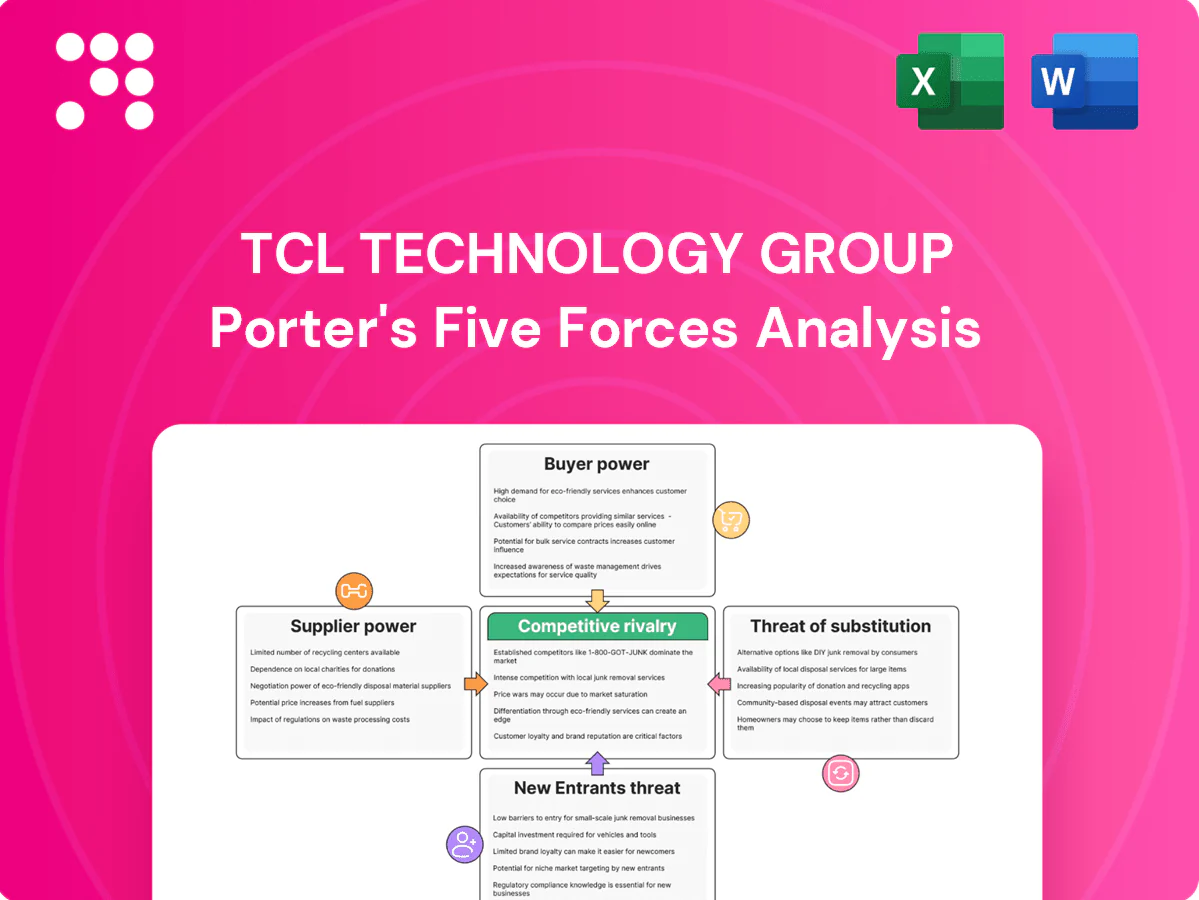

TCL Technology Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

TCL Technology Group faces intense rivalry, rising buyer sophistication, and moderate supplier leverage as it scales global display and smart device operations; threats from fast-moving entrants and substitutes pressure margins. This snapshot highlights key dynamics and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Vertical integration tempers dependence

Through CSOT and in-house module assembly, TCL internalizes key display inputs, reducing exposure to external panel suppliers and limiting price markups on strategic components while stabilizing lead times; by 2024 CSOT operated multiple Gen‑8 fabs supporting this shift. However, vertical integration shifts bargaining power upstream to raw‑material and equipment vendors, where silicon, glass and deposition tools remain concentrated. Net effect: supplier power moderated but not eliminated.

Upstream oligopolies in equipment/chemicals

Upstream oligopolies—ASML, Applied Materials, Lam Research, KLA and Tokyo Electron—held roughly 75% of semiconductor equipment revenue in 2024, while photoresists (JSR, Fujifilm, Sumitomo), specialty gases (Linde, Air Liquide, Praxair) and glass substrate markets are similarly concentrated, with top suppliers controlling around 60–80% of supply; this gives strong pricing and delivery priority power. Compliance and multi‑month qualification cycles materially raise switching costs, so TCL relies on multi‑year contracts and dual‑sourcing to mitigate supply disruption and pricing risk.

Commodity inputs with volatile pricing

Metals, plastics, rare earths and logistics costs for TCL fluctuate with global cycles and geopolitics; China supplied about 60% of global rare earths in 2024, concentrating supplier power. Price volatility passes into BOM and compresses margins as component costs swing quarter-to-quarter. Hedging and long-term contracts mitigate but cannot fully neutralize shocks. Scale buying and supplier consolidation give TCL some bargaining offsets.

Software and ecosystem dependencies

Licensing for OS, codecs and streaming apps concentrates influence in a few platforms; app-store revenue shares often reach 30% and certification fees per model can be in the low-to-mid five figures (2024). Certification requirements and revenue-share terms pressure panel economics and margins. Android TV/Google TV and Roku diversify options, but switching costs and engineering certification burdens remain non-trivial, so TCL maintains multiple ecosystem partnerships to reduce single-vendor reliance.

- OS concentration: app-store cuts up to 30%

- Certification costs: low-to-mid five figures/model (2024)

- Diversification: Android TV/Google TV/Roku reduce single-vendor risk

- Switching burden: engineering, certification and time-to-market impacts

Energy and utilities intensity

Display fabs and component plants are highly power- and water-intensive, with utilities often representing a material share of fab operating cost (commonly cited at up to 30% in industry analyses). Concentration in Guangdong/Huizhou exposes TCL to regional pricing and rationing shocks seen in recent China supply disruptions. Long-term utility contracts and on-site generation (solar/Gas CHP) can reduce supplier leverage. Sustainability mandates raise capex and compliance burdens.

- Exposure: regional concentration

- Cost: utilities significant (~up to 30%)

- Mitigation: long-term contracts, self-generation

- Risk: sustainability/regulatory compliance

Vertical integration cuts panel leverage; upstream oligopolies keep supplier power — 75/60/30%

Vertical integration via CSOT reduced panel supplier leverage, but upstream equipment and material oligopolies keep supplier power meaningful; ASML/Applied/Lam/KLA/TEL ~75% of semiconductor equipment revenue (2024). China supplied ~60% of rare earths (2024); app-store cuts up to 30% and certification fees low‑to‑mid five figures/model raise switching costs; utilities can be ~30% of fab OPEX.

| Metric | 2024 Data |

|---|---|

| Semiconductor equipment concentration | ~75% |

| China share of rare earths | ~60% |

| App-store revenue share | Up to 30% |

| Fab utilities OPEX | Up to 30% |

What is included in the product

Tailored Porter's Five Forces analysis for TCL Technology Group uncovering key drivers of competition, supplier and buyer power, and barriers to entry that shape profitability. Identifies disruptive substitutes and emerging threats while evaluating strategic levers TCL can use to defend market share and pricing.

A concise one-sheet Porter's Five Forces for TCL Technology that highlights supplier/customer power, competitive rivalry and threats of entry/substitutes—ideal for quick strategic fixes, customizable for current market shifts and ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Big-box retail and e-commerce leverage

Global retailers and platforms consolidate volume, forcing suppliers into lower pricing, MDF and promotional support; e‑commerce comprised about 24% of global retail sales in 2024 and Amazon held roughly 40% of US e‑commerce, amplifying buyer leverage. Control over shelf space and algorithms raises bargaining power, while chargebacks and strict SLAs shift fulfillment and quality costs onto suppliers. TCL frequently trades margin for scale and visibility to secure placement and volumes.

High price sensitivity in TVs/appliances

Categories are commoditized with transparent comparisons and frequent deal cycles, driving high price sensitivity; TCL held roughly 15% global TV market share in 2024. Consumers switch brands for small discounts, with peak‑sale discounts averaging about 12% in 2024, compressing gross margins. Promo intensity rose, pressuring ASPs, which fell ~6% YoY in 2024. Feature differentiation must justify any ASP premium to sustain margins.

Enterprise/OEM accounts concentrate demand

Enterprise/OEM, hospitality, signage and white-label customers place large negotiated orders that let a few buyers shape specs, delivery windows and warranty terms, increasing buyer leverage. Contract renewals—often annual or multi-year—create periodic pricing resets that pressure margins. TCL must defend share through stronger service offerings and lower total cost of ownership to retain these high-volume accounts.

Low switching costs, moderate lock-in

Bargaining power of customers is moderate: hardware swap is easy and brand loyalty is limited, though app ecosystems, UI familiarity and after-sales service create partial stickiness. Extended warranties and smart-home integration can deepen retention, but buyers can still exit at replacement cycles. TCL held about 9% global TV market share in 2023 (Omdia), underscoring competitive pressure.

- Low switching costs

- Partial lock-in: apps, UI, service

- Retention tools: warranties, smart-home

- Exit points: replacement cycles

Information-rich buyers

Information-rich buyers use reviews, benchmarks and price trackers to compare TCL devices across specs and updates, eroding information asymmetry and enabling aggressive bargaining; visible quality or OTA update failures quickly depress demand and review ratings, forcing faster remediation. Proactive communication and timely OTA improvements are therefore critical to preserve brand trust and margins.

- Reviews-driven purchases

- Benchmarks enable feature-for-price comparisons

- Price trackers increase switching

- OTA fixes reduce churn

Consolidated platforms, deep promos and falling ASPs squeeze TV makers' margins

Buyers hold moderate-to-high leverage as retail/platform consolidation and 24% global e-commerce (2024) with Amazon ~40% US e-commerce concentrate volume; TCL often trades margin for placement. Commoditization, 12% average promo depth (2024) and ASPs down ~6% YoY (2024) drive price sensitivity. Enterprise orders exert negotiated pressure despite partial stickiness from apps, warranties and smart‑home integration.

| Metric | Value | Implication |

|---|---|---|

| Global e‑commerce (2024) | 24% | Concentrated buyer power |

| Amazon US e‑commerce (2024) | ~40% | Platform leverage |

| TCL TV share (2024) | ~15% | Scale but margin pressure |

| Avg promo depth (2024) | 12% | Compresses ASPs |

| ASPs YoY (2024) | -6% | Margin erosion |

Same Document Delivered

TCL Technology Group Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis of TCL Technology Group, covering industry rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with concise strategic implications. The document displayed is the exact professionally formatted file you'll receive immediately after purchase—no placeholders, no samples. It's ready for immediate download and use.

Go Beyond the Preview—Access the Full Strategic Report

TCL Technology Group faces intense rivalry, rising buyer sophistication, and moderate supplier leverage as it scales global display and smart device operations; threats from fast-moving entrants and substitutes pressure margins. This snapshot highlights key dynamics and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Vertical integration tempers dependence

Through CSOT and in-house module assembly, TCL internalizes key display inputs, reducing exposure to external panel suppliers and limiting price markups on strategic components while stabilizing lead times; by 2024 CSOT operated multiple Gen‑8 fabs supporting this shift. However, vertical integration shifts bargaining power upstream to raw‑material and equipment vendors, where silicon, glass and deposition tools remain concentrated. Net effect: supplier power moderated but not eliminated.

Upstream oligopolies in equipment/chemicals

Upstream oligopolies—ASML, Applied Materials, Lam Research, KLA and Tokyo Electron—held roughly 75% of semiconductor equipment revenue in 2024, while photoresists (JSR, Fujifilm, Sumitomo), specialty gases (Linde, Air Liquide, Praxair) and glass substrate markets are similarly concentrated, with top suppliers controlling around 60–80% of supply; this gives strong pricing and delivery priority power. Compliance and multi‑month qualification cycles materially raise switching costs, so TCL relies on multi‑year contracts and dual‑sourcing to mitigate supply disruption and pricing risk.

Commodity inputs with volatile pricing

Metals, plastics, rare earths and logistics costs for TCL fluctuate with global cycles and geopolitics; China supplied about 60% of global rare earths in 2024, concentrating supplier power. Price volatility passes into BOM and compresses margins as component costs swing quarter-to-quarter. Hedging and long-term contracts mitigate but cannot fully neutralize shocks. Scale buying and supplier consolidation give TCL some bargaining offsets.

Software and ecosystem dependencies

Licensing for OS, codecs and streaming apps concentrates influence in a few platforms; app-store revenue shares often reach 30% and certification fees per model can be in the low-to-mid five figures (2024). Certification requirements and revenue-share terms pressure panel economics and margins. Android TV/Google TV and Roku diversify options, but switching costs and engineering certification burdens remain non-trivial, so TCL maintains multiple ecosystem partnerships to reduce single-vendor reliance.

- OS concentration: app-store cuts up to 30%

- Certification costs: low-to-mid five figures/model (2024)

- Diversification: Android TV/Google TV/Roku reduce single-vendor risk

- Switching burden: engineering, certification and time-to-market impacts

Energy and utilities intensity

Display fabs and component plants are highly power- and water-intensive, with utilities often representing a material share of fab operating cost (commonly cited at up to 30% in industry analyses). Concentration in Guangdong/Huizhou exposes TCL to regional pricing and rationing shocks seen in recent China supply disruptions. Long-term utility contracts and on-site generation (solar/Gas CHP) can reduce supplier leverage. Sustainability mandates raise capex and compliance burdens.

- Exposure: regional concentration

- Cost: utilities significant (~up to 30%)

- Mitigation: long-term contracts, self-generation

- Risk: sustainability/regulatory compliance

Vertical integration cuts panel leverage; upstream oligopolies keep supplier power — 75/60/30%

Vertical integration via CSOT reduced panel supplier leverage, but upstream equipment and material oligopolies keep supplier power meaningful; ASML/Applied/Lam/KLA/TEL ~75% of semiconductor equipment revenue (2024). China supplied ~60% of rare earths (2024); app-store cuts up to 30% and certification fees low‑to‑mid five figures/model raise switching costs; utilities can be ~30% of fab OPEX.

| Metric | 2024 Data |

|---|---|

| Semiconductor equipment concentration | ~75% |

| China share of rare earths | ~60% |

| App-store revenue share | Up to 30% |

| Fab utilities OPEX | Up to 30% |

What is included in the product

Tailored Porter's Five Forces analysis for TCL Technology Group uncovering key drivers of competition, supplier and buyer power, and barriers to entry that shape profitability. Identifies disruptive substitutes and emerging threats while evaluating strategic levers TCL can use to defend market share and pricing.

A concise one-sheet Porter's Five Forces for TCL Technology that highlights supplier/customer power, competitive rivalry and threats of entry/substitutes—ideal for quick strategic fixes, customizable for current market shifts and ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Big-box retail and e-commerce leverage

Global retailers and platforms consolidate volume, forcing suppliers into lower pricing, MDF and promotional support; e‑commerce comprised about 24% of global retail sales in 2024 and Amazon held roughly 40% of US e‑commerce, amplifying buyer leverage. Control over shelf space and algorithms raises bargaining power, while chargebacks and strict SLAs shift fulfillment and quality costs onto suppliers. TCL frequently trades margin for scale and visibility to secure placement and volumes.

High price sensitivity in TVs/appliances

Categories are commoditized with transparent comparisons and frequent deal cycles, driving high price sensitivity; TCL held roughly 15% global TV market share in 2024. Consumers switch brands for small discounts, with peak‑sale discounts averaging about 12% in 2024, compressing gross margins. Promo intensity rose, pressuring ASPs, which fell ~6% YoY in 2024. Feature differentiation must justify any ASP premium to sustain margins.

Enterprise/OEM accounts concentrate demand

Enterprise/OEM, hospitality, signage and white-label customers place large negotiated orders that let a few buyers shape specs, delivery windows and warranty terms, increasing buyer leverage. Contract renewals—often annual or multi-year—create periodic pricing resets that pressure margins. TCL must defend share through stronger service offerings and lower total cost of ownership to retain these high-volume accounts.

Low switching costs, moderate lock-in

Bargaining power of customers is moderate: hardware swap is easy and brand loyalty is limited, though app ecosystems, UI familiarity and after-sales service create partial stickiness. Extended warranties and smart-home integration can deepen retention, but buyers can still exit at replacement cycles. TCL held about 9% global TV market share in 2023 (Omdia), underscoring competitive pressure.

- Low switching costs

- Partial lock-in: apps, UI, service

- Retention tools: warranties, smart-home

- Exit points: replacement cycles

Information-rich buyers

Information-rich buyers use reviews, benchmarks and price trackers to compare TCL devices across specs and updates, eroding information asymmetry and enabling aggressive bargaining; visible quality or OTA update failures quickly depress demand and review ratings, forcing faster remediation. Proactive communication and timely OTA improvements are therefore critical to preserve brand trust and margins.

- Reviews-driven purchases

- Benchmarks enable feature-for-price comparisons

- Price trackers increase switching

- OTA fixes reduce churn

Consolidated platforms, deep promos and falling ASPs squeeze TV makers' margins

Buyers hold moderate-to-high leverage as retail/platform consolidation and 24% global e-commerce (2024) with Amazon ~40% US e-commerce concentrate volume; TCL often trades margin for placement. Commoditization, 12% average promo depth (2024) and ASPs down ~6% YoY (2024) drive price sensitivity. Enterprise orders exert negotiated pressure despite partial stickiness from apps, warranties and smart‑home integration.

| Metric | Value | Implication |

|---|---|---|

| Global e‑commerce (2024) | 24% | Concentrated buyer power |

| Amazon US e‑commerce (2024) | ~40% | Platform leverage |

| TCL TV share (2024) | ~15% | Scale but margin pressure |

| Avg promo depth (2024) | 12% | Compresses ASPs |

| ASPs YoY (2024) | -6% | Margin erosion |

Same Document Delivered

TCL Technology Group Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis of TCL Technology Group, covering industry rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with concise strategic implications. The document displayed is the exact professionally formatted file you'll receive immediately after purchase—no placeholders, no samples. It's ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

TCL Technology Group faces intense rivalry, rising buyer sophistication, and moderate supplier leverage as it scales global display and smart device operations; threats from fast-moving entrants and substitutes pressure margins. This snapshot highlights key dynamics and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Vertical integration tempers dependence

Through CSOT and in-house module assembly, TCL internalizes key display inputs, reducing exposure to external panel suppliers and limiting price markups on strategic components while stabilizing lead times; by 2024 CSOT operated multiple Gen‑8 fabs supporting this shift. However, vertical integration shifts bargaining power upstream to raw‑material and equipment vendors, where silicon, glass and deposition tools remain concentrated. Net effect: supplier power moderated but not eliminated.

Upstream oligopolies in equipment/chemicals

Upstream oligopolies—ASML, Applied Materials, Lam Research, KLA and Tokyo Electron—held roughly 75% of semiconductor equipment revenue in 2024, while photoresists (JSR, Fujifilm, Sumitomo), specialty gases (Linde, Air Liquide, Praxair) and glass substrate markets are similarly concentrated, with top suppliers controlling around 60–80% of supply; this gives strong pricing and delivery priority power. Compliance and multi‑month qualification cycles materially raise switching costs, so TCL relies on multi‑year contracts and dual‑sourcing to mitigate supply disruption and pricing risk.

Commodity inputs with volatile pricing

Metals, plastics, rare earths and logistics costs for TCL fluctuate with global cycles and geopolitics; China supplied about 60% of global rare earths in 2024, concentrating supplier power. Price volatility passes into BOM and compresses margins as component costs swing quarter-to-quarter. Hedging and long-term contracts mitigate but cannot fully neutralize shocks. Scale buying and supplier consolidation give TCL some bargaining offsets.

Software and ecosystem dependencies

Licensing for OS, codecs and streaming apps concentrates influence in a few platforms; app-store revenue shares often reach 30% and certification fees per model can be in the low-to-mid five figures (2024). Certification requirements and revenue-share terms pressure panel economics and margins. Android TV/Google TV and Roku diversify options, but switching costs and engineering certification burdens remain non-trivial, so TCL maintains multiple ecosystem partnerships to reduce single-vendor reliance.

- OS concentration: app-store cuts up to 30%

- Certification costs: low-to-mid five figures/model (2024)

- Diversification: Android TV/Google TV/Roku reduce single-vendor risk

- Switching burden: engineering, certification and time-to-market impacts

Energy and utilities intensity

Display fabs and component plants are highly power- and water-intensive, with utilities often representing a material share of fab operating cost (commonly cited at up to 30% in industry analyses). Concentration in Guangdong/Huizhou exposes TCL to regional pricing and rationing shocks seen in recent China supply disruptions. Long-term utility contracts and on-site generation (solar/Gas CHP) can reduce supplier leverage. Sustainability mandates raise capex and compliance burdens.

- Exposure: regional concentration

- Cost: utilities significant (~up to 30%)

- Mitigation: long-term contracts, self-generation

- Risk: sustainability/regulatory compliance

Vertical integration cuts panel leverage; upstream oligopolies keep supplier power — 75/60/30%

Vertical integration via CSOT reduced panel supplier leverage, but upstream equipment and material oligopolies keep supplier power meaningful; ASML/Applied/Lam/KLA/TEL ~75% of semiconductor equipment revenue (2024). China supplied ~60% of rare earths (2024); app-store cuts up to 30% and certification fees low‑to‑mid five figures/model raise switching costs; utilities can be ~30% of fab OPEX.

| Metric | 2024 Data |

|---|---|

| Semiconductor equipment concentration | ~75% |

| China share of rare earths | ~60% |

| App-store revenue share | Up to 30% |

| Fab utilities OPEX | Up to 30% |

What is included in the product

Tailored Porter's Five Forces analysis for TCL Technology Group uncovering key drivers of competition, supplier and buyer power, and barriers to entry that shape profitability. Identifies disruptive substitutes and emerging threats while evaluating strategic levers TCL can use to defend market share and pricing.

A concise one-sheet Porter's Five Forces for TCL Technology that highlights supplier/customer power, competitive rivalry and threats of entry/substitutes—ideal for quick strategic fixes, customizable for current market shifts and ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Big-box retail and e-commerce leverage

Global retailers and platforms consolidate volume, forcing suppliers into lower pricing, MDF and promotional support; e‑commerce comprised about 24% of global retail sales in 2024 and Amazon held roughly 40% of US e‑commerce, amplifying buyer leverage. Control over shelf space and algorithms raises bargaining power, while chargebacks and strict SLAs shift fulfillment and quality costs onto suppliers. TCL frequently trades margin for scale and visibility to secure placement and volumes.

High price sensitivity in TVs/appliances

Categories are commoditized with transparent comparisons and frequent deal cycles, driving high price sensitivity; TCL held roughly 15% global TV market share in 2024. Consumers switch brands for small discounts, with peak‑sale discounts averaging about 12% in 2024, compressing gross margins. Promo intensity rose, pressuring ASPs, which fell ~6% YoY in 2024. Feature differentiation must justify any ASP premium to sustain margins.

Enterprise/OEM accounts concentrate demand

Enterprise/OEM, hospitality, signage and white-label customers place large negotiated orders that let a few buyers shape specs, delivery windows and warranty terms, increasing buyer leverage. Contract renewals—often annual or multi-year—create periodic pricing resets that pressure margins. TCL must defend share through stronger service offerings and lower total cost of ownership to retain these high-volume accounts.

Low switching costs, moderate lock-in

Bargaining power of customers is moderate: hardware swap is easy and brand loyalty is limited, though app ecosystems, UI familiarity and after-sales service create partial stickiness. Extended warranties and smart-home integration can deepen retention, but buyers can still exit at replacement cycles. TCL held about 9% global TV market share in 2023 (Omdia), underscoring competitive pressure.

- Low switching costs

- Partial lock-in: apps, UI, service

- Retention tools: warranties, smart-home

- Exit points: replacement cycles

Information-rich buyers

Information-rich buyers use reviews, benchmarks and price trackers to compare TCL devices across specs and updates, eroding information asymmetry and enabling aggressive bargaining; visible quality or OTA update failures quickly depress demand and review ratings, forcing faster remediation. Proactive communication and timely OTA improvements are therefore critical to preserve brand trust and margins.

- Reviews-driven purchases

- Benchmarks enable feature-for-price comparisons

- Price trackers increase switching

- OTA fixes reduce churn

Consolidated platforms, deep promos and falling ASPs squeeze TV makers' margins

Buyers hold moderate-to-high leverage as retail/platform consolidation and 24% global e-commerce (2024) with Amazon ~40% US e-commerce concentrate volume; TCL often trades margin for placement. Commoditization, 12% average promo depth (2024) and ASPs down ~6% YoY (2024) drive price sensitivity. Enterprise orders exert negotiated pressure despite partial stickiness from apps, warranties and smart‑home integration.

| Metric | Value | Implication |

|---|---|---|

| Global e‑commerce (2024) | 24% | Concentrated buyer power |

| Amazon US e‑commerce (2024) | ~40% | Platform leverage |

| TCL TV share (2024) | ~15% | Scale but margin pressure |

| Avg promo depth (2024) | 12% | Compresses ASPs |

| ASPs YoY (2024) | -6% | Margin erosion |

Same Document Delivered

TCL Technology Group Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis of TCL Technology Group, covering industry rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with concise strategic implications. The document displayed is the exact professionally formatted file you'll receive immediately after purchase—no placeholders, no samples. It's ready for immediate download and use.