TECO Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

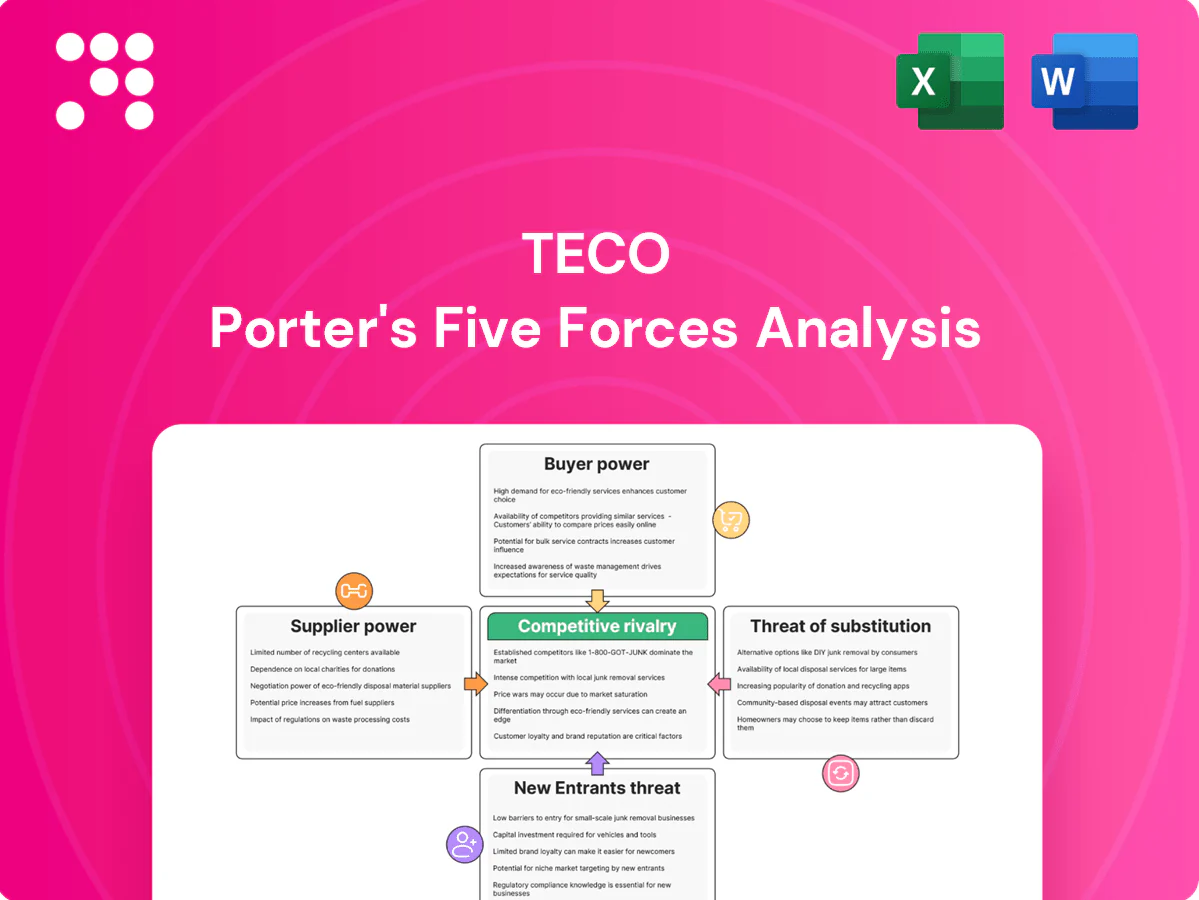

TECO faces moderate supplier power, rising competitive pressure, and evolving substitute risks that together shape its strategic outlook. This snapshot highlights key tensions but omits force-by-force ratings and visual evidence. Unlock the full Porter's Five Forces Analysis to see detailed ratings, scenarios, and strategic implications. Purchase the complete report for actionable, consultant-grade insights tailored to TECO.

Suppliers Bargaining Power

Semiconductor supplier concentration

Power electronics for motors and drives are sourced from a concentrated set of Tier-1 chipmakers such as Infineon, STMicro, ON Semiconductor and Wolfspeed, which raises supplier leverage. Allocation cycles and periodic lead-time spikes have squeezed margins and delayed inverter and automation deliveries. TECO mitigates risk via multi-vendor qualification, buffer inventory and long-term supply agreements, though substitution costs and suppliers’ technology roadmaps maintain supplier bargaining power.

Raw material volatility (copper, steel, magnets)

Copper windings, electrical steel and rare-earth magnets drive 40–60% of TECO’s material costs; LME copper averaged about USD 9,200/ton in 2024, GOES traded near EUR 1,500–1,800/ton and NdPr oxide averaged roughly USD 40/kg, creating pass-through risk as suppliers rapidly push price hikes unless contracts include indexation. Hedging and material-thrift design lower exposure but sustained spikes force repricing or erode margins on fixed-bid projects.

Standardized components vs proprietary parts

Where components are standardized (bearings, fasteners), TECO can dual-source and squeeze suppliers on price and lead times, lowering input risk; standardized SKUs often form the bulk of line items though a smaller share of BOM value. Proprietary high-efficiency motor and wind-subsystem parts raise supplier dependence and switching costs, amplified when 2024 supply-chain concentration keeps critical subassemblies near a few global suppliers. Design-for-supply and common platforms cut unique parts and restore leverage, while co-development improves performance but can lock TECO into higher switching costs.

Logistics, lead times, and regional footprint

Logistics constraints, elevated energy costs—Brent crude averaged about $87 per barrel in 2024—and regional port congestion heighten supplier bargaining during tight cycles, pressuring margins and lead times for TECO’s EPC contracts. TECO’s multi-region sourcing and nearshoring partially mitigate risk, while vendor-managed inventory strengthens negotiating leverage, yet time-sensitive EPC schedules magnify the impact of any supplier delays.

- Shipping constraints: elevated congestion increases delay risk

- Energy: Brent ~$87/bbl (2024) raises transport costs

- Resilience: multi-region sourcing + VMI improve stance

- Risk: EPC time-sensitivity amplifies supplier delays

Supplier innovation and co-engineering

Advanced materials and drives often originate with suppliers, giving them outsized influence on specifications and pricing; in 2024 many OEMs prioritized supplier co-engineering to secure early access. Joint R&D can improve performance but embeds dependency without firm IP and second-source contracts. Volume commitments can buy price concessions and allocation certainty in tight markets.

- Supplier influence: specification and price control

- Joint R&D: early access vs embedded dependency

- Mitigants: clear IP ownership and second-source plans

- Leverage: volume commitments for better terms

Concentrated suppliers raise bargaining power; manufacturers use multi-vendor, hedging, nearshoring

Suppliers of power electronics and critical materials (copper ~$9,200/t 2024, NdPr ~$40/kg, Brent ~$87/bbl) exert moderate-high bargaining power due to concentration and allocation spikes. TECO mitigates via multi-vendor qualification, long-term contracts, hedging and nearshoring, but proprietary parts and switching costs keep supplier leverage elevated.

| Item | 2024 | Impact |

|---|---|---|

| Copper | ~$9,200/t | Pass-through risk |

| NdPr oxide | ~$40/kg | Magnet cost driver |

| Brent | ~$87/bbl | Logistics cost |

| Tier‑1 chips | Concentrated | Allocation leverage |

What is included in the product

Tailored Porter's Five Forces analysis for TECO that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats to its market share. Includes strategic commentary identifying risks and opportunities to inform investor decks and internal strategy.

Compact TECO Porter's Five Forces one-sheet summarizing supplier, buyer, competitor, entrant and substitute pressures for rapid decision-making.

Customers Bargaining Power

Large OEMs, utilities, and EPCs

Large OEMs, utilities and EPCs place multi-year orders and use professional procurement teams to demand aggressive pricing and SLAs; in 2024 such enterprise contracts commonly secure over half of project volumes for industrial suppliers. Their scale heightens bargaining power, forcing TECO to compete on reliability, efficiency and lifecycle support to protect margins. Framework agreements stabilize volumes but typically compress prices and service margins.

Tender-driven, spec-heavy procurement

Tender-driven, spec-heavy procurement in ports is amplified by public procurement representing about 12% of OECD GDP in recent years, pushing buyers to prioritize compliance and lowest total cost and intensifying price competition. Standardized technical specs narrow differentiation and increase buyer leverage. TECO gains when it helps craft specs or delivers clear value-add beyond compliance, and prequalification requirements that limit bidders can partially offset buyer power.

Installed-base switching costs

Installed-base switching costs for motors, drives, and automation are high due to integration, spares, and training, and TECO’s strong aftermarket and digital monitoring—which industry reports in 2024 show expanding—raise exit barriers and soften buyer leverage; conversely, distributor-dominated channels lower switching friction and shift power to buyers, so ensuring backward compatibility keeps TECO embedded.

Total cost of ownership focus

Industrial buyers weigh efficiency (IE3/IE4), uptime, and maintenance alongside capex. TECO can command premiums if it proves TCO gains via energy savings and predictive maintenance, with 2024 industry data showing predictive maintenance cuts maintenance costs 20–40% and unplanned downtime up to 50%. Documented ROI reduces price-only negotiations; service bundles and warranties shift focus from upfront price.

- Efficiency: IE3/IE4 matter for energy spend

- Maintenance: −20–40% cost with predictive maintenance (2024)

- ROI proof reduces price pressure

- Service bundles/warranties tilt conversations away from capex

Demand cyclicality and inventory dynamics

Demand cyclicality in construction, manufacturing and renewables swings volumes and buyer leverage; in downturns buyers commonly push harder on pricing and extend payment terms 30–90 days.

In tight markets availability and delivery speed reduce buyer power; TECO’s backlog visibility and flexible capacity help limit concessions and preserve margins.

- Downturns: extended payment terms 30–90 days

- Tight market: delivery speed shifts leverage to supplier

- TECO: backlog visibility + flexible capacity = concession control

OEMs grab >50% projects; PdM cuts maintenance 20–40%, downtime 50%

Large OEMs/utilities secure >50% of 2024 project volumes, driving aggressive pricing and SLA demands; public procurement (~12% of OECD GDP) intensifies price-focused tenders. Predictive maintenance in 2024 cuts maintenance 20–40% and unplanned downtime up to 50%, enabling TECO to command TCO premiums. Downturns push payment terms 30–90 days; tight markets shift leverage to suppliers.

| Metric | 2024 Value |

|---|---|

| Enterprise contract volume | >50% |

| Public procurement | ~12% OECD GDP |

| Predictive maintenance impact | −20–40% maintenance; −50% downtime |

| Payment terms (downturn) | 30–90 days |

Same Document Delivered

TECO Porter's Five Forces Analysis

This preview shows the exact TECO Porter’s Five Forces analysis you’ll receive—comprehensive, professionally formatted, and ready for immediate use. It covers competitive rivalry, supplier and buyer power, threat of entry and substitutes, plus strategic implications. No placeholders, no changes—instant download after purchase.

Go Beyond the Preview—Access the Full Strategic Report

TECO faces moderate supplier power, rising competitive pressure, and evolving substitute risks that together shape its strategic outlook. This snapshot highlights key tensions but omits force-by-force ratings and visual evidence. Unlock the full Porter's Five Forces Analysis to see detailed ratings, scenarios, and strategic implications. Purchase the complete report for actionable, consultant-grade insights tailored to TECO.

Suppliers Bargaining Power

Semiconductor supplier concentration

Power electronics for motors and drives are sourced from a concentrated set of Tier-1 chipmakers such as Infineon, STMicro, ON Semiconductor and Wolfspeed, which raises supplier leverage. Allocation cycles and periodic lead-time spikes have squeezed margins and delayed inverter and automation deliveries. TECO mitigates risk via multi-vendor qualification, buffer inventory and long-term supply agreements, though substitution costs and suppliers’ technology roadmaps maintain supplier bargaining power.

Raw material volatility (copper, steel, magnets)

Copper windings, electrical steel and rare-earth magnets drive 40–60% of TECO’s material costs; LME copper averaged about USD 9,200/ton in 2024, GOES traded near EUR 1,500–1,800/ton and NdPr oxide averaged roughly USD 40/kg, creating pass-through risk as suppliers rapidly push price hikes unless contracts include indexation. Hedging and material-thrift design lower exposure but sustained spikes force repricing or erode margins on fixed-bid projects.

Standardized components vs proprietary parts

Where components are standardized (bearings, fasteners), TECO can dual-source and squeeze suppliers on price and lead times, lowering input risk; standardized SKUs often form the bulk of line items though a smaller share of BOM value. Proprietary high-efficiency motor and wind-subsystem parts raise supplier dependence and switching costs, amplified when 2024 supply-chain concentration keeps critical subassemblies near a few global suppliers. Design-for-supply and common platforms cut unique parts and restore leverage, while co-development improves performance but can lock TECO into higher switching costs.

Logistics, lead times, and regional footprint

Logistics constraints, elevated energy costs—Brent crude averaged about $87 per barrel in 2024—and regional port congestion heighten supplier bargaining during tight cycles, pressuring margins and lead times for TECO’s EPC contracts. TECO’s multi-region sourcing and nearshoring partially mitigate risk, while vendor-managed inventory strengthens negotiating leverage, yet time-sensitive EPC schedules magnify the impact of any supplier delays.

- Shipping constraints: elevated congestion increases delay risk

- Energy: Brent ~$87/bbl (2024) raises transport costs

- Resilience: multi-region sourcing + VMI improve stance

- Risk: EPC time-sensitivity amplifies supplier delays

Supplier innovation and co-engineering

Advanced materials and drives often originate with suppliers, giving them outsized influence on specifications and pricing; in 2024 many OEMs prioritized supplier co-engineering to secure early access. Joint R&D can improve performance but embeds dependency without firm IP and second-source contracts. Volume commitments can buy price concessions and allocation certainty in tight markets.

- Supplier influence: specification and price control

- Joint R&D: early access vs embedded dependency

- Mitigants: clear IP ownership and second-source plans

- Leverage: volume commitments for better terms

Concentrated suppliers raise bargaining power; manufacturers use multi-vendor, hedging, nearshoring

Suppliers of power electronics and critical materials (copper ~$9,200/t 2024, NdPr ~$40/kg, Brent ~$87/bbl) exert moderate-high bargaining power due to concentration and allocation spikes. TECO mitigates via multi-vendor qualification, long-term contracts, hedging and nearshoring, but proprietary parts and switching costs keep supplier leverage elevated.

| Item | 2024 | Impact |

|---|---|---|

| Copper | ~$9,200/t | Pass-through risk |

| NdPr oxide | ~$40/kg | Magnet cost driver |

| Brent | ~$87/bbl | Logistics cost |

| Tier‑1 chips | Concentrated | Allocation leverage |

What is included in the product

Tailored Porter's Five Forces analysis for TECO that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats to its market share. Includes strategic commentary identifying risks and opportunities to inform investor decks and internal strategy.

Compact TECO Porter's Five Forces one-sheet summarizing supplier, buyer, competitor, entrant and substitute pressures for rapid decision-making.

Customers Bargaining Power

Large OEMs, utilities, and EPCs

Large OEMs, utilities and EPCs place multi-year orders and use professional procurement teams to demand aggressive pricing and SLAs; in 2024 such enterprise contracts commonly secure over half of project volumes for industrial suppliers. Their scale heightens bargaining power, forcing TECO to compete on reliability, efficiency and lifecycle support to protect margins. Framework agreements stabilize volumes but typically compress prices and service margins.

Tender-driven, spec-heavy procurement

Tender-driven, spec-heavy procurement in ports is amplified by public procurement representing about 12% of OECD GDP in recent years, pushing buyers to prioritize compliance and lowest total cost and intensifying price competition. Standardized technical specs narrow differentiation and increase buyer leverage. TECO gains when it helps craft specs or delivers clear value-add beyond compliance, and prequalification requirements that limit bidders can partially offset buyer power.

Installed-base switching costs

Installed-base switching costs for motors, drives, and automation are high due to integration, spares, and training, and TECO’s strong aftermarket and digital monitoring—which industry reports in 2024 show expanding—raise exit barriers and soften buyer leverage; conversely, distributor-dominated channels lower switching friction and shift power to buyers, so ensuring backward compatibility keeps TECO embedded.

Total cost of ownership focus

Industrial buyers weigh efficiency (IE3/IE4), uptime, and maintenance alongside capex. TECO can command premiums if it proves TCO gains via energy savings and predictive maintenance, with 2024 industry data showing predictive maintenance cuts maintenance costs 20–40% and unplanned downtime up to 50%. Documented ROI reduces price-only negotiations; service bundles and warranties shift focus from upfront price.

- Efficiency: IE3/IE4 matter for energy spend

- Maintenance: −20–40% cost with predictive maintenance (2024)

- ROI proof reduces price pressure

- Service bundles/warranties tilt conversations away from capex

Demand cyclicality and inventory dynamics

Demand cyclicality in construction, manufacturing and renewables swings volumes and buyer leverage; in downturns buyers commonly push harder on pricing and extend payment terms 30–90 days.

In tight markets availability and delivery speed reduce buyer power; TECO’s backlog visibility and flexible capacity help limit concessions and preserve margins.

- Downturns: extended payment terms 30–90 days

- Tight market: delivery speed shifts leverage to supplier

- TECO: backlog visibility + flexible capacity = concession control

OEMs grab >50% projects; PdM cuts maintenance 20–40%, downtime 50%

Large OEMs/utilities secure >50% of 2024 project volumes, driving aggressive pricing and SLA demands; public procurement (~12% of OECD GDP) intensifies price-focused tenders. Predictive maintenance in 2024 cuts maintenance 20–40% and unplanned downtime up to 50%, enabling TECO to command TCO premiums. Downturns push payment terms 30–90 days; tight markets shift leverage to suppliers.

| Metric | 2024 Value |

|---|---|

| Enterprise contract volume | >50% |

| Public procurement | ~12% OECD GDP |

| Predictive maintenance impact | −20–40% maintenance; −50% downtime |

| Payment terms (downturn) | 30–90 days |

Same Document Delivered

TECO Porter's Five Forces Analysis

This preview shows the exact TECO Porter’s Five Forces analysis you’ll receive—comprehensive, professionally formatted, and ready for immediate use. It covers competitive rivalry, supplier and buyer power, threat of entry and substitutes, plus strategic implications. No placeholders, no changes—instant download after purchase.

Description

Go Beyond the Preview—Access the Full Strategic Report

TECO faces moderate supplier power, rising competitive pressure, and evolving substitute risks that together shape its strategic outlook. This snapshot highlights key tensions but omits force-by-force ratings and visual evidence. Unlock the full Porter's Five Forces Analysis to see detailed ratings, scenarios, and strategic implications. Purchase the complete report for actionable, consultant-grade insights tailored to TECO.

Suppliers Bargaining Power

Semiconductor supplier concentration

Power electronics for motors and drives are sourced from a concentrated set of Tier-1 chipmakers such as Infineon, STMicro, ON Semiconductor and Wolfspeed, which raises supplier leverage. Allocation cycles and periodic lead-time spikes have squeezed margins and delayed inverter and automation deliveries. TECO mitigates risk via multi-vendor qualification, buffer inventory and long-term supply agreements, though substitution costs and suppliers’ technology roadmaps maintain supplier bargaining power.

Raw material volatility (copper, steel, magnets)

Copper windings, electrical steel and rare-earth magnets drive 40–60% of TECO’s material costs; LME copper averaged about USD 9,200/ton in 2024, GOES traded near EUR 1,500–1,800/ton and NdPr oxide averaged roughly USD 40/kg, creating pass-through risk as suppliers rapidly push price hikes unless contracts include indexation. Hedging and material-thrift design lower exposure but sustained spikes force repricing or erode margins on fixed-bid projects.

Standardized components vs proprietary parts

Where components are standardized (bearings, fasteners), TECO can dual-source and squeeze suppliers on price and lead times, lowering input risk; standardized SKUs often form the bulk of line items though a smaller share of BOM value. Proprietary high-efficiency motor and wind-subsystem parts raise supplier dependence and switching costs, amplified when 2024 supply-chain concentration keeps critical subassemblies near a few global suppliers. Design-for-supply and common platforms cut unique parts and restore leverage, while co-development improves performance but can lock TECO into higher switching costs.

Logistics, lead times, and regional footprint

Logistics constraints, elevated energy costs—Brent crude averaged about $87 per barrel in 2024—and regional port congestion heighten supplier bargaining during tight cycles, pressuring margins and lead times for TECO’s EPC contracts. TECO’s multi-region sourcing and nearshoring partially mitigate risk, while vendor-managed inventory strengthens negotiating leverage, yet time-sensitive EPC schedules magnify the impact of any supplier delays.

- Shipping constraints: elevated congestion increases delay risk

- Energy: Brent ~$87/bbl (2024) raises transport costs

- Resilience: multi-region sourcing + VMI improve stance

- Risk: EPC time-sensitivity amplifies supplier delays

Supplier innovation and co-engineering

Advanced materials and drives often originate with suppliers, giving them outsized influence on specifications and pricing; in 2024 many OEMs prioritized supplier co-engineering to secure early access. Joint R&D can improve performance but embeds dependency without firm IP and second-source contracts. Volume commitments can buy price concessions and allocation certainty in tight markets.

- Supplier influence: specification and price control

- Joint R&D: early access vs embedded dependency

- Mitigants: clear IP ownership and second-source plans

- Leverage: volume commitments for better terms

Concentrated suppliers raise bargaining power; manufacturers use multi-vendor, hedging, nearshoring

Suppliers of power electronics and critical materials (copper ~$9,200/t 2024, NdPr ~$40/kg, Brent ~$87/bbl) exert moderate-high bargaining power due to concentration and allocation spikes. TECO mitigates via multi-vendor qualification, long-term contracts, hedging and nearshoring, but proprietary parts and switching costs keep supplier leverage elevated.

| Item | 2024 | Impact |

|---|---|---|

| Copper | ~$9,200/t | Pass-through risk |

| NdPr oxide | ~$40/kg | Magnet cost driver |

| Brent | ~$87/bbl | Logistics cost |

| Tier‑1 chips | Concentrated | Allocation leverage |

What is included in the product

Tailored Porter's Five Forces analysis for TECO that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats to its market share. Includes strategic commentary identifying risks and opportunities to inform investor decks and internal strategy.

Compact TECO Porter's Five Forces one-sheet summarizing supplier, buyer, competitor, entrant and substitute pressures for rapid decision-making.

Customers Bargaining Power

Large OEMs, utilities, and EPCs

Large OEMs, utilities and EPCs place multi-year orders and use professional procurement teams to demand aggressive pricing and SLAs; in 2024 such enterprise contracts commonly secure over half of project volumes for industrial suppliers. Their scale heightens bargaining power, forcing TECO to compete on reliability, efficiency and lifecycle support to protect margins. Framework agreements stabilize volumes but typically compress prices and service margins.

Tender-driven, spec-heavy procurement

Tender-driven, spec-heavy procurement in ports is amplified by public procurement representing about 12% of OECD GDP in recent years, pushing buyers to prioritize compliance and lowest total cost and intensifying price competition. Standardized technical specs narrow differentiation and increase buyer leverage. TECO gains when it helps craft specs or delivers clear value-add beyond compliance, and prequalification requirements that limit bidders can partially offset buyer power.

Installed-base switching costs

Installed-base switching costs for motors, drives, and automation are high due to integration, spares, and training, and TECO’s strong aftermarket and digital monitoring—which industry reports in 2024 show expanding—raise exit barriers and soften buyer leverage; conversely, distributor-dominated channels lower switching friction and shift power to buyers, so ensuring backward compatibility keeps TECO embedded.

Total cost of ownership focus

Industrial buyers weigh efficiency (IE3/IE4), uptime, and maintenance alongside capex. TECO can command premiums if it proves TCO gains via energy savings and predictive maintenance, with 2024 industry data showing predictive maintenance cuts maintenance costs 20–40% and unplanned downtime up to 50%. Documented ROI reduces price-only negotiations; service bundles and warranties shift focus from upfront price.

- Efficiency: IE3/IE4 matter for energy spend

- Maintenance: −20–40% cost with predictive maintenance (2024)

- ROI proof reduces price pressure

- Service bundles/warranties tilt conversations away from capex

Demand cyclicality and inventory dynamics

Demand cyclicality in construction, manufacturing and renewables swings volumes and buyer leverage; in downturns buyers commonly push harder on pricing and extend payment terms 30–90 days.

In tight markets availability and delivery speed reduce buyer power; TECO’s backlog visibility and flexible capacity help limit concessions and preserve margins.

- Downturns: extended payment terms 30–90 days

- Tight market: delivery speed shifts leverage to supplier

- TECO: backlog visibility + flexible capacity = concession control

OEMs grab >50% projects; PdM cuts maintenance 20–40%, downtime 50%

Large OEMs/utilities secure >50% of 2024 project volumes, driving aggressive pricing and SLA demands; public procurement (~12% of OECD GDP) intensifies price-focused tenders. Predictive maintenance in 2024 cuts maintenance 20–40% and unplanned downtime up to 50%, enabling TECO to command TCO premiums. Downturns push payment terms 30–90 days; tight markets shift leverage to suppliers.

| Metric | 2024 Value |

|---|---|

| Enterprise contract volume | >50% |

| Public procurement | ~12% OECD GDP |

| Predictive maintenance impact | −20–40% maintenance; −50% downtime |

| Payment terms (downturn) | 30–90 days |

Same Document Delivered

TECO Porter's Five Forces Analysis

This preview shows the exact TECO Porter’s Five Forces analysis you’ll receive—comprehensive, professionally formatted, and ready for immediate use. It covers competitive rivalry, supplier and buyer power, threat of entry and substitutes, plus strategic implications. No placeholders, no changes—instant download after purchase.