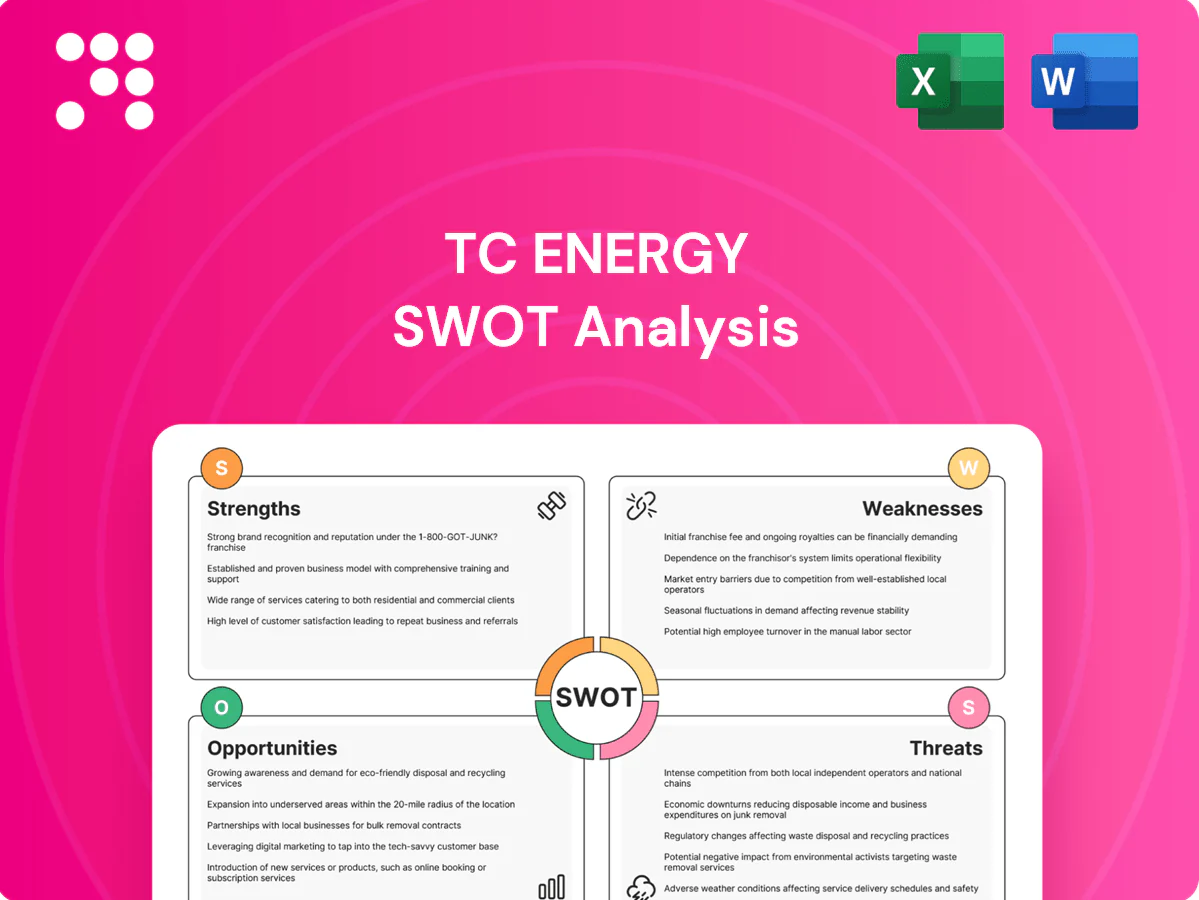

TC Energy SWOT Analysis

Make Insightful Decisions Backed by Expert Research

TC Energy’s SWOT highlights robust pipeline assets and regulated cash flows, balanced by regulatory and ESG risks; growth hinges on LNG and midstream optimization. Want the full story behind strengths, risks, and growth drivers? Purchase the complete SWOT analysis to get a fully editable, investor-ready report and Excel matrix.

Strengths

Extensive North American pipeline network

TC Energy operates a contiguous North American pipeline system of roughly 92,800 kilometres across Canada, the US and Mexico, giving wide market reach and route optionality. Network effects boost reliability and utilization, lowering unit operating costs per unit transported. Geographic diversification reduces reliance on any single basin or demand center. This scale and interconnected footprint create substantial barriers to entry for competitors.

Stable, long-term contracted cash flows

Take-or-pay and regulated tariff structures underpin predictable revenue for TC Energy, which operates about 93,000 km of pipelines and generates a majority of cash from fee-based contracts. Long-duration agreements with investment-grade counterparties reduce volume and price risk, giving multi-year cash flow visibility that supports capital plans and a stable dividend policy. This stability strengthens the credit profile and lowers the companys cost of capital.

Integrated gas value-chain capabilities

TC Energy’s integrated gas value chain—with over 90,000 km of pipelines plus large-scale storage and interconnects across Canada and the US—boosts system flexibility. Storage and balancing services generate ancillary revenue and raise customer stickiness. Integration supports reliability across seasonal and peak demand swings. This cements TC Energy as a critical infrastructure provider.

Operational excellence and safety culture

TC Energy operates roughly 93,300 km (about 57,900 miles) of natural gas and liquids pipelines, with established construction, integrity management and monitoring programs that limit downtime and enable rapid incident response. Scale supports deployment of best practices and cost efficiencies; consistent safety performance reduces liability and regulatory friction, strengthening reliability and shipper/regulator trust.

- Network: ~93,300 km pipelines

- Strength: robust integrity & monitoring

- Benefit: cost efficiencies from scale

- Outcome: reliability builds shipper/regulator trust

Diversification into power and energy storage

Diversification into power and energy storage gives TC Energy non-pipeline earnings streams that offset commodity and tariff cyclicality tied to its ~92,600 km transmission network; power and storage address grid reliability and renewable intermittency, creating optionality for participation in low-carbon transitions while leveraging existing customer and regulatory relationships.

- earnings diversification

- grid reliability upside

- low-carbon optionality

- leverages customer/regulatory ties

North American pipeline: ~93,300 km - fee-based cash flows, storage & power

TC Energy operates ~93,300 km of pipelines across Canada, US and Mexico, creating route optionality and high utilization. Fee-based and take-or-pay contracts provide predictable, multi-year cash flows and support investment-grade credit metrics. Integrated storage, power and regulated tariffs diversify earnings and enhance system reliability.

| Metric | Value |

|---|---|

| Pipeline network | ~93,300 km |

| Revenue type | Majority fee-based / take-or-pay |

| Diversification | Power & storage added |

What is included in the product

Delivers a strategic overview of TC Energy’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position across regulated pipelines, power and gas markets.

Provides a concise SWOT matrix for TC Energy to align strategy quickly and address regulatory, operational, and market pain points; editable format enables rapid updates to reflect pipeline developments and shifting energy policies.

Weaknesses

High capital intensity and long payback periods

Large greenfield projects require multi-billion-dollar upfront investment, often exceeding CAD 2–5 billion per project. Long construction timelines expose projects to delays and cost inflation, as seen across North American pipeline builds. Payback can span a decade and hinges on regulatory approvals and persistent demand. High capital intensity limits balance sheet flexibility during downturns.

Regulatory and permitting complexity

Multijurisdiction approvals for TC Energy projects increase timeline uncertainty, as seen with Trans Mountain where costs rose to about C$21.4 billion amid regulatory and stakeholder challenges. Opposition and litigation can force redesigns and stop-work orders, delaying in-service dates by years and deferring cash flow realization. Higher compliance and mitigation costs push project breakevens up and compress IRRs, straining returns on large-capital projects.

Concentration in hydrocarbons

Despite diversification, TC Energy's revenue remains heavily tied to hydrocarbon transport—pipelines and liquids dominate operations. Policy shifts such as Canada’s 40–45% GHG reduction by 2030 and net-zero by 2050, and IEA net-zero scenarios, threaten long-term demand. Rising ESG investing (global sustainable assets ~$41.1 trillion in 2022) can lift equity risk premia. Multi-decade asset-stranding risk for trunk pipelines is material.

Exposure to counterparty and basin risks

Shipper financial-health volatility raises contract-renewal and credit-loss risk for TC Energy, particularly where large customers dominate corridors; top-shipper concentration has historically driven earnings sensitivity. Basin-specific declines can cut throughput at re-contracting; oversupplied corridors invite tariff pressure during renegotiation. TC Energy operates about 57,500 km of pipelines across Canada, the US and Mexico, concentrating exposure in key basins.

- Shipper credit risk

- Basin throughput volatility

- Tariff renegotiation pressure

- Concentrated customers/basins

Legacy asset maintenance liabilities

Ageing pipelines across TC Energy’s ~92,600 km network drive ongoing integrity and upgrade spending, with unplanned outages or incidents generating material remediation costs and operational disruption. Maintenance capex increasingly competes with growth allocation, while heightened public scrutiny raises monitoring and remediation expenses.

- Ageing network: ~92,600 km

- Higher integrity spend

- Maintenance vs growth capex

- Increased public/monitoring costs

Capital-intense pipelines: CAD 2-5B greenfields, regulatory overruns, ESG risk

High capital intensity: greenfield projects often cost CAD 2–5 billion and carry multi‑year paybacks, limiting balance sheet flexibility. Multijurisdiction approvals and opposition raise schedule/cost risk—Trans Mountain costs rose to ~C$21.4 billion. Revenue remains hydrocarbon‑linked despite energy transition risks; pipeline network ~92,600 km increases integrity spend and outage exposure.

| Weakness | Metric | 2024/25 Data |

|---|---|---|

| Project capex | Typical greenfield | CAD 2–5B |

| Regulatory overruns | Trans Mountain cost | C$21.4B |

| Network scale | Total pipelines | ~92,600 km |

| ESG pressure | Global sustainable assets | ~US$41.1T (2022) |

Same Document Delivered

TC Energy SWOT Analysis

This is the actual TC Energy SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use once payment is completed.

Make Insightful Decisions Backed by Expert Research

TC Energy’s SWOT highlights robust pipeline assets and regulated cash flows, balanced by regulatory and ESG risks; growth hinges on LNG and midstream optimization. Want the full story behind strengths, risks, and growth drivers? Purchase the complete SWOT analysis to get a fully editable, investor-ready report and Excel matrix.

Strengths

Extensive North American pipeline network

TC Energy operates a contiguous North American pipeline system of roughly 92,800 kilometres across Canada, the US and Mexico, giving wide market reach and route optionality. Network effects boost reliability and utilization, lowering unit operating costs per unit transported. Geographic diversification reduces reliance on any single basin or demand center. This scale and interconnected footprint create substantial barriers to entry for competitors.

Stable, long-term contracted cash flows

Take-or-pay and regulated tariff structures underpin predictable revenue for TC Energy, which operates about 93,000 km of pipelines and generates a majority of cash from fee-based contracts. Long-duration agreements with investment-grade counterparties reduce volume and price risk, giving multi-year cash flow visibility that supports capital plans and a stable dividend policy. This stability strengthens the credit profile and lowers the companys cost of capital.

Integrated gas value-chain capabilities

TC Energy’s integrated gas value chain—with over 90,000 km of pipelines plus large-scale storage and interconnects across Canada and the US—boosts system flexibility. Storage and balancing services generate ancillary revenue and raise customer stickiness. Integration supports reliability across seasonal and peak demand swings. This cements TC Energy as a critical infrastructure provider.

Operational excellence and safety culture

TC Energy operates roughly 93,300 km (about 57,900 miles) of natural gas and liquids pipelines, with established construction, integrity management and monitoring programs that limit downtime and enable rapid incident response. Scale supports deployment of best practices and cost efficiencies; consistent safety performance reduces liability and regulatory friction, strengthening reliability and shipper/regulator trust.

- Network: ~93,300 km pipelines

- Strength: robust integrity & monitoring

- Benefit: cost efficiencies from scale

- Outcome: reliability builds shipper/regulator trust

Diversification into power and energy storage

Diversification into power and energy storage gives TC Energy non-pipeline earnings streams that offset commodity and tariff cyclicality tied to its ~92,600 km transmission network; power and storage address grid reliability and renewable intermittency, creating optionality for participation in low-carbon transitions while leveraging existing customer and regulatory relationships.

- earnings diversification

- grid reliability upside

- low-carbon optionality

- leverages customer/regulatory ties

North American pipeline: ~93,300 km - fee-based cash flows, storage & power

TC Energy operates ~93,300 km of pipelines across Canada, US and Mexico, creating route optionality and high utilization. Fee-based and take-or-pay contracts provide predictable, multi-year cash flows and support investment-grade credit metrics. Integrated storage, power and regulated tariffs diversify earnings and enhance system reliability.

| Metric | Value |

|---|---|

| Pipeline network | ~93,300 km |

| Revenue type | Majority fee-based / take-or-pay |

| Diversification | Power & storage added |

What is included in the product

Delivers a strategic overview of TC Energy’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position across regulated pipelines, power and gas markets.

Provides a concise SWOT matrix for TC Energy to align strategy quickly and address regulatory, operational, and market pain points; editable format enables rapid updates to reflect pipeline developments and shifting energy policies.

Weaknesses

High capital intensity and long payback periods

Large greenfield projects require multi-billion-dollar upfront investment, often exceeding CAD 2–5 billion per project. Long construction timelines expose projects to delays and cost inflation, as seen across North American pipeline builds. Payback can span a decade and hinges on regulatory approvals and persistent demand. High capital intensity limits balance sheet flexibility during downturns.

Regulatory and permitting complexity

Multijurisdiction approvals for TC Energy projects increase timeline uncertainty, as seen with Trans Mountain where costs rose to about C$21.4 billion amid regulatory and stakeholder challenges. Opposition and litigation can force redesigns and stop-work orders, delaying in-service dates by years and deferring cash flow realization. Higher compliance and mitigation costs push project breakevens up and compress IRRs, straining returns on large-capital projects.

Concentration in hydrocarbons

Despite diversification, TC Energy's revenue remains heavily tied to hydrocarbon transport—pipelines and liquids dominate operations. Policy shifts such as Canada’s 40–45% GHG reduction by 2030 and net-zero by 2050, and IEA net-zero scenarios, threaten long-term demand. Rising ESG investing (global sustainable assets ~$41.1 trillion in 2022) can lift equity risk premia. Multi-decade asset-stranding risk for trunk pipelines is material.

Exposure to counterparty and basin risks

Shipper financial-health volatility raises contract-renewal and credit-loss risk for TC Energy, particularly where large customers dominate corridors; top-shipper concentration has historically driven earnings sensitivity. Basin-specific declines can cut throughput at re-contracting; oversupplied corridors invite tariff pressure during renegotiation. TC Energy operates about 57,500 km of pipelines across Canada, the US and Mexico, concentrating exposure in key basins.

- Shipper credit risk

- Basin throughput volatility

- Tariff renegotiation pressure

- Concentrated customers/basins

Legacy asset maintenance liabilities

Ageing pipelines across TC Energy’s ~92,600 km network drive ongoing integrity and upgrade spending, with unplanned outages or incidents generating material remediation costs and operational disruption. Maintenance capex increasingly competes with growth allocation, while heightened public scrutiny raises monitoring and remediation expenses.

- Ageing network: ~92,600 km

- Higher integrity spend

- Maintenance vs growth capex

- Increased public/monitoring costs

Capital-intense pipelines: CAD 2-5B greenfields, regulatory overruns, ESG risk

High capital intensity: greenfield projects often cost CAD 2–5 billion and carry multi‑year paybacks, limiting balance sheet flexibility. Multijurisdiction approvals and opposition raise schedule/cost risk—Trans Mountain costs rose to ~C$21.4 billion. Revenue remains hydrocarbon‑linked despite energy transition risks; pipeline network ~92,600 km increases integrity spend and outage exposure.

| Weakness | Metric | 2024/25 Data |

|---|---|---|

| Project capex | Typical greenfield | CAD 2–5B |

| Regulatory overruns | Trans Mountain cost | C$21.4B |

| Network scale | Total pipelines | ~92,600 km |

| ESG pressure | Global sustainable assets | ~US$41.1T (2022) |

Same Document Delivered

TC Energy SWOT Analysis

This is the actual TC Energy SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use once payment is completed.

Description

Make Insightful Decisions Backed by Expert Research

TC Energy’s SWOT highlights robust pipeline assets and regulated cash flows, balanced by regulatory and ESG risks; growth hinges on LNG and midstream optimization. Want the full story behind strengths, risks, and growth drivers? Purchase the complete SWOT analysis to get a fully editable, investor-ready report and Excel matrix.

Strengths

Extensive North American pipeline network

TC Energy operates a contiguous North American pipeline system of roughly 92,800 kilometres across Canada, the US and Mexico, giving wide market reach and route optionality. Network effects boost reliability and utilization, lowering unit operating costs per unit transported. Geographic diversification reduces reliance on any single basin or demand center. This scale and interconnected footprint create substantial barriers to entry for competitors.

Stable, long-term contracted cash flows

Take-or-pay and regulated tariff structures underpin predictable revenue for TC Energy, which operates about 93,000 km of pipelines and generates a majority of cash from fee-based contracts. Long-duration agreements with investment-grade counterparties reduce volume and price risk, giving multi-year cash flow visibility that supports capital plans and a stable dividend policy. This stability strengthens the credit profile and lowers the companys cost of capital.

Integrated gas value-chain capabilities

TC Energy’s integrated gas value chain—with over 90,000 km of pipelines plus large-scale storage and interconnects across Canada and the US—boosts system flexibility. Storage and balancing services generate ancillary revenue and raise customer stickiness. Integration supports reliability across seasonal and peak demand swings. This cements TC Energy as a critical infrastructure provider.

Operational excellence and safety culture

TC Energy operates roughly 93,300 km (about 57,900 miles) of natural gas and liquids pipelines, with established construction, integrity management and monitoring programs that limit downtime and enable rapid incident response. Scale supports deployment of best practices and cost efficiencies; consistent safety performance reduces liability and regulatory friction, strengthening reliability and shipper/regulator trust.

- Network: ~93,300 km pipelines

- Strength: robust integrity & monitoring

- Benefit: cost efficiencies from scale

- Outcome: reliability builds shipper/regulator trust

Diversification into power and energy storage

Diversification into power and energy storage gives TC Energy non-pipeline earnings streams that offset commodity and tariff cyclicality tied to its ~92,600 km transmission network; power and storage address grid reliability and renewable intermittency, creating optionality for participation in low-carbon transitions while leveraging existing customer and regulatory relationships.

- earnings diversification

- grid reliability upside

- low-carbon optionality

- leverages customer/regulatory ties

North American pipeline: ~93,300 km - fee-based cash flows, storage & power

TC Energy operates ~93,300 km of pipelines across Canada, US and Mexico, creating route optionality and high utilization. Fee-based and take-or-pay contracts provide predictable, multi-year cash flows and support investment-grade credit metrics. Integrated storage, power and regulated tariffs diversify earnings and enhance system reliability.

| Metric | Value |

|---|---|

| Pipeline network | ~93,300 km |

| Revenue type | Majority fee-based / take-or-pay |

| Diversification | Power & storage added |

What is included in the product

Delivers a strategic overview of TC Energy’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position across regulated pipelines, power and gas markets.

Provides a concise SWOT matrix for TC Energy to align strategy quickly and address regulatory, operational, and market pain points; editable format enables rapid updates to reflect pipeline developments and shifting energy policies.

Weaknesses

High capital intensity and long payback periods

Large greenfield projects require multi-billion-dollar upfront investment, often exceeding CAD 2–5 billion per project. Long construction timelines expose projects to delays and cost inflation, as seen across North American pipeline builds. Payback can span a decade and hinges on regulatory approvals and persistent demand. High capital intensity limits balance sheet flexibility during downturns.

Regulatory and permitting complexity

Multijurisdiction approvals for TC Energy projects increase timeline uncertainty, as seen with Trans Mountain where costs rose to about C$21.4 billion amid regulatory and stakeholder challenges. Opposition and litigation can force redesigns and stop-work orders, delaying in-service dates by years and deferring cash flow realization. Higher compliance and mitigation costs push project breakevens up and compress IRRs, straining returns on large-capital projects.

Concentration in hydrocarbons

Despite diversification, TC Energy's revenue remains heavily tied to hydrocarbon transport—pipelines and liquids dominate operations. Policy shifts such as Canada’s 40–45% GHG reduction by 2030 and net-zero by 2050, and IEA net-zero scenarios, threaten long-term demand. Rising ESG investing (global sustainable assets ~$41.1 trillion in 2022) can lift equity risk premia. Multi-decade asset-stranding risk for trunk pipelines is material.

Exposure to counterparty and basin risks

Shipper financial-health volatility raises contract-renewal and credit-loss risk for TC Energy, particularly where large customers dominate corridors; top-shipper concentration has historically driven earnings sensitivity. Basin-specific declines can cut throughput at re-contracting; oversupplied corridors invite tariff pressure during renegotiation. TC Energy operates about 57,500 km of pipelines across Canada, the US and Mexico, concentrating exposure in key basins.

- Shipper credit risk

- Basin throughput volatility

- Tariff renegotiation pressure

- Concentrated customers/basins

Legacy asset maintenance liabilities

Ageing pipelines across TC Energy’s ~92,600 km network drive ongoing integrity and upgrade spending, with unplanned outages or incidents generating material remediation costs and operational disruption. Maintenance capex increasingly competes with growth allocation, while heightened public scrutiny raises monitoring and remediation expenses.

- Ageing network: ~92,600 km

- Higher integrity spend

- Maintenance vs growth capex

- Increased public/monitoring costs

Capital-intense pipelines: CAD 2-5B greenfields, regulatory overruns, ESG risk

High capital intensity: greenfield projects often cost CAD 2–5 billion and carry multi‑year paybacks, limiting balance sheet flexibility. Multijurisdiction approvals and opposition raise schedule/cost risk—Trans Mountain costs rose to ~C$21.4 billion. Revenue remains hydrocarbon‑linked despite energy transition risks; pipeline network ~92,600 km increases integrity spend and outage exposure.

| Weakness | Metric | 2024/25 Data |

|---|---|---|

| Project capex | Typical greenfield | CAD 2–5B |

| Regulatory overruns | Trans Mountain cost | C$21.4B |

| Network scale | Total pipelines | ~92,600 km |

| ESG pressure | Global sustainable assets | ~US$41.1T (2022) |

Same Document Delivered

TC Energy SWOT Analysis

This is the actual TC Energy SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use once payment is completed.