TechTarget Porter's Five Forces Analysis

Don't Miss the Bigger Picture

This snapshot highlights TechTarget’s competitive dynamics, key market pressures, and strategic vulnerabilities in concise form. It flags buyer and supplier power, threat of new entrants, and substitution risks shaping future margins. Want deeper, data-driven force ratings, visuals, and implications? Unlock the full Porter’s Five Forces Analysis to inform strategy and investment decisions.

Suppliers Bargaining Power

Specialist content creators

Experienced tech journalists, analysts and SMEs are scarce and command premium rates, commonly 2–4x standard writing fees; their credibility boosts audience trust and lead quality, raising switching costs. Concentration in AI, cloud and cybersecurity—which drove roughly 45% of enterprise content demand in 2024—increases supplier leverage. Long-term contracts and in-house editorial teams notably moderate this power.

Data and ad-tech infrastructure

TechTarget relies on marketing automation, intent-data enrichment and measurement tools hosted on major platforms that in 2024 accounted for roughly 68% of global IaaS/PaaS share (AWS/Azure/GCP), concentrating supplier bargaining power. Key platforms and APIs can impose fees, policy changes or data access limits that raise costs or impair targeting. Vendor consolidation in martech heightens dependency risk, while building proprietary data pipelines and first‑party intent reduces exposure.

Cloud hosting and delivery

Scalable hosting and CDN providers underpin TechTarget site performance and webinars; public cloud spending topped $600 billion in 2024 and the top three providers held roughly two-thirds of the market, giving suppliers significant leverage. Migration and integration create switching frictions. Usage-based pricing can spike during traffic or event surges. Multi-cloud/CDN strategies curb single-supplier power.

Event and webinar partners

Event and webinar partners (platforms like Zoom, ON24, Hopin and production vendors) materially shape audience experience and pricing; Zoom reported $4.39B revenue in fiscal 2024. Peak-demand windows compress supply and raise prices, while standardized formats and internal studios can cut external spend and reliance. Diversifying platforms reduces suppliers’ negotiation leverage and outage risk.

- Platform concentration: Zoom $4.39B FY2024

- Mitigation: internal studios, standard formats

- Strategy: multi-platform sourcing

Third-party research and syndication

Licensing analyst reports and benchmarks boosts TechTarget content relevance and engagement, but truly exclusive datasets are rare and command premium syndication fees, pressuring margins; building proprietary surveys over time lowers supplier dependence and captures first-party data while co-branded research deals balance cost-sharing with differentiation.

- Licensing increases appeal

- Exclusive data scarce/expensive

- Proprietary surveys reduce reliance

- Co-branding balances cost and uniqueness

Supplier power and cloud concentration lift pricing risk; AI drove 45%

Supplier power is high: niche tech journalists and exclusive datasets command 2–4x fees and lift switching costs; AI/cloud/cyber drove ~45% of enterprise content demand in 2024. Core infrastructure dependence is acute—AWS/Azure/GCP held ~68% IaaS/PaaS in 2024 and public cloud spend topped $600B—raising pricing and policy risks. Mitigants: in‑house studios, proprietary surveys, multi‑cloud and co‑branding reduce supplier leverage.

| Factor | 2024 Stat |

|---|---|

| Content demand concentration | ~45% |

| Top cloud share (AWS/Azure/GCP) | ~68% |

| Public cloud spend | $600B+ |

| Zoom revenue FY2024 | $4.39B |

What is included in the product

Tailored Porter's Five Forces analysis for TechTarget that uncovers competitive drivers, buyer and supplier power, substitutes, and entry risks, identifies disruptive threats and market dynamics affecting share and pricing, and delivers strategic insights ready for inclusion in investor materials or internal strategy decks.

TechTarget's Porter's Five Forces template delivers a clear one-sheet summary with customizable pressure levels and an instant spider chart, eliminating complex code and making it easy to drop into pitch decks, dashboards, or boardroom slides for faster, data-driven decisions.

Customers Bargaining Power

Tech vendors and agencies

Advertisers face many alternatives for lead-gen and brand spend, raising bargaining power as global digital ad spend topped roughly $600B in 2024 and channels compete on cost per lead. Budgets reallocate quickly toward lower-CPL, higher-ROI channels, while volume commitments secure discounts and custom packages. Demonstrable intent-data lifts, often producing double-digit increases in SQL conversion, temper pure price pressure.

Performance-driven procurement

Buyers now demand granular attribution, strict SLAs and make-goods, with pricing often tied to quality thresholds like MQL/SQL definitions, driving tougher negotiations and short cancellation windows (commonly 30–90 days). This performance-driven procurement compresses decision cycles and elevates enforcement of KPIs. Strong conversion metrics and vendor case studies—often showing multi-fold uplift—help vendors retain pricing power and reduce churn risk.

Consolidated enterprise accounts

Large global vendors drive significant revenue concentration at TechTarget; the company reported roughly $395 million in 2023 revenue, making top enterprise accounts materially important to pipeline health. Loss or pauses of a few consolidated accounts can swing quarterly bookings by millions, elevating short-term churn risk. Dedicated account management and multi-product bundles improve retention, and deeper cross-portfolio penetration dilutes single-buyer leverage.

Audience expectations (IT decision-makers)

IT decision-makers in 2024 demand unbiased, deep technical content and granular privacy controls; poor relevance reduces engagement and lead quality, indirectly empowering advertisers and partners. Compliance with GDPR and CCPA plus clear preference centers is mandatory. High trust reduces ad fatigue and improves conversion.

- 2024 Forrester: 69% of ITDMs prefer vendor-agnostic technical content

- GDPR/CCPA compliance required

- High trust lowers ad fatigue, boosts conversions

Cyclicality and macro sensitivity

IT marketing budgets swing with product cycles and macro conditions; Gartner forecast global IT spending around 5.1 trillion USD in 2024, heightening buyer leverage in slowdowns when buyers demand lower CPLs and flexible terms.

- Countercyclical lower-funnel intent preserves spend

- Diversified industry mix smooths volatility

Advertisers gain leverage as ~$600B digital ad market intensifies price and attribution pressure

Advertisers have high leverage as global digital ad spend reached ~$600B in 2024, driving price competition and CPL focus. Buyers demand granular attribution, SLAs and short cancellation windows, increasing negotiation pressure. TechTarget concentration (≈$395M revenue in 2023) means a few large accounts can swing bookings.

| Metric | Value |

|---|---|

| Global digital ad spend 2024 | ~$600B |

| TechTarget revenue 2023 | ~$395M |

| Global IT spend 2024 (Gartner) | $5.1T |

| Forrester ITDM preference | 69% |

Preview Before You Purchase

TechTarget Porter's Five Forces Analysis

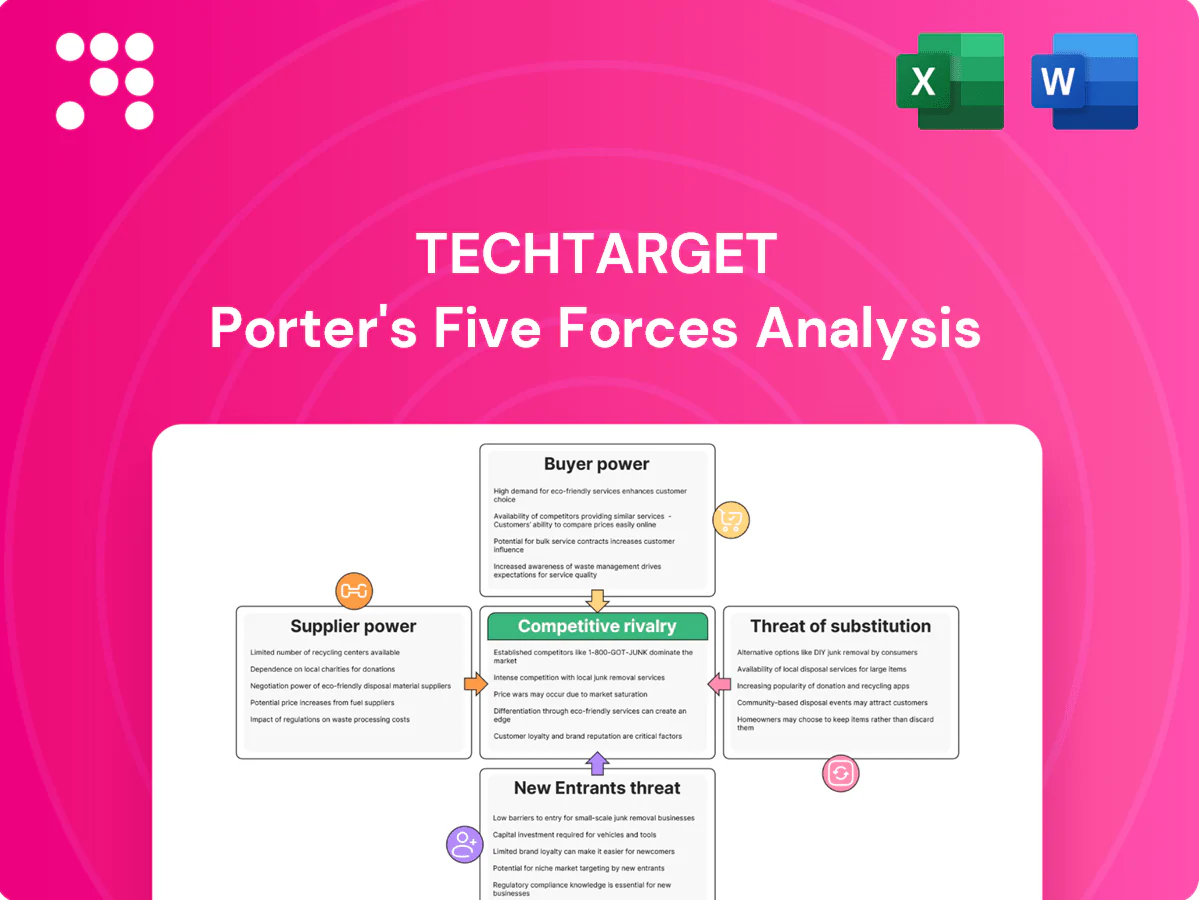

The TechTarget Porter's Five Forces analysis evaluates competitive rivalry, threat of new entrants, bargaining power of buyers and suppliers, and threat of substitutes with data-driven insights and strategic implications. This preview is the exact, professionally formatted document you'll receive instantly after purchase—no placeholders or changes. It's ready for immediate download and use to inform strategy and investment decisions.

Don't Miss the Bigger Picture

This snapshot highlights TechTarget’s competitive dynamics, key market pressures, and strategic vulnerabilities in concise form. It flags buyer and supplier power, threat of new entrants, and substitution risks shaping future margins. Want deeper, data-driven force ratings, visuals, and implications? Unlock the full Porter’s Five Forces Analysis to inform strategy and investment decisions.

Suppliers Bargaining Power

Specialist content creators

Experienced tech journalists, analysts and SMEs are scarce and command premium rates, commonly 2–4x standard writing fees; their credibility boosts audience trust and lead quality, raising switching costs. Concentration in AI, cloud and cybersecurity—which drove roughly 45% of enterprise content demand in 2024—increases supplier leverage. Long-term contracts and in-house editorial teams notably moderate this power.

Data and ad-tech infrastructure

TechTarget relies on marketing automation, intent-data enrichment and measurement tools hosted on major platforms that in 2024 accounted for roughly 68% of global IaaS/PaaS share (AWS/Azure/GCP), concentrating supplier bargaining power. Key platforms and APIs can impose fees, policy changes or data access limits that raise costs or impair targeting. Vendor consolidation in martech heightens dependency risk, while building proprietary data pipelines and first‑party intent reduces exposure.

Cloud hosting and delivery

Scalable hosting and CDN providers underpin TechTarget site performance and webinars; public cloud spending topped $600 billion in 2024 and the top three providers held roughly two-thirds of the market, giving suppliers significant leverage. Migration and integration create switching frictions. Usage-based pricing can spike during traffic or event surges. Multi-cloud/CDN strategies curb single-supplier power.

Event and webinar partners

Event and webinar partners (platforms like Zoom, ON24, Hopin and production vendors) materially shape audience experience and pricing; Zoom reported $4.39B revenue in fiscal 2024. Peak-demand windows compress supply and raise prices, while standardized formats and internal studios can cut external spend and reliance. Diversifying platforms reduces suppliers’ negotiation leverage and outage risk.

- Platform concentration: Zoom $4.39B FY2024

- Mitigation: internal studios, standard formats

- Strategy: multi-platform sourcing

Third-party research and syndication

Licensing analyst reports and benchmarks boosts TechTarget content relevance and engagement, but truly exclusive datasets are rare and command premium syndication fees, pressuring margins; building proprietary surveys over time lowers supplier dependence and captures first-party data while co-branded research deals balance cost-sharing with differentiation.

- Licensing increases appeal

- Exclusive data scarce/expensive

- Proprietary surveys reduce reliance

- Co-branding balances cost and uniqueness

Supplier power and cloud concentration lift pricing risk; AI drove 45%

Supplier power is high: niche tech journalists and exclusive datasets command 2–4x fees and lift switching costs; AI/cloud/cyber drove ~45% of enterprise content demand in 2024. Core infrastructure dependence is acute—AWS/Azure/GCP held ~68% IaaS/PaaS in 2024 and public cloud spend topped $600B—raising pricing and policy risks. Mitigants: in‑house studios, proprietary surveys, multi‑cloud and co‑branding reduce supplier leverage.

| Factor | 2024 Stat |

|---|---|

| Content demand concentration | ~45% |

| Top cloud share (AWS/Azure/GCP) | ~68% |

| Public cloud spend | $600B+ |

| Zoom revenue FY2024 | $4.39B |

What is included in the product

Tailored Porter's Five Forces analysis for TechTarget that uncovers competitive drivers, buyer and supplier power, substitutes, and entry risks, identifies disruptive threats and market dynamics affecting share and pricing, and delivers strategic insights ready for inclusion in investor materials or internal strategy decks.

TechTarget's Porter's Five Forces template delivers a clear one-sheet summary with customizable pressure levels and an instant spider chart, eliminating complex code and making it easy to drop into pitch decks, dashboards, or boardroom slides for faster, data-driven decisions.

Customers Bargaining Power

Tech vendors and agencies

Advertisers face many alternatives for lead-gen and brand spend, raising bargaining power as global digital ad spend topped roughly $600B in 2024 and channels compete on cost per lead. Budgets reallocate quickly toward lower-CPL, higher-ROI channels, while volume commitments secure discounts and custom packages. Demonstrable intent-data lifts, often producing double-digit increases in SQL conversion, temper pure price pressure.

Performance-driven procurement

Buyers now demand granular attribution, strict SLAs and make-goods, with pricing often tied to quality thresholds like MQL/SQL definitions, driving tougher negotiations and short cancellation windows (commonly 30–90 days). This performance-driven procurement compresses decision cycles and elevates enforcement of KPIs. Strong conversion metrics and vendor case studies—often showing multi-fold uplift—help vendors retain pricing power and reduce churn risk.

Consolidated enterprise accounts

Large global vendors drive significant revenue concentration at TechTarget; the company reported roughly $395 million in 2023 revenue, making top enterprise accounts materially important to pipeline health. Loss or pauses of a few consolidated accounts can swing quarterly bookings by millions, elevating short-term churn risk. Dedicated account management and multi-product bundles improve retention, and deeper cross-portfolio penetration dilutes single-buyer leverage.

Audience expectations (IT decision-makers)

IT decision-makers in 2024 demand unbiased, deep technical content and granular privacy controls; poor relevance reduces engagement and lead quality, indirectly empowering advertisers and partners. Compliance with GDPR and CCPA plus clear preference centers is mandatory. High trust reduces ad fatigue and improves conversion.

- 2024 Forrester: 69% of ITDMs prefer vendor-agnostic technical content

- GDPR/CCPA compliance required

- High trust lowers ad fatigue, boosts conversions

Cyclicality and macro sensitivity

IT marketing budgets swing with product cycles and macro conditions; Gartner forecast global IT spending around 5.1 trillion USD in 2024, heightening buyer leverage in slowdowns when buyers demand lower CPLs and flexible terms.

- Countercyclical lower-funnel intent preserves spend

- Diversified industry mix smooths volatility

Advertisers gain leverage as ~$600B digital ad market intensifies price and attribution pressure

Advertisers have high leverage as global digital ad spend reached ~$600B in 2024, driving price competition and CPL focus. Buyers demand granular attribution, SLAs and short cancellation windows, increasing negotiation pressure. TechTarget concentration (≈$395M revenue in 2023) means a few large accounts can swing bookings.

| Metric | Value |

|---|---|

| Global digital ad spend 2024 | ~$600B |

| TechTarget revenue 2023 | ~$395M |

| Global IT spend 2024 (Gartner) | $5.1T |

| Forrester ITDM preference | 69% |

Preview Before You Purchase

TechTarget Porter's Five Forces Analysis

The TechTarget Porter's Five Forces analysis evaluates competitive rivalry, threat of new entrants, bargaining power of buyers and suppliers, and threat of substitutes with data-driven insights and strategic implications. This preview is the exact, professionally formatted document you'll receive instantly after purchase—no placeholders or changes. It's ready for immediate download and use to inform strategy and investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

This snapshot highlights TechTarget’s competitive dynamics, key market pressures, and strategic vulnerabilities in concise form. It flags buyer and supplier power, threat of new entrants, and substitution risks shaping future margins. Want deeper, data-driven force ratings, visuals, and implications? Unlock the full Porter’s Five Forces Analysis to inform strategy and investment decisions.

Suppliers Bargaining Power

Specialist content creators

Experienced tech journalists, analysts and SMEs are scarce and command premium rates, commonly 2–4x standard writing fees; their credibility boosts audience trust and lead quality, raising switching costs. Concentration in AI, cloud and cybersecurity—which drove roughly 45% of enterprise content demand in 2024—increases supplier leverage. Long-term contracts and in-house editorial teams notably moderate this power.

Data and ad-tech infrastructure

TechTarget relies on marketing automation, intent-data enrichment and measurement tools hosted on major platforms that in 2024 accounted for roughly 68% of global IaaS/PaaS share (AWS/Azure/GCP), concentrating supplier bargaining power. Key platforms and APIs can impose fees, policy changes or data access limits that raise costs or impair targeting. Vendor consolidation in martech heightens dependency risk, while building proprietary data pipelines and first‑party intent reduces exposure.

Cloud hosting and delivery

Scalable hosting and CDN providers underpin TechTarget site performance and webinars; public cloud spending topped $600 billion in 2024 and the top three providers held roughly two-thirds of the market, giving suppliers significant leverage. Migration and integration create switching frictions. Usage-based pricing can spike during traffic or event surges. Multi-cloud/CDN strategies curb single-supplier power.

Event and webinar partners

Event and webinar partners (platforms like Zoom, ON24, Hopin and production vendors) materially shape audience experience and pricing; Zoom reported $4.39B revenue in fiscal 2024. Peak-demand windows compress supply and raise prices, while standardized formats and internal studios can cut external spend and reliance. Diversifying platforms reduces suppliers’ negotiation leverage and outage risk.

- Platform concentration: Zoom $4.39B FY2024

- Mitigation: internal studios, standard formats

- Strategy: multi-platform sourcing

Third-party research and syndication

Licensing analyst reports and benchmarks boosts TechTarget content relevance and engagement, but truly exclusive datasets are rare and command premium syndication fees, pressuring margins; building proprietary surveys over time lowers supplier dependence and captures first-party data while co-branded research deals balance cost-sharing with differentiation.

- Licensing increases appeal

- Exclusive data scarce/expensive

- Proprietary surveys reduce reliance

- Co-branding balances cost and uniqueness

Supplier power and cloud concentration lift pricing risk; AI drove 45%

Supplier power is high: niche tech journalists and exclusive datasets command 2–4x fees and lift switching costs; AI/cloud/cyber drove ~45% of enterprise content demand in 2024. Core infrastructure dependence is acute—AWS/Azure/GCP held ~68% IaaS/PaaS in 2024 and public cloud spend topped $600B—raising pricing and policy risks. Mitigants: in‑house studios, proprietary surveys, multi‑cloud and co‑branding reduce supplier leverage.

| Factor | 2024 Stat |

|---|---|

| Content demand concentration | ~45% |

| Top cloud share (AWS/Azure/GCP) | ~68% |

| Public cloud spend | $600B+ |

| Zoom revenue FY2024 | $4.39B |

What is included in the product

Tailored Porter's Five Forces analysis for TechTarget that uncovers competitive drivers, buyer and supplier power, substitutes, and entry risks, identifies disruptive threats and market dynamics affecting share and pricing, and delivers strategic insights ready for inclusion in investor materials or internal strategy decks.

TechTarget's Porter's Five Forces template delivers a clear one-sheet summary with customizable pressure levels and an instant spider chart, eliminating complex code and making it easy to drop into pitch decks, dashboards, or boardroom slides for faster, data-driven decisions.

Customers Bargaining Power

Tech vendors and agencies

Advertisers face many alternatives for lead-gen and brand spend, raising bargaining power as global digital ad spend topped roughly $600B in 2024 and channels compete on cost per lead. Budgets reallocate quickly toward lower-CPL, higher-ROI channels, while volume commitments secure discounts and custom packages. Demonstrable intent-data lifts, often producing double-digit increases in SQL conversion, temper pure price pressure.

Performance-driven procurement

Buyers now demand granular attribution, strict SLAs and make-goods, with pricing often tied to quality thresholds like MQL/SQL definitions, driving tougher negotiations and short cancellation windows (commonly 30–90 days). This performance-driven procurement compresses decision cycles and elevates enforcement of KPIs. Strong conversion metrics and vendor case studies—often showing multi-fold uplift—help vendors retain pricing power and reduce churn risk.

Consolidated enterprise accounts

Large global vendors drive significant revenue concentration at TechTarget; the company reported roughly $395 million in 2023 revenue, making top enterprise accounts materially important to pipeline health. Loss or pauses of a few consolidated accounts can swing quarterly bookings by millions, elevating short-term churn risk. Dedicated account management and multi-product bundles improve retention, and deeper cross-portfolio penetration dilutes single-buyer leverage.

Audience expectations (IT decision-makers)

IT decision-makers in 2024 demand unbiased, deep technical content and granular privacy controls; poor relevance reduces engagement and lead quality, indirectly empowering advertisers and partners. Compliance with GDPR and CCPA plus clear preference centers is mandatory. High trust reduces ad fatigue and improves conversion.

- 2024 Forrester: 69% of ITDMs prefer vendor-agnostic technical content

- GDPR/CCPA compliance required

- High trust lowers ad fatigue, boosts conversions

Cyclicality and macro sensitivity

IT marketing budgets swing with product cycles and macro conditions; Gartner forecast global IT spending around 5.1 trillion USD in 2024, heightening buyer leverage in slowdowns when buyers demand lower CPLs and flexible terms.

- Countercyclical lower-funnel intent preserves spend

- Diversified industry mix smooths volatility

Advertisers gain leverage as ~$600B digital ad market intensifies price and attribution pressure

Advertisers have high leverage as global digital ad spend reached ~$600B in 2024, driving price competition and CPL focus. Buyers demand granular attribution, SLAs and short cancellation windows, increasing negotiation pressure. TechTarget concentration (≈$395M revenue in 2023) means a few large accounts can swing bookings.

| Metric | Value |

|---|---|

| Global digital ad spend 2024 | ~$600B |

| TechTarget revenue 2023 | ~$395M |

| Global IT spend 2024 (Gartner) | $5.1T |

| Forrester ITDM preference | 69% |

Preview Before You Purchase

TechTarget Porter's Five Forces Analysis

The TechTarget Porter's Five Forces analysis evaluates competitive rivalry, threat of new entrants, bargaining power of buyers and suppliers, and threat of substitutes with data-driven insights and strategic implications. This preview is the exact, professionally formatted document you'll receive instantly after purchase—no placeholders or changes. It's ready for immediate download and use to inform strategy and investment decisions.