Tauber Oil Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Tauber Oil faces intense rivalry from majors and price-sensitive buyers, while supplier leverage and regulatory pressures constrain margins; threats from renewables and technological shifts also reshape competitive dynamics. Barriers to entry remain moderate given capital intensity, but niche players can still disrupt segments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tauber Oil’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated upstream sources

Producers, refiners and petrochemical plants remain relatively concentrated—OPEC+ and major refiners together accounted for about 45% of global liquids production in 2024—giving suppliers leverage over pricing, allocation and contract terms. Periodic OPEC+ policy moves and refinery turnarounds in 2024 tightened regional supply and spiked premiums for specific grades. Tauber must diversify counterparties and accept multiple grades to reduce supplier bargaining power.

Infrastructure gatekeepers

Pipeline operators, terminals and storage owners control critical capacity; US crude pipeline capacity was about 8.5 million b/d in 2024 and SPR capacity ≈713.5 million barrels, so allocation rules, nominations and take-or-pay contracts shift bargaining power to midstream. Congestion and maintenance windows push utilization over 90% on key routes, and 5–15 year throughput/storage deals secure access but cut optionality.

Quality and spec constraints

Strict 2024 product specs — diesel ≤15 ppm sulfur, gasoline RVP typically 7–15 psi and octane 87–95 AKI — limit substitutability and raise supplier leverage. Producers of compliant grades command premiums and tighter payment/delivery terms. Off-spec loads force marketers into costly reblending or downgrades, while robust QA/QC and assay optionality (batch testing, custody transfer assays) materially reduce exposure.

Geopolitical and weather exposure

Geopolitical sanctions and export bans in 2024, plus hurricanes and low river levels, repeatedly disrupted Tauber Oil supply basins; suppliers invoked force majeure or repriced cargoes, raising switching costs and the value of secured barrels, while hedging and multi-basin sourcing only partly offset shocks.

- Sanctions/re-routing pressure

- Weather-related shut-ins raise premiums

- Force majeure → higher switching costs

- Hedging/multi-basin mitigate but don’t eliminate risk

Credit and counterparty terms

Suppliers can insist on LC-backed payments, prepayments or tighter credit limits; in 2024, tighter markets and volatility (Brent ~86 USD/bbl average) shortened payment terms and widened premiums, raising working capital needs for marketers and increasing days payable pressure.

- LCs/prepayments increase WCR

- Shorter terms + wider premiums in 2024

- Strong balance sheet + trade finance lines = better terms

2024 supply squeeze: OPEC+ and refiners ≈45%, Brent ≈86 USD/bbl

Suppliers held strong leverage in 2024: OPEC+ and major refiners ≈45% of liquids supply, frequent policy shifts and refinery turnarounds spiked premiums and constrained allocation. Midstream owners (US pipeline capacity ≈8.5m b/d) and SPR ≈713.5m bbl tightened access, raising take-or-pay risk and working capital needs as Brent averaged ≈86 USD/bbl. Tauber must diversify grades, counterparties and secure trade finance.

| Metric | 2024 Value |

|---|---|

| OPEC+ + major refiners | ≈45% global liquids |

| US pipeline capacity | ≈8.5 million b/d |

| US SPR capacity | ≈713.5 million barrels |

| Brent average | ≈86 USD/bbl |

What is included in the product

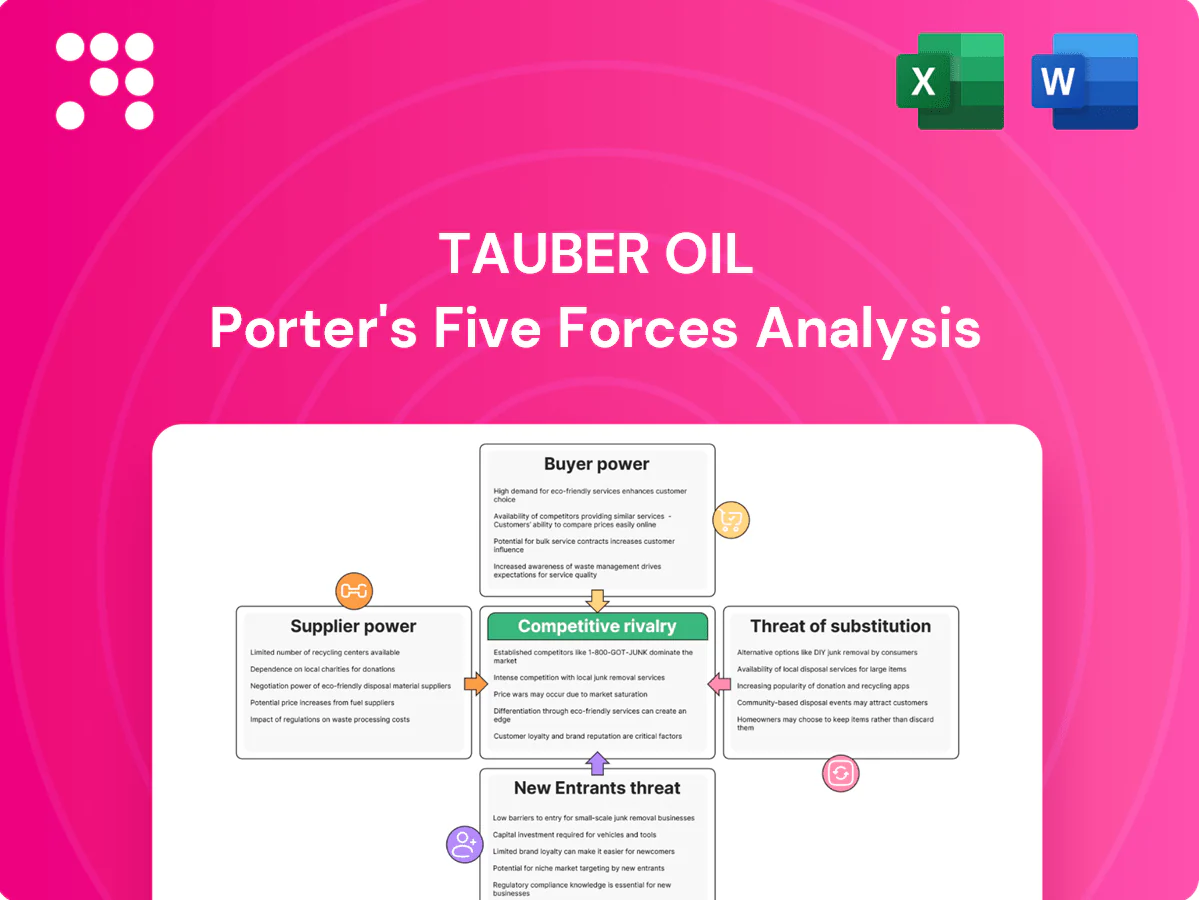

Provides a tailored Porter's Five Forces assessment of Tauber Oil, revealing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory pressures; highlights disruptive risks, pricing levers, and barriers that protect or expose Tauber’s market position.

A concise one-sheet Porter's Five Forces for Tauber Oil that visualizes competitive pressure with an editable spider chart, letting teams quickly customize inputs for new regulations or entrants and paste straight into decks.

Customers Bargaining Power

Large, sophisticated buyers

Refiners, airlines, retailers and industrials run competitive RFPs and benchmark purchases to transparent indices such as Platts, Argus and ICE, with 2024 global oil demand near 101.6 million b/d (IEA), intensifying scale-driven leverage. Large buyers routinely secure narrow differentials—often cents to under $1/barrel—forcing suppliers to compete on price, service and tailored logistics. Reliability and customized supply chains are decisive in winning contracts.

High price transparency

Platts and Argus benchmarks plus CME crude futures are published daily, with CME front‑month crude trading in the hundreds of thousands of contracts daily in 2024, making price signals highly transparent. Buyers use posted diffs and freight to arbitrage among marketers, squeezing distributor margins. Distributors must therefore create value through timing, basis management, and tailored logistics solutions to preserve margins.

Multi-sourcing and switching

Most buyers maintain multiple suppliers to preserve resilience and extract price tension, a trend reinforced by 2024 IEA data showing global oil demand grew roughly 1.3 mb/d, increasing procurement competition. Switching costs are moderate when product specs and delivery windows are met, enabling quick reallocation across suppliers. Contract optionality on volumes and liftings strengthens buyer bargaining, while deep relationships and performance KPIs (on-time delivery, quality) help suppliers defend share.

Service and logistics expectations

Buyers of Tauber Oil increasingly demand on-time delivery, tight demurrage control and inventory management; 2024 industry data show OECD commercial oil stocks near 2,800 million barrels, raising emphasis on just-in-time scheduling. Clients shift risk, quality liabilities and performance penalties onto marketers, but superior scheduling and storage access can offset price pressure and lower churn. Integrated logistics packages—blending shipping, storage and scheduling—reduce buyer leverage by bundling services and locking in capacity.

- On-time delivery: critical to avoid penalties and demurrage

- Demurrage control: often exceeds $10,000/day in market spikes

- Inventory mgmt: access to storage and scheduling cuts buyer bargaining power

Credit and payment leverage

Large buyers seek extended terms and credit accommodations, shifting working capital burden to the marketer; in 2024 many contracts moved toward 60–90 day payment windows, increasing exposure. Tight credit markets in 2024 amplified buyer bargaining power and pressured margins. Credit insurance and disciplined exposure limits remain primary defenses to protect cash flow and margins.

- Buyer term length: 60–90 days (2024)

- Risk mitigant: credit insurance

- Policy: strict exposure limits

Buyers drive narrow differentials as 2024 oil demand hits 101.6 mb/d

Large buyers use transparent benchmarks (Platts, Argus, CME) and scale to drive narrow differentials, forcing suppliers to compete on price, service and logistics. Multiple-sourcing and moderate switching costs give buyers leverage, while integrated logistics and storage access reduce that leverage. 2024 trends—101.6 mb/d demand, ~2,800 mb OECD stocks, 60–90 day terms—heighten price and credit pressure.

| Metric | 2024 |

|---|---|

| Global oil demand | 101.6 mb/d (IEA) |

| OECD commercial stocks | ~2,800 million barrels |

| Payment terms | 60–90 days |

| CME crude vol | hundreds of thousands contracts/day |

Preview Before You Purchase

Tauber Oil Porter's Five Forces Analysis

This preview shows the exact Tauber Oil Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professional, and complete. There are no placeholders or mockups; the file available for download after payment is this same document. It's ready for immediate use in decision-making, valuation, or strategic planning.

From Overview to Strategy Blueprint

Tauber Oil faces intense rivalry from majors and price-sensitive buyers, while supplier leverage and regulatory pressures constrain margins; threats from renewables and technological shifts also reshape competitive dynamics. Barriers to entry remain moderate given capital intensity, but niche players can still disrupt segments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tauber Oil’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated upstream sources

Producers, refiners and petrochemical plants remain relatively concentrated—OPEC+ and major refiners together accounted for about 45% of global liquids production in 2024—giving suppliers leverage over pricing, allocation and contract terms. Periodic OPEC+ policy moves and refinery turnarounds in 2024 tightened regional supply and spiked premiums for specific grades. Tauber must diversify counterparties and accept multiple grades to reduce supplier bargaining power.

Infrastructure gatekeepers

Pipeline operators, terminals and storage owners control critical capacity; US crude pipeline capacity was about 8.5 million b/d in 2024 and SPR capacity ≈713.5 million barrels, so allocation rules, nominations and take-or-pay contracts shift bargaining power to midstream. Congestion and maintenance windows push utilization over 90% on key routes, and 5–15 year throughput/storage deals secure access but cut optionality.

Quality and spec constraints

Strict 2024 product specs — diesel ≤15 ppm sulfur, gasoline RVP typically 7–15 psi and octane 87–95 AKI — limit substitutability and raise supplier leverage. Producers of compliant grades command premiums and tighter payment/delivery terms. Off-spec loads force marketers into costly reblending or downgrades, while robust QA/QC and assay optionality (batch testing, custody transfer assays) materially reduce exposure.

Geopolitical and weather exposure

Geopolitical sanctions and export bans in 2024, plus hurricanes and low river levels, repeatedly disrupted Tauber Oil supply basins; suppliers invoked force majeure or repriced cargoes, raising switching costs and the value of secured barrels, while hedging and multi-basin sourcing only partly offset shocks.

- Sanctions/re-routing pressure

- Weather-related shut-ins raise premiums

- Force majeure → higher switching costs

- Hedging/multi-basin mitigate but don’t eliminate risk

Credit and counterparty terms

Suppliers can insist on LC-backed payments, prepayments or tighter credit limits; in 2024, tighter markets and volatility (Brent ~86 USD/bbl average) shortened payment terms and widened premiums, raising working capital needs for marketers and increasing days payable pressure.

- LCs/prepayments increase WCR

- Shorter terms + wider premiums in 2024

- Strong balance sheet + trade finance lines = better terms

2024 supply squeeze: OPEC+ and refiners ≈45%, Brent ≈86 USD/bbl

Suppliers held strong leverage in 2024: OPEC+ and major refiners ≈45% of liquids supply, frequent policy shifts and refinery turnarounds spiked premiums and constrained allocation. Midstream owners (US pipeline capacity ≈8.5m b/d) and SPR ≈713.5m bbl tightened access, raising take-or-pay risk and working capital needs as Brent averaged ≈86 USD/bbl. Tauber must diversify grades, counterparties and secure trade finance.

| Metric | 2024 Value |

|---|---|

| OPEC+ + major refiners | ≈45% global liquids |

| US pipeline capacity | ≈8.5 million b/d |

| US SPR capacity | ≈713.5 million barrels |

| Brent average | ≈86 USD/bbl |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Tauber Oil, revealing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory pressures; highlights disruptive risks, pricing levers, and barriers that protect or expose Tauber’s market position.

A concise one-sheet Porter's Five Forces for Tauber Oil that visualizes competitive pressure with an editable spider chart, letting teams quickly customize inputs for new regulations or entrants and paste straight into decks.

Customers Bargaining Power

Large, sophisticated buyers

Refiners, airlines, retailers and industrials run competitive RFPs and benchmark purchases to transparent indices such as Platts, Argus and ICE, with 2024 global oil demand near 101.6 million b/d (IEA), intensifying scale-driven leverage. Large buyers routinely secure narrow differentials—often cents to under $1/barrel—forcing suppliers to compete on price, service and tailored logistics. Reliability and customized supply chains are decisive in winning contracts.

High price transparency

Platts and Argus benchmarks plus CME crude futures are published daily, with CME front‑month crude trading in the hundreds of thousands of contracts daily in 2024, making price signals highly transparent. Buyers use posted diffs and freight to arbitrage among marketers, squeezing distributor margins. Distributors must therefore create value through timing, basis management, and tailored logistics solutions to preserve margins.

Multi-sourcing and switching

Most buyers maintain multiple suppliers to preserve resilience and extract price tension, a trend reinforced by 2024 IEA data showing global oil demand grew roughly 1.3 mb/d, increasing procurement competition. Switching costs are moderate when product specs and delivery windows are met, enabling quick reallocation across suppliers. Contract optionality on volumes and liftings strengthens buyer bargaining, while deep relationships and performance KPIs (on-time delivery, quality) help suppliers defend share.

Service and logistics expectations

Buyers of Tauber Oil increasingly demand on-time delivery, tight demurrage control and inventory management; 2024 industry data show OECD commercial oil stocks near 2,800 million barrels, raising emphasis on just-in-time scheduling. Clients shift risk, quality liabilities and performance penalties onto marketers, but superior scheduling and storage access can offset price pressure and lower churn. Integrated logistics packages—blending shipping, storage and scheduling—reduce buyer leverage by bundling services and locking in capacity.

- On-time delivery: critical to avoid penalties and demurrage

- Demurrage control: often exceeds $10,000/day in market spikes

- Inventory mgmt: access to storage and scheduling cuts buyer bargaining power

Credit and payment leverage

Large buyers seek extended terms and credit accommodations, shifting working capital burden to the marketer; in 2024 many contracts moved toward 60–90 day payment windows, increasing exposure. Tight credit markets in 2024 amplified buyer bargaining power and pressured margins. Credit insurance and disciplined exposure limits remain primary defenses to protect cash flow and margins.

- Buyer term length: 60–90 days (2024)

- Risk mitigant: credit insurance

- Policy: strict exposure limits

Buyers drive narrow differentials as 2024 oil demand hits 101.6 mb/d

Large buyers use transparent benchmarks (Platts, Argus, CME) and scale to drive narrow differentials, forcing suppliers to compete on price, service and logistics. Multiple-sourcing and moderate switching costs give buyers leverage, while integrated logistics and storage access reduce that leverage. 2024 trends—101.6 mb/d demand, ~2,800 mb OECD stocks, 60–90 day terms—heighten price and credit pressure.

| Metric | 2024 |

|---|---|

| Global oil demand | 101.6 mb/d (IEA) |

| OECD commercial stocks | ~2,800 million barrels |

| Payment terms | 60–90 days |

| CME crude vol | hundreds of thousands contracts/day |

Preview Before You Purchase

Tauber Oil Porter's Five Forces Analysis

This preview shows the exact Tauber Oil Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professional, and complete. There are no placeholders or mockups; the file available for download after payment is this same document. It's ready for immediate use in decision-making, valuation, or strategic planning.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Tauber Oil faces intense rivalry from majors and price-sensitive buyers, while supplier leverage and regulatory pressures constrain margins; threats from renewables and technological shifts also reshape competitive dynamics. Barriers to entry remain moderate given capital intensity, but niche players can still disrupt segments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tauber Oil’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated upstream sources

Producers, refiners and petrochemical plants remain relatively concentrated—OPEC+ and major refiners together accounted for about 45% of global liquids production in 2024—giving suppliers leverage over pricing, allocation and contract terms. Periodic OPEC+ policy moves and refinery turnarounds in 2024 tightened regional supply and spiked premiums for specific grades. Tauber must diversify counterparties and accept multiple grades to reduce supplier bargaining power.

Infrastructure gatekeepers

Pipeline operators, terminals and storage owners control critical capacity; US crude pipeline capacity was about 8.5 million b/d in 2024 and SPR capacity ≈713.5 million barrels, so allocation rules, nominations and take-or-pay contracts shift bargaining power to midstream. Congestion and maintenance windows push utilization over 90% on key routes, and 5–15 year throughput/storage deals secure access but cut optionality.

Quality and spec constraints

Strict 2024 product specs — diesel ≤15 ppm sulfur, gasoline RVP typically 7–15 psi and octane 87–95 AKI — limit substitutability and raise supplier leverage. Producers of compliant grades command premiums and tighter payment/delivery terms. Off-spec loads force marketers into costly reblending or downgrades, while robust QA/QC and assay optionality (batch testing, custody transfer assays) materially reduce exposure.

Geopolitical and weather exposure

Geopolitical sanctions and export bans in 2024, plus hurricanes and low river levels, repeatedly disrupted Tauber Oil supply basins; suppliers invoked force majeure or repriced cargoes, raising switching costs and the value of secured barrels, while hedging and multi-basin sourcing only partly offset shocks.

- Sanctions/re-routing pressure

- Weather-related shut-ins raise premiums

- Force majeure → higher switching costs

- Hedging/multi-basin mitigate but don’t eliminate risk

Credit and counterparty terms

Suppliers can insist on LC-backed payments, prepayments or tighter credit limits; in 2024, tighter markets and volatility (Brent ~86 USD/bbl average) shortened payment terms and widened premiums, raising working capital needs for marketers and increasing days payable pressure.

- LCs/prepayments increase WCR

- Shorter terms + wider premiums in 2024

- Strong balance sheet + trade finance lines = better terms

2024 supply squeeze: OPEC+ and refiners ≈45%, Brent ≈86 USD/bbl

Suppliers held strong leverage in 2024: OPEC+ and major refiners ≈45% of liquids supply, frequent policy shifts and refinery turnarounds spiked premiums and constrained allocation. Midstream owners (US pipeline capacity ≈8.5m b/d) and SPR ≈713.5m bbl tightened access, raising take-or-pay risk and working capital needs as Brent averaged ≈86 USD/bbl. Tauber must diversify grades, counterparties and secure trade finance.

| Metric | 2024 Value |

|---|---|

| OPEC+ + major refiners | ≈45% global liquids |

| US pipeline capacity | ≈8.5 million b/d |

| US SPR capacity | ≈713.5 million barrels |

| Brent average | ≈86 USD/bbl |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Tauber Oil, revealing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory pressures; highlights disruptive risks, pricing levers, and barriers that protect or expose Tauber’s market position.

A concise one-sheet Porter's Five Forces for Tauber Oil that visualizes competitive pressure with an editable spider chart, letting teams quickly customize inputs for new regulations or entrants and paste straight into decks.

Customers Bargaining Power

Large, sophisticated buyers

Refiners, airlines, retailers and industrials run competitive RFPs and benchmark purchases to transparent indices such as Platts, Argus and ICE, with 2024 global oil demand near 101.6 million b/d (IEA), intensifying scale-driven leverage. Large buyers routinely secure narrow differentials—often cents to under $1/barrel—forcing suppliers to compete on price, service and tailored logistics. Reliability and customized supply chains are decisive in winning contracts.

High price transparency

Platts and Argus benchmarks plus CME crude futures are published daily, with CME front‑month crude trading in the hundreds of thousands of contracts daily in 2024, making price signals highly transparent. Buyers use posted diffs and freight to arbitrage among marketers, squeezing distributor margins. Distributors must therefore create value through timing, basis management, and tailored logistics solutions to preserve margins.

Multi-sourcing and switching

Most buyers maintain multiple suppliers to preserve resilience and extract price tension, a trend reinforced by 2024 IEA data showing global oil demand grew roughly 1.3 mb/d, increasing procurement competition. Switching costs are moderate when product specs and delivery windows are met, enabling quick reallocation across suppliers. Contract optionality on volumes and liftings strengthens buyer bargaining, while deep relationships and performance KPIs (on-time delivery, quality) help suppliers defend share.

Service and logistics expectations

Buyers of Tauber Oil increasingly demand on-time delivery, tight demurrage control and inventory management; 2024 industry data show OECD commercial oil stocks near 2,800 million barrels, raising emphasis on just-in-time scheduling. Clients shift risk, quality liabilities and performance penalties onto marketers, but superior scheduling and storage access can offset price pressure and lower churn. Integrated logistics packages—blending shipping, storage and scheduling—reduce buyer leverage by bundling services and locking in capacity.

- On-time delivery: critical to avoid penalties and demurrage

- Demurrage control: often exceeds $10,000/day in market spikes

- Inventory mgmt: access to storage and scheduling cuts buyer bargaining power

Credit and payment leverage

Large buyers seek extended terms and credit accommodations, shifting working capital burden to the marketer; in 2024 many contracts moved toward 60–90 day payment windows, increasing exposure. Tight credit markets in 2024 amplified buyer bargaining power and pressured margins. Credit insurance and disciplined exposure limits remain primary defenses to protect cash flow and margins.

- Buyer term length: 60–90 days (2024)

- Risk mitigant: credit insurance

- Policy: strict exposure limits

Buyers drive narrow differentials as 2024 oil demand hits 101.6 mb/d

Large buyers use transparent benchmarks (Platts, Argus, CME) and scale to drive narrow differentials, forcing suppliers to compete on price, service and logistics. Multiple-sourcing and moderate switching costs give buyers leverage, while integrated logistics and storage access reduce that leverage. 2024 trends—101.6 mb/d demand, ~2,800 mb OECD stocks, 60–90 day terms—heighten price and credit pressure.

| Metric | 2024 |

|---|---|

| Global oil demand | 101.6 mb/d (IEA) |

| OECD commercial stocks | ~2,800 million barrels |

| Payment terms | 60–90 days |

| CME crude vol | hundreds of thousands contracts/day |

Preview Before You Purchase

Tauber Oil Porter's Five Forces Analysis

This preview shows the exact Tauber Oil Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professional, and complete. There are no placeholders or mockups; the file available for download after payment is this same document. It's ready for immediate use in decision-making, valuation, or strategic planning.