TCTM Kids IT Education PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

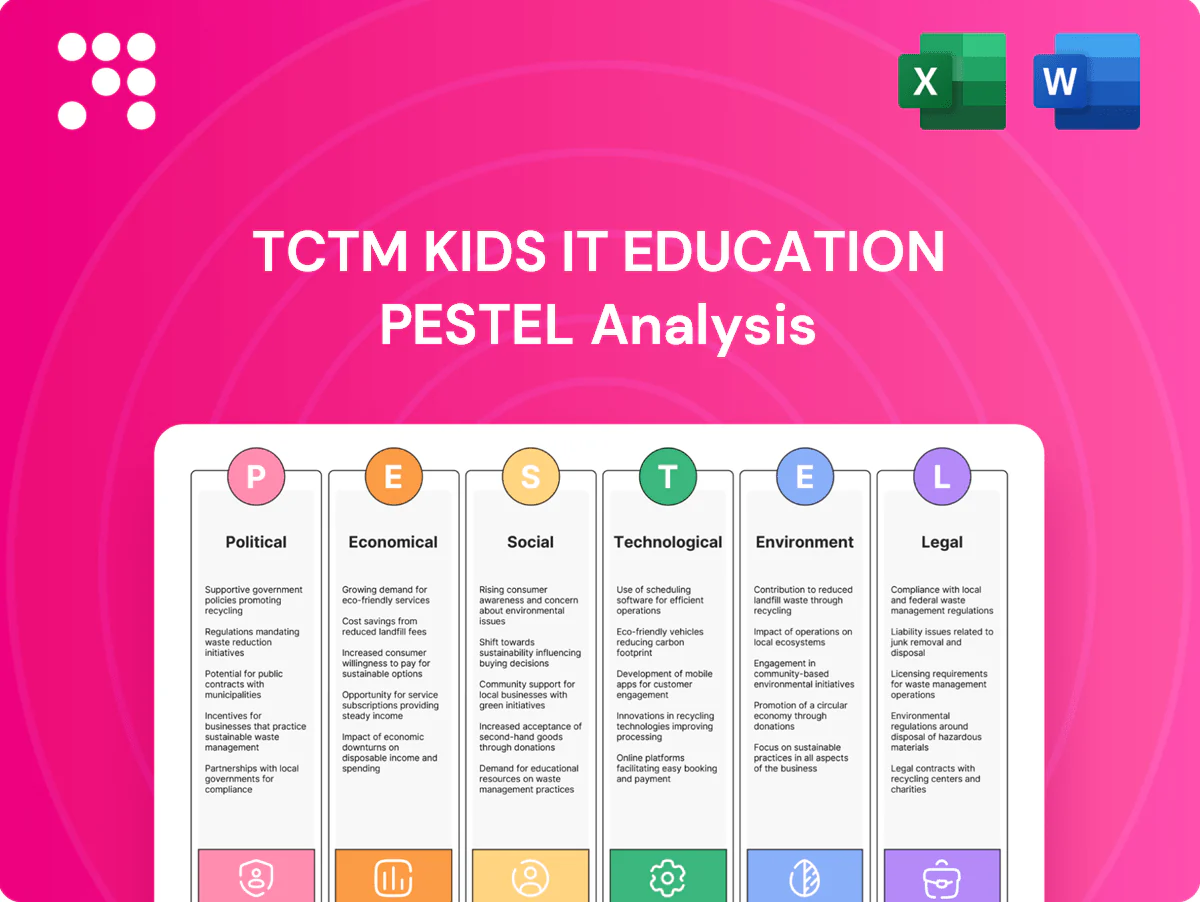

Discover how political, economic, social, technological, legal, and environmental forces are shaping TCTM Kids IT Education’s future in our concise PESTLE snapshot. Use these insights to anticipate risks, spot growth areas, and refine strategy. Purchase the full analysis for the complete, actionable breakdown and ready-to-use templates.

Political factors

Education policy priorities

National and regional emphasis on STEM/ICT drives funding, partnerships and school adoption, supporting a global EdTech market projected to reach about $404 billion by 2025. Shifts in curricula or digital literacy mandates—adopted by over 120 countries—create new demand and require content alignment. Engaging ministries and school boards helps anticipate changes, while advocacy and pilot programs can shape policy direction and procurement decisions.

Public funding and grants

Availability of tech-education grants in 2024 drove program affordability and scale, with many K-12 STEM grants targeting expansion of digital literacy; competitive grant cycles increasingly demand measurable outcomes and quarterly compliance reporting. Co-funding models with schools have been shown to lower customer-acquisition costs and boost retention by aligning incentives. Diversifying public, private and philanthropic funding reduces exposure to political budget cuts and annual funding volatility.

Political stability and procurement

Political stability shapes the viability of long-term contracts with public schools and NGOs given public procurement represents about 12% of GDP globally (World Bank). Procurement rules commonly set vendor eligibility, local-content requirements and pricing transparency that affect margins and bidding. Election cycles often pause or reprioritize spending, so building bipartisan value propositions reduces disruption to multi-year programs.

Digital inclusion agendas

Government broadband and device access drives addressable market growth as 2.9 billion people remained offline (ITU/UN ~2023); EU targets 100 Mbps for all households by 2025, expanding school connectivity. Participation in national inclusion schemes opens subsidized channels and procurement; WCAG compliance boosts eligibility for public tenders; tracking regional rollouts guides geographic expansion.

- Market expansion: 2.9B offline

- EU target: 100 Mbps by 2025

- Subsidies: access to public procurement

- Compliance: WCAG increases eligibility

Trade and foreign content rules

Restrictions on foreign edtech content, data hosting, or cross-border payments can materially affect TCTM Kids IT Education delivery; by 2024 over 60 countries had some form of data localization or transfer restriction, forcing local hosting to qualify for public tenders and comply with GDPR-like rules. Device tariffs in markets such as India and parts of Africa can add 15–30% to device costs, raising total cost of ownership for families and reducing device penetration. Structuring partnerships or joint ventures with local entities often eases regulatory entry and procurement access, and can cut compliance lead times by months.

- data-localization: over 60 countries by 2024

- device-tariffs: +15–30% TCO

- payment-fees: cross-border costs add ~1–3%+

- local-partnerships: speed procurement and compliance

EdTech: $404B market, 2.9B offline, tariffs lift costs

Strong national STEM/ICT mandates and grants (EdTech market ~$404B by 2025) drive school adoption and partnerships; procurement rules and election cycles affect multi-year contracts. Data-localization (60+ countries) and device tariffs (+15–30% TCO) raise compliance and cost barriers; broadband rollouts expand addressable market (2.9B offline 2023). Diversified public/private funding reduces political exposure.

| Metric | 2024-25 | Implication |

|---|---|---|

| EdTech market | $404B by 2025 | Scale opportunity |

| Offline population | 2.9B (2023) | Market expansion |

| Data-localization | 60+ countries | Local hosting needed |

| Device tariffs | +15–30% TCO | Higher costs |

| Public procurement | ~12% GDP | Significant channel |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact TCTM Kids IT Education, with data-backed insights, region-specific regulatory context, forward-looking scenarios and practical recommendations designed for executives, investors and entrepreneurs to identify risks, opportunities and funding-ready strategy.

Visually segmented PESTLE summary for TCTM Kids IT Education that clarifies external risks and opportunities at a glance, ready to drop into presentations or planning sessions.

Economic factors

Household disposable income

Household disposable income varies widely—OECD 2023 data show per‑capita net disposable incomes ranging roughly below US$5,000 in low‑income countries to over US$40,000 in high‑income markets—shaping pricing tiers and scholarship needs. Economic slowdowns push demand toward freemium or school‑funded models and increase uptake of bundled family plans. Offering installment payments and family bundles preserves enrollment. Monitoring regional income trends guides market selection and pricing strategy.

School and district budgets

K-12 budget cycles and US average per-pupil spending near $16,000 (2023–24) slow B2B sales velocity as purchases cluster around fiscal year and grant windows. 2–3 year multi-year contracts boost revenue predictability but demand proof of impact. Aligning to core academic standards unlocks curriculum budgets. Evidence-based ROI is essential to defend renewals during tight cycles.

Device and connectivity costs

Hardware and connectivity affordability directly shapes access and completion, with ITU reporting about 2.9 billion people offline (~36% of world) as of 2023, concentrating barriers in price-sensitive markets. Strategic OEM and ISP partnerships can subsidize devices or data bundles to lower entry costs. Offline and low-bandwidth modes extend reach where monthly data or device purchase is unaffordable. Presenting total cost of ownership to parents and schools increases enrollment and retention.

Talent and instructor wages

Instructor and facilitator wages drive unit economics: US coding instructors commonly earn roughly 25–60 USD/hour while offshore rates (Philippines, India) range ~4–12 USD/hour, influencing margins as TCTM scales. Hybrid delivery and AI-assisted tutoring can cut per-student delivery cost by industry estimates up to 30%, improving margin scalability. Investing in trainer upskilling raises instructional quality and retention, supporting lifetime value growth.

- Wage ranges: US 25–60 USD/hr; offshore 4–12 USD/hr

- Market size: global edtech ~404.8B USD (HolonIQ 2024)

- AI/hybrid cost reduction: industry estimates up to 30%

- Upskilling: boosts quality and retention

- Geographic arbitrage: supports global delivery centers

Currency and inflation exposure

FX volatility—eg DXY swings in 2024—raises import and SaaS costs and forces frequent international price updates for TCTM Kids IT Education.

Elevated inflation in 2024 pressured household budgets and school procurement, requiring flexible, subscription-based pricing and discounts.

Multi-currency billing and simple hedging cut FX risk while localized pricing preserves conversion and enrollment rates.

- FX exposure: impacts SaaS licenses

- Inflation: compresses disposable income

- Mitigation: multi-currency billing, hedges

- Strategy: local pricing to protect conversions

EdTech: $404B market, 2.9B offline, tariffs lift costs

Household disposable income diverges widely—OECD 2023 shows

| Metric | Value | Implication |

|---|---|---|

| Edtech market | USD404.8B (2024) | Large TAM |

| Per‑pupil US | ~USD16,000 (2023–24) | Procurement timing |

| Offline | 2.9B (2023) | Need low‑bandwidth |

What You See Is What You Get

TCTM Kids IT Education PESTLE Analysis

The preview shown here is the exact TCTM Kids IT Education PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are the final document with no placeholders. After payment you’ll instantly download this same, professionally structured file.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are shaping TCTM Kids IT Education’s future in our concise PESTLE snapshot. Use these insights to anticipate risks, spot growth areas, and refine strategy. Purchase the full analysis for the complete, actionable breakdown and ready-to-use templates.

Political factors

Education policy priorities

National and regional emphasis on STEM/ICT drives funding, partnerships and school adoption, supporting a global EdTech market projected to reach about $404 billion by 2025. Shifts in curricula or digital literacy mandates—adopted by over 120 countries—create new demand and require content alignment. Engaging ministries and school boards helps anticipate changes, while advocacy and pilot programs can shape policy direction and procurement decisions.

Public funding and grants

Availability of tech-education grants in 2024 drove program affordability and scale, with many K-12 STEM grants targeting expansion of digital literacy; competitive grant cycles increasingly demand measurable outcomes and quarterly compliance reporting. Co-funding models with schools have been shown to lower customer-acquisition costs and boost retention by aligning incentives. Diversifying public, private and philanthropic funding reduces exposure to political budget cuts and annual funding volatility.

Political stability and procurement

Political stability shapes the viability of long-term contracts with public schools and NGOs given public procurement represents about 12% of GDP globally (World Bank). Procurement rules commonly set vendor eligibility, local-content requirements and pricing transparency that affect margins and bidding. Election cycles often pause or reprioritize spending, so building bipartisan value propositions reduces disruption to multi-year programs.

Digital inclusion agendas

Government broadband and device access drives addressable market growth as 2.9 billion people remained offline (ITU/UN ~2023); EU targets 100 Mbps for all households by 2025, expanding school connectivity. Participation in national inclusion schemes opens subsidized channels and procurement; WCAG compliance boosts eligibility for public tenders; tracking regional rollouts guides geographic expansion.

- Market expansion: 2.9B offline

- EU target: 100 Mbps by 2025

- Subsidies: access to public procurement

- Compliance: WCAG increases eligibility

Trade and foreign content rules

Restrictions on foreign edtech content, data hosting, or cross-border payments can materially affect TCTM Kids IT Education delivery; by 2024 over 60 countries had some form of data localization or transfer restriction, forcing local hosting to qualify for public tenders and comply with GDPR-like rules. Device tariffs in markets such as India and parts of Africa can add 15–30% to device costs, raising total cost of ownership for families and reducing device penetration. Structuring partnerships or joint ventures with local entities often eases regulatory entry and procurement access, and can cut compliance lead times by months.

- data-localization: over 60 countries by 2024

- device-tariffs: +15–30% TCO

- payment-fees: cross-border costs add ~1–3%+

- local-partnerships: speed procurement and compliance

EdTech: $404B market, 2.9B offline, tariffs lift costs

Strong national STEM/ICT mandates and grants (EdTech market ~$404B by 2025) drive school adoption and partnerships; procurement rules and election cycles affect multi-year contracts. Data-localization (60+ countries) and device tariffs (+15–30% TCO) raise compliance and cost barriers; broadband rollouts expand addressable market (2.9B offline 2023). Diversified public/private funding reduces political exposure.

| Metric | 2024-25 | Implication |

|---|---|---|

| EdTech market | $404B by 2025 | Scale opportunity |

| Offline population | 2.9B (2023) | Market expansion |

| Data-localization | 60+ countries | Local hosting needed |

| Device tariffs | +15–30% TCO | Higher costs |

| Public procurement | ~12% GDP | Significant channel |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact TCTM Kids IT Education, with data-backed insights, region-specific regulatory context, forward-looking scenarios and practical recommendations designed for executives, investors and entrepreneurs to identify risks, opportunities and funding-ready strategy.

Visually segmented PESTLE summary for TCTM Kids IT Education that clarifies external risks and opportunities at a glance, ready to drop into presentations or planning sessions.

Economic factors

Household disposable income

Household disposable income varies widely—OECD 2023 data show per‑capita net disposable incomes ranging roughly below US$5,000 in low‑income countries to over US$40,000 in high‑income markets—shaping pricing tiers and scholarship needs. Economic slowdowns push demand toward freemium or school‑funded models and increase uptake of bundled family plans. Offering installment payments and family bundles preserves enrollment. Monitoring regional income trends guides market selection and pricing strategy.

School and district budgets

K-12 budget cycles and US average per-pupil spending near $16,000 (2023–24) slow B2B sales velocity as purchases cluster around fiscal year and grant windows. 2–3 year multi-year contracts boost revenue predictability but demand proof of impact. Aligning to core academic standards unlocks curriculum budgets. Evidence-based ROI is essential to defend renewals during tight cycles.

Device and connectivity costs

Hardware and connectivity affordability directly shapes access and completion, with ITU reporting about 2.9 billion people offline (~36% of world) as of 2023, concentrating barriers in price-sensitive markets. Strategic OEM and ISP partnerships can subsidize devices or data bundles to lower entry costs. Offline and low-bandwidth modes extend reach where monthly data or device purchase is unaffordable. Presenting total cost of ownership to parents and schools increases enrollment and retention.

Talent and instructor wages

Instructor and facilitator wages drive unit economics: US coding instructors commonly earn roughly 25–60 USD/hour while offshore rates (Philippines, India) range ~4–12 USD/hour, influencing margins as TCTM scales. Hybrid delivery and AI-assisted tutoring can cut per-student delivery cost by industry estimates up to 30%, improving margin scalability. Investing in trainer upskilling raises instructional quality and retention, supporting lifetime value growth.

- Wage ranges: US 25–60 USD/hr; offshore 4–12 USD/hr

- Market size: global edtech ~404.8B USD (HolonIQ 2024)

- AI/hybrid cost reduction: industry estimates up to 30%

- Upskilling: boosts quality and retention

- Geographic arbitrage: supports global delivery centers

Currency and inflation exposure

FX volatility—eg DXY swings in 2024—raises import and SaaS costs and forces frequent international price updates for TCTM Kids IT Education.

Elevated inflation in 2024 pressured household budgets and school procurement, requiring flexible, subscription-based pricing and discounts.

Multi-currency billing and simple hedging cut FX risk while localized pricing preserves conversion and enrollment rates.

- FX exposure: impacts SaaS licenses

- Inflation: compresses disposable income

- Mitigation: multi-currency billing, hedges

- Strategy: local pricing to protect conversions

EdTech: $404B market, 2.9B offline, tariffs lift costs

Household disposable income diverges widely—OECD 2023 shows

| Metric | Value | Implication |

|---|---|---|

| Edtech market | USD404.8B (2024) | Large TAM |

| Per‑pupil US | ~USD16,000 (2023–24) | Procurement timing |

| Offline | 2.9B (2023) | Need low‑bandwidth |

What You See Is What You Get

TCTM Kids IT Education PESTLE Analysis

The preview shown here is the exact TCTM Kids IT Education PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are the final document with no placeholders. After payment you’ll instantly download this same, professionally structured file.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are shaping TCTM Kids IT Education’s future in our concise PESTLE snapshot. Use these insights to anticipate risks, spot growth areas, and refine strategy. Purchase the full analysis for the complete, actionable breakdown and ready-to-use templates.

Political factors

Education policy priorities

National and regional emphasis on STEM/ICT drives funding, partnerships and school adoption, supporting a global EdTech market projected to reach about $404 billion by 2025. Shifts in curricula or digital literacy mandates—adopted by over 120 countries—create new demand and require content alignment. Engaging ministries and school boards helps anticipate changes, while advocacy and pilot programs can shape policy direction and procurement decisions.

Public funding and grants

Availability of tech-education grants in 2024 drove program affordability and scale, with many K-12 STEM grants targeting expansion of digital literacy; competitive grant cycles increasingly demand measurable outcomes and quarterly compliance reporting. Co-funding models with schools have been shown to lower customer-acquisition costs and boost retention by aligning incentives. Diversifying public, private and philanthropic funding reduces exposure to political budget cuts and annual funding volatility.

Political stability and procurement

Political stability shapes the viability of long-term contracts with public schools and NGOs given public procurement represents about 12% of GDP globally (World Bank). Procurement rules commonly set vendor eligibility, local-content requirements and pricing transparency that affect margins and bidding. Election cycles often pause or reprioritize spending, so building bipartisan value propositions reduces disruption to multi-year programs.

Digital inclusion agendas

Government broadband and device access drives addressable market growth as 2.9 billion people remained offline (ITU/UN ~2023); EU targets 100 Mbps for all households by 2025, expanding school connectivity. Participation in national inclusion schemes opens subsidized channels and procurement; WCAG compliance boosts eligibility for public tenders; tracking regional rollouts guides geographic expansion.

- Market expansion: 2.9B offline

- EU target: 100 Mbps by 2025

- Subsidies: access to public procurement

- Compliance: WCAG increases eligibility

Trade and foreign content rules

Restrictions on foreign edtech content, data hosting, or cross-border payments can materially affect TCTM Kids IT Education delivery; by 2024 over 60 countries had some form of data localization or transfer restriction, forcing local hosting to qualify for public tenders and comply with GDPR-like rules. Device tariffs in markets such as India and parts of Africa can add 15–30% to device costs, raising total cost of ownership for families and reducing device penetration. Structuring partnerships or joint ventures with local entities often eases regulatory entry and procurement access, and can cut compliance lead times by months.

- data-localization: over 60 countries by 2024

- device-tariffs: +15–30% TCO

- payment-fees: cross-border costs add ~1–3%+

- local-partnerships: speed procurement and compliance

EdTech: $404B market, 2.9B offline, tariffs lift costs

Strong national STEM/ICT mandates and grants (EdTech market ~$404B by 2025) drive school adoption and partnerships; procurement rules and election cycles affect multi-year contracts. Data-localization (60+ countries) and device tariffs (+15–30% TCO) raise compliance and cost barriers; broadband rollouts expand addressable market (2.9B offline 2023). Diversified public/private funding reduces political exposure.

| Metric | 2024-25 | Implication |

|---|---|---|

| EdTech market | $404B by 2025 | Scale opportunity |

| Offline population | 2.9B (2023) | Market expansion |

| Data-localization | 60+ countries | Local hosting needed |

| Device tariffs | +15–30% TCO | Higher costs |

| Public procurement | ~12% GDP | Significant channel |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact TCTM Kids IT Education, with data-backed insights, region-specific regulatory context, forward-looking scenarios and practical recommendations designed for executives, investors and entrepreneurs to identify risks, opportunities and funding-ready strategy.

Visually segmented PESTLE summary for TCTM Kids IT Education that clarifies external risks and opportunities at a glance, ready to drop into presentations or planning sessions.

Economic factors

Household disposable income

Household disposable income varies widely—OECD 2023 data show per‑capita net disposable incomes ranging roughly below US$5,000 in low‑income countries to over US$40,000 in high‑income markets—shaping pricing tiers and scholarship needs. Economic slowdowns push demand toward freemium or school‑funded models and increase uptake of bundled family plans. Offering installment payments and family bundles preserves enrollment. Monitoring regional income trends guides market selection and pricing strategy.

School and district budgets

K-12 budget cycles and US average per-pupil spending near $16,000 (2023–24) slow B2B sales velocity as purchases cluster around fiscal year and grant windows. 2–3 year multi-year contracts boost revenue predictability but demand proof of impact. Aligning to core academic standards unlocks curriculum budgets. Evidence-based ROI is essential to defend renewals during tight cycles.

Device and connectivity costs

Hardware and connectivity affordability directly shapes access and completion, with ITU reporting about 2.9 billion people offline (~36% of world) as of 2023, concentrating barriers in price-sensitive markets. Strategic OEM and ISP partnerships can subsidize devices or data bundles to lower entry costs. Offline and low-bandwidth modes extend reach where monthly data or device purchase is unaffordable. Presenting total cost of ownership to parents and schools increases enrollment and retention.

Talent and instructor wages

Instructor and facilitator wages drive unit economics: US coding instructors commonly earn roughly 25–60 USD/hour while offshore rates (Philippines, India) range ~4–12 USD/hour, influencing margins as TCTM scales. Hybrid delivery and AI-assisted tutoring can cut per-student delivery cost by industry estimates up to 30%, improving margin scalability. Investing in trainer upskilling raises instructional quality and retention, supporting lifetime value growth.

- Wage ranges: US 25–60 USD/hr; offshore 4–12 USD/hr

- Market size: global edtech ~404.8B USD (HolonIQ 2024)

- AI/hybrid cost reduction: industry estimates up to 30%

- Upskilling: boosts quality and retention

- Geographic arbitrage: supports global delivery centers

Currency and inflation exposure

FX volatility—eg DXY swings in 2024—raises import and SaaS costs and forces frequent international price updates for TCTM Kids IT Education.

Elevated inflation in 2024 pressured household budgets and school procurement, requiring flexible, subscription-based pricing and discounts.

Multi-currency billing and simple hedging cut FX risk while localized pricing preserves conversion and enrollment rates.

- FX exposure: impacts SaaS licenses

- Inflation: compresses disposable income

- Mitigation: multi-currency billing, hedges

- Strategy: local pricing to protect conversions

EdTech: $404B market, 2.9B offline, tariffs lift costs

Household disposable income diverges widely—OECD 2023 shows

| Metric | Value | Implication |

|---|---|---|

| Edtech market | USD404.8B (2024) | Large TAM |

| Per‑pupil US | ~USD16,000 (2023–24) | Procurement timing |

| Offline | 2.9B (2023) | Need low‑bandwidth |

What You See Is What You Get

TCTM Kids IT Education PESTLE Analysis

The preview shown here is the exact TCTM Kids IT Education PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are the final document with no placeholders. After payment you’ll instantly download this same, professionally structured file.