Tata Motors Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

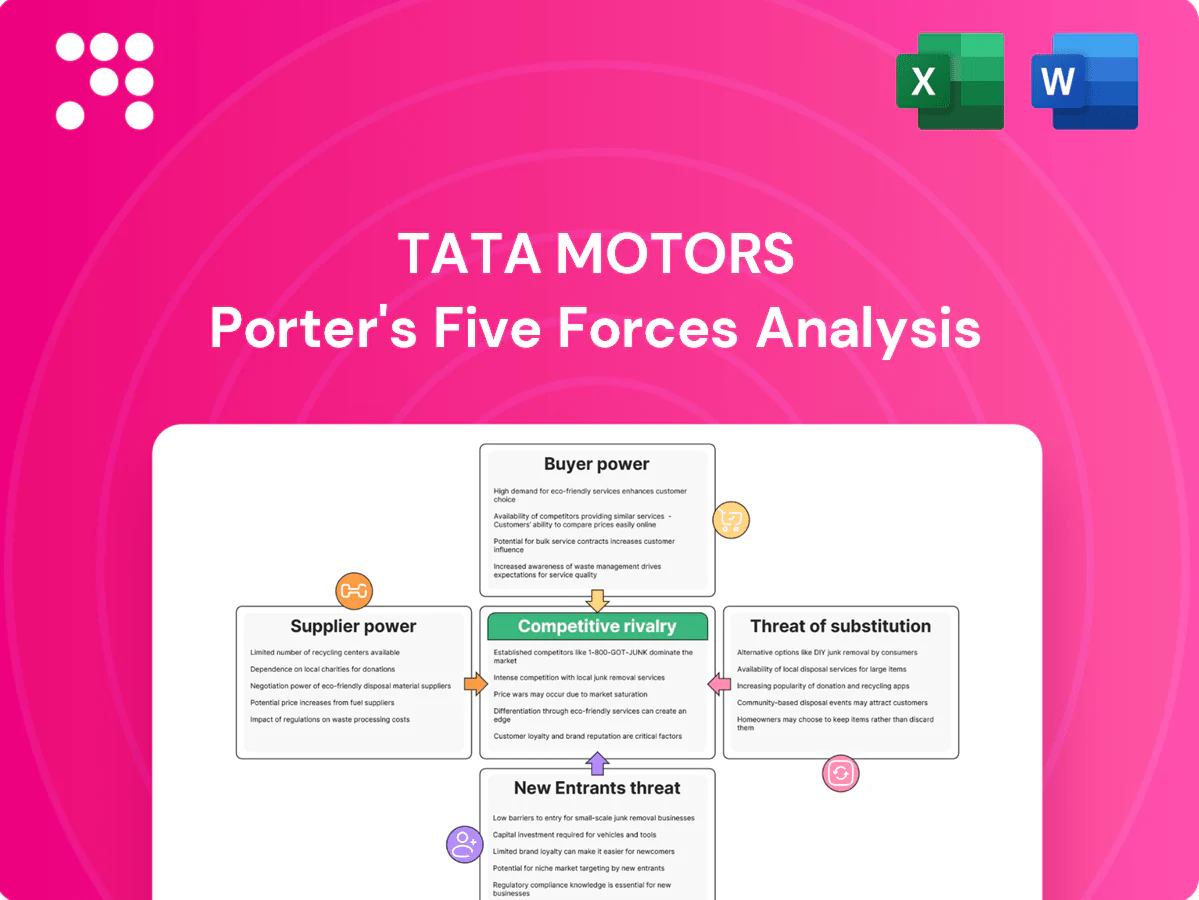

Tata Motors faces intense rivalry from global OEMs and domestic players, rising supplier leverage for EV components, moderate buyer power, growing threat of regulated substitutes and high capital barriers for new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tata Motors’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated critical components

Semiconductors, batteries and advanced electronics for Tata Motors come from a concentrated global supplier base; global semiconductor sales were about $600–620 billion in 2023–24 and top 5 EV cell makers supplied roughly 80% of cells in 2024, so shortages can derail production and lift input costs. Dual-sourcing and strategic inventories partially mitigate disruption, and long-term offtake agreements reduce but do not eliminate systemic risk.

Commodity price volatility

Steel, aluminium and rubber price swings materially pressure margins in PV and CV segments, but Tata Motors reported a 2024 raw-material cost inflationary impact partially offset by a 6% YoY improvement in sourcing efficiency. Pass-through to selling prices is constrained by intense competition and affordability limits, keeping margin recovery muted. Strategic hedging, Tata Group buying synergies and a targeted localization push — reducing commodity/FX transmission — have cushioned volatility.

Tier-1 module dependence

Tier-1 dependence on complex modules (powertrains, ADAS, infotainment) raises switching costs as deep integration and software calibration extend beyond mechanical parts; 2024 design-in cycles give Tier-1s leverage during model development. Co-development spreads technical and financial risk but locks specifications and IP, narrowing procurement options. Supplier performance directly affects quality and launch timelines, making supplier reliability a critical bargaining factor.

EV battery ecosystem gaps

Limited local cell manufacturing leaves India importing over 80% of lithium-ion cells in 2024, raising logistics and tariff-driven costs; battery pack suppliers therefore hold pricing power as EV volumes climb and global pack costs fell to roughly $120–130/kWh in 2024. Tata Motors’ announced cell-sourcing and backward-integration plans within the Tata Group aim to reduce supplier leverage. Recycling and switching toward LFP chemistry, which saw ~25% global share in 2024, can diversify inputs and lower dependence.

- Import reliance: over 80% of cells (2024)

- Pack cost: ~$120–130/kWh (2024)

- LFP share: ~25% (2024)

- Mitigants: Tata Group cell sourcing, backward integration, recycling

Mitigating group and scale

Tata Motors leverages Tata Group procurement and intra-group linkage with Tata Steel to strengthen bargaining power, while its dominant scale in India enhances purchase leverage and inventory management. Vendor development and localization programs expand the supplier base and reduce import dependence. Supplier financing and capability-building initiatives deepen supplier relationships and resilience. Jaguar Land Rover (JLR) sourcing practices feed global quality and sourcing learnings back into Tata Motors.

- Group procurement: intra-group sourcing with Tata Steel

- Scale: market-leading volumes in India improve leverage

- Localization: vendor development broadens supplier base

- Supplier support: financing and capability building

- JLR learnings: global sourcing and quality practices

Moderate–high supplier power: 80% imported cells; pack cost $120–130/kWh

Supplier power is moderate-to-high for Tata Motors due to concentrated semiconductor and cell suppliers, with >80% cells imported in 2024 and pack costs ~$120–130/kWh. Commodity swings (steel, aluminium) and complex Tier-1 modules raise switching costs and margin risk. Tata Group procurement, localization and planned cell integration materially mitigate but do not eliminate supplier leverage.

| Metric | 2024 |

|---|---|

| Imported cells | ~80% |

| Pack cost | $120–130/kWh |

| LFP share | ~25% |

What is included in the product

Tailored Porter’s Five Forces analysis of Tata Motors uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and disruptive trends—evaluating how these forces shape pricing, margins, market entry barriers, and strategic positioning for investors and strategists.

One-sheet Porter's Five Forces for Tata Motors—clear, customizable force levels and instant spider chart visuals to streamline strategic decisions and slide-ready summaries; swap in your data or duplicate tabs for scenario analysis without macros.

Customers Bargaining Power

Price-sensitive mass market

India sold about 3.6 million passenger vehicles in 2024, and buyers remain highly price- and value-conscious; even 1–2% price moves can sway choices across segments. Discounts, feature bundles and financing (≈72% of PV purchases financed in 2024) are primary levers dealers and OEMs use. High elasticity of demand constrains Tata Motors' ability to expand margins without volume trade-offs.

Fleet and institutional buyers

Fleet and institutional buyers negotiate steep volume-based discounts, significant for Tata Motors given its roughly 45% share of India’s commercial vehicle market in 2024. Large tenders compress margins and enforce robust service SLAs, with procurement often awarded on lowest total cost of ownership rather than headline price. Total cost of ownership—fuel, maintenance, residual value—trumps upfront price for fleet decision-making. Downtime penalties embedded in contracts raise aftermarket and service expectations and influence pricing.

EV early adopters vs pragmatists

EV early adopters prioritize tech and OTA features while pragmatists weight range, charging and resale—Tata Nexon EV's ARAI range ~312 km and DC charge 0–80% in ~56 minutes set a benchmark. FAME-II incentives and competitive low-interest EV loans materially lift conversion. With 30+ passenger EV models in India by 2024, comparison shopping intensifies and extended warranties/OTA updates become key bargaining levers.

After-sales and uptime demands

After-sales service coverage, parts availability and uptime drive loyalty for Tata Motors customers, with rising lifecycle costs prompting brand switches; extended warranties and AMC plans are now key retention tools. Digital service platforms and predictive maintenance raise expectations—McKinsey 2024 finds predictive maintenance can cut downtime by up to 30%.

- Service coverage: network reach and turnaround times

- Parts availability: spares fill rate impacts downtime

- Uptime & digital maintenance: predictive maintenance reduces downtime ≈30% (McKinsey 2024)

Information transparency

Information transparency: online reviews and comparison tools sharply increase buyer knowledge, forcing Tata Motors to match feature sets across price bands and reducing brand loyalty; real-time price discovery undermines dealer-level pricing power while configurators and e-commerce compress negotiation spreads, accelerating margin pressure on traditional retail channels.

- Online reviews boost buyer information

- Real-time pricing weakens dealers

- Feature parity expected per price point

- Configurators compress negotiation spreads

India cars (3.6M), 72% financed squeeze OEM margins

Indian buyers (3.6m PVs sold in 2024) are highly price‑sensitive; 72% financed purchases and 1–2% price moves shift demand, limiting Tata Motors' margin power. Fleet buyers (Tata ~45% CV share 2024) extract volume discounts and TCO-based contracts, pressuring margins. EV buyers compare tech, range (Nexon EV ~312 km) and charging (0–80% ~56 min); 30+ EV models heighten bargaining.

| Metric | 2024 |

|---|---|

| PV sales (India) | 3.6M |

| PV finance rate | ≈72% |

| Tata CV share | ≈45% |

| Nexon EV range | ~312 km |

Preview Before You Purchase

Tata Motors Porter's Five Forces Analysis

This preview shows the exact Tata Motors Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The document is the full, professionally formatted analysis ready for download and use upon payment. You’re viewing the deliverable in its final form.

Go Beyond the Preview—Access the Full Strategic Report

Tata Motors faces intense rivalry from global OEMs and domestic players, rising supplier leverage for EV components, moderate buyer power, growing threat of regulated substitutes and high capital barriers for new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tata Motors’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated critical components

Semiconductors, batteries and advanced electronics for Tata Motors come from a concentrated global supplier base; global semiconductor sales were about $600–620 billion in 2023–24 and top 5 EV cell makers supplied roughly 80% of cells in 2024, so shortages can derail production and lift input costs. Dual-sourcing and strategic inventories partially mitigate disruption, and long-term offtake agreements reduce but do not eliminate systemic risk.

Commodity price volatility

Steel, aluminium and rubber price swings materially pressure margins in PV and CV segments, but Tata Motors reported a 2024 raw-material cost inflationary impact partially offset by a 6% YoY improvement in sourcing efficiency. Pass-through to selling prices is constrained by intense competition and affordability limits, keeping margin recovery muted. Strategic hedging, Tata Group buying synergies and a targeted localization push — reducing commodity/FX transmission — have cushioned volatility.

Tier-1 module dependence

Tier-1 dependence on complex modules (powertrains, ADAS, infotainment) raises switching costs as deep integration and software calibration extend beyond mechanical parts; 2024 design-in cycles give Tier-1s leverage during model development. Co-development spreads technical and financial risk but locks specifications and IP, narrowing procurement options. Supplier performance directly affects quality and launch timelines, making supplier reliability a critical bargaining factor.

EV battery ecosystem gaps

Limited local cell manufacturing leaves India importing over 80% of lithium-ion cells in 2024, raising logistics and tariff-driven costs; battery pack suppliers therefore hold pricing power as EV volumes climb and global pack costs fell to roughly $120–130/kWh in 2024. Tata Motors’ announced cell-sourcing and backward-integration plans within the Tata Group aim to reduce supplier leverage. Recycling and switching toward LFP chemistry, which saw ~25% global share in 2024, can diversify inputs and lower dependence.

- Import reliance: over 80% of cells (2024)

- Pack cost: ~$120–130/kWh (2024)

- LFP share: ~25% (2024)

- Mitigants: Tata Group cell sourcing, backward integration, recycling

Mitigating group and scale

Tata Motors leverages Tata Group procurement and intra-group linkage with Tata Steel to strengthen bargaining power, while its dominant scale in India enhances purchase leverage and inventory management. Vendor development and localization programs expand the supplier base and reduce import dependence. Supplier financing and capability-building initiatives deepen supplier relationships and resilience. Jaguar Land Rover (JLR) sourcing practices feed global quality and sourcing learnings back into Tata Motors.

- Group procurement: intra-group sourcing with Tata Steel

- Scale: market-leading volumes in India improve leverage

- Localization: vendor development broadens supplier base

- Supplier support: financing and capability building

- JLR learnings: global sourcing and quality practices

Moderate–high supplier power: 80% imported cells; pack cost $120–130/kWh

Supplier power is moderate-to-high for Tata Motors due to concentrated semiconductor and cell suppliers, with >80% cells imported in 2024 and pack costs ~$120–130/kWh. Commodity swings (steel, aluminium) and complex Tier-1 modules raise switching costs and margin risk. Tata Group procurement, localization and planned cell integration materially mitigate but do not eliminate supplier leverage.

| Metric | 2024 |

|---|---|

| Imported cells | ~80% |

| Pack cost | $120–130/kWh |

| LFP share | ~25% |

What is included in the product

Tailored Porter’s Five Forces analysis of Tata Motors uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and disruptive trends—evaluating how these forces shape pricing, margins, market entry barriers, and strategic positioning for investors and strategists.

One-sheet Porter's Five Forces for Tata Motors—clear, customizable force levels and instant spider chart visuals to streamline strategic decisions and slide-ready summaries; swap in your data or duplicate tabs for scenario analysis without macros.

Customers Bargaining Power

Price-sensitive mass market

India sold about 3.6 million passenger vehicles in 2024, and buyers remain highly price- and value-conscious; even 1–2% price moves can sway choices across segments. Discounts, feature bundles and financing (≈72% of PV purchases financed in 2024) are primary levers dealers and OEMs use. High elasticity of demand constrains Tata Motors' ability to expand margins without volume trade-offs.

Fleet and institutional buyers

Fleet and institutional buyers negotiate steep volume-based discounts, significant for Tata Motors given its roughly 45% share of India’s commercial vehicle market in 2024. Large tenders compress margins and enforce robust service SLAs, with procurement often awarded on lowest total cost of ownership rather than headline price. Total cost of ownership—fuel, maintenance, residual value—trumps upfront price for fleet decision-making. Downtime penalties embedded in contracts raise aftermarket and service expectations and influence pricing.

EV early adopters vs pragmatists

EV early adopters prioritize tech and OTA features while pragmatists weight range, charging and resale—Tata Nexon EV's ARAI range ~312 km and DC charge 0–80% in ~56 minutes set a benchmark. FAME-II incentives and competitive low-interest EV loans materially lift conversion. With 30+ passenger EV models in India by 2024, comparison shopping intensifies and extended warranties/OTA updates become key bargaining levers.

After-sales and uptime demands

After-sales service coverage, parts availability and uptime drive loyalty for Tata Motors customers, with rising lifecycle costs prompting brand switches; extended warranties and AMC plans are now key retention tools. Digital service platforms and predictive maintenance raise expectations—McKinsey 2024 finds predictive maintenance can cut downtime by up to 30%.

- Service coverage: network reach and turnaround times

- Parts availability: spares fill rate impacts downtime

- Uptime & digital maintenance: predictive maintenance reduces downtime ≈30% (McKinsey 2024)

Information transparency

Information transparency: online reviews and comparison tools sharply increase buyer knowledge, forcing Tata Motors to match feature sets across price bands and reducing brand loyalty; real-time price discovery undermines dealer-level pricing power while configurators and e-commerce compress negotiation spreads, accelerating margin pressure on traditional retail channels.

- Online reviews boost buyer information

- Real-time pricing weakens dealers

- Feature parity expected per price point

- Configurators compress negotiation spreads

India cars (3.6M), 72% financed squeeze OEM margins

Indian buyers (3.6m PVs sold in 2024) are highly price‑sensitive; 72% financed purchases and 1–2% price moves shift demand, limiting Tata Motors' margin power. Fleet buyers (Tata ~45% CV share 2024) extract volume discounts and TCO-based contracts, pressuring margins. EV buyers compare tech, range (Nexon EV ~312 km) and charging (0–80% ~56 min); 30+ EV models heighten bargaining.

| Metric | 2024 |

|---|---|

| PV sales (India) | 3.6M |

| PV finance rate | ≈72% |

| Tata CV share | ≈45% |

| Nexon EV range | ~312 km |

Preview Before You Purchase

Tata Motors Porter's Five Forces Analysis

This preview shows the exact Tata Motors Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The document is the full, professionally formatted analysis ready for download and use upon payment. You’re viewing the deliverable in its final form.

Description

Go Beyond the Preview—Access the Full Strategic Report

Tata Motors faces intense rivalry from global OEMs and domestic players, rising supplier leverage for EV components, moderate buyer power, growing threat of regulated substitutes and high capital barriers for new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tata Motors’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated critical components

Semiconductors, batteries and advanced electronics for Tata Motors come from a concentrated global supplier base; global semiconductor sales were about $600–620 billion in 2023–24 and top 5 EV cell makers supplied roughly 80% of cells in 2024, so shortages can derail production and lift input costs. Dual-sourcing and strategic inventories partially mitigate disruption, and long-term offtake agreements reduce but do not eliminate systemic risk.

Commodity price volatility

Steel, aluminium and rubber price swings materially pressure margins in PV and CV segments, but Tata Motors reported a 2024 raw-material cost inflationary impact partially offset by a 6% YoY improvement in sourcing efficiency. Pass-through to selling prices is constrained by intense competition and affordability limits, keeping margin recovery muted. Strategic hedging, Tata Group buying synergies and a targeted localization push — reducing commodity/FX transmission — have cushioned volatility.

Tier-1 module dependence

Tier-1 dependence on complex modules (powertrains, ADAS, infotainment) raises switching costs as deep integration and software calibration extend beyond mechanical parts; 2024 design-in cycles give Tier-1s leverage during model development. Co-development spreads technical and financial risk but locks specifications and IP, narrowing procurement options. Supplier performance directly affects quality and launch timelines, making supplier reliability a critical bargaining factor.

EV battery ecosystem gaps

Limited local cell manufacturing leaves India importing over 80% of lithium-ion cells in 2024, raising logistics and tariff-driven costs; battery pack suppliers therefore hold pricing power as EV volumes climb and global pack costs fell to roughly $120–130/kWh in 2024. Tata Motors’ announced cell-sourcing and backward-integration plans within the Tata Group aim to reduce supplier leverage. Recycling and switching toward LFP chemistry, which saw ~25% global share in 2024, can diversify inputs and lower dependence.

- Import reliance: over 80% of cells (2024)

- Pack cost: ~$120–130/kWh (2024)

- LFP share: ~25% (2024)

- Mitigants: Tata Group cell sourcing, backward integration, recycling

Mitigating group and scale

Tata Motors leverages Tata Group procurement and intra-group linkage with Tata Steel to strengthen bargaining power, while its dominant scale in India enhances purchase leverage and inventory management. Vendor development and localization programs expand the supplier base and reduce import dependence. Supplier financing and capability-building initiatives deepen supplier relationships and resilience. Jaguar Land Rover (JLR) sourcing practices feed global quality and sourcing learnings back into Tata Motors.

- Group procurement: intra-group sourcing with Tata Steel

- Scale: market-leading volumes in India improve leverage

- Localization: vendor development broadens supplier base

- Supplier support: financing and capability building

- JLR learnings: global sourcing and quality practices

Moderate–high supplier power: 80% imported cells; pack cost $120–130/kWh

Supplier power is moderate-to-high for Tata Motors due to concentrated semiconductor and cell suppliers, with >80% cells imported in 2024 and pack costs ~$120–130/kWh. Commodity swings (steel, aluminium) and complex Tier-1 modules raise switching costs and margin risk. Tata Group procurement, localization and planned cell integration materially mitigate but do not eliminate supplier leverage.

| Metric | 2024 |

|---|---|

| Imported cells | ~80% |

| Pack cost | $120–130/kWh |

| LFP share | ~25% |

What is included in the product

Tailored Porter’s Five Forces analysis of Tata Motors uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and disruptive trends—evaluating how these forces shape pricing, margins, market entry barriers, and strategic positioning for investors and strategists.

One-sheet Porter's Five Forces for Tata Motors—clear, customizable force levels and instant spider chart visuals to streamline strategic decisions and slide-ready summaries; swap in your data or duplicate tabs for scenario analysis without macros.

Customers Bargaining Power

Price-sensitive mass market

India sold about 3.6 million passenger vehicles in 2024, and buyers remain highly price- and value-conscious; even 1–2% price moves can sway choices across segments. Discounts, feature bundles and financing (≈72% of PV purchases financed in 2024) are primary levers dealers and OEMs use. High elasticity of demand constrains Tata Motors' ability to expand margins without volume trade-offs.

Fleet and institutional buyers

Fleet and institutional buyers negotiate steep volume-based discounts, significant for Tata Motors given its roughly 45% share of India’s commercial vehicle market in 2024. Large tenders compress margins and enforce robust service SLAs, with procurement often awarded on lowest total cost of ownership rather than headline price. Total cost of ownership—fuel, maintenance, residual value—trumps upfront price for fleet decision-making. Downtime penalties embedded in contracts raise aftermarket and service expectations and influence pricing.

EV early adopters vs pragmatists

EV early adopters prioritize tech and OTA features while pragmatists weight range, charging and resale—Tata Nexon EV's ARAI range ~312 km and DC charge 0–80% in ~56 minutes set a benchmark. FAME-II incentives and competitive low-interest EV loans materially lift conversion. With 30+ passenger EV models in India by 2024, comparison shopping intensifies and extended warranties/OTA updates become key bargaining levers.

After-sales and uptime demands

After-sales service coverage, parts availability and uptime drive loyalty for Tata Motors customers, with rising lifecycle costs prompting brand switches; extended warranties and AMC plans are now key retention tools. Digital service platforms and predictive maintenance raise expectations—McKinsey 2024 finds predictive maintenance can cut downtime by up to 30%.

- Service coverage: network reach and turnaround times

- Parts availability: spares fill rate impacts downtime

- Uptime & digital maintenance: predictive maintenance reduces downtime ≈30% (McKinsey 2024)

Information transparency

Information transparency: online reviews and comparison tools sharply increase buyer knowledge, forcing Tata Motors to match feature sets across price bands and reducing brand loyalty; real-time price discovery undermines dealer-level pricing power while configurators and e-commerce compress negotiation spreads, accelerating margin pressure on traditional retail channels.

- Online reviews boost buyer information

- Real-time pricing weakens dealers

- Feature parity expected per price point

- Configurators compress negotiation spreads

India cars (3.6M), 72% financed squeeze OEM margins

Indian buyers (3.6m PVs sold in 2024) are highly price‑sensitive; 72% financed purchases and 1–2% price moves shift demand, limiting Tata Motors' margin power. Fleet buyers (Tata ~45% CV share 2024) extract volume discounts and TCO-based contracts, pressuring margins. EV buyers compare tech, range (Nexon EV ~312 km) and charging (0–80% ~56 min); 30+ EV models heighten bargaining.

| Metric | 2024 |

|---|---|

| PV sales (India) | 3.6M |

| PV finance rate | ≈72% |

| Tata CV share | ≈45% |

| Nexon EV range | ~312 km |

Preview Before You Purchase

Tata Motors Porter's Five Forces Analysis

This preview shows the exact Tata Motors Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The document is the full, professionally formatted analysis ready for download and use upon payment. You’re viewing the deliverable in its final form.