Transcontinental SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Discover how Transcontinental’s print-to-packaging scale, digital transition efforts, and distribution network shape competitive advantage and risk exposure; our 3–5 sentence snapshot highlights key points, but the full SWOT delivers research-backed insights, editable Word and Excel files, and strategic takeaways—purchase the complete report to plan, pitch, or invest with confidence.

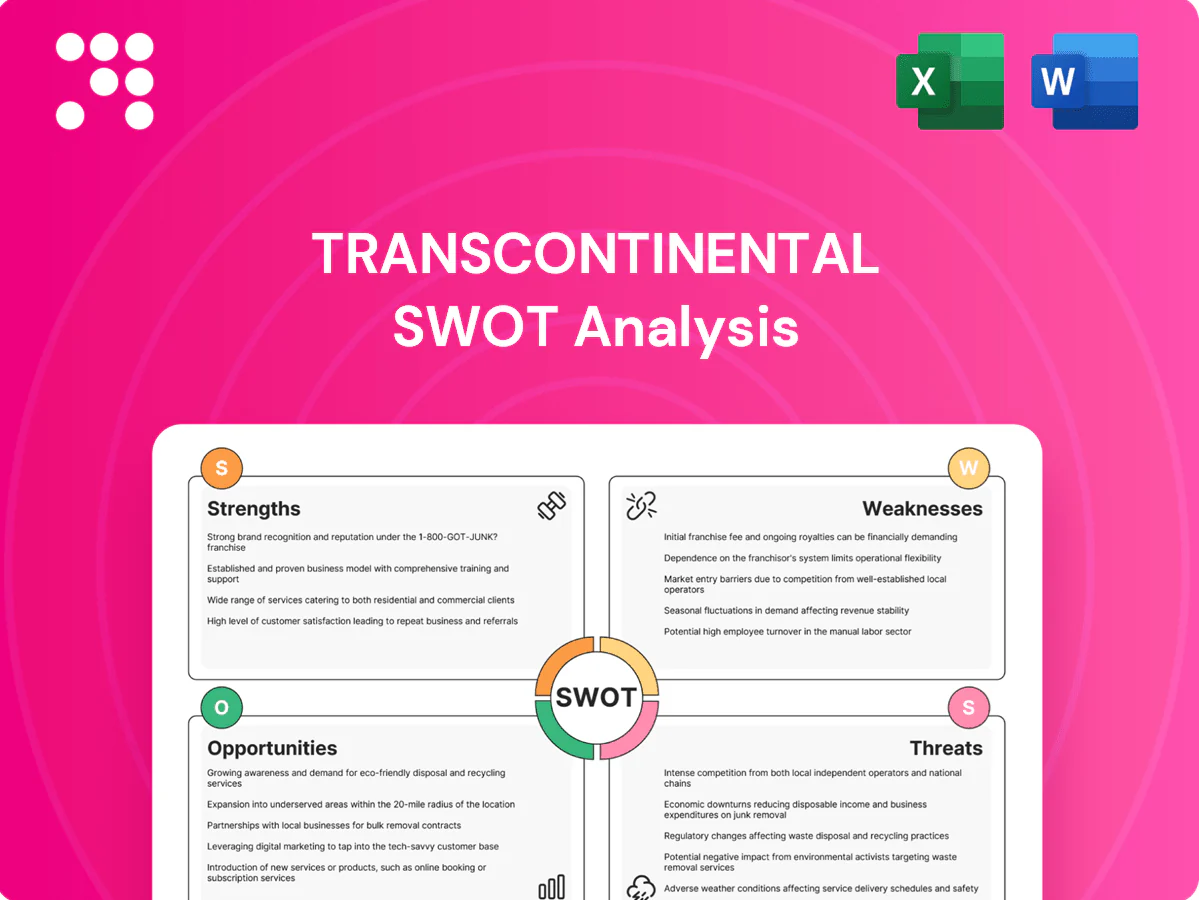

Strengths

Leading flexible packaging scale

As one of North America’s largest flexible packaging players, TC Transcontinental leverages a network of over 50 manufacturing sites and more than 8,000 packaging employees to drive scale in procurement, manufacturing and distribution. This scale supports cost leadership and reliable service for blue‑chip CPG clients, enables faster commercialization of new materials and creates meaningful barriers to entry in high‑spec applications.

Diversified multi-segment portfolio

Transcontinental’s mix of packaging, printing and educational publishing delivered resilience in 2024, with group revenue of about CAD 3.6 billion and packaging comprising the majority of sales. Legacy printing and publishing continued to generate steady operating cash flow, funding capital allocation to high-growth flexible packaging. Multi-segment client relationships boost cross-selling and reduce single-market shock risk.

Deep customer relationships

Long-term contracts with food, beverage and industrial clients provide anchored volumes and planning visibility, supporting Transcontinental’s recurring packaging operations as of 2024. Co-development of bespoke packaging solutions embeds TC into customers’ workflows, raising switching costs and retention. Broad service scope from premedia through distribution increases customer stickiness and cross-selling opportunities.

Innovation in sustainable materials

Investments in recyclable, PCR and mono-material structures position Transcontinental to meet tightening regulator and retailer mandates, reducing conversion risk and shortening compliance cycles. Technical labs and iterative design processes accelerate time-to-market for sustainable SKUs, enabling faster commercialisation and higher win rates with major CPGs. Strong sustainability credentials allow premium pricing and strengthen bids with ESG-oriented customers, improving margin resilience.

Canadian market leadership

As Canada’s largest printer and leading francophone educational publisher, Transcontinental leverages strong local brand equity and a national bilingual footprint, supporting broad market coverage and recurring contracts; reported FY2024 revenue ~CAD 2.5B and ~11,000 employees reinforce scale. Government and education ties underpin steady demand and help win regulated public tenders.

- National reach, bilingual services

- FY2024 revenue ~CAD 2.5B; ~11,000 employees

- Strong public/education contracts

North American flexible-packaging leader: scale, cost advantage, sustainable mono-material edge

TC Transcontinental is a top North American flexible‑packaging player with >50 sites and >8,000 packaging employees, driving scale, cost leadership and barriers in high‑spec segments. FY2024 group revenue ~CAD 3.6B with packaging as majority; printing/publishing ~CAD 2.5B supports cash flow for packaging growth. Long‑term CPG contracts and sustainable mono‑material/PCR investments raise switching costs and pricing power.

| Metric | Value (FY2024) |

|---|---|

| Group revenue | ~CAD 3.6B |

| Printing/publishing revenue | ~CAD 2.5B |

| Packaging sites | >50 |

| Packaging employees | >8,000 |

| Total employees | ~11,000 |

What is included in the product

Provides a concise SWOT analysis of Transcontinental, outlining its operational strengths and weaknesses, market opportunities such as packaging growth and digital diversification, and threats from industry consolidation and digital disruption.

Provides a focused SWOT matrix for Transcontinental to quickly surface strategic risks and opportunities across print, packaging and media, streamlining executive decisions and cross‑unit alignment.

Weaknesses

Secular print decline

Commercial printing at Transcontinental faces ongoing volume erosion as clients shift to digital media, compressing plant utilization and weakening pricing power. Resilient near-term cash flow from long-term contracts and packaging diversification cushions revenue loss but is likely to weaken if secular trends persist. The company remains exposed to periodic asset write-downs as press capacity becomes redundant. This structural decline constrains long-term margin recovery and capital allocation flexibility.

Input cost volatility

Resin, films, inks and energy cost volatility remains a key weakness for Transcontinental, with market swings in 2024 creating timing mismatches that compress margins when customer pass-through clauses lag. Hedging programs mitigate but are imperfect, leaving short-term exposure that can dent quarter-to-quarter gross margins. Delays in contractual pass-throughs force temporary margin erosion and working-capital strain.

Capital intensity

Packaging operations require continuous investment in presses, extrusion and converting lines, creating a high capex and maintenance burden that strains free cash flow in industry downcycles. Payback on these assets is reliant on stable volumes and long production runs, making returns sensitive to demand swings. During downturns balance sheet flexibility can tighten as working capital and capex needs compete with debt service and shareholder returns.

Customer concentration

Customer concentration at Transcontinental is a weakness: large CPG accounts account for an outsized share of printing and packaging volumes, intensifying renegotiation leverage and pricing pressure; loss of a major program would materially reduce capacity utilization and margins, and apparent diversification across CPG segments can still mask top-customer dependency.

- High revenue share from major CPG clients

- Renegotiation and pricing pressure risk

- Material capacity/utilization impact if a key program lost

- CPG diversification may obscure single-customer concentration

Exposure to regulatory scrutiny

Plastics exposure: tightening regulations and expanding EPR schemes—Canada's federal single-use plastics prohibition phases in through 2025—raise compliance costs and operational complexity for Transcontinental. Negative public perception pressures retailers' specs, while legacy plastic products face redesign needs or obsolescence risk.

- Regulatory timing: Canada prohibition phasing to 2025

- Cost/complexity: higher compliance burden

- Reputational pressure: retailer specification risk

- Product risk: legacy redesign/obsolescence

Packaging 65% of sales; capex and client concentration squeeze margins

Commercial printing secular decline compresses volumes and pricing power; 2024 revenue ~CAD 3.0B with packaging now ~65% of sales, limiting print recovery. Input-cost volatility and lagging pass-throughs dent margins; 2024 capex ~CAD 140M strains FCF. Customer concentration is high: top 5 clients ~28% of revenue, raising renegotiation and utilization risk.

| Metric | 2024 |

|---|---|

| Total revenue | ~CAD 3.0B |

| Packaging share | ~65% |

| Capex | ~CAD 140M |

| Top‑5 customer share | ~28% |

Preview the Actual Deliverable

Transcontinental SWOT Analysis

This is the actual Transcontinental SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live preview of the real file; the complete document becomes available after checkout.

Go Beyond the Preview—Access the Full Strategic Report

Discover how Transcontinental’s print-to-packaging scale, digital transition efforts, and distribution network shape competitive advantage and risk exposure; our 3–5 sentence snapshot highlights key points, but the full SWOT delivers research-backed insights, editable Word and Excel files, and strategic takeaways—purchase the complete report to plan, pitch, or invest with confidence.

Strengths

Leading flexible packaging scale

As one of North America’s largest flexible packaging players, TC Transcontinental leverages a network of over 50 manufacturing sites and more than 8,000 packaging employees to drive scale in procurement, manufacturing and distribution. This scale supports cost leadership and reliable service for blue‑chip CPG clients, enables faster commercialization of new materials and creates meaningful barriers to entry in high‑spec applications.

Diversified multi-segment portfolio

Transcontinental’s mix of packaging, printing and educational publishing delivered resilience in 2024, with group revenue of about CAD 3.6 billion and packaging comprising the majority of sales. Legacy printing and publishing continued to generate steady operating cash flow, funding capital allocation to high-growth flexible packaging. Multi-segment client relationships boost cross-selling and reduce single-market shock risk.

Deep customer relationships

Long-term contracts with food, beverage and industrial clients provide anchored volumes and planning visibility, supporting Transcontinental’s recurring packaging operations as of 2024. Co-development of bespoke packaging solutions embeds TC into customers’ workflows, raising switching costs and retention. Broad service scope from premedia through distribution increases customer stickiness and cross-selling opportunities.

Innovation in sustainable materials

Investments in recyclable, PCR and mono-material structures position Transcontinental to meet tightening regulator and retailer mandates, reducing conversion risk and shortening compliance cycles. Technical labs and iterative design processes accelerate time-to-market for sustainable SKUs, enabling faster commercialisation and higher win rates with major CPGs. Strong sustainability credentials allow premium pricing and strengthen bids with ESG-oriented customers, improving margin resilience.

Canadian market leadership

As Canada’s largest printer and leading francophone educational publisher, Transcontinental leverages strong local brand equity and a national bilingual footprint, supporting broad market coverage and recurring contracts; reported FY2024 revenue ~CAD 2.5B and ~11,000 employees reinforce scale. Government and education ties underpin steady demand and help win regulated public tenders.

- National reach, bilingual services

- FY2024 revenue ~CAD 2.5B; ~11,000 employees

- Strong public/education contracts

North American flexible-packaging leader: scale, cost advantage, sustainable mono-material edge

TC Transcontinental is a top North American flexible‑packaging player with >50 sites and >8,000 packaging employees, driving scale, cost leadership and barriers in high‑spec segments. FY2024 group revenue ~CAD 3.6B with packaging as majority; printing/publishing ~CAD 2.5B supports cash flow for packaging growth. Long‑term CPG contracts and sustainable mono‑material/PCR investments raise switching costs and pricing power.

| Metric | Value (FY2024) |

|---|---|

| Group revenue | ~CAD 3.6B |

| Printing/publishing revenue | ~CAD 2.5B |

| Packaging sites | >50 |

| Packaging employees | >8,000 |

| Total employees | ~11,000 |

What is included in the product

Provides a concise SWOT analysis of Transcontinental, outlining its operational strengths and weaknesses, market opportunities such as packaging growth and digital diversification, and threats from industry consolidation and digital disruption.

Provides a focused SWOT matrix for Transcontinental to quickly surface strategic risks and opportunities across print, packaging and media, streamlining executive decisions and cross‑unit alignment.

Weaknesses

Secular print decline

Commercial printing at Transcontinental faces ongoing volume erosion as clients shift to digital media, compressing plant utilization and weakening pricing power. Resilient near-term cash flow from long-term contracts and packaging diversification cushions revenue loss but is likely to weaken if secular trends persist. The company remains exposed to periodic asset write-downs as press capacity becomes redundant. This structural decline constrains long-term margin recovery and capital allocation flexibility.

Input cost volatility

Resin, films, inks and energy cost volatility remains a key weakness for Transcontinental, with market swings in 2024 creating timing mismatches that compress margins when customer pass-through clauses lag. Hedging programs mitigate but are imperfect, leaving short-term exposure that can dent quarter-to-quarter gross margins. Delays in contractual pass-throughs force temporary margin erosion and working-capital strain.

Capital intensity

Packaging operations require continuous investment in presses, extrusion and converting lines, creating a high capex and maintenance burden that strains free cash flow in industry downcycles. Payback on these assets is reliant on stable volumes and long production runs, making returns sensitive to demand swings. During downturns balance sheet flexibility can tighten as working capital and capex needs compete with debt service and shareholder returns.

Customer concentration

Customer concentration at Transcontinental is a weakness: large CPG accounts account for an outsized share of printing and packaging volumes, intensifying renegotiation leverage and pricing pressure; loss of a major program would materially reduce capacity utilization and margins, and apparent diversification across CPG segments can still mask top-customer dependency.

- High revenue share from major CPG clients

- Renegotiation and pricing pressure risk

- Material capacity/utilization impact if a key program lost

- CPG diversification may obscure single-customer concentration

Exposure to regulatory scrutiny

Plastics exposure: tightening regulations and expanding EPR schemes—Canada's federal single-use plastics prohibition phases in through 2025—raise compliance costs and operational complexity for Transcontinental. Negative public perception pressures retailers' specs, while legacy plastic products face redesign needs or obsolescence risk.

- Regulatory timing: Canada prohibition phasing to 2025

- Cost/complexity: higher compliance burden

- Reputational pressure: retailer specification risk

- Product risk: legacy redesign/obsolescence

Packaging 65% of sales; capex and client concentration squeeze margins

Commercial printing secular decline compresses volumes and pricing power; 2024 revenue ~CAD 3.0B with packaging now ~65% of sales, limiting print recovery. Input-cost volatility and lagging pass-throughs dent margins; 2024 capex ~CAD 140M strains FCF. Customer concentration is high: top 5 clients ~28% of revenue, raising renegotiation and utilization risk.

| Metric | 2024 |

|---|---|

| Total revenue | ~CAD 3.0B |

| Packaging share | ~65% |

| Capex | ~CAD 140M |

| Top‑5 customer share | ~28% |

Preview the Actual Deliverable

Transcontinental SWOT Analysis

This is the actual Transcontinental SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live preview of the real file; the complete document becomes available after checkout.

Description

Go Beyond the Preview—Access the Full Strategic Report

Discover how Transcontinental’s print-to-packaging scale, digital transition efforts, and distribution network shape competitive advantage and risk exposure; our 3–5 sentence snapshot highlights key points, but the full SWOT delivers research-backed insights, editable Word and Excel files, and strategic takeaways—purchase the complete report to plan, pitch, or invest with confidence.

Strengths

Leading flexible packaging scale

As one of North America’s largest flexible packaging players, TC Transcontinental leverages a network of over 50 manufacturing sites and more than 8,000 packaging employees to drive scale in procurement, manufacturing and distribution. This scale supports cost leadership and reliable service for blue‑chip CPG clients, enables faster commercialization of new materials and creates meaningful barriers to entry in high‑spec applications.

Diversified multi-segment portfolio

Transcontinental’s mix of packaging, printing and educational publishing delivered resilience in 2024, with group revenue of about CAD 3.6 billion and packaging comprising the majority of sales. Legacy printing and publishing continued to generate steady operating cash flow, funding capital allocation to high-growth flexible packaging. Multi-segment client relationships boost cross-selling and reduce single-market shock risk.

Deep customer relationships

Long-term contracts with food, beverage and industrial clients provide anchored volumes and planning visibility, supporting Transcontinental’s recurring packaging operations as of 2024. Co-development of bespoke packaging solutions embeds TC into customers’ workflows, raising switching costs and retention. Broad service scope from premedia through distribution increases customer stickiness and cross-selling opportunities.

Innovation in sustainable materials

Investments in recyclable, PCR and mono-material structures position Transcontinental to meet tightening regulator and retailer mandates, reducing conversion risk and shortening compliance cycles. Technical labs and iterative design processes accelerate time-to-market for sustainable SKUs, enabling faster commercialisation and higher win rates with major CPGs. Strong sustainability credentials allow premium pricing and strengthen bids with ESG-oriented customers, improving margin resilience.

Canadian market leadership

As Canada’s largest printer and leading francophone educational publisher, Transcontinental leverages strong local brand equity and a national bilingual footprint, supporting broad market coverage and recurring contracts; reported FY2024 revenue ~CAD 2.5B and ~11,000 employees reinforce scale. Government and education ties underpin steady demand and help win regulated public tenders.

- National reach, bilingual services

- FY2024 revenue ~CAD 2.5B; ~11,000 employees

- Strong public/education contracts

North American flexible-packaging leader: scale, cost advantage, sustainable mono-material edge

TC Transcontinental is a top North American flexible‑packaging player with >50 sites and >8,000 packaging employees, driving scale, cost leadership and barriers in high‑spec segments. FY2024 group revenue ~CAD 3.6B with packaging as majority; printing/publishing ~CAD 2.5B supports cash flow for packaging growth. Long‑term CPG contracts and sustainable mono‑material/PCR investments raise switching costs and pricing power.

| Metric | Value (FY2024) |

|---|---|

| Group revenue | ~CAD 3.6B |

| Printing/publishing revenue | ~CAD 2.5B |

| Packaging sites | >50 |

| Packaging employees | >8,000 |

| Total employees | ~11,000 |

What is included in the product

Provides a concise SWOT analysis of Transcontinental, outlining its operational strengths and weaknesses, market opportunities such as packaging growth and digital diversification, and threats from industry consolidation and digital disruption.

Provides a focused SWOT matrix for Transcontinental to quickly surface strategic risks and opportunities across print, packaging and media, streamlining executive decisions and cross‑unit alignment.

Weaknesses

Secular print decline

Commercial printing at Transcontinental faces ongoing volume erosion as clients shift to digital media, compressing plant utilization and weakening pricing power. Resilient near-term cash flow from long-term contracts and packaging diversification cushions revenue loss but is likely to weaken if secular trends persist. The company remains exposed to periodic asset write-downs as press capacity becomes redundant. This structural decline constrains long-term margin recovery and capital allocation flexibility.

Input cost volatility

Resin, films, inks and energy cost volatility remains a key weakness for Transcontinental, with market swings in 2024 creating timing mismatches that compress margins when customer pass-through clauses lag. Hedging programs mitigate but are imperfect, leaving short-term exposure that can dent quarter-to-quarter gross margins. Delays in contractual pass-throughs force temporary margin erosion and working-capital strain.

Capital intensity

Packaging operations require continuous investment in presses, extrusion and converting lines, creating a high capex and maintenance burden that strains free cash flow in industry downcycles. Payback on these assets is reliant on stable volumes and long production runs, making returns sensitive to demand swings. During downturns balance sheet flexibility can tighten as working capital and capex needs compete with debt service and shareholder returns.

Customer concentration

Customer concentration at Transcontinental is a weakness: large CPG accounts account for an outsized share of printing and packaging volumes, intensifying renegotiation leverage and pricing pressure; loss of a major program would materially reduce capacity utilization and margins, and apparent diversification across CPG segments can still mask top-customer dependency.

- High revenue share from major CPG clients

- Renegotiation and pricing pressure risk

- Material capacity/utilization impact if a key program lost

- CPG diversification may obscure single-customer concentration

Exposure to regulatory scrutiny

Plastics exposure: tightening regulations and expanding EPR schemes—Canada's federal single-use plastics prohibition phases in through 2025—raise compliance costs and operational complexity for Transcontinental. Negative public perception pressures retailers' specs, while legacy plastic products face redesign needs or obsolescence risk.

- Regulatory timing: Canada prohibition phasing to 2025

- Cost/complexity: higher compliance burden

- Reputational pressure: retailer specification risk

- Product risk: legacy redesign/obsolescence

Packaging 65% of sales; capex and client concentration squeeze margins

Commercial printing secular decline compresses volumes and pricing power; 2024 revenue ~CAD 3.0B with packaging now ~65% of sales, limiting print recovery. Input-cost volatility and lagging pass-throughs dent margins; 2024 capex ~CAD 140M strains FCF. Customer concentration is high: top 5 clients ~28% of revenue, raising renegotiation and utilization risk.

| Metric | 2024 |

|---|---|

| Total revenue | ~CAD 3.0B |

| Packaging share | ~65% |

| Capex | ~CAD 140M |

| Top‑5 customer share | ~28% |

Preview the Actual Deliverable

Transcontinental SWOT Analysis

This is the actual Transcontinental SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live preview of the real file; the complete document becomes available after checkout.