Telefónica Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

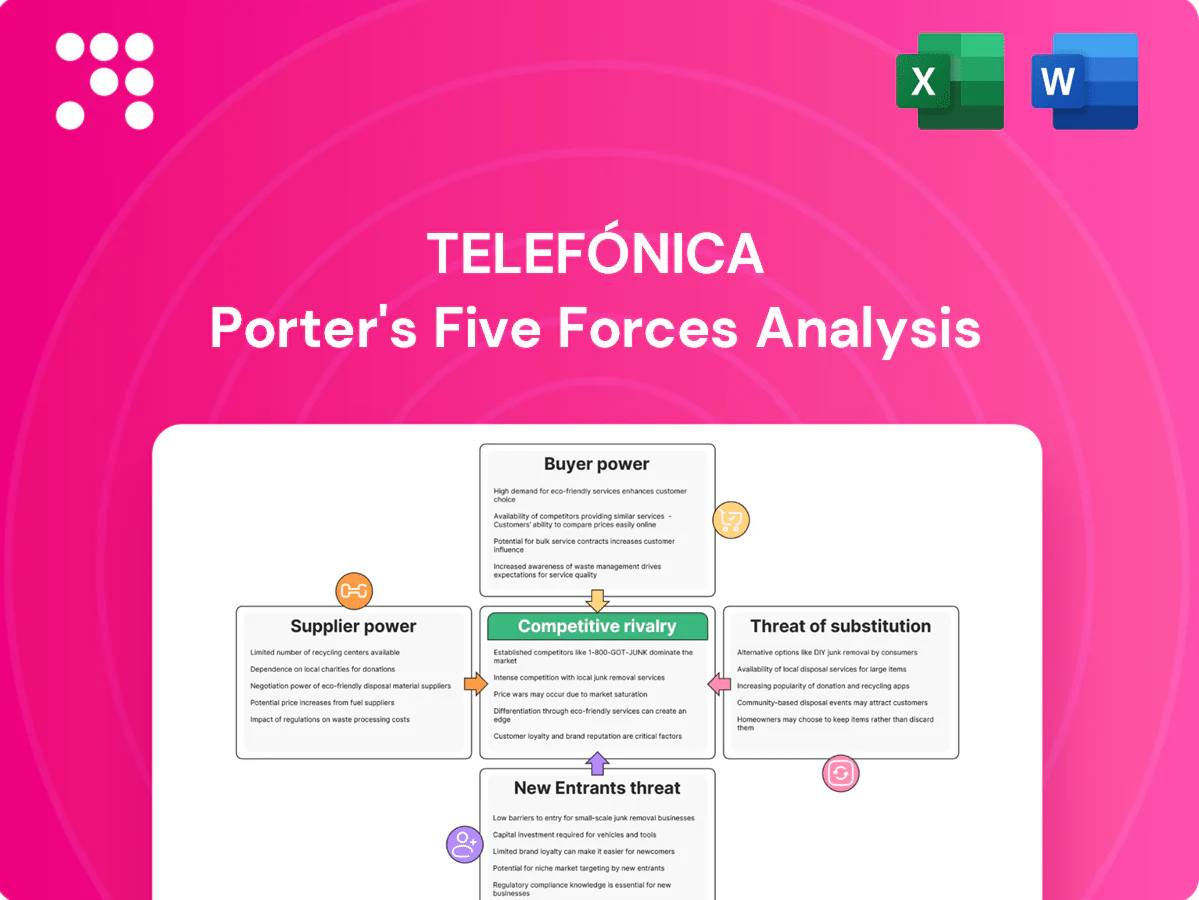

Telefónica navigates high competitive rivalry, moderate supplier power, and rising substitute threats as digital services reshape telecom margins. Regulatory pressure and capital intensity limit new entrants but amplify incumbents' strategic importance. Buyer demand for bundled, low-cost offerings increases margin pressure, while spectrum and infrastructure needs keep barriers high. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Telefónica’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated network vendors

Radio, core and transport gear is sourced from a few large OEMs—Ericsson, Nokia and Huawei—who together account for roughly 80% of the global RAN market, concentrating supplier leverage. Limited alternatives in specific technologies can raise costs and reduce bargaining flexibility. Telefónica mitigates risk via multi-vendor deployments, standardized interfaces and Open RAN pilots, but vendor lock-in remains a concern in critical network layers.

Spectrum and regulatory dependence

Spectrum for 700 MHz, 3.4–3.8 GHz and 26 GHz is government‑allocated, creating non‑negotiable, high‑cost inputs for Telefónica. Auction designs and license obligations (typically 10–20 year terms) shape upfront cash demands and multi‑year investment timelines. Renewal risks, recurring fees and policy shifts across markets materially influence margins and Telefónica’s pricing power.

Tower, fiber, and data center landlords

Independent towercos and wholesale fiber/data‑center landlords can push pricing where coverage is sparse; long‑term leases—typically 10+ years with annual escalators around 1–3%—reduce Telefónica’s short‑term flexibility. Telefónica began infrastructure carve‑outs and partnerships (eg Telxius spin‑off from 2016–17) to rebalance supplier power. Local market density and available asset alternatives ultimately set landlord leverage.

Content and OTT partners

IT, cloud, and software ecosystems

Core IT stacks, BSS/OSS and cloud services create high switching costs—migration and re‑integration can consume 5–15% of annual IT spend—and proprietary platforms amplify vendor power and integration complexity. In 2024 the global cloud market reached ~600bn USD with AWS ~32%, Azure ~22%, GCP ~10%, concentrating supplier leverage. Adoption of open standards and cloud‑native architectures and strategic co‑innovation deals can reduce lock‑in but often trade margin for speed and capability.

- 5–15%: typical migration cost of annual IT spend

- 600bn USD: 2024 cloud market size

- AWS 32% / Azure 22% / GCP 10%: 2024 market shares

- Co‑innovation: margin concession for faster capability

Concentrated RAN suppliers (~80%), dominant cloud share, locked-in spectrum costs

Telefónica faces concentrated supplier power in RAN (Ericsson/Nokia/Huawei ≈80% share), cloud (2024 market ≈600bn USD; AWS 32%/Azure 22%/GCP 10%) and premium content, while spectrum auctions (licenses 10–20y) and tower landlords impose non‑negotiable costs. Multi‑vendor, Open RAN and asset carve‑outs reduce but do not eliminate lock‑in and switching costs (IT migrations ~5–15%).

| Metric | Value |

|---|---|

| RAN concentration | ~80% |

| Cloud market 2024 | ~600bn USD |

| AWS/Azure/GCP | 32% / 22% / 10% |

| IT migration cost | 5–15% of annual IT spend |

| Spectrum license term | 10–20 years |

What is included in the product

Tailored Porter's Five Forces analysis of Telefónica uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and disruptive technologies—evaluating how these forces shape pricing, profitability, market entry risks and strategic defenses; fully editable for use in investor materials, strategy decks, or academic projects.

One-sheet Telefónica Porter's Five Forces summary that instantly visualizes competitive pressure with a spider chart and customizable levels—perfect for rapid deck-ready decisions; no macros, easy data swaps, and seamless integration into broader Excel dashboards for quick boardroom clarity.

Customers Bargaining Power

Price-sensitive mass market

Residential customers in Europe and Latin America are highly price-aware, driving Telefónica into frequent promotional cycles that lower effective prices and expectations of discounts. Prepaid penetration in Latin America remained around 60% in 2024, amplifying sensitivity to downgrades during economic downturns. These dynamics compress ARPU and force higher retention spending to curb churn, increasing unit-level customer economics pressure.

High churn and portability

Number portability, typically completed within one working day in the EU, lowers switching frictions and raises subscriber mobility. High annual churn rates in mobile markets (often 20–30%) force Telefónica into aggressive win-back and loyalty spending. Service parity in mature markets narrows differentiation, while network quality and coverage remain key levers to moderate buyer power.

Enterprise procurement strength

Large corporates run competitive RFPs across multiple carriers, forcing Telefónica to compete on price and SLAs in lengthy procurement cycles; multi-year, multi-country contracts routinely secure double-digit volume commitments. Managed services and security add-ons widen scope but face tight benchmarking and margin compression. Telefónica’s scale — €35.1bn revenue in 2024 and operations across 11 markets — helps offset some negotiating pressure.

Bundling dampens leverage

Convergent quad-play bundles raise switching costs for households, with Telefónica reporting over 300 million retail accesses by 2024 that deepen household ties; device financing and family plans (device-financing penetration ~30% in many EU markets) add stickiness, while integrated billing and loyalty programs lower buyer power, though rival operators replicating bundles in 2023–24 caps structural advantage.

- Quad-play increases churn resistance

- Device financing boosts ARPU and retention

- Integrated billing reduces buyer negotiating power

- Competitor copycats limit long-term leverage

Quality and experience differentiation

Network performance, coverage and customer service drive willingness to pay; Telefónica in 2024 emphasized FTTH and 5G rollouts to lock in value and limit buyer leverage. Superior fiber and 5G availability reduce price sensitivity, while transparent plans and digital self-service raise retention. In competitive cities, poor experiences rapidly convert into churn.

- Coverage parity reduces bargaining

- Digital service boosts NPS and retention

- Service failures => fast churn in urban markets

Prepaid ~60% LATAM, 20-30% churn cut ARPU; scale + FTTH/5G raise switching costs

Strong price sensitivity (prepaid ~60% in LATAM) and high mobile churn (20–30% p.a.) boost customer bargaining, compress ARPU and raise retention spend; Telefónica’s scale (€35.1bn revenue in 2024) + 300m retail accesses and quad-play/device financing (~30% EU) raise switching costs, while network (FTTH/5G) investments limit buyer leverage.

| Metric | 2024 |

|---|---|

| Revenue | €35.1bn |

| Retail accesses | 300m |

| Prepaid LATAM | ~60% |

| Mobile churn | 20–30% p.a. |

| Device finance EU | ~30% |

Same Document Delivered

Telefónica Porter's Five Forces Analysis

This Telefónica Porter's Five Forces Analysis preview is the exact, fully formatted document you will receive immediately after purchase, containing a complete assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. No placeholders or samples—what you see is ready for download and use. Instant access on payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Telefónica navigates high competitive rivalry, moderate supplier power, and rising substitute threats as digital services reshape telecom margins. Regulatory pressure and capital intensity limit new entrants but amplify incumbents' strategic importance. Buyer demand for bundled, low-cost offerings increases margin pressure, while spectrum and infrastructure needs keep barriers high. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Telefónica’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated network vendors

Radio, core and transport gear is sourced from a few large OEMs—Ericsson, Nokia and Huawei—who together account for roughly 80% of the global RAN market, concentrating supplier leverage. Limited alternatives in specific technologies can raise costs and reduce bargaining flexibility. Telefónica mitigates risk via multi-vendor deployments, standardized interfaces and Open RAN pilots, but vendor lock-in remains a concern in critical network layers.

Spectrum and regulatory dependence

Spectrum for 700 MHz, 3.4–3.8 GHz and 26 GHz is government‑allocated, creating non‑negotiable, high‑cost inputs for Telefónica. Auction designs and license obligations (typically 10–20 year terms) shape upfront cash demands and multi‑year investment timelines. Renewal risks, recurring fees and policy shifts across markets materially influence margins and Telefónica’s pricing power.

Tower, fiber, and data center landlords

Independent towercos and wholesale fiber/data‑center landlords can push pricing where coverage is sparse; long‑term leases—typically 10+ years with annual escalators around 1–3%—reduce Telefónica’s short‑term flexibility. Telefónica began infrastructure carve‑outs and partnerships (eg Telxius spin‑off from 2016–17) to rebalance supplier power. Local market density and available asset alternatives ultimately set landlord leverage.

Content and OTT partners

IT, cloud, and software ecosystems

Core IT stacks, BSS/OSS and cloud services create high switching costs—migration and re‑integration can consume 5–15% of annual IT spend—and proprietary platforms amplify vendor power and integration complexity. In 2024 the global cloud market reached ~600bn USD with AWS ~32%, Azure ~22%, GCP ~10%, concentrating supplier leverage. Adoption of open standards and cloud‑native architectures and strategic co‑innovation deals can reduce lock‑in but often trade margin for speed and capability.

- 5–15%: typical migration cost of annual IT spend

- 600bn USD: 2024 cloud market size

- AWS 32% / Azure 22% / GCP 10%: 2024 market shares

- Co‑innovation: margin concession for faster capability

Concentrated RAN suppliers (~80%), dominant cloud share, locked-in spectrum costs

Telefónica faces concentrated supplier power in RAN (Ericsson/Nokia/Huawei ≈80% share), cloud (2024 market ≈600bn USD; AWS 32%/Azure 22%/GCP 10%) and premium content, while spectrum auctions (licenses 10–20y) and tower landlords impose non‑negotiable costs. Multi‑vendor, Open RAN and asset carve‑outs reduce but do not eliminate lock‑in and switching costs (IT migrations ~5–15%).

| Metric | Value |

|---|---|

| RAN concentration | ~80% |

| Cloud market 2024 | ~600bn USD |

| AWS/Azure/GCP | 32% / 22% / 10% |

| IT migration cost | 5–15% of annual IT spend |

| Spectrum license term | 10–20 years |

What is included in the product

Tailored Porter's Five Forces analysis of Telefónica uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and disruptive technologies—evaluating how these forces shape pricing, profitability, market entry risks and strategic defenses; fully editable for use in investor materials, strategy decks, or academic projects.

One-sheet Telefónica Porter's Five Forces summary that instantly visualizes competitive pressure with a spider chart and customizable levels—perfect for rapid deck-ready decisions; no macros, easy data swaps, and seamless integration into broader Excel dashboards for quick boardroom clarity.

Customers Bargaining Power

Price-sensitive mass market

Residential customers in Europe and Latin America are highly price-aware, driving Telefónica into frequent promotional cycles that lower effective prices and expectations of discounts. Prepaid penetration in Latin America remained around 60% in 2024, amplifying sensitivity to downgrades during economic downturns. These dynamics compress ARPU and force higher retention spending to curb churn, increasing unit-level customer economics pressure.

High churn and portability

Number portability, typically completed within one working day in the EU, lowers switching frictions and raises subscriber mobility. High annual churn rates in mobile markets (often 20–30%) force Telefónica into aggressive win-back and loyalty spending. Service parity in mature markets narrows differentiation, while network quality and coverage remain key levers to moderate buyer power.

Enterprise procurement strength

Large corporates run competitive RFPs across multiple carriers, forcing Telefónica to compete on price and SLAs in lengthy procurement cycles; multi-year, multi-country contracts routinely secure double-digit volume commitments. Managed services and security add-ons widen scope but face tight benchmarking and margin compression. Telefónica’s scale — €35.1bn revenue in 2024 and operations across 11 markets — helps offset some negotiating pressure.

Bundling dampens leverage

Convergent quad-play bundles raise switching costs for households, with Telefónica reporting over 300 million retail accesses by 2024 that deepen household ties; device financing and family plans (device-financing penetration ~30% in many EU markets) add stickiness, while integrated billing and loyalty programs lower buyer power, though rival operators replicating bundles in 2023–24 caps structural advantage.

- Quad-play increases churn resistance

- Device financing boosts ARPU and retention

- Integrated billing reduces buyer negotiating power

- Competitor copycats limit long-term leverage

Quality and experience differentiation

Network performance, coverage and customer service drive willingness to pay; Telefónica in 2024 emphasized FTTH and 5G rollouts to lock in value and limit buyer leverage. Superior fiber and 5G availability reduce price sensitivity, while transparent plans and digital self-service raise retention. In competitive cities, poor experiences rapidly convert into churn.

- Coverage parity reduces bargaining

- Digital service boosts NPS and retention

- Service failures => fast churn in urban markets

Prepaid ~60% LATAM, 20-30% churn cut ARPU; scale + FTTH/5G raise switching costs

Strong price sensitivity (prepaid ~60% in LATAM) and high mobile churn (20–30% p.a.) boost customer bargaining, compress ARPU and raise retention spend; Telefónica’s scale (€35.1bn revenue in 2024) + 300m retail accesses and quad-play/device financing (~30% EU) raise switching costs, while network (FTTH/5G) investments limit buyer leverage.

| Metric | 2024 |

|---|---|

| Revenue | €35.1bn |

| Retail accesses | 300m |

| Prepaid LATAM | ~60% |

| Mobile churn | 20–30% p.a. |

| Device finance EU | ~30% |

Same Document Delivered

Telefónica Porter's Five Forces Analysis

This Telefónica Porter's Five Forces Analysis preview is the exact, fully formatted document you will receive immediately after purchase, containing a complete assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. No placeholders or samples—what you see is ready for download and use. Instant access on payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Telefónica navigates high competitive rivalry, moderate supplier power, and rising substitute threats as digital services reshape telecom margins. Regulatory pressure and capital intensity limit new entrants but amplify incumbents' strategic importance. Buyer demand for bundled, low-cost offerings increases margin pressure, while spectrum and infrastructure needs keep barriers high. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Telefónica’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated network vendors

Radio, core and transport gear is sourced from a few large OEMs—Ericsson, Nokia and Huawei—who together account for roughly 80% of the global RAN market, concentrating supplier leverage. Limited alternatives in specific technologies can raise costs and reduce bargaining flexibility. Telefónica mitigates risk via multi-vendor deployments, standardized interfaces and Open RAN pilots, but vendor lock-in remains a concern in critical network layers.

Spectrum and regulatory dependence

Spectrum for 700 MHz, 3.4–3.8 GHz and 26 GHz is government‑allocated, creating non‑negotiable, high‑cost inputs for Telefónica. Auction designs and license obligations (typically 10–20 year terms) shape upfront cash demands and multi‑year investment timelines. Renewal risks, recurring fees and policy shifts across markets materially influence margins and Telefónica’s pricing power.

Tower, fiber, and data center landlords

Independent towercos and wholesale fiber/data‑center landlords can push pricing where coverage is sparse; long‑term leases—typically 10+ years with annual escalators around 1–3%—reduce Telefónica’s short‑term flexibility. Telefónica began infrastructure carve‑outs and partnerships (eg Telxius spin‑off from 2016–17) to rebalance supplier power. Local market density and available asset alternatives ultimately set landlord leverage.

Content and OTT partners

IT, cloud, and software ecosystems

Core IT stacks, BSS/OSS and cloud services create high switching costs—migration and re‑integration can consume 5–15% of annual IT spend—and proprietary platforms amplify vendor power and integration complexity. In 2024 the global cloud market reached ~600bn USD with AWS ~32%, Azure ~22%, GCP ~10%, concentrating supplier leverage. Adoption of open standards and cloud‑native architectures and strategic co‑innovation deals can reduce lock‑in but often trade margin for speed and capability.

- 5–15%: typical migration cost of annual IT spend

- 600bn USD: 2024 cloud market size

- AWS 32% / Azure 22% / GCP 10%: 2024 market shares

- Co‑innovation: margin concession for faster capability

Concentrated RAN suppliers (~80%), dominant cloud share, locked-in spectrum costs

Telefónica faces concentrated supplier power in RAN (Ericsson/Nokia/Huawei ≈80% share), cloud (2024 market ≈600bn USD; AWS 32%/Azure 22%/GCP 10%) and premium content, while spectrum auctions (licenses 10–20y) and tower landlords impose non‑negotiable costs. Multi‑vendor, Open RAN and asset carve‑outs reduce but do not eliminate lock‑in and switching costs (IT migrations ~5–15%).

| Metric | Value |

|---|---|

| RAN concentration | ~80% |

| Cloud market 2024 | ~600bn USD |

| AWS/Azure/GCP | 32% / 22% / 10% |

| IT migration cost | 5–15% of annual IT spend |

| Spectrum license term | 10–20 years |

What is included in the product

Tailored Porter's Five Forces analysis of Telefónica uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and disruptive technologies—evaluating how these forces shape pricing, profitability, market entry risks and strategic defenses; fully editable for use in investor materials, strategy decks, or academic projects.

One-sheet Telefónica Porter's Five Forces summary that instantly visualizes competitive pressure with a spider chart and customizable levels—perfect for rapid deck-ready decisions; no macros, easy data swaps, and seamless integration into broader Excel dashboards for quick boardroom clarity.

Customers Bargaining Power

Price-sensitive mass market

Residential customers in Europe and Latin America are highly price-aware, driving Telefónica into frequent promotional cycles that lower effective prices and expectations of discounts. Prepaid penetration in Latin America remained around 60% in 2024, amplifying sensitivity to downgrades during economic downturns. These dynamics compress ARPU and force higher retention spending to curb churn, increasing unit-level customer economics pressure.

High churn and portability

Number portability, typically completed within one working day in the EU, lowers switching frictions and raises subscriber mobility. High annual churn rates in mobile markets (often 20–30%) force Telefónica into aggressive win-back and loyalty spending. Service parity in mature markets narrows differentiation, while network quality and coverage remain key levers to moderate buyer power.

Enterprise procurement strength

Large corporates run competitive RFPs across multiple carriers, forcing Telefónica to compete on price and SLAs in lengthy procurement cycles; multi-year, multi-country contracts routinely secure double-digit volume commitments. Managed services and security add-ons widen scope but face tight benchmarking and margin compression. Telefónica’s scale — €35.1bn revenue in 2024 and operations across 11 markets — helps offset some negotiating pressure.

Bundling dampens leverage

Convergent quad-play bundles raise switching costs for households, with Telefónica reporting over 300 million retail accesses by 2024 that deepen household ties; device financing and family plans (device-financing penetration ~30% in many EU markets) add stickiness, while integrated billing and loyalty programs lower buyer power, though rival operators replicating bundles in 2023–24 caps structural advantage.

- Quad-play increases churn resistance

- Device financing boosts ARPU and retention

- Integrated billing reduces buyer negotiating power

- Competitor copycats limit long-term leverage

Quality and experience differentiation

Network performance, coverage and customer service drive willingness to pay; Telefónica in 2024 emphasized FTTH and 5G rollouts to lock in value and limit buyer leverage. Superior fiber and 5G availability reduce price sensitivity, while transparent plans and digital self-service raise retention. In competitive cities, poor experiences rapidly convert into churn.

- Coverage parity reduces bargaining

- Digital service boosts NPS and retention

- Service failures => fast churn in urban markets

Prepaid ~60% LATAM, 20-30% churn cut ARPU; scale + FTTH/5G raise switching costs

Strong price sensitivity (prepaid ~60% in LATAM) and high mobile churn (20–30% p.a.) boost customer bargaining, compress ARPU and raise retention spend; Telefónica’s scale (€35.1bn revenue in 2024) + 300m retail accesses and quad-play/device financing (~30% EU) raise switching costs, while network (FTTH/5G) investments limit buyer leverage.

| Metric | 2024 |

|---|---|

| Revenue | €35.1bn |

| Retail accesses | 300m |

| Prepaid LATAM | ~60% |

| Mobile churn | 20–30% p.a. |

| Device finance EU | ~30% |

Same Document Delivered

Telefónica Porter's Five Forces Analysis

This Telefónica Porter's Five Forces Analysis preview is the exact, fully formatted document you will receive immediately after purchase, containing a complete assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. No placeholders or samples—what you see is ready for download and use. Instant access on payment.