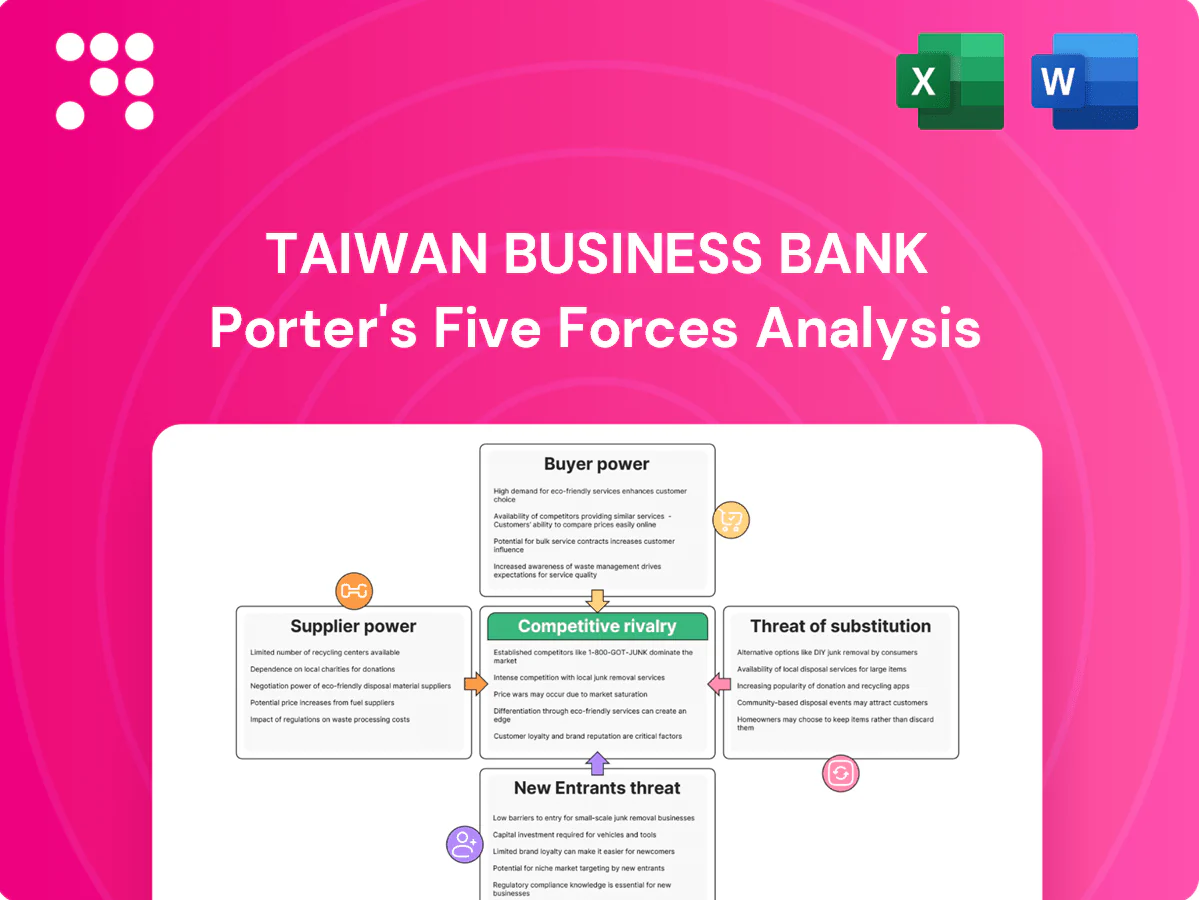

Taiwan Business Bank Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Taiwan Business Bank faces moderate bargaining power from corporate clients, high regulatory barriers, and growing fintech-driven substitute threats. Competitive rivalry is intense among domestic banks while supplier power remains limited, shaping margin pressures and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Taiwan Business Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Sticky retail deposits cushion power

As a traditional bank Taiwan Business Bank relies on core retail and SME deposits as primary funding suppliers; these tend to be sticky and price‑insensitive, moderating supplier power. Rate cycles can raise deposit betas and lift funding costs, and Taiwan’s competitive market in 2024 nudged promotional rates higher, slightly elevating supplier leverage. Diversified, granular deposits reduce concentration risk; Taiwan’s population of about 23.5 million in 2024 supports a broad deposit base.

Wholesale funding and interbank sources

When tapping interbank, CDs or bond markets, institutional suppliers gain leverage via pricing and covenants, pressuring margins and imposing tighter terms. 2024 market volatility widened spreads and shortened tenors, raising refinancing risk; Taiwan banks' loan-to-deposit ratio averaged about 81% in 2024, keeping reliance manageable. Maintaining strong credit ratings and Basel III liquidity buffers (LCR ≥100%) reduces this supplier power.

Technology and core banking vendors

Core systems, cloud, cybersecurity and payment-rail vendors exert switching-cost power: industry estimates in 2024 put global core banking software revenue near USD 15 billion, concentrating vendor leverage. Vendor lock-in and integration complexity raise dependence and migration costs for Taiwan Business Bank. Multi-vendor architectures, open APIs, scale contracts and regulatory due diligence (FSC guidance) can rebalance bargaining dynamics.

Human capital and specialized talent

Human capital for risk, compliance, SME credit underwriting and digital roles is scarce, raising supplier bargaining power; SMEs account for 97% of Taiwan enterprises and ~78% of employment (2024), amplifying underwriting demand. Wage inflation and retention packages lift operating costs, while training pipelines and analytics tools reduce dependence on star performers; employer brand and internal mobility further contain this power.

- Scarcity raises hiring leverage

- SMEs 97% of firms → higher SME underwriting needs

- Training + analytics lower single-person risk

- Employer brand & mobility reduce turnover pressure

Regulators as quasi-suppliers of licenses

Regulators act as quasi-suppliers by issuing banking licenses, NT$3 million deposit insurance coverage per depositor (CDIC), and gating access to national payment rails; their capital and compliance rules (Basel III implementation in Taiwan) materially shape Taiwan Business Bank’s product economics and margins. Strong supervisory ties and early engagement on rule changes reduce shock risk, while non-compliance or sudden regulatory tightening can sharply raise regulatory bargaining power.

- Licenses: regulator-controlled

- Deposit insurance: NT$3,000,000 per depositor (CDIC)

- Payment access: gatekept by central clearing/RTC systems

- Compliance/capital: Basel III standards drive costs

Sticky retail deposits, rising funding costs and vendor leverage reshape Taiwan banking sector

Retail deposits remain sticky and price‑insensitive (Taiwan population 23.5M in 2024; bank LDR ~81%), tempering supplier power. Institutional funding and 2024 market volatility raised spreads and tenor risk, nudging funding costs higher. Vendors (core software ~$15bn revenue globally in 2024), talent scarcity and regulator rules (CDIC NT$3,000,000) increase supplier leverage but can be mitigated.

| Supplier | Metric | 2024 value |

|---|---|---|

| Retail deposits | Population / LDR | 23.5M / 81% |

| Institutional funding | Market volatility | Wider spreads, shorter tenors |

| Vendors | Core banking market | USD 15bn |

| Regulator | Deposit insurance | NT$3,000,000 |

| Talent | SME share | 97% firms, 78% employment |

What is included in the product

Tailored Porter’s Five Forces analysis for Taiwan Business Bank that uncovers key drivers of competition, customer influence, and market entry risks. It evaluates supplier and buyer power, identifies substitutes and disruptive threats, and highlights dynamics that deter entrants to protect incumbency.

A concise one-sheet Porter's Five Forces for Taiwan Business Bank—perfect for quick decision-making and board decks. Swap in your own data or duplicate tabs for scenario testing (pre/post regulation, new entrants) with no complex code required.

Customers Bargaining Power

SME clientele price sensitivity

SMEs are highly cost-conscious on loan rates and fees, elevating buyer power. SMEs account for roughly 97% of Taiwanese firms and employ about 78% of the workforce, concentrating negotiating influence. Relationship banking, collateral structures and bundled services raise switching frictions, blunting pure price pressure. Government guarantee schemes and value-added advisory in 2024 help standardize terms and compress spreads.

Multi-banking and easy comparisons

Digital channels and aggregators let clients compare rates instantly; with Taiwan internet penetration over 90% in 2024, rate transparency has risen sharply. Larger SMEs typically maintain 2–4 banking relationships, increasing their leverage in fee and pricing negotiations. Transparent pricing shifts competition toward service quality and speed, while proactive RM coverage and tailored credit lines materially reduce churn.

Wealth and retail segments

Affluent clients shop wealth and FX pricing across banks and brokers, increasing price sensitivity and switching propensity. Robo-advisors and online brokers intensify fee pressure by offering lower-cost automated advisory and trading. Holistic financial planning and exclusive product access can reduce buyer power by creating higher switching costs. Loyalty programs and ecosystem partnerships strengthen retention and cross-sell opportunities.

Cross-border and FX users

Clients executing trade finance and remittances shop spreads and turnaround: 2024 benchmarks show fintech remitters at 0.2–0.5% vs traditional banks 0.5–1.0% and same‑day vs 1–3 day settlement.

Specialist FX platforms intensify price pressure, while end‑to‑end documentation and compliance assurance provide measurable non‑price differentiation and reduce operational risk.

Preferential tiers for corporates (eg, >US$1m turnover) delivering up to 20–50% fee discounts help Taiwan Business Bank rebalance customer bargaining power.

Credit quality dispersion

Credit quality dispersion drives bargaining power as higher-quality borrowers—large corporates and low-risk SMEs—can negotiate lower spreads and softer covenants, especially in benign credit cycles; conversely, when underwriting tightens and risk-based pricing is applied, margin erosion is contained and pricing discipline restored. Taiwan Business Bank’s diversified portfolio limits concentration risk and reduces any single buyer group’s leverage.

- Higher-quality borrowers: stronger negotiation

- Loose cycles: rises in low-risk segment power

- Tight underwriting: curbs margin erosion

- Diversification: limits exposure to one buyer group

SME-driven pricing and 92% internet penetration fuel fintech fee transparency and switching

SMEs (97% of firms; 78% of employment) drive strong buyer power on loan pricing; Taiwan internet penetration ~92% in 2024 raises rate transparency. Fintech remitters/spreads 0.2–0.5% vs banks 0.5–1.0%, same‑day vs 1–3 day settlement increases switching. Volume tiers (eg >US$1m) offer up to 50% fee discounts; portfolio diversification limits single‑group leverage.

| Metric | 2024 |

|---|---|

| SME share of firms | 97% |

| SME employment | 78% |

| Internet penetration | ~92% |

| Fintech spreads | 0.2–0.5% |

| Bank spreads | 0.5–1.0% |

| Volume discounts | up to 50% |

Full Version Awaits

Taiwan Business Bank Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Taiwan Business Bank you’ll receive—fully formatted and ready to use. The document is the final deliverable, not a sample or placeholder, and will be available instantly after purchase. No surprises, download and use immediately.

A Must-Have Tool for Decision-Makers

Taiwan Business Bank faces moderate bargaining power from corporate clients, high regulatory barriers, and growing fintech-driven substitute threats. Competitive rivalry is intense among domestic banks while supplier power remains limited, shaping margin pressures and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Taiwan Business Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Sticky retail deposits cushion power

As a traditional bank Taiwan Business Bank relies on core retail and SME deposits as primary funding suppliers; these tend to be sticky and price‑insensitive, moderating supplier power. Rate cycles can raise deposit betas and lift funding costs, and Taiwan’s competitive market in 2024 nudged promotional rates higher, slightly elevating supplier leverage. Diversified, granular deposits reduce concentration risk; Taiwan’s population of about 23.5 million in 2024 supports a broad deposit base.

Wholesale funding and interbank sources

When tapping interbank, CDs or bond markets, institutional suppliers gain leverage via pricing and covenants, pressuring margins and imposing tighter terms. 2024 market volatility widened spreads and shortened tenors, raising refinancing risk; Taiwan banks' loan-to-deposit ratio averaged about 81% in 2024, keeping reliance manageable. Maintaining strong credit ratings and Basel III liquidity buffers (LCR ≥100%) reduces this supplier power.

Technology and core banking vendors

Core systems, cloud, cybersecurity and payment-rail vendors exert switching-cost power: industry estimates in 2024 put global core banking software revenue near USD 15 billion, concentrating vendor leverage. Vendor lock-in and integration complexity raise dependence and migration costs for Taiwan Business Bank. Multi-vendor architectures, open APIs, scale contracts and regulatory due diligence (FSC guidance) can rebalance bargaining dynamics.

Human capital and specialized talent

Human capital for risk, compliance, SME credit underwriting and digital roles is scarce, raising supplier bargaining power; SMEs account for 97% of Taiwan enterprises and ~78% of employment (2024), amplifying underwriting demand. Wage inflation and retention packages lift operating costs, while training pipelines and analytics tools reduce dependence on star performers; employer brand and internal mobility further contain this power.

- Scarcity raises hiring leverage

- SMEs 97% of firms → higher SME underwriting needs

- Training + analytics lower single-person risk

- Employer brand & mobility reduce turnover pressure

Regulators as quasi-suppliers of licenses

Regulators act as quasi-suppliers by issuing banking licenses, NT$3 million deposit insurance coverage per depositor (CDIC), and gating access to national payment rails; their capital and compliance rules (Basel III implementation in Taiwan) materially shape Taiwan Business Bank’s product economics and margins. Strong supervisory ties and early engagement on rule changes reduce shock risk, while non-compliance or sudden regulatory tightening can sharply raise regulatory bargaining power.

- Licenses: regulator-controlled

- Deposit insurance: NT$3,000,000 per depositor (CDIC)

- Payment access: gatekept by central clearing/RTC systems

- Compliance/capital: Basel III standards drive costs

Sticky retail deposits, rising funding costs and vendor leverage reshape Taiwan banking sector

Retail deposits remain sticky and price‑insensitive (Taiwan population 23.5M in 2024; bank LDR ~81%), tempering supplier power. Institutional funding and 2024 market volatility raised spreads and tenor risk, nudging funding costs higher. Vendors (core software ~$15bn revenue globally in 2024), talent scarcity and regulator rules (CDIC NT$3,000,000) increase supplier leverage but can be mitigated.

| Supplier | Metric | 2024 value |

|---|---|---|

| Retail deposits | Population / LDR | 23.5M / 81% |

| Institutional funding | Market volatility | Wider spreads, shorter tenors |

| Vendors | Core banking market | USD 15bn |

| Regulator | Deposit insurance | NT$3,000,000 |

| Talent | SME share | 97% firms, 78% employment |

What is included in the product

Tailored Porter’s Five Forces analysis for Taiwan Business Bank that uncovers key drivers of competition, customer influence, and market entry risks. It evaluates supplier and buyer power, identifies substitutes and disruptive threats, and highlights dynamics that deter entrants to protect incumbency.

A concise one-sheet Porter's Five Forces for Taiwan Business Bank—perfect for quick decision-making and board decks. Swap in your own data or duplicate tabs for scenario testing (pre/post regulation, new entrants) with no complex code required.

Customers Bargaining Power

SME clientele price sensitivity

SMEs are highly cost-conscious on loan rates and fees, elevating buyer power. SMEs account for roughly 97% of Taiwanese firms and employ about 78% of the workforce, concentrating negotiating influence. Relationship banking, collateral structures and bundled services raise switching frictions, blunting pure price pressure. Government guarantee schemes and value-added advisory in 2024 help standardize terms and compress spreads.

Multi-banking and easy comparisons

Digital channels and aggregators let clients compare rates instantly; with Taiwan internet penetration over 90% in 2024, rate transparency has risen sharply. Larger SMEs typically maintain 2–4 banking relationships, increasing their leverage in fee and pricing negotiations. Transparent pricing shifts competition toward service quality and speed, while proactive RM coverage and tailored credit lines materially reduce churn.

Wealth and retail segments

Affluent clients shop wealth and FX pricing across banks and brokers, increasing price sensitivity and switching propensity. Robo-advisors and online brokers intensify fee pressure by offering lower-cost automated advisory and trading. Holistic financial planning and exclusive product access can reduce buyer power by creating higher switching costs. Loyalty programs and ecosystem partnerships strengthen retention and cross-sell opportunities.

Cross-border and FX users

Clients executing trade finance and remittances shop spreads and turnaround: 2024 benchmarks show fintech remitters at 0.2–0.5% vs traditional banks 0.5–1.0% and same‑day vs 1–3 day settlement.

Specialist FX platforms intensify price pressure, while end‑to‑end documentation and compliance assurance provide measurable non‑price differentiation and reduce operational risk.

Preferential tiers for corporates (eg, >US$1m turnover) delivering up to 20–50% fee discounts help Taiwan Business Bank rebalance customer bargaining power.

Credit quality dispersion

Credit quality dispersion drives bargaining power as higher-quality borrowers—large corporates and low-risk SMEs—can negotiate lower spreads and softer covenants, especially in benign credit cycles; conversely, when underwriting tightens and risk-based pricing is applied, margin erosion is contained and pricing discipline restored. Taiwan Business Bank’s diversified portfolio limits concentration risk and reduces any single buyer group’s leverage.

- Higher-quality borrowers: stronger negotiation

- Loose cycles: rises in low-risk segment power

- Tight underwriting: curbs margin erosion

- Diversification: limits exposure to one buyer group

SME-driven pricing and 92% internet penetration fuel fintech fee transparency and switching

SMEs (97% of firms; 78% of employment) drive strong buyer power on loan pricing; Taiwan internet penetration ~92% in 2024 raises rate transparency. Fintech remitters/spreads 0.2–0.5% vs banks 0.5–1.0%, same‑day vs 1–3 day settlement increases switching. Volume tiers (eg >US$1m) offer up to 50% fee discounts; portfolio diversification limits single‑group leverage.

| Metric | 2024 |

|---|---|

| SME share of firms | 97% |

| SME employment | 78% |

| Internet penetration | ~92% |

| Fintech spreads | 0.2–0.5% |

| Bank spreads | 0.5–1.0% |

| Volume discounts | up to 50% |

Full Version Awaits

Taiwan Business Bank Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Taiwan Business Bank you’ll receive—fully formatted and ready to use. The document is the final deliverable, not a sample or placeholder, and will be available instantly after purchase. No surprises, download and use immediately.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Taiwan Business Bank faces moderate bargaining power from corporate clients, high regulatory barriers, and growing fintech-driven substitute threats. Competitive rivalry is intense among domestic banks while supplier power remains limited, shaping margin pressures and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Taiwan Business Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Sticky retail deposits cushion power

As a traditional bank Taiwan Business Bank relies on core retail and SME deposits as primary funding suppliers; these tend to be sticky and price‑insensitive, moderating supplier power. Rate cycles can raise deposit betas and lift funding costs, and Taiwan’s competitive market in 2024 nudged promotional rates higher, slightly elevating supplier leverage. Diversified, granular deposits reduce concentration risk; Taiwan’s population of about 23.5 million in 2024 supports a broad deposit base.

Wholesale funding and interbank sources

When tapping interbank, CDs or bond markets, institutional suppliers gain leverage via pricing and covenants, pressuring margins and imposing tighter terms. 2024 market volatility widened spreads and shortened tenors, raising refinancing risk; Taiwan banks' loan-to-deposit ratio averaged about 81% in 2024, keeping reliance manageable. Maintaining strong credit ratings and Basel III liquidity buffers (LCR ≥100%) reduces this supplier power.

Technology and core banking vendors

Core systems, cloud, cybersecurity and payment-rail vendors exert switching-cost power: industry estimates in 2024 put global core banking software revenue near USD 15 billion, concentrating vendor leverage. Vendor lock-in and integration complexity raise dependence and migration costs for Taiwan Business Bank. Multi-vendor architectures, open APIs, scale contracts and regulatory due diligence (FSC guidance) can rebalance bargaining dynamics.

Human capital and specialized talent

Human capital for risk, compliance, SME credit underwriting and digital roles is scarce, raising supplier bargaining power; SMEs account for 97% of Taiwan enterprises and ~78% of employment (2024), amplifying underwriting demand. Wage inflation and retention packages lift operating costs, while training pipelines and analytics tools reduce dependence on star performers; employer brand and internal mobility further contain this power.

- Scarcity raises hiring leverage

- SMEs 97% of firms → higher SME underwriting needs

- Training + analytics lower single-person risk

- Employer brand & mobility reduce turnover pressure

Regulators as quasi-suppliers of licenses

Regulators act as quasi-suppliers by issuing banking licenses, NT$3 million deposit insurance coverage per depositor (CDIC), and gating access to national payment rails; their capital and compliance rules (Basel III implementation in Taiwan) materially shape Taiwan Business Bank’s product economics and margins. Strong supervisory ties and early engagement on rule changes reduce shock risk, while non-compliance or sudden regulatory tightening can sharply raise regulatory bargaining power.

- Licenses: regulator-controlled

- Deposit insurance: NT$3,000,000 per depositor (CDIC)

- Payment access: gatekept by central clearing/RTC systems

- Compliance/capital: Basel III standards drive costs

Sticky retail deposits, rising funding costs and vendor leverage reshape Taiwan banking sector

Retail deposits remain sticky and price‑insensitive (Taiwan population 23.5M in 2024; bank LDR ~81%), tempering supplier power. Institutional funding and 2024 market volatility raised spreads and tenor risk, nudging funding costs higher. Vendors (core software ~$15bn revenue globally in 2024), talent scarcity and regulator rules (CDIC NT$3,000,000) increase supplier leverage but can be mitigated.

| Supplier | Metric | 2024 value |

|---|---|---|

| Retail deposits | Population / LDR | 23.5M / 81% |

| Institutional funding | Market volatility | Wider spreads, shorter tenors |

| Vendors | Core banking market | USD 15bn |

| Regulator | Deposit insurance | NT$3,000,000 |

| Talent | SME share | 97% firms, 78% employment |

What is included in the product

Tailored Porter’s Five Forces analysis for Taiwan Business Bank that uncovers key drivers of competition, customer influence, and market entry risks. It evaluates supplier and buyer power, identifies substitutes and disruptive threats, and highlights dynamics that deter entrants to protect incumbency.

A concise one-sheet Porter's Five Forces for Taiwan Business Bank—perfect for quick decision-making and board decks. Swap in your own data or duplicate tabs for scenario testing (pre/post regulation, new entrants) with no complex code required.

Customers Bargaining Power

SME clientele price sensitivity

SMEs are highly cost-conscious on loan rates and fees, elevating buyer power. SMEs account for roughly 97% of Taiwanese firms and employ about 78% of the workforce, concentrating negotiating influence. Relationship banking, collateral structures and bundled services raise switching frictions, blunting pure price pressure. Government guarantee schemes and value-added advisory in 2024 help standardize terms and compress spreads.

Multi-banking and easy comparisons

Digital channels and aggregators let clients compare rates instantly; with Taiwan internet penetration over 90% in 2024, rate transparency has risen sharply. Larger SMEs typically maintain 2–4 banking relationships, increasing their leverage in fee and pricing negotiations. Transparent pricing shifts competition toward service quality and speed, while proactive RM coverage and tailored credit lines materially reduce churn.

Wealth and retail segments

Affluent clients shop wealth and FX pricing across banks and brokers, increasing price sensitivity and switching propensity. Robo-advisors and online brokers intensify fee pressure by offering lower-cost automated advisory and trading. Holistic financial planning and exclusive product access can reduce buyer power by creating higher switching costs. Loyalty programs and ecosystem partnerships strengthen retention and cross-sell opportunities.

Cross-border and FX users

Clients executing trade finance and remittances shop spreads and turnaround: 2024 benchmarks show fintech remitters at 0.2–0.5% vs traditional banks 0.5–1.0% and same‑day vs 1–3 day settlement.

Specialist FX platforms intensify price pressure, while end‑to‑end documentation and compliance assurance provide measurable non‑price differentiation and reduce operational risk.

Preferential tiers for corporates (eg, >US$1m turnover) delivering up to 20–50% fee discounts help Taiwan Business Bank rebalance customer bargaining power.

Credit quality dispersion

Credit quality dispersion drives bargaining power as higher-quality borrowers—large corporates and low-risk SMEs—can negotiate lower spreads and softer covenants, especially in benign credit cycles; conversely, when underwriting tightens and risk-based pricing is applied, margin erosion is contained and pricing discipline restored. Taiwan Business Bank’s diversified portfolio limits concentration risk and reduces any single buyer group’s leverage.

- Higher-quality borrowers: stronger negotiation

- Loose cycles: rises in low-risk segment power

- Tight underwriting: curbs margin erosion

- Diversification: limits exposure to one buyer group

SME-driven pricing and 92% internet penetration fuel fintech fee transparency and switching

SMEs (97% of firms; 78% of employment) drive strong buyer power on loan pricing; Taiwan internet penetration ~92% in 2024 raises rate transparency. Fintech remitters/spreads 0.2–0.5% vs banks 0.5–1.0%, same‑day vs 1–3 day settlement increases switching. Volume tiers (eg >US$1m) offer up to 50% fee discounts; portfolio diversification limits single‑group leverage.

| Metric | 2024 |

|---|---|

| SME share of firms | 97% |

| SME employment | 78% |

| Internet penetration | ~92% |

| Fintech spreads | 0.2–0.5% |

| Bank spreads | 0.5–1.0% |

| Volume discounts | up to 50% |

Full Version Awaits

Taiwan Business Bank Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Taiwan Business Bank you’ll receive—fully formatted and ready to use. The document is the final deliverable, not a sample or placeholder, and will be available instantly after purchase. No surprises, download and use immediately.