Tata Consumer Products PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our concise PESTLE Analysis of Tata Consumer Products—highlighting political, economic, social, technological, legal, and environmental forces shaping its outlook. Use these insights to anticipate risks and spot growth opportunities across markets. Purchase the full report for the complete, ready-to-use analysis and actionable recommendations.

Political factors

Agri and food policy shifts

Government controls on tea, coffee, pulses and spices directly affect input costs and availability; the Centre's PLI for food processing (outlay INR 10,900 crore) can reduce capex pressure for processing and packaging investments.

Periodic changes in MSP, procurement norms or subsidies materially alter sourcing economics and margins, given Tata Consumer's reliance on contracted and spot procurement.

Sudden policy reversals or export/import curbs heighten planning risk across categories, impacting inventory, pricing and supplier contracts.

Trade tariffs and import-export rules

Customs duties on raw tea, coffee, packaging and additives directly squeeze gross margins for Tata Consumer Products, which reported consolidated revenue of INR 13,214 crore in FY24, making even small tariff shifts material. Export incentives or barriers, including RoDTEP credits and destination tariffs, alter global routing and pricing strategies. Non-tariff measures such as random quality inspections can delay shipments by days, raising logistic costs. Diversifying sourcing across India, Kenya and Vietnam reduces country-specific tariff shocks.

Geopolitical and logistics stability

Geopolitical and logistics instability—disruptions in Straits like Malacca (which carries roughly one-third of global trade) and port blockages can raise delivery times and costs for Tata Consumer. Political unrest in origin countries such as Kenya or Sri Lanka can curb harvests and exports, tightening supplies. Currency controls and sanctions (eg post-2022 regimes) complicate payments and hedging. Expanding multi-origin sourcing across India, Kenya and Sri Lanka lowers concentration risk.

Public health and nutrition agendas

Government drives on salt reduction, sugar limits and mandatory fortification are forcing reformulation: WHO targets a 30% relative reduction in population salt intake by 2025 and recommends free sugars <10% of energy, while school and workplace nutrition programs shift procurement toward lower-sodium/sugar SKUs; front-of-pack labelling adoption is reshaping purchase decisions and proactive compliance can convert regulation into brand trust and sales resilience.

- Policy: WHO 30% salt reduction by 2025

- Sugar: WHO <10% energy from free sugars

- Programs: schools/workplaces drive healthier SKUs

- Labeling: FOP rules alter choice; compliance = brand trust

Local governance and incentives

- State approvals: single-window/permits

- Land & water: allocation limits affect capacity

- Municipal standards: CPCB/FSSAI compliance costs

- Infrastructure: Rs 11.1 lakh crore capex expands distribution

- Govt relations: de-risks expansions

PLI INR 10,900 cr, tariffs/NTMs and WHO -30% salt reshape food margins

Government controls (PLI INR 10,900 crore) and MSP/procurement shifts materially affect input costs and capex economics for Tata Consumer (consol revenue INR 13,214 crore FY24). Tariff and non‑tariff measures alter margins and logistics; multi‑origin sourcing (India, Kenya, Vietnam, Sri Lanka) reduces concentration risk. Nutrition policies (WHO salt/sugar targets) force reformulation and labeling compliance, affecting SKUs and procurement.

| Factor | Impact | Key data |

|---|---|---|

| PLI | Capex support | INR 10,900 cr |

| Tariffs/NTMs | Margin risk | Revenue INR 13,214 cr (FY24) |

| Nutrition regs | Reformulation cost | WHO salt target -30% by 2025 |

What is included in the product

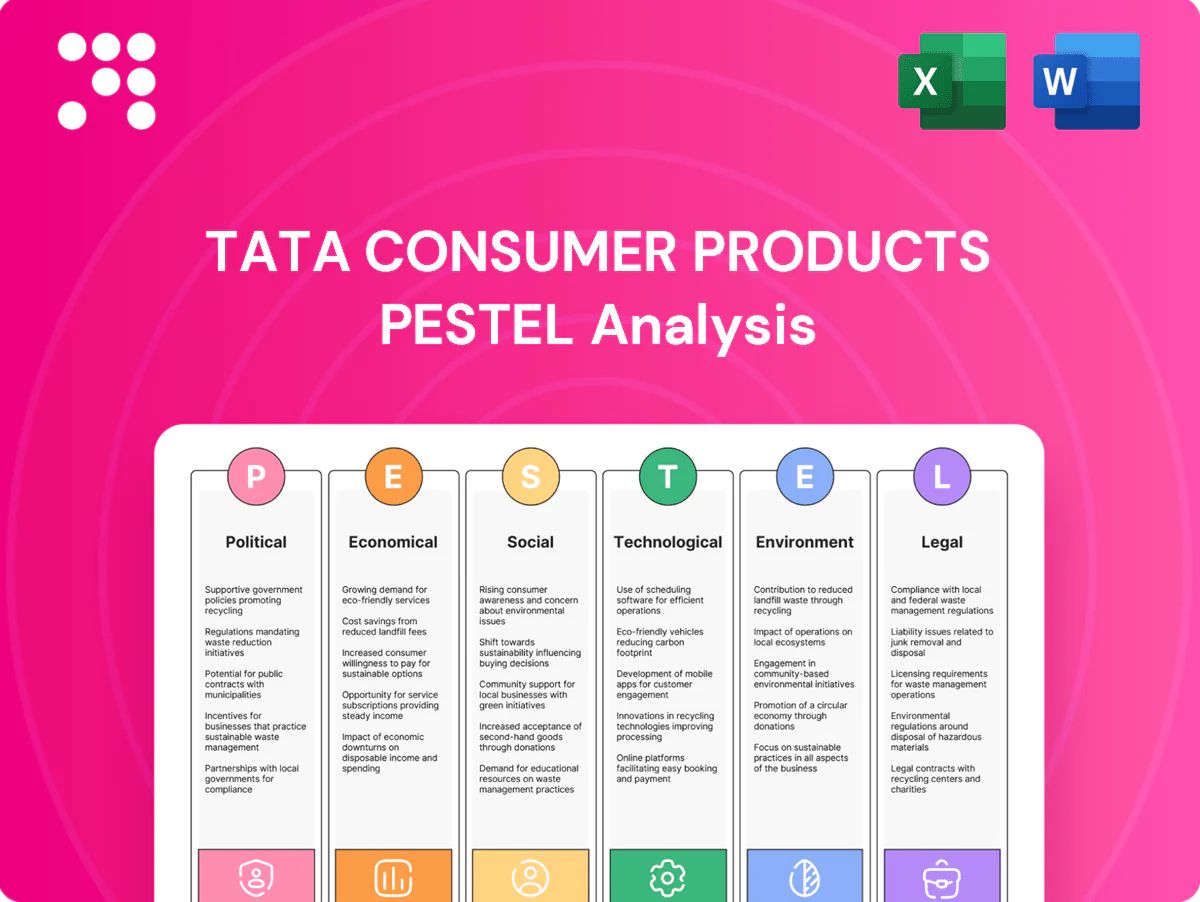

Explores how external macro-environmental factors uniquely affect Tata Consumer Products across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with each section backed by current data and trends. Designed to help executives and investors identify actionable risks and opportunities for strategic planning.

Clean, summarized PESTLE of Tata Consumer Products, visually segmented for quick interpretation and easily dropped into presentations or shared across teams to streamline external risk and market-position discussions.

Economic factors

Commodity price volatility

Tea, coffee and spice prices are cyclical and weather-sensitive, directly inflating TCPL’s COGS during supply shocks; India tea auctions and arabica/robusta swings drove input cost volatility in 2024. Long-term contracts and hedging programs mitigate but do not eliminate spikes, leaving residual exposure in quarterly margins. Passing costs through depends on brand strength and timing; Tata Consumer’s FY24 consolidated revenue of INR 12,338 crore provided pricing power and scale, while a diversified portfolio across beverages and spices buffers single-commodity shocks.

Inflation and consumer spending

Food inflation is squeezing household budgets and shifting volumes toward value packs, while premiumization endures among affluent consumers who still trade up in beverages and specialty teas. Price elasticity varies sharply—staples like salt show low elasticity versus discretionary beverages which are highly elastic—forcing Tata Consumer to rely on pack-price architecture to defend volumes and margins.

FX fluctuations and global exposure

Multiple-currency revenues and imported inputs expose Tata Consumer Products earnings to FX swings, with the Indian rupee averaging around 83 per USD in 2024–25, amplifying imported cost inflation and overseas debt service burdens.

Rupee depreciation has raised input costs for tea and coffee processing, while natural hedges from local sourcing and offsetting exports reduce but do not remove volatility.

Transparent pricing actions and active treasury policies, including forward covers and currency layering, have helped stabilize cash flows and protect margins.

Distribution and retail structure

India's distribution: kirana still supplies ~55% of FMCG (2024), modern trade ~12% and e-commerce ~6% of sales (2024); each channel shows distinct margin profiles with e-commerce and modern trade compressing trade margins. Route-to-market efficiency can swing working capital by 10–20 days. Retail consolidation (top 5 retailers ~30% organized share, 2024) pressures trade terms; direct-to-consumer initiatives can lift gross margin by ~300–500 bps and improve customer data.

- kirana ~55% (2024)

- modern trade ~12% (2024)

- e‑commerce ~6% (2024)

- working capital ±10–20 days

- top‑5 retailers ~30% organized share (2024)

- D2C +300–500 bps gross margin

Macroeconomic growth cycles

Macroeconomic cycles drive Tata Consumer Products: IMF projected India GDP growth at 6.8% in 2024, supporting rising incomes that expand packaged-food penetration and upgrade rates, while slowdowns delay discretionary trials and out-of-home consumption.

- Rising incomes: IMF 2024 India GDP 6.8%

- Slowdowns: defer discretionary & OOH spend

- Rural growth: sustains staples

- Urban momentum: boosts convenience

- Balanced exposure: smooths cycle impact

PLI INR 10,900 cr, tariffs/NTMs and WHO -30% salt reshape food margins

Economic factors: commodity-driven COGS volatility (tea/coffee) and weather shocks compress margins despite hedges; FY24 revenue INR 12,338 crore supports pricing power. Food inflation shifts volumes to value packs while premiumization sustains ASPs. FX (rupee ~83/USD 2024–25) raises imported input costs; distribution mix (kirana ~55%) shapes margins.

| Metric | Value |

|---|---|

| FY24 revenue | INR 12,338 crore |

| Rupee (avg 24–25) | ~83/USD |

| India GDP 2024 (IMF) | 6.8% |

| Kirana share | ~55% |

Preview the Actual Deliverable

Tata Consumer Products PESTLE Analysis

The Tata Consumer Products PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders, no surprises—this is the final, downloadable file.

Skip the Research. Get the Strategy.

Unlock strategic clarity with our concise PESTLE Analysis of Tata Consumer Products—highlighting political, economic, social, technological, legal, and environmental forces shaping its outlook. Use these insights to anticipate risks and spot growth opportunities across markets. Purchase the full report for the complete, ready-to-use analysis and actionable recommendations.

Political factors

Agri and food policy shifts

Government controls on tea, coffee, pulses and spices directly affect input costs and availability; the Centre's PLI for food processing (outlay INR 10,900 crore) can reduce capex pressure for processing and packaging investments.

Periodic changes in MSP, procurement norms or subsidies materially alter sourcing economics and margins, given Tata Consumer's reliance on contracted and spot procurement.

Sudden policy reversals or export/import curbs heighten planning risk across categories, impacting inventory, pricing and supplier contracts.

Trade tariffs and import-export rules

Customs duties on raw tea, coffee, packaging and additives directly squeeze gross margins for Tata Consumer Products, which reported consolidated revenue of INR 13,214 crore in FY24, making even small tariff shifts material. Export incentives or barriers, including RoDTEP credits and destination tariffs, alter global routing and pricing strategies. Non-tariff measures such as random quality inspections can delay shipments by days, raising logistic costs. Diversifying sourcing across India, Kenya and Vietnam reduces country-specific tariff shocks.

Geopolitical and logistics stability

Geopolitical and logistics instability—disruptions in Straits like Malacca (which carries roughly one-third of global trade) and port blockages can raise delivery times and costs for Tata Consumer. Political unrest in origin countries such as Kenya or Sri Lanka can curb harvests and exports, tightening supplies. Currency controls and sanctions (eg post-2022 regimes) complicate payments and hedging. Expanding multi-origin sourcing across India, Kenya and Sri Lanka lowers concentration risk.

Public health and nutrition agendas

Government drives on salt reduction, sugar limits and mandatory fortification are forcing reformulation: WHO targets a 30% relative reduction in population salt intake by 2025 and recommends free sugars <10% of energy, while school and workplace nutrition programs shift procurement toward lower-sodium/sugar SKUs; front-of-pack labelling adoption is reshaping purchase decisions and proactive compliance can convert regulation into brand trust and sales resilience.

- Policy: WHO 30% salt reduction by 2025

- Sugar: WHO <10% energy from free sugars

- Programs: schools/workplaces drive healthier SKUs

- Labeling: FOP rules alter choice; compliance = brand trust

Local governance and incentives

- State approvals: single-window/permits

- Land & water: allocation limits affect capacity

- Municipal standards: CPCB/FSSAI compliance costs

- Infrastructure: Rs 11.1 lakh crore capex expands distribution

- Govt relations: de-risks expansions

PLI INR 10,900 cr, tariffs/NTMs and WHO -30% salt reshape food margins

Government controls (PLI INR 10,900 crore) and MSP/procurement shifts materially affect input costs and capex economics for Tata Consumer (consol revenue INR 13,214 crore FY24). Tariff and non‑tariff measures alter margins and logistics; multi‑origin sourcing (India, Kenya, Vietnam, Sri Lanka) reduces concentration risk. Nutrition policies (WHO salt/sugar targets) force reformulation and labeling compliance, affecting SKUs and procurement.

| Factor | Impact | Key data |

|---|---|---|

| PLI | Capex support | INR 10,900 cr |

| Tariffs/NTMs | Margin risk | Revenue INR 13,214 cr (FY24) |

| Nutrition regs | Reformulation cost | WHO salt target -30% by 2025 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Tata Consumer Products across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with each section backed by current data and trends. Designed to help executives and investors identify actionable risks and opportunities for strategic planning.

Clean, summarized PESTLE of Tata Consumer Products, visually segmented for quick interpretation and easily dropped into presentations or shared across teams to streamline external risk and market-position discussions.

Economic factors

Commodity price volatility

Tea, coffee and spice prices are cyclical and weather-sensitive, directly inflating TCPL’s COGS during supply shocks; India tea auctions and arabica/robusta swings drove input cost volatility in 2024. Long-term contracts and hedging programs mitigate but do not eliminate spikes, leaving residual exposure in quarterly margins. Passing costs through depends on brand strength and timing; Tata Consumer’s FY24 consolidated revenue of INR 12,338 crore provided pricing power and scale, while a diversified portfolio across beverages and spices buffers single-commodity shocks.

Inflation and consumer spending

Food inflation is squeezing household budgets and shifting volumes toward value packs, while premiumization endures among affluent consumers who still trade up in beverages and specialty teas. Price elasticity varies sharply—staples like salt show low elasticity versus discretionary beverages which are highly elastic—forcing Tata Consumer to rely on pack-price architecture to defend volumes and margins.

FX fluctuations and global exposure

Multiple-currency revenues and imported inputs expose Tata Consumer Products earnings to FX swings, with the Indian rupee averaging around 83 per USD in 2024–25, amplifying imported cost inflation and overseas debt service burdens.

Rupee depreciation has raised input costs for tea and coffee processing, while natural hedges from local sourcing and offsetting exports reduce but do not remove volatility.

Transparent pricing actions and active treasury policies, including forward covers and currency layering, have helped stabilize cash flows and protect margins.

Distribution and retail structure

India's distribution: kirana still supplies ~55% of FMCG (2024), modern trade ~12% and e-commerce ~6% of sales (2024); each channel shows distinct margin profiles with e-commerce and modern trade compressing trade margins. Route-to-market efficiency can swing working capital by 10–20 days. Retail consolidation (top 5 retailers ~30% organized share, 2024) pressures trade terms; direct-to-consumer initiatives can lift gross margin by ~300–500 bps and improve customer data.

- kirana ~55% (2024)

- modern trade ~12% (2024)

- e‑commerce ~6% (2024)

- working capital ±10–20 days

- top‑5 retailers ~30% organized share (2024)

- D2C +300–500 bps gross margin

Macroeconomic growth cycles

Macroeconomic cycles drive Tata Consumer Products: IMF projected India GDP growth at 6.8% in 2024, supporting rising incomes that expand packaged-food penetration and upgrade rates, while slowdowns delay discretionary trials and out-of-home consumption.

- Rising incomes: IMF 2024 India GDP 6.8%

- Slowdowns: defer discretionary & OOH spend

- Rural growth: sustains staples

- Urban momentum: boosts convenience

- Balanced exposure: smooths cycle impact

PLI INR 10,900 cr, tariffs/NTMs and WHO -30% salt reshape food margins

Economic factors: commodity-driven COGS volatility (tea/coffee) and weather shocks compress margins despite hedges; FY24 revenue INR 12,338 crore supports pricing power. Food inflation shifts volumes to value packs while premiumization sustains ASPs. FX (rupee ~83/USD 2024–25) raises imported input costs; distribution mix (kirana ~55%) shapes margins.

| Metric | Value |

|---|---|

| FY24 revenue | INR 12,338 crore |

| Rupee (avg 24–25) | ~83/USD |

| India GDP 2024 (IMF) | 6.8% |

| Kirana share | ~55% |

Preview the Actual Deliverable

Tata Consumer Products PESTLE Analysis

The Tata Consumer Products PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders, no surprises—this is the final, downloadable file.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our concise PESTLE Analysis of Tata Consumer Products—highlighting political, economic, social, technological, legal, and environmental forces shaping its outlook. Use these insights to anticipate risks and spot growth opportunities across markets. Purchase the full report for the complete, ready-to-use analysis and actionable recommendations.

Political factors

Agri and food policy shifts

Government controls on tea, coffee, pulses and spices directly affect input costs and availability; the Centre's PLI for food processing (outlay INR 10,900 crore) can reduce capex pressure for processing and packaging investments.

Periodic changes in MSP, procurement norms or subsidies materially alter sourcing economics and margins, given Tata Consumer's reliance on contracted and spot procurement.

Sudden policy reversals or export/import curbs heighten planning risk across categories, impacting inventory, pricing and supplier contracts.

Trade tariffs and import-export rules

Customs duties on raw tea, coffee, packaging and additives directly squeeze gross margins for Tata Consumer Products, which reported consolidated revenue of INR 13,214 crore in FY24, making even small tariff shifts material. Export incentives or barriers, including RoDTEP credits and destination tariffs, alter global routing and pricing strategies. Non-tariff measures such as random quality inspections can delay shipments by days, raising logistic costs. Diversifying sourcing across India, Kenya and Vietnam reduces country-specific tariff shocks.

Geopolitical and logistics stability

Geopolitical and logistics instability—disruptions in Straits like Malacca (which carries roughly one-third of global trade) and port blockages can raise delivery times and costs for Tata Consumer. Political unrest in origin countries such as Kenya or Sri Lanka can curb harvests and exports, tightening supplies. Currency controls and sanctions (eg post-2022 regimes) complicate payments and hedging. Expanding multi-origin sourcing across India, Kenya and Sri Lanka lowers concentration risk.

Public health and nutrition agendas

Government drives on salt reduction, sugar limits and mandatory fortification are forcing reformulation: WHO targets a 30% relative reduction in population salt intake by 2025 and recommends free sugars <10% of energy, while school and workplace nutrition programs shift procurement toward lower-sodium/sugar SKUs; front-of-pack labelling adoption is reshaping purchase decisions and proactive compliance can convert regulation into brand trust and sales resilience.

- Policy: WHO 30% salt reduction by 2025

- Sugar: WHO <10% energy from free sugars

- Programs: schools/workplaces drive healthier SKUs

- Labeling: FOP rules alter choice; compliance = brand trust

Local governance and incentives

- State approvals: single-window/permits

- Land & water: allocation limits affect capacity

- Municipal standards: CPCB/FSSAI compliance costs

- Infrastructure: Rs 11.1 lakh crore capex expands distribution

- Govt relations: de-risks expansions

PLI INR 10,900 cr, tariffs/NTMs and WHO -30% salt reshape food margins

Government controls (PLI INR 10,900 crore) and MSP/procurement shifts materially affect input costs and capex economics for Tata Consumer (consol revenue INR 13,214 crore FY24). Tariff and non‑tariff measures alter margins and logistics; multi‑origin sourcing (India, Kenya, Vietnam, Sri Lanka) reduces concentration risk. Nutrition policies (WHO salt/sugar targets) force reformulation and labeling compliance, affecting SKUs and procurement.

| Factor | Impact | Key data |

|---|---|---|

| PLI | Capex support | INR 10,900 cr |

| Tariffs/NTMs | Margin risk | Revenue INR 13,214 cr (FY24) |

| Nutrition regs | Reformulation cost | WHO salt target -30% by 2025 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Tata Consumer Products across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with each section backed by current data and trends. Designed to help executives and investors identify actionable risks and opportunities for strategic planning.

Clean, summarized PESTLE of Tata Consumer Products, visually segmented for quick interpretation and easily dropped into presentations or shared across teams to streamline external risk and market-position discussions.

Economic factors

Commodity price volatility

Tea, coffee and spice prices are cyclical and weather-sensitive, directly inflating TCPL’s COGS during supply shocks; India tea auctions and arabica/robusta swings drove input cost volatility in 2024. Long-term contracts and hedging programs mitigate but do not eliminate spikes, leaving residual exposure in quarterly margins. Passing costs through depends on brand strength and timing; Tata Consumer’s FY24 consolidated revenue of INR 12,338 crore provided pricing power and scale, while a diversified portfolio across beverages and spices buffers single-commodity shocks.

Inflation and consumer spending

Food inflation is squeezing household budgets and shifting volumes toward value packs, while premiumization endures among affluent consumers who still trade up in beverages and specialty teas. Price elasticity varies sharply—staples like salt show low elasticity versus discretionary beverages which are highly elastic—forcing Tata Consumer to rely on pack-price architecture to defend volumes and margins.

FX fluctuations and global exposure

Multiple-currency revenues and imported inputs expose Tata Consumer Products earnings to FX swings, with the Indian rupee averaging around 83 per USD in 2024–25, amplifying imported cost inflation and overseas debt service burdens.

Rupee depreciation has raised input costs for tea and coffee processing, while natural hedges from local sourcing and offsetting exports reduce but do not remove volatility.

Transparent pricing actions and active treasury policies, including forward covers and currency layering, have helped stabilize cash flows and protect margins.

Distribution and retail structure

India's distribution: kirana still supplies ~55% of FMCG (2024), modern trade ~12% and e-commerce ~6% of sales (2024); each channel shows distinct margin profiles with e-commerce and modern trade compressing trade margins. Route-to-market efficiency can swing working capital by 10–20 days. Retail consolidation (top 5 retailers ~30% organized share, 2024) pressures trade terms; direct-to-consumer initiatives can lift gross margin by ~300–500 bps and improve customer data.

- kirana ~55% (2024)

- modern trade ~12% (2024)

- e‑commerce ~6% (2024)

- working capital ±10–20 days

- top‑5 retailers ~30% organized share (2024)

- D2C +300–500 bps gross margin

Macroeconomic growth cycles

Macroeconomic cycles drive Tata Consumer Products: IMF projected India GDP growth at 6.8% in 2024, supporting rising incomes that expand packaged-food penetration and upgrade rates, while slowdowns delay discretionary trials and out-of-home consumption.

- Rising incomes: IMF 2024 India GDP 6.8%

- Slowdowns: defer discretionary & OOH spend

- Rural growth: sustains staples

- Urban momentum: boosts convenience

- Balanced exposure: smooths cycle impact

PLI INR 10,900 cr, tariffs/NTMs and WHO -30% salt reshape food margins

Economic factors: commodity-driven COGS volatility (tea/coffee) and weather shocks compress margins despite hedges; FY24 revenue INR 12,338 crore supports pricing power. Food inflation shifts volumes to value packs while premiumization sustains ASPs. FX (rupee ~83/USD 2024–25) raises imported input costs; distribution mix (kirana ~55%) shapes margins.

| Metric | Value |

|---|---|

| FY24 revenue | INR 12,338 crore |

| Rupee (avg 24–25) | ~83/USD |

| India GDP 2024 (IMF) | 6.8% |

| Kirana share | ~55% |

Preview the Actual Deliverable

Tata Consumer Products PESTLE Analysis

The Tata Consumer Products PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders, no surprises—this is the final, downloadable file.