technotrans SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Technotrans SWOT reveals key strengths in thermal management and global service network, but also highlights margin pressure and cyclical end-markets. Want strategic clarity? Purchase the full SWOT analysis for a research-backed, investor-ready report with editable Word and Excel deliverables to plan, pitch, and act with confidence.

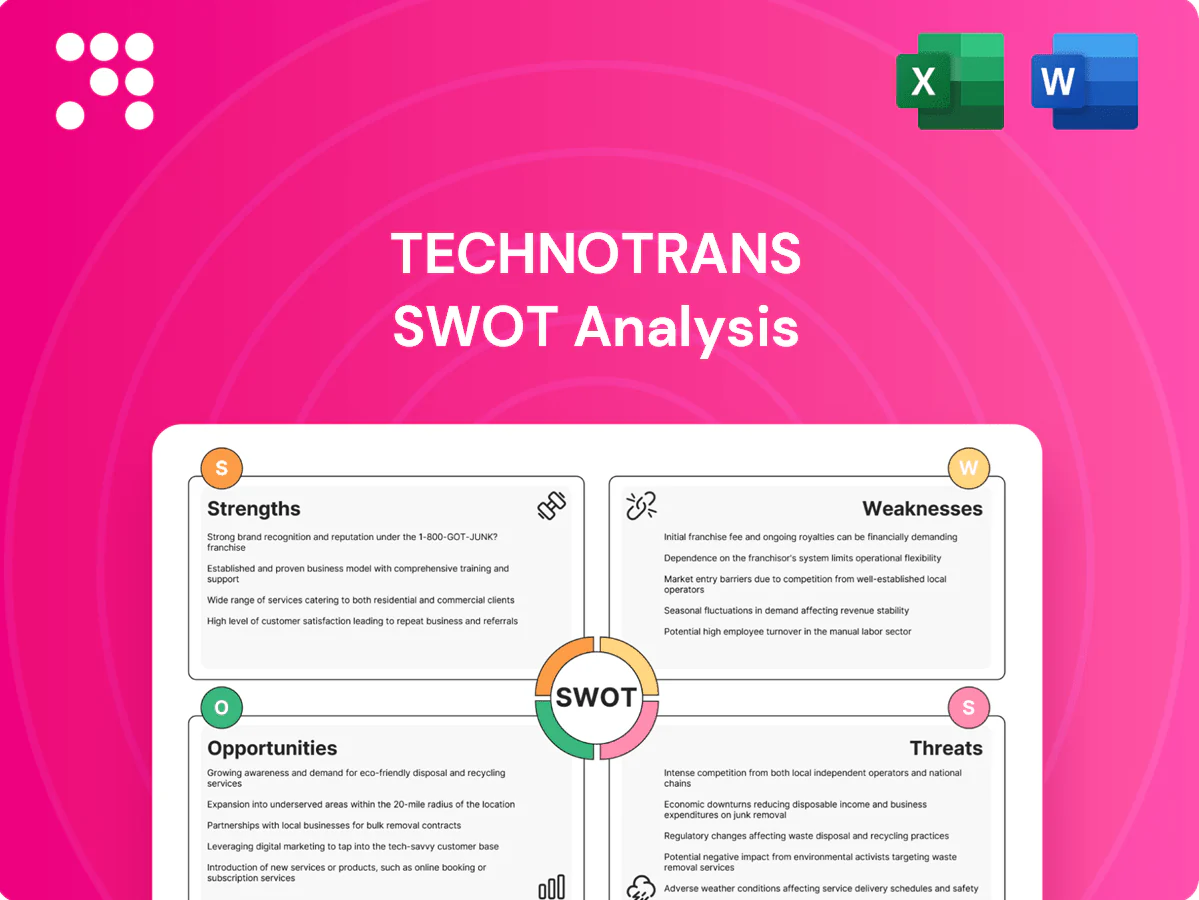

Strengths

Diversified thermal portfolio

Technotrans offers cooling, temperature control, filtration and spray systems, spreading risk across complementary product lines and enabling cross-selling and bundled solutions; this breadth helps stabilize revenue across cycles and supports tailored customization for niche industrial needs.

Multi-industry exposure

Serving four distinct industries—printing, plastics, laser, and e-mobility—mitigates dependence on any single market; demand weakness in one vertical can be offset by strength in another. This mix enhances resilience to industry-specific downturns and reduces revenue volatility. It also broadens the company’s innovation pipeline by exposing R&D to diverse applications and technology transfer opportunities.

Engineering and integration know-how

Strong systems integration in thermal and fluid technology is a high barrier capability that lets technotrans deliver turnkey, reliable, precise controls valued by industrial clients. This expertise supported technotrans’s 2024 revenue of €292m and elevated gross margins versus peers, enabling premium pricing and stickier customer relationships. Integrated solutions shorten time-to-solution for custom projects, reducing deployment cycles and boosting repeat orders.

Efficiency and sustainability focus

Energy-efficient thermal management lowers customers' total cost of ownership through reduced energy consumption and longer equipment life, while technotrans' sustainability positioning maps to the EU CSRD rollout from 2024 and the Fit for 55 55% emissions target by 2030, helping win tenders and secure long-term contracts versus lower-cost, less efficient rivals.

- Reduces TCO

- Aligns with CSRD (2024)

- Supports Fit for 55 (55% by 2030)

- Differentiates vs low-cost rivals

Reputation in niche applications

Technotrans AGs established presence in printing and high-precision cooling processes—backed by a publicly listed profile on the Frankfurt exchange—underpins credibility and has built an installed base of thousands of systems, de-risking adoption for new clients. High uptime and strict quality benchmarks support strong repeat business and enable entry into adjacent applications.

- Listed on Frankfurt exchange

- Installed base: thousands of systems

- High uptime → strong repeat business

- Reputation enables adjacent-market entry

Diversified thermal-fluid systems bolster resilient €292m 2024 revenue

Technotrans combines diversified thermal-fluid product lines and systems integration to stabilize revenue and enable cross-selling; 2024 revenue reached €292m. Serving printing, plastics, laser and e-mobility reduces market concentration risk and boosts R&D transfer. Energy-efficient solutions align with CSRD (2024) and Fit for 55 (55% by 2030), strengthening tenders and long-term contracts.

| Metric | Value |

|---|---|

| Revenue (2024) | €292m |

| Installed base | Thousands of systems |

| Listing | Frankfurt Exchange |

| Regulatory alignment | CSRD (2024), Fit for 55 (55% by 2030) |

What is included in the product

Provides a concise SWOT analysis of technotrans, identifying internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making and future growth.

Provides a concise technotrans SWOT matrix for fast strategic alignment and clear stakeholder communication; editable, visual format enables quick updates and seamless integration into reports and presentations.

Weaknesses

Scale versus global peers

Compared with large HVAC and thermal conglomerates, technotrans operates at a noticeably smaller scale, limiting purchasing leverage and squeezing R&D spend; this size gap also slows expansion of global service coverage and can force tighter margins in price-sensitive bids.

Exposure to cyclical capex

Exposure to cyclical capex makes technotrans vulnerable as industrial equipment demand follows capital spending cycles; the company reported revenues of €257.2m in 2023, highlighting scale tied to customer capex. Downturns in printing or plastics can sharply reduce orders, while project-based revenues are lumpy and less predictable, amplifying working capital swings during slowdowns.

Portfolio complexity

Custom solutions and a broad SKU mix increase operational complexity for technotrans, headquartered in Sassenberg and listed on SDAX, driving longer lead times and higher cost-to-serve; industry studies show customization can raise unit costs by up to 25%. Complexity complicates quality control across variants and can slow standardization efforts, risking delayed responses to bespoke customer needs.

Aftermarket footprint limitations

Aftermarket footprint limitations mean thinner service networks in some regions, causing slower response times and higher downtime for technotrans customers; limited local parts availability further reduces equipment uptime and weakens lifecycle revenue capture, increasing churn risk to competitors with denser service coverage.

- Thinner regional service coverage

- Slower response times

- Limited local parts availability

- Lower lifecycle revenue capture

- Higher customer churn risk

Legacy sector dependence

Printing, while stable in specific niches, is structurally mature across many markets, and Technotrans reliance on legacy printing-related revenues limits upside as higher-growth segments expand; reallocating R&D and capex has been slower than peers, creating opportunity cost and focus dilution.

- Legacy printing dependence

- Slow resource shift to growth areas

- Opportunity cost from focus dilution

Scale limits R and D; revenue €257.2m, customization +25%

Smaller scale vs HVAC giants limits purchasing power and R&D, tying revenues to cyclical capex (revenue €257.2m in 2023) and producing lumpy project income; customization raises unit costs (industry studies: up to 25%) while aftermarket/service reach from Sassenberg and SDAX listing remains shallow, risking downtime and churn.

| Metric | Value |

|---|---|

| Revenue (2023) | €257.2m |

| Customization cost uplift | up to 25% |

Preview Before You Purchase

technotrans SWOT Analysis

This is the actual SWOT analysis document for technotrans you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and is fully editable. Buy now to unlock the complete, detailed version.

Go Beyond the Preview—Access the Full Strategic Report

Technotrans SWOT reveals key strengths in thermal management and global service network, but also highlights margin pressure and cyclical end-markets. Want strategic clarity? Purchase the full SWOT analysis for a research-backed, investor-ready report with editable Word and Excel deliverables to plan, pitch, and act with confidence.

Strengths

Diversified thermal portfolio

Technotrans offers cooling, temperature control, filtration and spray systems, spreading risk across complementary product lines and enabling cross-selling and bundled solutions; this breadth helps stabilize revenue across cycles and supports tailored customization for niche industrial needs.

Multi-industry exposure

Serving four distinct industries—printing, plastics, laser, and e-mobility—mitigates dependence on any single market; demand weakness in one vertical can be offset by strength in another. This mix enhances resilience to industry-specific downturns and reduces revenue volatility. It also broadens the company’s innovation pipeline by exposing R&D to diverse applications and technology transfer opportunities.

Engineering and integration know-how

Strong systems integration in thermal and fluid technology is a high barrier capability that lets technotrans deliver turnkey, reliable, precise controls valued by industrial clients. This expertise supported technotrans’s 2024 revenue of €292m and elevated gross margins versus peers, enabling premium pricing and stickier customer relationships. Integrated solutions shorten time-to-solution for custom projects, reducing deployment cycles and boosting repeat orders.

Efficiency and sustainability focus

Energy-efficient thermal management lowers customers' total cost of ownership through reduced energy consumption and longer equipment life, while technotrans' sustainability positioning maps to the EU CSRD rollout from 2024 and the Fit for 55 55% emissions target by 2030, helping win tenders and secure long-term contracts versus lower-cost, less efficient rivals.

- Reduces TCO

- Aligns with CSRD (2024)

- Supports Fit for 55 (55% by 2030)

- Differentiates vs low-cost rivals

Reputation in niche applications

Technotrans AGs established presence in printing and high-precision cooling processes—backed by a publicly listed profile on the Frankfurt exchange—underpins credibility and has built an installed base of thousands of systems, de-risking adoption for new clients. High uptime and strict quality benchmarks support strong repeat business and enable entry into adjacent applications.

- Listed on Frankfurt exchange

- Installed base: thousands of systems

- High uptime → strong repeat business

- Reputation enables adjacent-market entry

Diversified thermal-fluid systems bolster resilient €292m 2024 revenue

Technotrans combines diversified thermal-fluid product lines and systems integration to stabilize revenue and enable cross-selling; 2024 revenue reached €292m. Serving printing, plastics, laser and e-mobility reduces market concentration risk and boosts R&D transfer. Energy-efficient solutions align with CSRD (2024) and Fit for 55 (55% by 2030), strengthening tenders and long-term contracts.

| Metric | Value |

|---|---|

| Revenue (2024) | €292m |

| Installed base | Thousands of systems |

| Listing | Frankfurt Exchange |

| Regulatory alignment | CSRD (2024), Fit for 55 (55% by 2030) |

What is included in the product

Provides a concise SWOT analysis of technotrans, identifying internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making and future growth.

Provides a concise technotrans SWOT matrix for fast strategic alignment and clear stakeholder communication; editable, visual format enables quick updates and seamless integration into reports and presentations.

Weaknesses

Scale versus global peers

Compared with large HVAC and thermal conglomerates, technotrans operates at a noticeably smaller scale, limiting purchasing leverage and squeezing R&D spend; this size gap also slows expansion of global service coverage and can force tighter margins in price-sensitive bids.

Exposure to cyclical capex

Exposure to cyclical capex makes technotrans vulnerable as industrial equipment demand follows capital spending cycles; the company reported revenues of €257.2m in 2023, highlighting scale tied to customer capex. Downturns in printing or plastics can sharply reduce orders, while project-based revenues are lumpy and less predictable, amplifying working capital swings during slowdowns.

Portfolio complexity

Custom solutions and a broad SKU mix increase operational complexity for technotrans, headquartered in Sassenberg and listed on SDAX, driving longer lead times and higher cost-to-serve; industry studies show customization can raise unit costs by up to 25%. Complexity complicates quality control across variants and can slow standardization efforts, risking delayed responses to bespoke customer needs.

Aftermarket footprint limitations

Aftermarket footprint limitations mean thinner service networks in some regions, causing slower response times and higher downtime for technotrans customers; limited local parts availability further reduces equipment uptime and weakens lifecycle revenue capture, increasing churn risk to competitors with denser service coverage.

- Thinner regional service coverage

- Slower response times

- Limited local parts availability

- Lower lifecycle revenue capture

- Higher customer churn risk

Legacy sector dependence

Printing, while stable in specific niches, is structurally mature across many markets, and Technotrans reliance on legacy printing-related revenues limits upside as higher-growth segments expand; reallocating R&D and capex has been slower than peers, creating opportunity cost and focus dilution.

- Legacy printing dependence

- Slow resource shift to growth areas

- Opportunity cost from focus dilution

Scale limits R and D; revenue €257.2m, customization +25%

Smaller scale vs HVAC giants limits purchasing power and R&D, tying revenues to cyclical capex (revenue €257.2m in 2023) and producing lumpy project income; customization raises unit costs (industry studies: up to 25%) while aftermarket/service reach from Sassenberg and SDAX listing remains shallow, risking downtime and churn.

| Metric | Value |

|---|---|

| Revenue (2023) | €257.2m |

| Customization cost uplift | up to 25% |

Preview Before You Purchase

technotrans SWOT Analysis

This is the actual SWOT analysis document for technotrans you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and is fully editable. Buy now to unlock the complete, detailed version.

Description

Go Beyond the Preview—Access the Full Strategic Report

Technotrans SWOT reveals key strengths in thermal management and global service network, but also highlights margin pressure and cyclical end-markets. Want strategic clarity? Purchase the full SWOT analysis for a research-backed, investor-ready report with editable Word and Excel deliverables to plan, pitch, and act with confidence.

Strengths

Diversified thermal portfolio

Technotrans offers cooling, temperature control, filtration and spray systems, spreading risk across complementary product lines and enabling cross-selling and bundled solutions; this breadth helps stabilize revenue across cycles and supports tailored customization for niche industrial needs.

Multi-industry exposure

Serving four distinct industries—printing, plastics, laser, and e-mobility—mitigates dependence on any single market; demand weakness in one vertical can be offset by strength in another. This mix enhances resilience to industry-specific downturns and reduces revenue volatility. It also broadens the company’s innovation pipeline by exposing R&D to diverse applications and technology transfer opportunities.

Engineering and integration know-how

Strong systems integration in thermal and fluid technology is a high barrier capability that lets technotrans deliver turnkey, reliable, precise controls valued by industrial clients. This expertise supported technotrans’s 2024 revenue of €292m and elevated gross margins versus peers, enabling premium pricing and stickier customer relationships. Integrated solutions shorten time-to-solution for custom projects, reducing deployment cycles and boosting repeat orders.

Efficiency and sustainability focus

Energy-efficient thermal management lowers customers' total cost of ownership through reduced energy consumption and longer equipment life, while technotrans' sustainability positioning maps to the EU CSRD rollout from 2024 and the Fit for 55 55% emissions target by 2030, helping win tenders and secure long-term contracts versus lower-cost, less efficient rivals.

- Reduces TCO

- Aligns with CSRD (2024)

- Supports Fit for 55 (55% by 2030)

- Differentiates vs low-cost rivals

Reputation in niche applications

Technotrans AGs established presence in printing and high-precision cooling processes—backed by a publicly listed profile on the Frankfurt exchange—underpins credibility and has built an installed base of thousands of systems, de-risking adoption for new clients. High uptime and strict quality benchmarks support strong repeat business and enable entry into adjacent applications.

- Listed on Frankfurt exchange

- Installed base: thousands of systems

- High uptime → strong repeat business

- Reputation enables adjacent-market entry

Diversified thermal-fluid systems bolster resilient €292m 2024 revenue

Technotrans combines diversified thermal-fluid product lines and systems integration to stabilize revenue and enable cross-selling; 2024 revenue reached €292m. Serving printing, plastics, laser and e-mobility reduces market concentration risk and boosts R&D transfer. Energy-efficient solutions align with CSRD (2024) and Fit for 55 (55% by 2030), strengthening tenders and long-term contracts.

| Metric | Value |

|---|---|

| Revenue (2024) | €292m |

| Installed base | Thousands of systems |

| Listing | Frankfurt Exchange |

| Regulatory alignment | CSRD (2024), Fit for 55 (55% by 2030) |

What is included in the product

Provides a concise SWOT analysis of technotrans, identifying internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making and future growth.

Provides a concise technotrans SWOT matrix for fast strategic alignment and clear stakeholder communication; editable, visual format enables quick updates and seamless integration into reports and presentations.

Weaknesses

Scale versus global peers

Compared with large HVAC and thermal conglomerates, technotrans operates at a noticeably smaller scale, limiting purchasing leverage and squeezing R&D spend; this size gap also slows expansion of global service coverage and can force tighter margins in price-sensitive bids.

Exposure to cyclical capex

Exposure to cyclical capex makes technotrans vulnerable as industrial equipment demand follows capital spending cycles; the company reported revenues of €257.2m in 2023, highlighting scale tied to customer capex. Downturns in printing or plastics can sharply reduce orders, while project-based revenues are lumpy and less predictable, amplifying working capital swings during slowdowns.

Portfolio complexity

Custom solutions and a broad SKU mix increase operational complexity for technotrans, headquartered in Sassenberg and listed on SDAX, driving longer lead times and higher cost-to-serve; industry studies show customization can raise unit costs by up to 25%. Complexity complicates quality control across variants and can slow standardization efforts, risking delayed responses to bespoke customer needs.

Aftermarket footprint limitations

Aftermarket footprint limitations mean thinner service networks in some regions, causing slower response times and higher downtime for technotrans customers; limited local parts availability further reduces equipment uptime and weakens lifecycle revenue capture, increasing churn risk to competitors with denser service coverage.

- Thinner regional service coverage

- Slower response times

- Limited local parts availability

- Lower lifecycle revenue capture

- Higher customer churn risk

Legacy sector dependence

Printing, while stable in specific niches, is structurally mature across many markets, and Technotrans reliance on legacy printing-related revenues limits upside as higher-growth segments expand; reallocating R&D and capex has been slower than peers, creating opportunity cost and focus dilution.

- Legacy printing dependence

- Slow resource shift to growth areas

- Opportunity cost from focus dilution

Scale limits R and D; revenue €257.2m, customization +25%

Smaller scale vs HVAC giants limits purchasing power and R&D, tying revenues to cyclical capex (revenue €257.2m in 2023) and producing lumpy project income; customization raises unit costs (industry studies: up to 25%) while aftermarket/service reach from Sassenberg and SDAX listing remains shallow, risking downtime and churn.

| Metric | Value |

|---|---|

| Revenue (2023) | €257.2m |

| Customization cost uplift | up to 25% |

Preview Before You Purchase

technotrans SWOT Analysis

This is the actual SWOT analysis document for technotrans you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and is fully editable. Buy now to unlock the complete, detailed version.