TDK PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic foresight with our targeted PESTLE Analysis of TDK, revealing how political, economic, and technological shifts reshape its outlook. This concise, research-backed report highlights risks and growth levers for investors and strategists. Purchase the full version to access actionable, exportable insights and stay ahead of market moves.

Political factors

Trade tensions & export controls

US–China technology frictions and expanded export controls (notably US measures in 2022–23 alongside the CHIPS Act $52 billion semiconductor push) constrain advanced components, tooling and cross-border design collaboration; Asia accounts for over 70% of global semiconductor manufacturing, raising lead-time and routing risk. TDK must segment products/customers, tighten licensing, redesign supply routes, and accept higher compliance costs. Strategic dual-sourcing and regionalization mitigate shocks and production-footprint shifts.

Industrial policy & subsidies

CHIPS and Science Act provides $52.7 billion in US incentives, the EU Chips Act targets up to €43 billion to boost capacity, and Japan has rolled multi-billion-yen subsidy programs; these grants lower capex for TDK’s advanced materials, magnetics and power-electronics projects but impose local-job and tech-sharing conditions, while shifting policy cycles create timing and approval risks for plant and R&D investments.

Geopolitical supply-chain exposure

Concentration risks around East Asia, notably Taiwan where TSMC held ~53% foundry share in 2024 and Taiwan supplied >60% of leading-edge wafer capacity, create continuity threats for TDK’s wafers, substrates and passive components. Political instability or conflict could disrupt inputs with wafer lead times already 20–30 weeks in 2024. TDK needs buffer inventory, alternate nodes, diversified logistics lanes and expanded insurance and geopolitical monitoring as core planning inputs.

Localization & procurement mandates

Governments and regulations (eg US IRA, EU Battery Regulation) increasingly mandate local content in automotive and energy projects, driving OEMs to pressure suppliers to align regional footprints; global EV sales reached about 14 million in 2023 (IEA), intensifying localization. TDK may expand local production and engineering to win programs, raising fixed costs but improving resilience and customer proximity.

- Local mandates: regulatory push (US, EU, India)

- OEM pressure: regional sourcing alignment

- TDK action: expand localized production/engineering

- Impact: higher fixed costs; better resilience and proximity

Public investment in electrification

Public electrification spending, including the US Bipartisan Infrastructure Law $7.5 billion EV charger fund and the EU Recovery Facility (~€806.9 billion overall), lifts demand for power inductors, capacitors and sensors as EV and grid modernization pipelines (US target 500,000 chargers by 2030) give multiyear visibility in automotive and industrial segments; TDK can tailor portfolios to qualify for funded projects while policy reversals remain a planning risk.

- EV incentives → higher component demand

- Policy pipelines → multiyear revenue visibility

- Aligning SKUs enables funded-project eligibility

- Reversal risk → scenario planning required

Geopolitical export controls, subsidy race and Taiwan bottlenecks drive EV supply regionalization

Geopolitical tech tensions and export controls (US measures 2022–24; CHIPS $52.7B) raise compliance and redesign costs for TDK. Subsidies (EU ~€43B, Japan multibillion) lower capex but require local jobs/tech sharing. Taiwan concentration (TSMC ~53% foundry share 2024) and 20–30 week wafer lead times heighten continuity risk. EV policy-driven demand (global EVs ~14M in 2023; US 500k chargers target by 2030) forces regionalization.

| Metric | Value |

|---|---|

| CHIPS/US | $52.7B |

| EU Chips | ~€43B |

| TSMC foundry | ~53% (2024) |

| Global EVs | ~14M (2023) |

What is included in the product

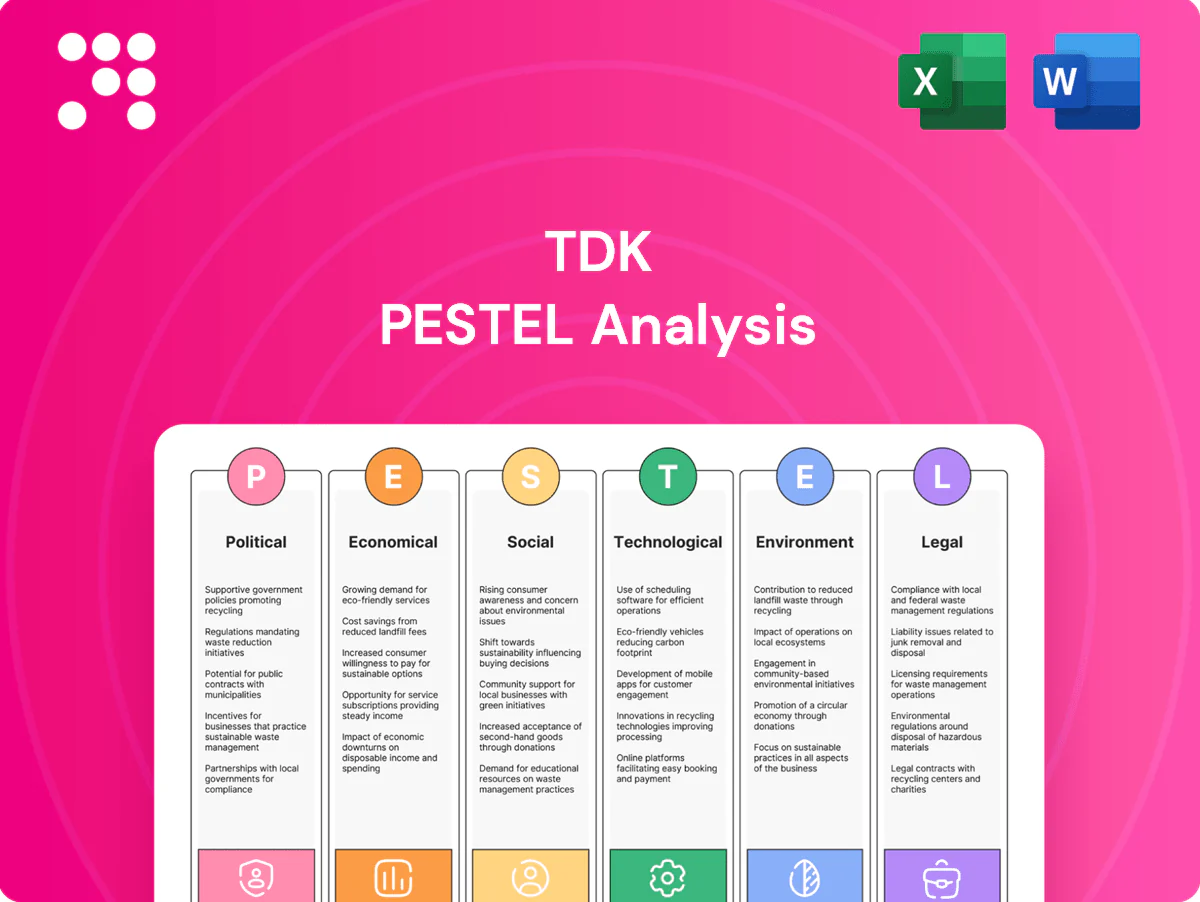

Explores how macro-environmental factors uniquely affect TDK across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry trends to reveal threats and opportunities. Designed for executives, consultants, and investors, the analysis offers forward-looking insights and ready-to-use formatting for strategic planning, pitches, and reports.

A compact, category-segmented PESTLE summary of TDK that simplifies external risk assessment and market-position discussions, easily dropped into presentations or shared across teams for quick alignment.

Economic factors

Electronics demand cyclicality

End-market cyclicality is pronounced: global smartphone shipments fell about 8% in 2023 (IDC), while automotive electronics—with the automotive semiconductor market up roughly 10% in 2023 (SIA)—and industrial demand remained steadier. Inventory corrections historically compress orders and pricing, pressuring near-term margins. TDK offsets volatility by tilting its portfolio toward automotive/industrial (roughly two-thirds components exposure) and using flexible manufacturing to shift mix rapidly.

FX volatility (JPY, USD, EUR, CNY)

TDK's revenue mix is highly international while manufacturing and many operating costs remain yen- and local-currency driven, so USD/JPY, EUR/JPY and CNY/JPY swings materially affect margins and competitiveness; yen weakness around 150–160 per USD in 2023–2024 widened reported sales but compressed local-cost margins.

Active hedging programs and shifting production to regional cost bases (Asia, Europe, Americas) have reduced FX-driven earnings volatility, with TDK citing routine use of forwards and natural hedges in FY2024 reporting.

Long-term OEM contracts rely on pricing clauses and pass-through mechanisms; absence of timely indexation can force margin erosion during rapid moves in USD, EUR or CNY versus JPY, making contract terms pivotal for 2024–25 profitability.

Input costs & materials availability

Rare earths, copper, nickel and specialty ceramics now drive TDKs BOM; mid-2025 prices were about copper USD 9,000/t, nickel USD 22,000–25,000/t and NdPr oxide ~USD 70/kg, so spikes and supply constraints can compress margins and delay deliveries. Long-term offtakes and closed-loop recycling reduce exposure, while design-to-cost and value engineering help preserve ASPs.

Interest rates & capex cycles

Higher global policy rates, with the US federal funds target at 5.25–5.50% (July 2025), raise financing costs and temper consumer electronics demand, while automotive, factory automation and energy capex remain resilient but mainly project-driven. TDK times capacity expansions to utilization and funded demand, and its strong balance sheet supports selective counter-cyclical investment.

- Fed funds 5.25–5.50% (Jul 2025)

- Consumer electronics demand softer

- Automotive/factory/energy capex project-driven

- TDK expansion tied to utilization/funded demand

- Strong balance sheet enables counter-cyclical spend

OEM consolidation & pricing power

Larger OEMs concentrated buying power—top five smartphone OEMs accounted for about 65% of global shipments in 2024 (IDC)—drive aggressive cost-downs and enforce dual sourcing, pressuring suppliers on price and volume stability. TDK defends pricing with scale and differentiated performance specs, while platform wins and multi-year agreements (TDK FY2024 revenue ¥1.62 trillion) help stabilize volumes. Services and integrated modules raise switching costs, strengthening pricing resilience.

- OEM concentration ~65% (top 5, IDC 2024)

- Dual sourcing common procurement term

- TDK FY2024 revenue ¥1.62 trillion

- Platform wins + multi-year contracts = volume stability

- Services/modules = higher switching costs

Geopolitical export controls, subsidy race and Taiwan bottlenecks drive EV supply regionalization

Smartphone shipments -8% (2023, IDC) vs auto semiconductors +10% (2023, SIA); inventory cuts compress near-term margins.

FX: USD/JPY ~150–160 (2023–24)—moves materially affect margins; FY2024 revenue ¥1.62 trillion.

Inputs & rates: Cu ~USD9,000/t, Ni USD22–25k/t, NdPr ~USD70/kg (mid‑2025); Fed funds 5.25–5.50% (Jul 2025).

| Metric | Value |

|---|---|

| Smartphones (2023) | -8% |

| Auto semis (2023) | +10% |

| FY2024 revenue | ¥1.62T |

| USD/JPY | 150–160 |

| Copper | USD9,000/t |

| Nickel | USD22–25k/t |

| NdPr oxide | ~USD70/kg |

| Fed funds (Jul 2025) | 5.25–5.50% |

Full Version Awaits

TDK PESTLE Analysis

The preview shown here is the exact TDK PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; what you see is the final file available for immediate download.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic foresight with our targeted PESTLE Analysis of TDK, revealing how political, economic, and technological shifts reshape its outlook. This concise, research-backed report highlights risks and growth levers for investors and strategists. Purchase the full version to access actionable, exportable insights and stay ahead of market moves.

Political factors

Trade tensions & export controls

US–China technology frictions and expanded export controls (notably US measures in 2022–23 alongside the CHIPS Act $52 billion semiconductor push) constrain advanced components, tooling and cross-border design collaboration; Asia accounts for over 70% of global semiconductor manufacturing, raising lead-time and routing risk. TDK must segment products/customers, tighten licensing, redesign supply routes, and accept higher compliance costs. Strategic dual-sourcing and regionalization mitigate shocks and production-footprint shifts.

Industrial policy & subsidies

CHIPS and Science Act provides $52.7 billion in US incentives, the EU Chips Act targets up to €43 billion to boost capacity, and Japan has rolled multi-billion-yen subsidy programs; these grants lower capex for TDK’s advanced materials, magnetics and power-electronics projects but impose local-job and tech-sharing conditions, while shifting policy cycles create timing and approval risks for plant and R&D investments.

Geopolitical supply-chain exposure

Concentration risks around East Asia, notably Taiwan where TSMC held ~53% foundry share in 2024 and Taiwan supplied >60% of leading-edge wafer capacity, create continuity threats for TDK’s wafers, substrates and passive components. Political instability or conflict could disrupt inputs with wafer lead times already 20–30 weeks in 2024. TDK needs buffer inventory, alternate nodes, diversified logistics lanes and expanded insurance and geopolitical monitoring as core planning inputs.

Localization & procurement mandates

Governments and regulations (eg US IRA, EU Battery Regulation) increasingly mandate local content in automotive and energy projects, driving OEMs to pressure suppliers to align regional footprints; global EV sales reached about 14 million in 2023 (IEA), intensifying localization. TDK may expand local production and engineering to win programs, raising fixed costs but improving resilience and customer proximity.

- Local mandates: regulatory push (US, EU, India)

- OEM pressure: regional sourcing alignment

- TDK action: expand localized production/engineering

- Impact: higher fixed costs; better resilience and proximity

Public investment in electrification

Public electrification spending, including the US Bipartisan Infrastructure Law $7.5 billion EV charger fund and the EU Recovery Facility (~€806.9 billion overall), lifts demand for power inductors, capacitors and sensors as EV and grid modernization pipelines (US target 500,000 chargers by 2030) give multiyear visibility in automotive and industrial segments; TDK can tailor portfolios to qualify for funded projects while policy reversals remain a planning risk.

- EV incentives → higher component demand

- Policy pipelines → multiyear revenue visibility

- Aligning SKUs enables funded-project eligibility

- Reversal risk → scenario planning required

Geopolitical export controls, subsidy race and Taiwan bottlenecks drive EV supply regionalization

Geopolitical tech tensions and export controls (US measures 2022–24; CHIPS $52.7B) raise compliance and redesign costs for TDK. Subsidies (EU ~€43B, Japan multibillion) lower capex but require local jobs/tech sharing. Taiwan concentration (TSMC ~53% foundry share 2024) and 20–30 week wafer lead times heighten continuity risk. EV policy-driven demand (global EVs ~14M in 2023; US 500k chargers target by 2030) forces regionalization.

| Metric | Value |

|---|---|

| CHIPS/US | $52.7B |

| EU Chips | ~€43B |

| TSMC foundry | ~53% (2024) |

| Global EVs | ~14M (2023) |

What is included in the product

Explores how macro-environmental factors uniquely affect TDK across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry trends to reveal threats and opportunities. Designed for executives, consultants, and investors, the analysis offers forward-looking insights and ready-to-use formatting for strategic planning, pitches, and reports.

A compact, category-segmented PESTLE summary of TDK that simplifies external risk assessment and market-position discussions, easily dropped into presentations or shared across teams for quick alignment.

Economic factors

Electronics demand cyclicality

End-market cyclicality is pronounced: global smartphone shipments fell about 8% in 2023 (IDC), while automotive electronics—with the automotive semiconductor market up roughly 10% in 2023 (SIA)—and industrial demand remained steadier. Inventory corrections historically compress orders and pricing, pressuring near-term margins. TDK offsets volatility by tilting its portfolio toward automotive/industrial (roughly two-thirds components exposure) and using flexible manufacturing to shift mix rapidly.

FX volatility (JPY, USD, EUR, CNY)

TDK's revenue mix is highly international while manufacturing and many operating costs remain yen- and local-currency driven, so USD/JPY, EUR/JPY and CNY/JPY swings materially affect margins and competitiveness; yen weakness around 150–160 per USD in 2023–2024 widened reported sales but compressed local-cost margins.

Active hedging programs and shifting production to regional cost bases (Asia, Europe, Americas) have reduced FX-driven earnings volatility, with TDK citing routine use of forwards and natural hedges in FY2024 reporting.

Long-term OEM contracts rely on pricing clauses and pass-through mechanisms; absence of timely indexation can force margin erosion during rapid moves in USD, EUR or CNY versus JPY, making contract terms pivotal for 2024–25 profitability.

Input costs & materials availability

Rare earths, copper, nickel and specialty ceramics now drive TDKs BOM; mid-2025 prices were about copper USD 9,000/t, nickel USD 22,000–25,000/t and NdPr oxide ~USD 70/kg, so spikes and supply constraints can compress margins and delay deliveries. Long-term offtakes and closed-loop recycling reduce exposure, while design-to-cost and value engineering help preserve ASPs.

Interest rates & capex cycles

Higher global policy rates, with the US federal funds target at 5.25–5.50% (July 2025), raise financing costs and temper consumer electronics demand, while automotive, factory automation and energy capex remain resilient but mainly project-driven. TDK times capacity expansions to utilization and funded demand, and its strong balance sheet supports selective counter-cyclical investment.

- Fed funds 5.25–5.50% (Jul 2025)

- Consumer electronics demand softer

- Automotive/factory/energy capex project-driven

- TDK expansion tied to utilization/funded demand

- Strong balance sheet enables counter-cyclical spend

OEM consolidation & pricing power

Larger OEMs concentrated buying power—top five smartphone OEMs accounted for about 65% of global shipments in 2024 (IDC)—drive aggressive cost-downs and enforce dual sourcing, pressuring suppliers on price and volume stability. TDK defends pricing with scale and differentiated performance specs, while platform wins and multi-year agreements (TDK FY2024 revenue ¥1.62 trillion) help stabilize volumes. Services and integrated modules raise switching costs, strengthening pricing resilience.

- OEM concentration ~65% (top 5, IDC 2024)

- Dual sourcing common procurement term

- TDK FY2024 revenue ¥1.62 trillion

- Platform wins + multi-year contracts = volume stability

- Services/modules = higher switching costs

Geopolitical export controls, subsidy race and Taiwan bottlenecks drive EV supply regionalization

Smartphone shipments -8% (2023, IDC) vs auto semiconductors +10% (2023, SIA); inventory cuts compress near-term margins.

FX: USD/JPY ~150–160 (2023–24)—moves materially affect margins; FY2024 revenue ¥1.62 trillion.

Inputs & rates: Cu ~USD9,000/t, Ni USD22–25k/t, NdPr ~USD70/kg (mid‑2025); Fed funds 5.25–5.50% (Jul 2025).

| Metric | Value |

|---|---|

| Smartphones (2023) | -8% |

| Auto semis (2023) | +10% |

| FY2024 revenue | ¥1.62T |

| USD/JPY | 150–160 |

| Copper | USD9,000/t |

| Nickel | USD22–25k/t |

| NdPr oxide | ~USD70/kg |

| Fed funds (Jul 2025) | 5.25–5.50% |

Full Version Awaits

TDK PESTLE Analysis

The preview shown here is the exact TDK PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; what you see is the final file available for immediate download.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic foresight with our targeted PESTLE Analysis of TDK, revealing how political, economic, and technological shifts reshape its outlook. This concise, research-backed report highlights risks and growth levers for investors and strategists. Purchase the full version to access actionable, exportable insights and stay ahead of market moves.

Political factors

Trade tensions & export controls

US–China technology frictions and expanded export controls (notably US measures in 2022–23 alongside the CHIPS Act $52 billion semiconductor push) constrain advanced components, tooling and cross-border design collaboration; Asia accounts for over 70% of global semiconductor manufacturing, raising lead-time and routing risk. TDK must segment products/customers, tighten licensing, redesign supply routes, and accept higher compliance costs. Strategic dual-sourcing and regionalization mitigate shocks and production-footprint shifts.

Industrial policy & subsidies

CHIPS and Science Act provides $52.7 billion in US incentives, the EU Chips Act targets up to €43 billion to boost capacity, and Japan has rolled multi-billion-yen subsidy programs; these grants lower capex for TDK’s advanced materials, magnetics and power-electronics projects but impose local-job and tech-sharing conditions, while shifting policy cycles create timing and approval risks for plant and R&D investments.

Geopolitical supply-chain exposure

Concentration risks around East Asia, notably Taiwan where TSMC held ~53% foundry share in 2024 and Taiwan supplied >60% of leading-edge wafer capacity, create continuity threats for TDK’s wafers, substrates and passive components. Political instability or conflict could disrupt inputs with wafer lead times already 20–30 weeks in 2024. TDK needs buffer inventory, alternate nodes, diversified logistics lanes and expanded insurance and geopolitical monitoring as core planning inputs.

Localization & procurement mandates

Governments and regulations (eg US IRA, EU Battery Regulation) increasingly mandate local content in automotive and energy projects, driving OEMs to pressure suppliers to align regional footprints; global EV sales reached about 14 million in 2023 (IEA), intensifying localization. TDK may expand local production and engineering to win programs, raising fixed costs but improving resilience and customer proximity.

- Local mandates: regulatory push (US, EU, India)

- OEM pressure: regional sourcing alignment

- TDK action: expand localized production/engineering

- Impact: higher fixed costs; better resilience and proximity

Public investment in electrification

Public electrification spending, including the US Bipartisan Infrastructure Law $7.5 billion EV charger fund and the EU Recovery Facility (~€806.9 billion overall), lifts demand for power inductors, capacitors and sensors as EV and grid modernization pipelines (US target 500,000 chargers by 2030) give multiyear visibility in automotive and industrial segments; TDK can tailor portfolios to qualify for funded projects while policy reversals remain a planning risk.

- EV incentives → higher component demand

- Policy pipelines → multiyear revenue visibility

- Aligning SKUs enables funded-project eligibility

- Reversal risk → scenario planning required

Geopolitical export controls, subsidy race and Taiwan bottlenecks drive EV supply regionalization

Geopolitical tech tensions and export controls (US measures 2022–24; CHIPS $52.7B) raise compliance and redesign costs for TDK. Subsidies (EU ~€43B, Japan multibillion) lower capex but require local jobs/tech sharing. Taiwan concentration (TSMC ~53% foundry share 2024) and 20–30 week wafer lead times heighten continuity risk. EV policy-driven demand (global EVs ~14M in 2023; US 500k chargers target by 2030) forces regionalization.

| Metric | Value |

|---|---|

| CHIPS/US | $52.7B |

| EU Chips | ~€43B |

| TSMC foundry | ~53% (2024) |

| Global EVs | ~14M (2023) |

What is included in the product

Explores how macro-environmental factors uniquely affect TDK across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry trends to reveal threats and opportunities. Designed for executives, consultants, and investors, the analysis offers forward-looking insights and ready-to-use formatting for strategic planning, pitches, and reports.

A compact, category-segmented PESTLE summary of TDK that simplifies external risk assessment and market-position discussions, easily dropped into presentations or shared across teams for quick alignment.

Economic factors

Electronics demand cyclicality

End-market cyclicality is pronounced: global smartphone shipments fell about 8% in 2023 (IDC), while automotive electronics—with the automotive semiconductor market up roughly 10% in 2023 (SIA)—and industrial demand remained steadier. Inventory corrections historically compress orders and pricing, pressuring near-term margins. TDK offsets volatility by tilting its portfolio toward automotive/industrial (roughly two-thirds components exposure) and using flexible manufacturing to shift mix rapidly.

FX volatility (JPY, USD, EUR, CNY)

TDK's revenue mix is highly international while manufacturing and many operating costs remain yen- and local-currency driven, so USD/JPY, EUR/JPY and CNY/JPY swings materially affect margins and competitiveness; yen weakness around 150–160 per USD in 2023–2024 widened reported sales but compressed local-cost margins.

Active hedging programs and shifting production to regional cost bases (Asia, Europe, Americas) have reduced FX-driven earnings volatility, with TDK citing routine use of forwards and natural hedges in FY2024 reporting.

Long-term OEM contracts rely on pricing clauses and pass-through mechanisms; absence of timely indexation can force margin erosion during rapid moves in USD, EUR or CNY versus JPY, making contract terms pivotal for 2024–25 profitability.

Input costs & materials availability

Rare earths, copper, nickel and specialty ceramics now drive TDKs BOM; mid-2025 prices were about copper USD 9,000/t, nickel USD 22,000–25,000/t and NdPr oxide ~USD 70/kg, so spikes and supply constraints can compress margins and delay deliveries. Long-term offtakes and closed-loop recycling reduce exposure, while design-to-cost and value engineering help preserve ASPs.

Interest rates & capex cycles

Higher global policy rates, with the US federal funds target at 5.25–5.50% (July 2025), raise financing costs and temper consumer electronics demand, while automotive, factory automation and energy capex remain resilient but mainly project-driven. TDK times capacity expansions to utilization and funded demand, and its strong balance sheet supports selective counter-cyclical investment.

- Fed funds 5.25–5.50% (Jul 2025)

- Consumer electronics demand softer

- Automotive/factory/energy capex project-driven

- TDK expansion tied to utilization/funded demand

- Strong balance sheet enables counter-cyclical spend

OEM consolidation & pricing power

Larger OEMs concentrated buying power—top five smartphone OEMs accounted for about 65% of global shipments in 2024 (IDC)—drive aggressive cost-downs and enforce dual sourcing, pressuring suppliers on price and volume stability. TDK defends pricing with scale and differentiated performance specs, while platform wins and multi-year agreements (TDK FY2024 revenue ¥1.62 trillion) help stabilize volumes. Services and integrated modules raise switching costs, strengthening pricing resilience.

- OEM concentration ~65% (top 5, IDC 2024)

- Dual sourcing common procurement term

- TDK FY2024 revenue ¥1.62 trillion

- Platform wins + multi-year contracts = volume stability

- Services/modules = higher switching costs

Geopolitical export controls, subsidy race and Taiwan bottlenecks drive EV supply regionalization

Smartphone shipments -8% (2023, IDC) vs auto semiconductors +10% (2023, SIA); inventory cuts compress near-term margins.

FX: USD/JPY ~150–160 (2023–24)—moves materially affect margins; FY2024 revenue ¥1.62 trillion.

Inputs & rates: Cu ~USD9,000/t, Ni USD22–25k/t, NdPr ~USD70/kg (mid‑2025); Fed funds 5.25–5.50% (Jul 2025).

| Metric | Value |

|---|---|

| Smartphones (2023) | -8% |

| Auto semis (2023) | +10% |

| FY2024 revenue | ¥1.62T |

| USD/JPY | 150–160 |

| Copper | USD9,000/t |

| Nickel | USD22–25k/t |

| NdPr oxide | ~USD70/kg |

| Fed funds (Jul 2025) | 5.25–5.50% |

Full Version Awaits

TDK PESTLE Analysis

The preview shown here is the exact TDK PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; what you see is the final file available for immediate download.