Tata Power Company Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Tata Power faces moderate supplier power, evolving buyer expectations, regulated barriers limiting new entrants, rising substitute threats from renewables, and intense industry rivalry shaping margins; this snapshot highlights key competitive tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights tailored to Tata Power Company.

Suppliers Bargaining Power

Diverse fuel sources but concentrated critical suppliers

Coal, gas and renewable component suppliers are pivotal; the seaborne LNG market is concentrated with the top three exporters supplying roughly 60% of global shipments in 2024, tightening negotiating leverage for thermal buyers. Price volatility and currency swings have amplified supplier power for imported coal and LNG, pressuring margins on thermal portfolios. Renewables face limited Tier-1 inverter and turbine OEMs, constraining procurement terms; Tata Power mitigates via diversified mix and hedging but remains exposed on critical inputs.

Long-term contracts and vertical integration temper leverage

Long-term fuel linkages, PPAs and OEM framework agreements substantially reduce Tata Power’s spot exposure, shifting bargaining leverage away from suppliers; its solar cell and module manufacturing provides backward integration that lowers reliance on external module vendors. Standardization and multi-vendor procurement further dilute supplier power, though capacity ramp-up and scale constraints in manufacturing can limit full insulation from supplier leverage.

EPC and balance-of-plant capacity cycles affect pricing

When EPC and balance-of-plant capacity tightens, vendors can raise prices or allocate capacity to larger, higher-margin orders, squeezing developers’ margins; industry downcycles reverse this, shifting bargaining power to buyers.

Tata Power’s renewable ambition — a stated target of 30 GW by 2030 and a project pipeline of over 10 GW as of 2024 — helps secure EPC/BOS slots at competitive terms.

Nevertheless, peak renewables cycles still lift BOS and logistics costs, often producing double-digit price spikes that temper procurement leverage.

Grid access and land as quasi-suppliers

Transmission connectivity, evacuation capacity and land banks act as quasi-suppliers for Tata Power, with limited alternatives and potential bottlenecks that can raise supplier power; Tata Power reported ~14.9 GW consolidated capacity by FY2024, increasing reliance on evacuation infrastructure. State utilities and CTU timelines can delay projects, implicitly increasing costs, while early-stage approvals and land-acquisition expertise mitigate delays but cannot eliminate occasional cost overruns.

- Transmission: constrained timelines by CTU/Discoms

- Evacuation: limited alternatives, risk of cost overruns

- Land banks: strategic advantage, reduce lead time

- Mitigation: early approvals, land expertise

Financial capital and skilled labor as strategic inputs

Rising rates and tighter lending norms in 2024 pushed financiers to tighten terms, increasing supplier (financier) bargaining power; lenders commonly insist on DSCR covenants (>1.2) and stricter limits on merchant exposure. Specialized O&M and digital talent remain scarce, creating upward wage pressure and higher contract costs. Tata Power’s FY2024 consolidated balance sheet and Tata parentage partially mitigate these pressures.

Coal/LNG concentration raises supplier leverage; large generator 14.9 GW

Coal/LNG market concentration (top 3 ≈60% of seaborne LNG in 2024) and commodity volatility elevate supplier leverage; Tata Power’s 14.9 GW consolidated (FY2024) and 30 GW by 2030 target partially mitigate through scale. Long-term PPAs, OEM frameworks and in-house module manufacturing reduce spot exposure, but EPC/BOS tightness and DSCR>1.2 lender covenants increase supplier/financier bargaining power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| LNG/coal exporters | Top3 ≈60% | Higher price/availability risk |

| Transmission/Evacuation | 14.9 GW consolidated | Bottleneck risk, delays |

| Finance | DSCR>1.2 | Stricter terms |

What is included in the product

Tailored Porter's Five Forces analysis for Tata Power Company uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive forces and regulatory dynamics that shape its pricing power and strategic positioning.

Concise one-sheet Porter's Five Forces for Tata Power—customizable pressure levels with an instant spider chart, copy-ready for pitch decks or boardroom slides, no macros, swap in your own data and integrate seamlessly with Excel dashboards or the accompanying Word report.

Customers Bargaining Power

State DISCOMs as dominant buyers

State DISCOMs buy over 70% of generation through long-term PPAs, giving them strong pricing and payment leverage over Tata Power. Competitive reverse auctions have driven renewables tariffs down to about INR 2.00/kWh in recent bids, squeezing margins. DISCOM outstanding dues were roughly INR 1.4 trillion in 2024, creating working-capital stress for generators. Financially stronger DISCOM counterparties lower default risk but cap pricing upside.

Commercial and industrial customers pursue low-cost green power

Commercial and industrial buyers increasingly use open access and group captive arrangements to secure cheaper renewables, exerting strong price pressure on suppliers; Tata Power reported roughly 11 GW of installed capacity with about 5 GW renewables by 2024, intensifying C&I competition for green power. Their high price sensitivity and clear alternatives heighten negotiating leverage, though bundled offerings and firm reliability SLAs can justify modest premium pricing. Regulatory facilitation keeps switching costs moderate, aiding C&I mobility.

Retail consumers in licensed areas have limited switching

In Tata Power’s licensed distribution areas customers have limited switching due to regulated supply and average residential tariffs near INR 7–9/kWh in 2024, reducing short-term bargaining leverage. Where competition exists, service quality and outage performance drive churn and retention. Digital billing, loyalty programs and rooftop solar bundles (India rooftop capacity ~10 GW by 2024) strengthen stickiness while regulators cap pricing flexibility.

Demand for sustainability and traceability shapes contracts

Buyers increasingly demand RE attributes, RECs and 24x7 green blends; corporates push for firmed renewables—battery or hydro-backed supply—raising willingness to pay for dispatchable green power as decarbonization timelines shorten.

- Buyers seek RECs and 24x7 green blends

- Firming with storage/hydro raises value capture

- Corporate 2030–2040 targets tighten expectations

- Transparent tracking differentiates amid price pressure

Power traders and exchanges offer alternative sourcing

High DISCOM PPA share (~70%) and INR 1.4tn dues raise buyer leverage; IEX leads spot market

Large DISCOM share (~70% generation via PPAs) and INR 1.4tn outstanding dues (2024) give buyers strong payment and price leverage; competitive renewables bids ~INR 2.00/kWh and C&I open-access (growing demand for firm 24x7 green power) push prices down while raising premium for firmed supply; IEX dominates short-term flexibility (~90–95%), keeping bilateral terms under pressure.

| Metric | Value (2024) |

|---|---|

| DISCOM PPA share | ~70% |

| DISCOM dues | INR 1.4tn |

| Renewables auction price | ~INR 2.00/kWh |

| IEX share | 90–95% |

| Tata Power capacity | ~11 GW (5 GW renew) |

What You See Is What You Get

Tata Power Company Porter's Five Forces Analysis

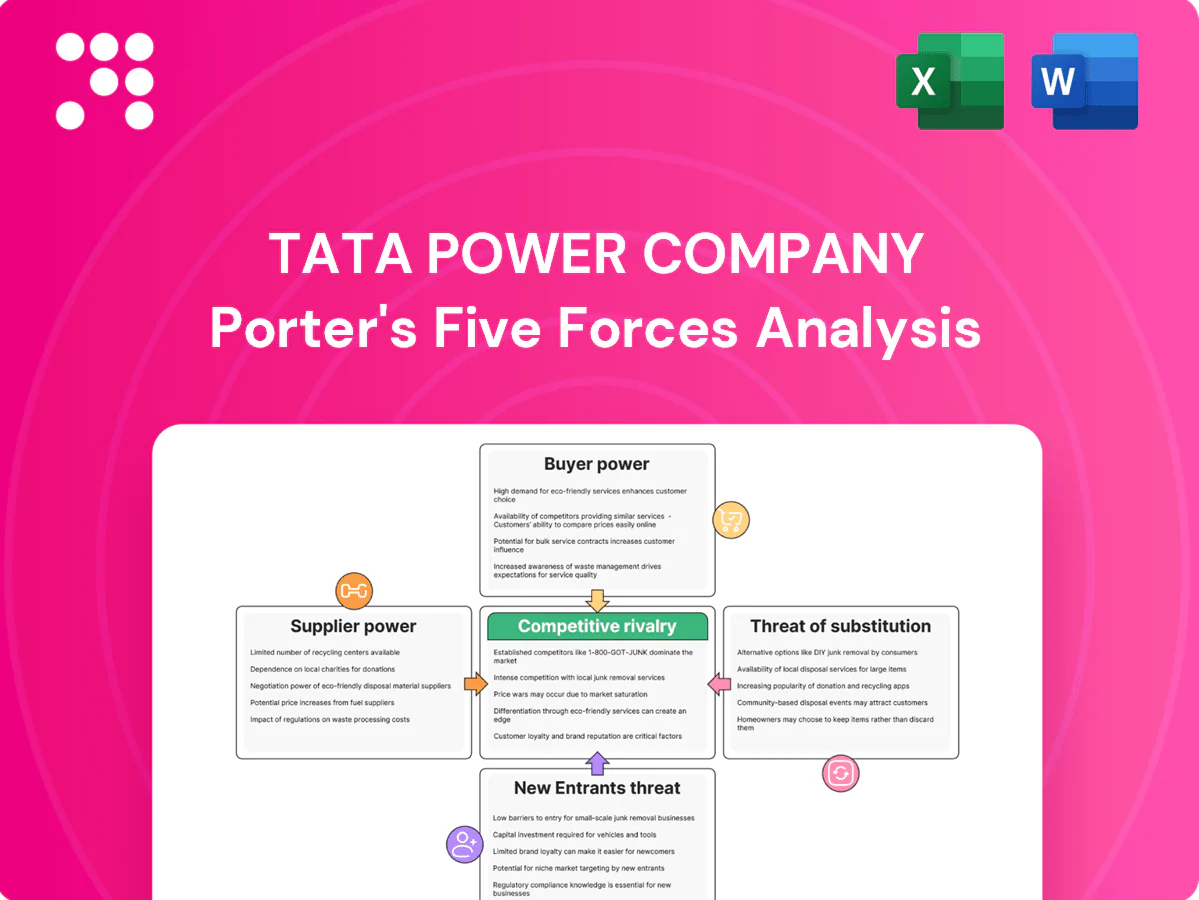

This preview shows the exact Tata Power Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The file is the complete, professionally formatted assessment, covering supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry. Once you buy, you’ll get instant access to this identical document, ready for download and use.

A Must-Have Tool for Decision-Makers

Tata Power faces moderate supplier power, evolving buyer expectations, regulated barriers limiting new entrants, rising substitute threats from renewables, and intense industry rivalry shaping margins; this snapshot highlights key competitive tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights tailored to Tata Power Company.

Suppliers Bargaining Power

Diverse fuel sources but concentrated critical suppliers

Coal, gas and renewable component suppliers are pivotal; the seaborne LNG market is concentrated with the top three exporters supplying roughly 60% of global shipments in 2024, tightening negotiating leverage for thermal buyers. Price volatility and currency swings have amplified supplier power for imported coal and LNG, pressuring margins on thermal portfolios. Renewables face limited Tier-1 inverter and turbine OEMs, constraining procurement terms; Tata Power mitigates via diversified mix and hedging but remains exposed on critical inputs.

Long-term contracts and vertical integration temper leverage

Long-term fuel linkages, PPAs and OEM framework agreements substantially reduce Tata Power’s spot exposure, shifting bargaining leverage away from suppliers; its solar cell and module manufacturing provides backward integration that lowers reliance on external module vendors. Standardization and multi-vendor procurement further dilute supplier power, though capacity ramp-up and scale constraints in manufacturing can limit full insulation from supplier leverage.

EPC and balance-of-plant capacity cycles affect pricing

When EPC and balance-of-plant capacity tightens, vendors can raise prices or allocate capacity to larger, higher-margin orders, squeezing developers’ margins; industry downcycles reverse this, shifting bargaining power to buyers.

Tata Power’s renewable ambition — a stated target of 30 GW by 2030 and a project pipeline of over 10 GW as of 2024 — helps secure EPC/BOS slots at competitive terms.

Nevertheless, peak renewables cycles still lift BOS and logistics costs, often producing double-digit price spikes that temper procurement leverage.

Grid access and land as quasi-suppliers

Transmission connectivity, evacuation capacity and land banks act as quasi-suppliers for Tata Power, with limited alternatives and potential bottlenecks that can raise supplier power; Tata Power reported ~14.9 GW consolidated capacity by FY2024, increasing reliance on evacuation infrastructure. State utilities and CTU timelines can delay projects, implicitly increasing costs, while early-stage approvals and land-acquisition expertise mitigate delays but cannot eliminate occasional cost overruns.

- Transmission: constrained timelines by CTU/Discoms

- Evacuation: limited alternatives, risk of cost overruns

- Land banks: strategic advantage, reduce lead time

- Mitigation: early approvals, land expertise

Financial capital and skilled labor as strategic inputs

Rising rates and tighter lending norms in 2024 pushed financiers to tighten terms, increasing supplier (financier) bargaining power; lenders commonly insist on DSCR covenants (>1.2) and stricter limits on merchant exposure. Specialized O&M and digital talent remain scarce, creating upward wage pressure and higher contract costs. Tata Power’s FY2024 consolidated balance sheet and Tata parentage partially mitigate these pressures.

Coal/LNG concentration raises supplier leverage; large generator 14.9 GW

Coal/LNG market concentration (top 3 ≈60% of seaborne LNG in 2024) and commodity volatility elevate supplier leverage; Tata Power’s 14.9 GW consolidated (FY2024) and 30 GW by 2030 target partially mitigate through scale. Long-term PPAs, OEM frameworks and in-house module manufacturing reduce spot exposure, but EPC/BOS tightness and DSCR>1.2 lender covenants increase supplier/financier bargaining power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| LNG/coal exporters | Top3 ≈60% | Higher price/availability risk |

| Transmission/Evacuation | 14.9 GW consolidated | Bottleneck risk, delays |

| Finance | DSCR>1.2 | Stricter terms |

What is included in the product

Tailored Porter's Five Forces analysis for Tata Power Company uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive forces and regulatory dynamics that shape its pricing power and strategic positioning.

Concise one-sheet Porter's Five Forces for Tata Power—customizable pressure levels with an instant spider chart, copy-ready for pitch decks or boardroom slides, no macros, swap in your own data and integrate seamlessly with Excel dashboards or the accompanying Word report.

Customers Bargaining Power

State DISCOMs as dominant buyers

State DISCOMs buy over 70% of generation through long-term PPAs, giving them strong pricing and payment leverage over Tata Power. Competitive reverse auctions have driven renewables tariffs down to about INR 2.00/kWh in recent bids, squeezing margins. DISCOM outstanding dues were roughly INR 1.4 trillion in 2024, creating working-capital stress for generators. Financially stronger DISCOM counterparties lower default risk but cap pricing upside.

Commercial and industrial customers pursue low-cost green power

Commercial and industrial buyers increasingly use open access and group captive arrangements to secure cheaper renewables, exerting strong price pressure on suppliers; Tata Power reported roughly 11 GW of installed capacity with about 5 GW renewables by 2024, intensifying C&I competition for green power. Their high price sensitivity and clear alternatives heighten negotiating leverage, though bundled offerings and firm reliability SLAs can justify modest premium pricing. Regulatory facilitation keeps switching costs moderate, aiding C&I mobility.

Retail consumers in licensed areas have limited switching

In Tata Power’s licensed distribution areas customers have limited switching due to regulated supply and average residential tariffs near INR 7–9/kWh in 2024, reducing short-term bargaining leverage. Where competition exists, service quality and outage performance drive churn and retention. Digital billing, loyalty programs and rooftop solar bundles (India rooftop capacity ~10 GW by 2024) strengthen stickiness while regulators cap pricing flexibility.

Demand for sustainability and traceability shapes contracts

Buyers increasingly demand RE attributes, RECs and 24x7 green blends; corporates push for firmed renewables—battery or hydro-backed supply—raising willingness to pay for dispatchable green power as decarbonization timelines shorten.

- Buyers seek RECs and 24x7 green blends

- Firming with storage/hydro raises value capture

- Corporate 2030–2040 targets tighten expectations

- Transparent tracking differentiates amid price pressure

Power traders and exchanges offer alternative sourcing

High DISCOM PPA share (~70%) and INR 1.4tn dues raise buyer leverage; IEX leads spot market

Large DISCOM share (~70% generation via PPAs) and INR 1.4tn outstanding dues (2024) give buyers strong payment and price leverage; competitive renewables bids ~INR 2.00/kWh and C&I open-access (growing demand for firm 24x7 green power) push prices down while raising premium for firmed supply; IEX dominates short-term flexibility (~90–95%), keeping bilateral terms under pressure.

| Metric | Value (2024) |

|---|---|

| DISCOM PPA share | ~70% |

| DISCOM dues | INR 1.4tn |

| Renewables auction price | ~INR 2.00/kWh |

| IEX share | 90–95% |

| Tata Power capacity | ~11 GW (5 GW renew) |

What You See Is What You Get

Tata Power Company Porter's Five Forces Analysis

This preview shows the exact Tata Power Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The file is the complete, professionally formatted assessment, covering supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry. Once you buy, you’ll get instant access to this identical document, ready for download and use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Tata Power faces moderate supplier power, evolving buyer expectations, regulated barriers limiting new entrants, rising substitute threats from renewables, and intense industry rivalry shaping margins; this snapshot highlights key competitive tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights tailored to Tata Power Company.

Suppliers Bargaining Power

Diverse fuel sources but concentrated critical suppliers

Coal, gas and renewable component suppliers are pivotal; the seaborne LNG market is concentrated with the top three exporters supplying roughly 60% of global shipments in 2024, tightening negotiating leverage for thermal buyers. Price volatility and currency swings have amplified supplier power for imported coal and LNG, pressuring margins on thermal portfolios. Renewables face limited Tier-1 inverter and turbine OEMs, constraining procurement terms; Tata Power mitigates via diversified mix and hedging but remains exposed on critical inputs.

Long-term contracts and vertical integration temper leverage

Long-term fuel linkages, PPAs and OEM framework agreements substantially reduce Tata Power’s spot exposure, shifting bargaining leverage away from suppliers; its solar cell and module manufacturing provides backward integration that lowers reliance on external module vendors. Standardization and multi-vendor procurement further dilute supplier power, though capacity ramp-up and scale constraints in manufacturing can limit full insulation from supplier leverage.

EPC and balance-of-plant capacity cycles affect pricing

When EPC and balance-of-plant capacity tightens, vendors can raise prices or allocate capacity to larger, higher-margin orders, squeezing developers’ margins; industry downcycles reverse this, shifting bargaining power to buyers.

Tata Power’s renewable ambition — a stated target of 30 GW by 2030 and a project pipeline of over 10 GW as of 2024 — helps secure EPC/BOS slots at competitive terms.

Nevertheless, peak renewables cycles still lift BOS and logistics costs, often producing double-digit price spikes that temper procurement leverage.

Grid access and land as quasi-suppliers

Transmission connectivity, evacuation capacity and land banks act as quasi-suppliers for Tata Power, with limited alternatives and potential bottlenecks that can raise supplier power; Tata Power reported ~14.9 GW consolidated capacity by FY2024, increasing reliance on evacuation infrastructure. State utilities and CTU timelines can delay projects, implicitly increasing costs, while early-stage approvals and land-acquisition expertise mitigate delays but cannot eliminate occasional cost overruns.

- Transmission: constrained timelines by CTU/Discoms

- Evacuation: limited alternatives, risk of cost overruns

- Land banks: strategic advantage, reduce lead time

- Mitigation: early approvals, land expertise

Financial capital and skilled labor as strategic inputs

Rising rates and tighter lending norms in 2024 pushed financiers to tighten terms, increasing supplier (financier) bargaining power; lenders commonly insist on DSCR covenants (>1.2) and stricter limits on merchant exposure. Specialized O&M and digital talent remain scarce, creating upward wage pressure and higher contract costs. Tata Power’s FY2024 consolidated balance sheet and Tata parentage partially mitigate these pressures.

Coal/LNG concentration raises supplier leverage; large generator 14.9 GW

Coal/LNG market concentration (top 3 ≈60% of seaborne LNG in 2024) and commodity volatility elevate supplier leverage; Tata Power’s 14.9 GW consolidated (FY2024) and 30 GW by 2030 target partially mitigate through scale. Long-term PPAs, OEM frameworks and in-house module manufacturing reduce spot exposure, but EPC/BOS tightness and DSCR>1.2 lender covenants increase supplier/financier bargaining power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| LNG/coal exporters | Top3 ≈60% | Higher price/availability risk |

| Transmission/Evacuation | 14.9 GW consolidated | Bottleneck risk, delays |

| Finance | DSCR>1.2 | Stricter terms |

What is included in the product

Tailored Porter's Five Forces analysis for Tata Power Company uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive forces and regulatory dynamics that shape its pricing power and strategic positioning.

Concise one-sheet Porter's Five Forces for Tata Power—customizable pressure levels with an instant spider chart, copy-ready for pitch decks or boardroom slides, no macros, swap in your own data and integrate seamlessly with Excel dashboards or the accompanying Word report.

Customers Bargaining Power

State DISCOMs as dominant buyers

State DISCOMs buy over 70% of generation through long-term PPAs, giving them strong pricing and payment leverage over Tata Power. Competitive reverse auctions have driven renewables tariffs down to about INR 2.00/kWh in recent bids, squeezing margins. DISCOM outstanding dues were roughly INR 1.4 trillion in 2024, creating working-capital stress for generators. Financially stronger DISCOM counterparties lower default risk but cap pricing upside.

Commercial and industrial customers pursue low-cost green power

Commercial and industrial buyers increasingly use open access and group captive arrangements to secure cheaper renewables, exerting strong price pressure on suppliers; Tata Power reported roughly 11 GW of installed capacity with about 5 GW renewables by 2024, intensifying C&I competition for green power. Their high price sensitivity and clear alternatives heighten negotiating leverage, though bundled offerings and firm reliability SLAs can justify modest premium pricing. Regulatory facilitation keeps switching costs moderate, aiding C&I mobility.

Retail consumers in licensed areas have limited switching

In Tata Power’s licensed distribution areas customers have limited switching due to regulated supply and average residential tariffs near INR 7–9/kWh in 2024, reducing short-term bargaining leverage. Where competition exists, service quality and outage performance drive churn and retention. Digital billing, loyalty programs and rooftop solar bundles (India rooftop capacity ~10 GW by 2024) strengthen stickiness while regulators cap pricing flexibility.

Demand for sustainability and traceability shapes contracts

Buyers increasingly demand RE attributes, RECs and 24x7 green blends; corporates push for firmed renewables—battery or hydro-backed supply—raising willingness to pay for dispatchable green power as decarbonization timelines shorten.

- Buyers seek RECs and 24x7 green blends

- Firming with storage/hydro raises value capture

- Corporate 2030–2040 targets tighten expectations

- Transparent tracking differentiates amid price pressure

Power traders and exchanges offer alternative sourcing

High DISCOM PPA share (~70%) and INR 1.4tn dues raise buyer leverage; IEX leads spot market

Large DISCOM share (~70% generation via PPAs) and INR 1.4tn outstanding dues (2024) give buyers strong payment and price leverage; competitive renewables bids ~INR 2.00/kWh and C&I open-access (growing demand for firm 24x7 green power) push prices down while raising premium for firmed supply; IEX dominates short-term flexibility (~90–95%), keeping bilateral terms under pressure.

| Metric | Value (2024) |

|---|---|

| DISCOM PPA share | ~70% |

| DISCOM dues | INR 1.4tn |

| Renewables auction price | ~INR 2.00/kWh |

| IEX share | 90–95% |

| Tata Power capacity | ~11 GW (5 GW renew) |

What You See Is What You Get

Tata Power Company Porter's Five Forces Analysis

This preview shows the exact Tata Power Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The file is the complete, professionally formatted assessment, covering supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry. Once you buy, you’ll get instant access to this identical document, ready for download and use.