TCM Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

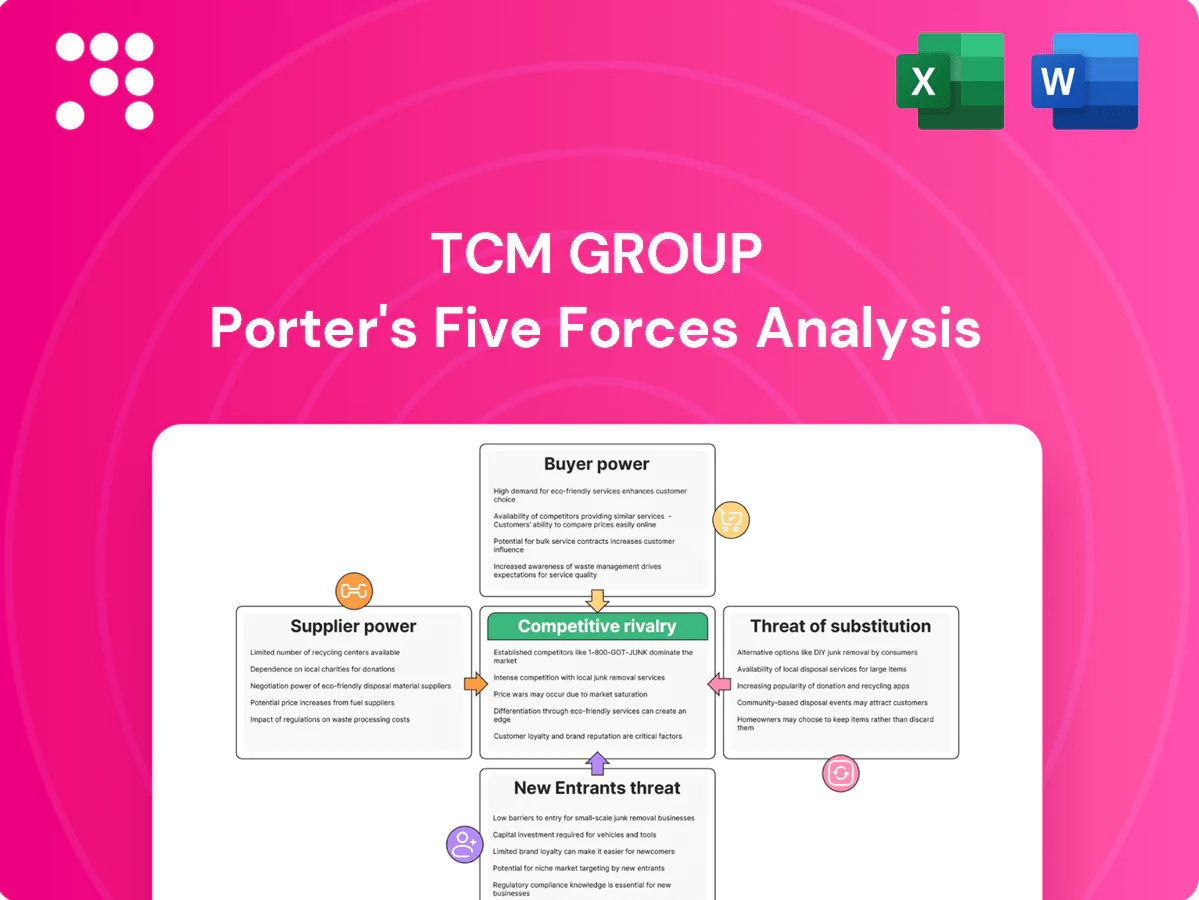

This snapshot highlights TCM Group’s competitive tensions across supplier leverage, buyer power, and new entrant threats, offering a clear but concise view of market dynamics. The brief flags key strategic pressures and potential vulnerabilities that merit deeper, data-driven analysis. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations tailored to TCM Group.

Suppliers Bargaining Power

Concentrated hardware suppliers

High-quality hinges, slides and fittings are concentrated among a few European suppliers (Blum ~€1.9bn revenue 2023; Hettich ~€1.2bn), giving them leverage on pricing and terms in 2024. TCM can dual-source but tight performance specs limit viable alternatives. Long-term contracts and volume commitments partially mitigate this power, yet a 10% supplier price rise can quickly shave several percentage points off gross margins.

Commodity wood panels and laminates

Particleboard, MDF and laminates remain widely available, keeping switching costs moderate, but global timber and resin market volatility has transmitted upstream shocks (notable price spikes during 2021–24).

FSC and PEFC certification constrains the supplier pool—combined certified forest area exceeded 500 million hectares in 2024—raising compliance and traceability costs.

Producers mitigate risk via hedging and 2–6 weeks of strategic inventories, yet these measures do not fully neutralize raw-material price pass-through.

Finishes, adhesives, and coatings

Chemical inputs for finishes, adhesives and coatings face specification lock-in and regulatory constraints—ECHA lists ~22,000 REACH-registered substances (2024)—which raises supplier stickiness. EU VOC rules (Directive 2004/42/EC) set limits down to about 30 g/L for some paints, reducing viable substitutes and lifting supplier power. Quality risks from switching (adhesion failures) deter frequent changes, so buyers use framework agreements to trade lower prices for guaranteed supply and specs.

Logistics and energy dependencies

Energy-intensive manufacturing leaves TCM exposed to utility pricing; industry accounts for about 37% of global final energy use (IEA), magnifying supplier leverage on costs. Volatile freight markets and carrier capacity directly affect inbound materials and store deliveries, while regional sourcing cuts—but does not eliminate—this exposure. Targeted energy-efficiency investments can structurally reduce supplier leverage over time.

- energy-exposure: high (industry ~37% global final energy use)

- freight-risk: affects inbound/outbound margins

- regional-sourcing: lowers but not removes risk

- capex-opportunity: efficiency reduces long-run supplier power

Digital tools and machinery vendors

Digital tools and machinery vendors: CNC, ERP and design/configuration software tie operations to specific vendors, concentrating supplier power; global CNC market was about USD 13B in 2024 and ERP ~USD 50B in 2024, amplifying switching costs. Upgrades and maintenance create quasi-lock-in and lifecycle costs that can add meaningful recurring spend. Negotiating enterprise licenses and strict SLAs can curb leverage while adopting open standards (STEP, OPC UA) reduces dependence over time.

- Vendor lock-in: CNC/ERP integration raises switching costs

- Market size: CNC ~USD 13B, ERP ~USD 50B (2024)

- Lifecycle spend: upgrades/maintenance drive recurring costs

- Mitigation: enterprise contracts, SLAs, open standards

Fittings concentration boosts supplier pricing power; panels volatile after 2021–24 shocks

High-end fittings concentrated (Blum €1.9bn, Hettich €1.2bn in 2023) giving pricing leverage in 2024; dual-sourcing limited by specs. Bulk panels more contestable but 2021–24 raw-material shocks raise volatility. Certification and regulatory constraints narrow supplier pool and raise costs. Energy, freight and CNC/ERP lock-in sustain supplier power despite hedging and inventories.

| Metric | 2024 figure | Impact |

|---|---|---|

| Blum revenue | €1.9bn (2023) | Supplier leverage |

| Hettich revenue | €1.2bn (2023) | Concentration |

| Certified forest area | >500m ha (2024) | Compliance cost |

| CNC market | USD 13B (2024) | Vendor lock-in |

| ERP market | USD 50B (2024) | Switching cost |

| Industry energy use | ~37% | Cost exposure |

| REACH substances | ~22,000 (2024) | Regulatory constraints |

What is included in the product

Concise Porter's Five Forces analysis of TCM Group highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive trends and entry barriers that shape TCM's pricing power and strategic positioning.

One-sheet Porter's Five Forces for TCM Group—quickly visualize competitive pressure with a clean radar chart, customize force levels to reflect new data or scenarios, and drop into pitch decks or dashboards without macros or complex setup.

Customers Bargaining Power

Franchisees and independent retailers

Franchisees and independent retailers buy at scale and in 2024 negotiated rebates commonly up to 8% and credit terms averaging around 60 days, giving them clear bargaining leverage. Their ability to switch brands strengthens negotiating power, though multi‑year showroom investments and local fit‑outs create material switching frictions. Strong brand pull from Svane, Tvis, Nettoline and kitchn offsets some pressure by driving footfall and margins. Performance‑based incentives and tiered rebates align interests and reduce churn.

End-consumer price transparency

End-consumer price transparency is amplified by online configurators and competing quotes: in 2024 about 62% of buyers used digital tools to compare styles, materials and delivery times, pushing retailers toward routine discounts. Strong design, white-glove service and extended warranties reduce pure price comparisons and retain margin. Offering point-of-sale financing and targeted promotions raised close rates by roughly 14% in sector studies last year.

Project and trade customers

Builders and renovators place larger, repeat orders with tight lead times, giving project customers outsized leverage over price and service levels. Industry surveys in 2024 indicate project/trade accounts can represent around 30% of supplier revenue and more than half of order-value volatility, concentrating negotiating power. Contractual penalties for delays shift delivery risk and costs onto TCM, while framework agreements lock volumes but typically compress margins.

Customization and switching costs

Made-to-measure designs raise perceived uniqueness and reduce like-for-like comparisons, while comprehensive post-sale support and warranty terms increase customer stickiness; however, cross-brand modular components keep substitution viable and design-file portability can accelerate churn.

- Customization reduces direct comparison

- Warranty/support increase retention

- Modularity enables future substitution

- Data portability raises churn risk

Demand cyclicality

Macro downturns (IMF 2024 global growth 3.0%) amplify buyer power as deferred renovations and aggressive price negotiation increase; in upcycles capacity constraints and shorter lead times shift leverage back to TCM. Regular promotional calendars train customers to wait for discounts, while a diversified brand portfolio smooths revenue volatility across cycles.

- Downturns: deferred demand → stronger buyers

- Upcycles: capacity limits → TCM pricing power

- Promotions: conditions waiting behavior

- Diversification: reduces cycle-driven swings

Retailers secure up to 8% rebates, ~60-day terms; configurators and POS lift close rates 14%

Franchisees/retailers secure rebates up to 8% and ~60-day terms in 2024, giving clear leverage. 62% of consumers used digital configurators, pressuring prices despite brand pull from Svane/Tvis. Project accounts ≈30% revenue, driving order volatility and stronger buyer bargaining. Downturns (IMF 2024 growth 3.0%) amplify buyer power; POS financing lifted close rates ~14%.

Full Version Awaits

TCM Group Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for TCM Group you'll receive—fully formatted, comprehensive and ready for immediate use. The document contains the same strategic assessment, industry forces, evidence-backed insights and implications that will be available for instant download after purchase.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This snapshot highlights TCM Group’s competitive tensions across supplier leverage, buyer power, and new entrant threats, offering a clear but concise view of market dynamics. The brief flags key strategic pressures and potential vulnerabilities that merit deeper, data-driven analysis. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations tailored to TCM Group.

Suppliers Bargaining Power

Concentrated hardware suppliers

High-quality hinges, slides and fittings are concentrated among a few European suppliers (Blum ~€1.9bn revenue 2023; Hettich ~€1.2bn), giving them leverage on pricing and terms in 2024. TCM can dual-source but tight performance specs limit viable alternatives. Long-term contracts and volume commitments partially mitigate this power, yet a 10% supplier price rise can quickly shave several percentage points off gross margins.

Commodity wood panels and laminates

Particleboard, MDF and laminates remain widely available, keeping switching costs moderate, but global timber and resin market volatility has transmitted upstream shocks (notable price spikes during 2021–24).

FSC and PEFC certification constrains the supplier pool—combined certified forest area exceeded 500 million hectares in 2024—raising compliance and traceability costs.

Producers mitigate risk via hedging and 2–6 weeks of strategic inventories, yet these measures do not fully neutralize raw-material price pass-through.

Finishes, adhesives, and coatings

Chemical inputs for finishes, adhesives and coatings face specification lock-in and regulatory constraints—ECHA lists ~22,000 REACH-registered substances (2024)—which raises supplier stickiness. EU VOC rules (Directive 2004/42/EC) set limits down to about 30 g/L for some paints, reducing viable substitutes and lifting supplier power. Quality risks from switching (adhesion failures) deter frequent changes, so buyers use framework agreements to trade lower prices for guaranteed supply and specs.

Logistics and energy dependencies

Energy-intensive manufacturing leaves TCM exposed to utility pricing; industry accounts for about 37% of global final energy use (IEA), magnifying supplier leverage on costs. Volatile freight markets and carrier capacity directly affect inbound materials and store deliveries, while regional sourcing cuts—but does not eliminate—this exposure. Targeted energy-efficiency investments can structurally reduce supplier leverage over time.

- energy-exposure: high (industry ~37% global final energy use)

- freight-risk: affects inbound/outbound margins

- regional-sourcing: lowers but not removes risk

- capex-opportunity: efficiency reduces long-run supplier power

Digital tools and machinery vendors

Digital tools and machinery vendors: CNC, ERP and design/configuration software tie operations to specific vendors, concentrating supplier power; global CNC market was about USD 13B in 2024 and ERP ~USD 50B in 2024, amplifying switching costs. Upgrades and maintenance create quasi-lock-in and lifecycle costs that can add meaningful recurring spend. Negotiating enterprise licenses and strict SLAs can curb leverage while adopting open standards (STEP, OPC UA) reduces dependence over time.

- Vendor lock-in: CNC/ERP integration raises switching costs

- Market size: CNC ~USD 13B, ERP ~USD 50B (2024)

- Lifecycle spend: upgrades/maintenance drive recurring costs

- Mitigation: enterprise contracts, SLAs, open standards

Fittings concentration boosts supplier pricing power; panels volatile after 2021–24 shocks

High-end fittings concentrated (Blum €1.9bn, Hettich €1.2bn in 2023) giving pricing leverage in 2024; dual-sourcing limited by specs. Bulk panels more contestable but 2021–24 raw-material shocks raise volatility. Certification and regulatory constraints narrow supplier pool and raise costs. Energy, freight and CNC/ERP lock-in sustain supplier power despite hedging and inventories.

| Metric | 2024 figure | Impact |

|---|---|---|

| Blum revenue | €1.9bn (2023) | Supplier leverage |

| Hettich revenue | €1.2bn (2023) | Concentration |

| Certified forest area | >500m ha (2024) | Compliance cost |

| CNC market | USD 13B (2024) | Vendor lock-in |

| ERP market | USD 50B (2024) | Switching cost |

| Industry energy use | ~37% | Cost exposure |

| REACH substances | ~22,000 (2024) | Regulatory constraints |

What is included in the product

Concise Porter's Five Forces analysis of TCM Group highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive trends and entry barriers that shape TCM's pricing power and strategic positioning.

One-sheet Porter's Five Forces for TCM Group—quickly visualize competitive pressure with a clean radar chart, customize force levels to reflect new data or scenarios, and drop into pitch decks or dashboards without macros or complex setup.

Customers Bargaining Power

Franchisees and independent retailers

Franchisees and independent retailers buy at scale and in 2024 negotiated rebates commonly up to 8% and credit terms averaging around 60 days, giving them clear bargaining leverage. Their ability to switch brands strengthens negotiating power, though multi‑year showroom investments and local fit‑outs create material switching frictions. Strong brand pull from Svane, Tvis, Nettoline and kitchn offsets some pressure by driving footfall and margins. Performance‑based incentives and tiered rebates align interests and reduce churn.

End-consumer price transparency

End-consumer price transparency is amplified by online configurators and competing quotes: in 2024 about 62% of buyers used digital tools to compare styles, materials and delivery times, pushing retailers toward routine discounts. Strong design, white-glove service and extended warranties reduce pure price comparisons and retain margin. Offering point-of-sale financing and targeted promotions raised close rates by roughly 14% in sector studies last year.

Project and trade customers

Builders and renovators place larger, repeat orders with tight lead times, giving project customers outsized leverage over price and service levels. Industry surveys in 2024 indicate project/trade accounts can represent around 30% of supplier revenue and more than half of order-value volatility, concentrating negotiating power. Contractual penalties for delays shift delivery risk and costs onto TCM, while framework agreements lock volumes but typically compress margins.

Customization and switching costs

Made-to-measure designs raise perceived uniqueness and reduce like-for-like comparisons, while comprehensive post-sale support and warranty terms increase customer stickiness; however, cross-brand modular components keep substitution viable and design-file portability can accelerate churn.

- Customization reduces direct comparison

- Warranty/support increase retention

- Modularity enables future substitution

- Data portability raises churn risk

Demand cyclicality

Macro downturns (IMF 2024 global growth 3.0%) amplify buyer power as deferred renovations and aggressive price negotiation increase; in upcycles capacity constraints and shorter lead times shift leverage back to TCM. Regular promotional calendars train customers to wait for discounts, while a diversified brand portfolio smooths revenue volatility across cycles.

- Downturns: deferred demand → stronger buyers

- Upcycles: capacity limits → TCM pricing power

- Promotions: conditions waiting behavior

- Diversification: reduces cycle-driven swings

Retailers secure up to 8% rebates, ~60-day terms; configurators and POS lift close rates 14%

Franchisees/retailers secure rebates up to 8% and ~60-day terms in 2024, giving clear leverage. 62% of consumers used digital configurators, pressuring prices despite brand pull from Svane/Tvis. Project accounts ≈30% revenue, driving order volatility and stronger buyer bargaining. Downturns (IMF 2024 growth 3.0%) amplify buyer power; POS financing lifted close rates ~14%.

Full Version Awaits

TCM Group Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for TCM Group you'll receive—fully formatted, comprehensive and ready for immediate use. The document contains the same strategic assessment, industry forces, evidence-backed insights and implications that will be available for instant download after purchase.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This snapshot highlights TCM Group’s competitive tensions across supplier leverage, buyer power, and new entrant threats, offering a clear but concise view of market dynamics. The brief flags key strategic pressures and potential vulnerabilities that merit deeper, data-driven analysis. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations tailored to TCM Group.

Suppliers Bargaining Power

Concentrated hardware suppliers

High-quality hinges, slides and fittings are concentrated among a few European suppliers (Blum ~€1.9bn revenue 2023; Hettich ~€1.2bn), giving them leverage on pricing and terms in 2024. TCM can dual-source but tight performance specs limit viable alternatives. Long-term contracts and volume commitments partially mitigate this power, yet a 10% supplier price rise can quickly shave several percentage points off gross margins.

Commodity wood panels and laminates

Particleboard, MDF and laminates remain widely available, keeping switching costs moderate, but global timber and resin market volatility has transmitted upstream shocks (notable price spikes during 2021–24).

FSC and PEFC certification constrains the supplier pool—combined certified forest area exceeded 500 million hectares in 2024—raising compliance and traceability costs.

Producers mitigate risk via hedging and 2–6 weeks of strategic inventories, yet these measures do not fully neutralize raw-material price pass-through.

Finishes, adhesives, and coatings

Chemical inputs for finishes, adhesives and coatings face specification lock-in and regulatory constraints—ECHA lists ~22,000 REACH-registered substances (2024)—which raises supplier stickiness. EU VOC rules (Directive 2004/42/EC) set limits down to about 30 g/L for some paints, reducing viable substitutes and lifting supplier power. Quality risks from switching (adhesion failures) deter frequent changes, so buyers use framework agreements to trade lower prices for guaranteed supply and specs.

Logistics and energy dependencies

Energy-intensive manufacturing leaves TCM exposed to utility pricing; industry accounts for about 37% of global final energy use (IEA), magnifying supplier leverage on costs. Volatile freight markets and carrier capacity directly affect inbound materials and store deliveries, while regional sourcing cuts—but does not eliminate—this exposure. Targeted energy-efficiency investments can structurally reduce supplier leverage over time.

- energy-exposure: high (industry ~37% global final energy use)

- freight-risk: affects inbound/outbound margins

- regional-sourcing: lowers but not removes risk

- capex-opportunity: efficiency reduces long-run supplier power

Digital tools and machinery vendors

Digital tools and machinery vendors: CNC, ERP and design/configuration software tie operations to specific vendors, concentrating supplier power; global CNC market was about USD 13B in 2024 and ERP ~USD 50B in 2024, amplifying switching costs. Upgrades and maintenance create quasi-lock-in and lifecycle costs that can add meaningful recurring spend. Negotiating enterprise licenses and strict SLAs can curb leverage while adopting open standards (STEP, OPC UA) reduces dependence over time.

- Vendor lock-in: CNC/ERP integration raises switching costs

- Market size: CNC ~USD 13B, ERP ~USD 50B (2024)

- Lifecycle spend: upgrades/maintenance drive recurring costs

- Mitigation: enterprise contracts, SLAs, open standards

Fittings concentration boosts supplier pricing power; panels volatile after 2021–24 shocks

High-end fittings concentrated (Blum €1.9bn, Hettich €1.2bn in 2023) giving pricing leverage in 2024; dual-sourcing limited by specs. Bulk panels more contestable but 2021–24 raw-material shocks raise volatility. Certification and regulatory constraints narrow supplier pool and raise costs. Energy, freight and CNC/ERP lock-in sustain supplier power despite hedging and inventories.

| Metric | 2024 figure | Impact |

|---|---|---|

| Blum revenue | €1.9bn (2023) | Supplier leverage |

| Hettich revenue | €1.2bn (2023) | Concentration |

| Certified forest area | >500m ha (2024) | Compliance cost |

| CNC market | USD 13B (2024) | Vendor lock-in |

| ERP market | USD 50B (2024) | Switching cost |

| Industry energy use | ~37% | Cost exposure |

| REACH substances | ~22,000 (2024) | Regulatory constraints |

What is included in the product

Concise Porter's Five Forces analysis of TCM Group highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive trends and entry barriers that shape TCM's pricing power and strategic positioning.

One-sheet Porter's Five Forces for TCM Group—quickly visualize competitive pressure with a clean radar chart, customize force levels to reflect new data or scenarios, and drop into pitch decks or dashboards without macros or complex setup.

Customers Bargaining Power

Franchisees and independent retailers

Franchisees and independent retailers buy at scale and in 2024 negotiated rebates commonly up to 8% and credit terms averaging around 60 days, giving them clear bargaining leverage. Their ability to switch brands strengthens negotiating power, though multi‑year showroom investments and local fit‑outs create material switching frictions. Strong brand pull from Svane, Tvis, Nettoline and kitchn offsets some pressure by driving footfall and margins. Performance‑based incentives and tiered rebates align interests and reduce churn.

End-consumer price transparency

End-consumer price transparency is amplified by online configurators and competing quotes: in 2024 about 62% of buyers used digital tools to compare styles, materials and delivery times, pushing retailers toward routine discounts. Strong design, white-glove service and extended warranties reduce pure price comparisons and retain margin. Offering point-of-sale financing and targeted promotions raised close rates by roughly 14% in sector studies last year.

Project and trade customers

Builders and renovators place larger, repeat orders with tight lead times, giving project customers outsized leverage over price and service levels. Industry surveys in 2024 indicate project/trade accounts can represent around 30% of supplier revenue and more than half of order-value volatility, concentrating negotiating power. Contractual penalties for delays shift delivery risk and costs onto TCM, while framework agreements lock volumes but typically compress margins.

Customization and switching costs

Made-to-measure designs raise perceived uniqueness and reduce like-for-like comparisons, while comprehensive post-sale support and warranty terms increase customer stickiness; however, cross-brand modular components keep substitution viable and design-file portability can accelerate churn.

- Customization reduces direct comparison

- Warranty/support increase retention

- Modularity enables future substitution

- Data portability raises churn risk

Demand cyclicality

Macro downturns (IMF 2024 global growth 3.0%) amplify buyer power as deferred renovations and aggressive price negotiation increase; in upcycles capacity constraints and shorter lead times shift leverage back to TCM. Regular promotional calendars train customers to wait for discounts, while a diversified brand portfolio smooths revenue volatility across cycles.

- Downturns: deferred demand → stronger buyers

- Upcycles: capacity limits → TCM pricing power

- Promotions: conditions waiting behavior

- Diversification: reduces cycle-driven swings

Retailers secure up to 8% rebates, ~60-day terms; configurators and POS lift close rates 14%

Franchisees/retailers secure rebates up to 8% and ~60-day terms in 2024, giving clear leverage. 62% of consumers used digital configurators, pressuring prices despite brand pull from Svane/Tvis. Project accounts ≈30% revenue, driving order volatility and stronger buyer bargaining. Downturns (IMF 2024 growth 3.0%) amplify buyer power; POS financing lifted close rates ~14%.

Full Version Awaits

TCM Group Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for TCM Group you'll receive—fully formatted, comprehensive and ready for immediate use. The document contains the same strategic assessment, industry forces, evidence-backed insights and implications that will be available for instant download after purchase.