2C & loyalty: direct consumer relationships

- Impact: lowers buyer power in premium/differentiated segments

Platform fees force promos; staples pressured; INR 10,108

Buyers have high leverage: platform commissions 8–27% and delisting risks force heavy promo spend despite Tata Consumer’s premium positioning. Staples show high elasticity (food CPI ~8% in 2023), e-comm share 6–8% (2024) and private-label ~6% (2024), pressuring pricing. Tata Consumer revenue INR 10,108 crore (FY2024) and ~27% branded tea share sustain some pricing power.

| Metric | 2023–24 |

|---|---|

| Platform commissions | 8–27% |

| Food CPI | ~8% |

| E‑commerce FMCG share | 6–8% |

| Private label share | ~6% |

| Tata Consumer rev | INR 10,108 crore |

| Branded tea share | ~27% |

Preview the Actual Deliverable

Tata Consumer Products Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces Analysis of Tata Consumer Products you’ll receive—no samples or placeholders. The document is fully formatted and ready for use, covering competitive rivalry, supplier and buyer power, threats of entry and substitutes. Once purchased, you get this same file instantly.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Tata Consumer Products faces moderate supplier power, strong buyer expectations, and competitive rivalry across tea, coffee, and branded foods; this snapshot uncovers key pressure points and strategic levers. Want the full picture? Purchase the complete Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Commodity input concentration

Tea, coffee and spices for Tata Consumer Products come from limited agro-climatic zones such as Assam, Nilgiris, Darjeeling and select coffee belts, with Darjeeling contributing under 1% of India’s tea volume; weather volatility (floods/droughts in 2023–24) and geopolitical shocks tighten availability and lift auction/prices, while certified and specialty grades (organic, single-origin) shrink supplier pools, increasing supplier leverage during crop shortages.

Farmer fragmentation vs aggregator influence

Millions of smallholders—over 1.2 million tea smallholders in India and roughly 400,000 coffee growers nationally—supply crops but often sell via auctions, estates and traders. Intermediaries and organized estates can coordinate pricing and quality, raising supplier bargaining power. Tea auction mechanisms compress transparency and pass price volatility to buyers. Long-term direct-procurement and agronomy programs can partly offset this power.

Switching costs on quality and provenance

Blends rely on origin, leaf grade and flavor profile, so rapid supplier switching risks noticeable taste shifts that can erode brand equity. Reformulating with new sources to maintain consistency is costly and time-consuming, constraining procurement flexibility. Certification requirements like Rainforest Alliance or Fairtrade further narrow eligible suppliers, strengthening suppliers' bargaining power.

Packaging and logistics dependencies

Packaging and logistics dependencies give suppliers episodic but material power: resins, paperboard, glass and aluminum supply chains remain cyclical and at times consolidated, amplifying price pass-through to Tata Consumer Products; freight and container market volatility drives cost spikes on export lanes; changing packaging specs requires revalidation and tooling, raising switching barriers.

Mitigants via scale and integration

Tata Consumer Products leverages scale and multi-origin sourcing plus hedging to dampen spot shocks; FY24 consolidated revenue ~₹13,000 crore supports purchasing leverage and diversification. Backward linkages via Tata Coffee, long-term contracts and supplier development improve availability and resilience. Dual-sourcing and localized packing reduce bottlenecks, lowering average supplier power across cycles.

- Scale: diversified procurement across origins

- Integration: Tata Coffee backward linkages

- Contracts: long-term agreements improve availability

- Operations: dual-sourcing and local packing cut bottlenecks

Concentrated origins, weather shocks vs scale: FY24 revenue ₹13,000 crore

Suppliers hold episodic power due to concentrated origins, weather shocks (2023–24 floods/droughts) and certified/specialty supply limits; millions of smallholders (tea 1.2M, coffee 400k) sell via auctions/intermediaries, raising price transmission; TataCP scale (FY24 revenue ~₹13,000 crore), Tata Coffee integration, long-term contracts and dual-sourcing reduce net supplier leverage.

| Metric | 2024 value |

|---|---|

| FY24 revenue | ₹13,000 crore |

| Tea smallholders | 1.2M |

| Coffee growers | 400k |

| Darjeeling share | <1% |

What is included in the product

Concise Porter's Five Forces assessment of Tata Consumer Products, highlighting competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying strategic levers and emerging disruptors shaping its market position.

One-sheet Porter's Five Forces for Tata Consumer Products that pinpoints supplier/buyer power, competitive rivalry, and threats of entry/substitution—perfect for quick strategic decisions, pitch decks, and boardroom clarity.

Customers Bargaining Power

Retailer and e-commerce gatekeepers

Modern trade, quick-commerce and marketplaces extract margins, promo funding and shelf fees—platform commissions commonly range 8–27%—giving buyers leverage and enabling private-label expansion using superior shopper data. Delisting or loss of visibility can slash category sales, increasing dependence on gatekeepers, while strong Tata Consumer brands retain pricing power but must spend heavily on activation and platform promo funding to secure space.

Highly price-sensitive end consumers

Staples like salt, pulses and tea show high price elasticity; during 2023-24 inflationary pressure (food CPI ~8% in 2023) consumers downtrade to lower tiers, squeezing Tata Consumer Products price realization. Unit-size engineering and value packs mitigate losses but do not fully offset elasticity. Promotions and trade packs, often involving 5-7% effective discounts, are frequently used to defend share.

Low switching costs across brands

Comparable taste profiles and ubiquitous retail and online availability make brand switching easy for Tata Consumer Products consumers, while e-commerce and modern trade—accounting for roughly 6–8% of FMCG sales in India in 2024—amplify assortment visibility.

Online reviews and social proof accelerate trial and reduce search frictions; even with loyalty programs and heritage brands, loyalty is fragile in commoditized tea/coffee segments.

These dynamics keep buyer bargaining power structurally high for TCP, pressuring pricing and margin resilience.

Private label alternatives

Retailers increasingly push private labels in tea, coffee, bottled water and staples at lower price points, narrowing perceived gaps with national brands through improved formulations and packaging; Euromonitor estimated Indian FMCG private label share near 6% in 2024. Shelf prioritization and algorithmic e-commerce placement favor own brands, expanding buyer choice and strengthening customer bargaining power against Tata Consumer Products.

- Private label share ~6% (2024)

- Higher shelf/algorithmic visibility

- Price-driven switching increases buyer leverage

Mitigants from brand equity and portfolios

Iconic brands like Tata Tea and Tetley, health credentials and consistent quality curb switching; Tata Consumer reported consolidated revenue of INR 10,108 crore in FY2024, supporting premium pricing and moderating buyer leverage.

- Brand strength: ~27% branded tea market share (India)

- Portfolio bundling: strengthens trade negotiation

- D2C & loyalty: direct consumer relationships

- Impact: lowers buyer power in premium/differentiated segments

Platform fees force promos; staples pressured; INR 10,108

Buyers have high leverage: platform commissions 8–27% and delisting risks force heavy promo spend despite Tata Consumer’s premium positioning. Staples show high elasticity (food CPI ~8% in 2023), e-comm share 6–8% (2024) and private-label ~6% (2024), pressuring pricing. Tata Consumer revenue INR 10,108 crore (FY2024) and ~27% branded tea share sustain some pricing power.

| Metric | 2023–24 |

|---|---|

| Platform commissions | 8–27% |

| Food CPI | ~8% |

| E‑commerce FMCG share | 6–8% |

| Private label share | ~6% |

| Tata Consumer rev | INR 10,108 crore |

| Branded tea share | ~27% |

Preview the Actual Deliverable

Tata Consumer Products Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces Analysis of Tata Consumer Products you’ll receive—no samples or placeholders. The document is fully formatted and ready for use, covering competitive rivalry, supplier and buyer power, threats of entry and substitutes. Once purchased, you get this same file instantly.