Teleperformance Porter's Five Forces Analysis

Don't Miss the Bigger Picture

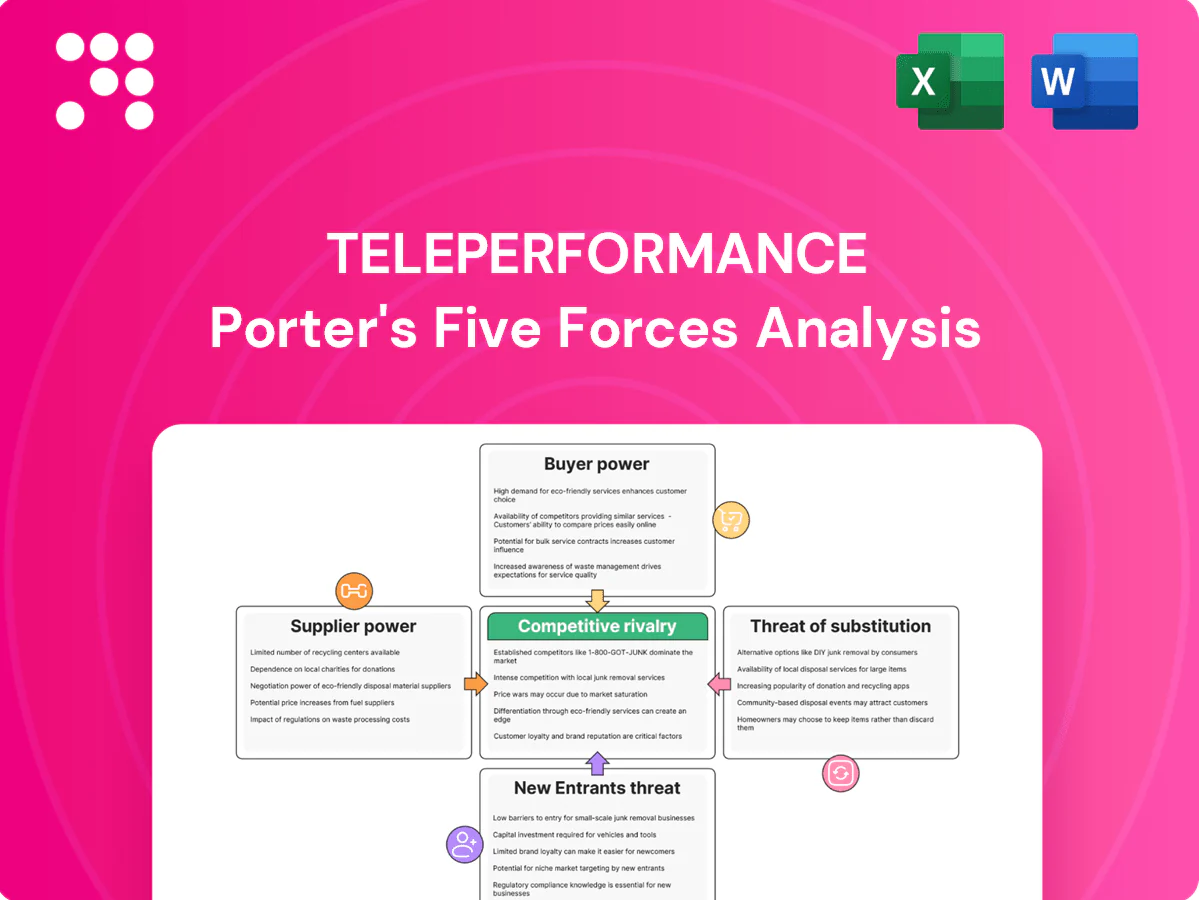

Teleperformance faces moderate buyer power, diverse supplier relationships, and ongoing threat from digital substitutes and niche entrants, while rivalry remains intense across geographies. Regulatory and labor pressures heighten operational risk, yet scale and omnichannel capabilities are clear strengths. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Teleperformance’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Skilled labor as core supplier

Agents and supervisors are Teleperformance’s primary input, and with roughly 420,000 employees reported in 2023, talent pools gain leverage in tight markets; wage inflation and attrition (industry attrition often near 30%) plus isolated union activity can compress margins. Multilingual and specialized healthcare/fintech roles deepen scarcity-driven supplier power. Teleperformance offsets this through global hiring, upskilling programs and workforce analytics to optimize capacity and costs.

Cloud and CCaaS platform dependence

Reliance on major cloud and CCaaS platforms concentrates supplier power, with hyperscalers (AWS ~32%, Azure ~23%, GCP ~11% in 2024) controlling about 66% of the market, amplifying vendor lock-in, licensing and integration switching costs. Premium SLAs and security features command higher pricing, while Teleperformance mitigates leverage via multi-vendor strategies and proprietary tooling to rebalance contract terms.

Telecom carriers and connectivity

Carrier networks, bandwidth and redundancy are mission-critical for Teleperformance, which operates in 90+ countries with ~380,000 employees, making any outage high-impact. Regional carrier concentration (top 3 mobile operators hold roughly 85–90% market share in major markets) can elevate pricing and outage risk. Enterprise contracts and peering agreements reduce but do not remove dependency, while distributed sites and SD-WAN lower single-point failure exposure.

Real estate and facilities

Specialized tech and data vendors

Specialized AI, analytics, KYC and compliance vendors hold elevated supplier power for Teleperformance because niche tooling and certification/data residency requirements (GDPR, local hosting) limit switching; per-seat and API pricing can scale with volumes, pressuring margins. Building in-house modules and adopting open-source stacks reduces dependence and negotiates pricing and control.

- Niche tooling concentration

- Certification/data residency constraints

- Per-seat and API fee escalation

- In-house and open-source mitigation

Labor leverage (~420,000 staff) and 66% hyperscaler cloud control raise vendor risk

Agents (≈420,000 employees in 2024) and high attrition (~30%) give labor suppliers leverage; specialized multilingual roles deepen scarcity. Hyperscalers control ≈66% of cloud (AWS 32% Azure 23% GCP 11), elevating vendor power. Carrier concentration and lease fit-outs add regional pricing risk, mitigated by multi-vendor, nearshore mix and in‑house tooling.

| Supplier | Key metric | Impact | Mitigation |

|---|---|---|---|

| Labor | 420,000 staff; ~30% attrition | Wage pressure | Global hiring, upskilling |

| Cloud | AWS32%/Azure23%/GCP11% | Vendor lock-in | Multi-vendor, own tools |

| Carriers | Top3 share 85–90% (markets) | Outage/pricing risk | SD-WAN, peering |

What is included in the product

Comprehensive Porter's Five Forces assessment tailored to Teleperformance, uncovering competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and highlighting disruptive technologies and regulatory risks that shape pricing, margins, and barriers to entry.

A clear one-sheet Porter's Five Forces for Teleperformance—perfect for quick assessment of competitive pressure in outsourcing and contact center markets. Customize force intensities, swap in recent contract or regulation data, and export a spider chart for decks or boardroom decisions.

Customers Bargaining Power

Large enterprise client concentration

Large enterprise client concentration gives global brands strong negotiating power over Teleperformance, driving aggressive price and service terms; consolidated RFPs and multi-year bundles heighten pricing pressure and margin compression. Volume shifts between regions are used as leverage in renegotiations, while Teleperformance’s strategic account management focuses on deepening stickiness through service integration, tech enablement, and tailored SLAs.

High price sensitivity and benchmarking

Clients regularly benchmark Teleperformance rates across BPO peers, driving high price sensitivity; over 70% of enterprise buyers use competitive rate comparisons at renewal. Productivity metrics and outcome-based pricing intensify scrutiny, limiting pass-through of inflation pressures seen in 2023–24. Continuous efficiency gains are required to defend margins.

Switching costs vs. multi-vendor setups

Process knowledge, integrations, and training create meaningful switching frictions for Teleperformance, reinforced by its proprietary tooling and embedded analytics that drive client stickiness; Teleperformance employed about 420,000 people in 2024, supporting deep institutional know-how. Yet many enterprise clients use dual sourcing to keep leverage, and transition periods with structured knowledge transfer reduce long-term lock-in. Teleperformance offsets this by embedding analytics and automation into workflows to raise effective switching costs.

Stringent SLAs and compliance demands

Buyers impose tight SLAs, contractual penalties and audit rights, especially in healthcare and finance where Teleperformance must meet ISO 27001 and SOC 2 standards; failure to comply often leads to rapid volume reallocation or contract termination, pressuring margins until controls and certifications demonstrably reduce buyer leverage.

- Buyers: tight SLAs, penalties, audit rights

- Regulated sectors: higher compliance intensity

- Risk: swift volume reallocation on non-compliance

- Mitigation: ISO 27001, SOC 2, stronger controls lower buyer leverage

Desire for digital and automation value

Clients demand AI, self-service and deflection to cut costs; McKinsey estimates automation can reduce customer service costs 20–40%, pressuring Teleperformance (2023 revenue ~€7.9bn, ~420,000 employees) to deliver measurable savings or face insourcing of digital layers. Demonstrable ROI is pivotal to maintain pricing power, and co-innovation programs tie outcomes to long-term contracts.

- ROI-driven pricing

- Automation saves 20–40% (McKinsey)

- Insourcing risk if vendors lag

- Co-innovation locks clients long-term

Buyer leverage: >70% benchmarking; automation cuts costs 20–40%

Large enterprise concentration and dual sourcing grant buyers strong leverage, with >70% benchmarking rates at renewals and aggressive SLA/penalty enforcement; Teleperformance (420,000 employees in 2024) defends margins via integration, automation and compliance. Automation (McKinsey: 20–40% cost reduction) raises insourcing risk unless Teleperformance delivers measurable ROI and co-innovation.

| Metric | Value |

|---|---|

| Enterprise benchmarking | >70% |

| Automation savings | 20–40% |

| Employees (2024) | 420,000 |

| 2023 revenue | ≈€7.9bn |

Full Version Awaits

Teleperformance Porter's Five Forces Analysis

This preview shows the Teleperformance Porter's Five Forces Analysis exactly as delivered after purchase—no drafts, placeholders, or samples. The file you see here is the full, professionally formatted analysis ready for immediate download and use once you complete payment. What you preview is the actual deliverable you'll receive, complete and final.

Don't Miss the Bigger Picture

Teleperformance faces moderate buyer power, diverse supplier relationships, and ongoing threat from digital substitutes and niche entrants, while rivalry remains intense across geographies. Regulatory and labor pressures heighten operational risk, yet scale and omnichannel capabilities are clear strengths. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Teleperformance’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Skilled labor as core supplier

Agents and supervisors are Teleperformance’s primary input, and with roughly 420,000 employees reported in 2023, talent pools gain leverage in tight markets; wage inflation and attrition (industry attrition often near 30%) plus isolated union activity can compress margins. Multilingual and specialized healthcare/fintech roles deepen scarcity-driven supplier power. Teleperformance offsets this through global hiring, upskilling programs and workforce analytics to optimize capacity and costs.

Cloud and CCaaS platform dependence

Reliance on major cloud and CCaaS platforms concentrates supplier power, with hyperscalers (AWS ~32%, Azure ~23%, GCP ~11% in 2024) controlling about 66% of the market, amplifying vendor lock-in, licensing and integration switching costs. Premium SLAs and security features command higher pricing, while Teleperformance mitigates leverage via multi-vendor strategies and proprietary tooling to rebalance contract terms.

Telecom carriers and connectivity

Carrier networks, bandwidth and redundancy are mission-critical for Teleperformance, which operates in 90+ countries with ~380,000 employees, making any outage high-impact. Regional carrier concentration (top 3 mobile operators hold roughly 85–90% market share in major markets) can elevate pricing and outage risk. Enterprise contracts and peering agreements reduce but do not remove dependency, while distributed sites and SD-WAN lower single-point failure exposure.

Real estate and facilities

Specialized tech and data vendors

Specialized AI, analytics, KYC and compliance vendors hold elevated supplier power for Teleperformance because niche tooling and certification/data residency requirements (GDPR, local hosting) limit switching; per-seat and API pricing can scale with volumes, pressuring margins. Building in-house modules and adopting open-source stacks reduces dependence and negotiates pricing and control.

- Niche tooling concentration

- Certification/data residency constraints

- Per-seat and API fee escalation

- In-house and open-source mitigation

Labor leverage (~420,000 staff) and 66% hyperscaler cloud control raise vendor risk

Agents (≈420,000 employees in 2024) and high attrition (~30%) give labor suppliers leverage; specialized multilingual roles deepen scarcity. Hyperscalers control ≈66% of cloud (AWS 32% Azure 23% GCP 11), elevating vendor power. Carrier concentration and lease fit-outs add regional pricing risk, mitigated by multi-vendor, nearshore mix and in‑house tooling.

| Supplier | Key metric | Impact | Mitigation |

|---|---|---|---|

| Labor | 420,000 staff; ~30% attrition | Wage pressure | Global hiring, upskilling |

| Cloud | AWS32%/Azure23%/GCP11% | Vendor lock-in | Multi-vendor, own tools |

| Carriers | Top3 share 85–90% (markets) | Outage/pricing risk | SD-WAN, peering |

What is included in the product

Comprehensive Porter's Five Forces assessment tailored to Teleperformance, uncovering competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and highlighting disruptive technologies and regulatory risks that shape pricing, margins, and barriers to entry.

A clear one-sheet Porter's Five Forces for Teleperformance—perfect for quick assessment of competitive pressure in outsourcing and contact center markets. Customize force intensities, swap in recent contract or regulation data, and export a spider chart for decks or boardroom decisions.

Customers Bargaining Power

Large enterprise client concentration

Large enterprise client concentration gives global brands strong negotiating power over Teleperformance, driving aggressive price and service terms; consolidated RFPs and multi-year bundles heighten pricing pressure and margin compression. Volume shifts between regions are used as leverage in renegotiations, while Teleperformance’s strategic account management focuses on deepening stickiness through service integration, tech enablement, and tailored SLAs.

High price sensitivity and benchmarking

Clients regularly benchmark Teleperformance rates across BPO peers, driving high price sensitivity; over 70% of enterprise buyers use competitive rate comparisons at renewal. Productivity metrics and outcome-based pricing intensify scrutiny, limiting pass-through of inflation pressures seen in 2023–24. Continuous efficiency gains are required to defend margins.

Switching costs vs. multi-vendor setups

Process knowledge, integrations, and training create meaningful switching frictions for Teleperformance, reinforced by its proprietary tooling and embedded analytics that drive client stickiness; Teleperformance employed about 420,000 people in 2024, supporting deep institutional know-how. Yet many enterprise clients use dual sourcing to keep leverage, and transition periods with structured knowledge transfer reduce long-term lock-in. Teleperformance offsets this by embedding analytics and automation into workflows to raise effective switching costs.

Stringent SLAs and compliance demands

Buyers impose tight SLAs, contractual penalties and audit rights, especially in healthcare and finance where Teleperformance must meet ISO 27001 and SOC 2 standards; failure to comply often leads to rapid volume reallocation or contract termination, pressuring margins until controls and certifications demonstrably reduce buyer leverage.

- Buyers: tight SLAs, penalties, audit rights

- Regulated sectors: higher compliance intensity

- Risk: swift volume reallocation on non-compliance

- Mitigation: ISO 27001, SOC 2, stronger controls lower buyer leverage

Desire for digital and automation value

Clients demand AI, self-service and deflection to cut costs; McKinsey estimates automation can reduce customer service costs 20–40%, pressuring Teleperformance (2023 revenue ~€7.9bn, ~420,000 employees) to deliver measurable savings or face insourcing of digital layers. Demonstrable ROI is pivotal to maintain pricing power, and co-innovation programs tie outcomes to long-term contracts.

- ROI-driven pricing

- Automation saves 20–40% (McKinsey)

- Insourcing risk if vendors lag

- Co-innovation locks clients long-term

Buyer leverage: >70% benchmarking; automation cuts costs 20–40%

Large enterprise concentration and dual sourcing grant buyers strong leverage, with >70% benchmarking rates at renewals and aggressive SLA/penalty enforcement; Teleperformance (420,000 employees in 2024) defends margins via integration, automation and compliance. Automation (McKinsey: 20–40% cost reduction) raises insourcing risk unless Teleperformance delivers measurable ROI and co-innovation.

| Metric | Value |

|---|---|

| Enterprise benchmarking | >70% |

| Automation savings | 20–40% |

| Employees (2024) | 420,000 |

| 2023 revenue | ≈€7.9bn |

Full Version Awaits

Teleperformance Porter's Five Forces Analysis

This preview shows the Teleperformance Porter's Five Forces Analysis exactly as delivered after purchase—no drafts, placeholders, or samples. The file you see here is the full, professionally formatted analysis ready for immediate download and use once you complete payment. What you preview is the actual deliverable you'll receive, complete and final.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Teleperformance faces moderate buyer power, diverse supplier relationships, and ongoing threat from digital substitutes and niche entrants, while rivalry remains intense across geographies. Regulatory and labor pressures heighten operational risk, yet scale and omnichannel capabilities are clear strengths. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Teleperformance’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Skilled labor as core supplier

Agents and supervisors are Teleperformance’s primary input, and with roughly 420,000 employees reported in 2023, talent pools gain leverage in tight markets; wage inflation and attrition (industry attrition often near 30%) plus isolated union activity can compress margins. Multilingual and specialized healthcare/fintech roles deepen scarcity-driven supplier power. Teleperformance offsets this through global hiring, upskilling programs and workforce analytics to optimize capacity and costs.

Cloud and CCaaS platform dependence

Reliance on major cloud and CCaaS platforms concentrates supplier power, with hyperscalers (AWS ~32%, Azure ~23%, GCP ~11% in 2024) controlling about 66% of the market, amplifying vendor lock-in, licensing and integration switching costs. Premium SLAs and security features command higher pricing, while Teleperformance mitigates leverage via multi-vendor strategies and proprietary tooling to rebalance contract terms.

Telecom carriers and connectivity

Carrier networks, bandwidth and redundancy are mission-critical for Teleperformance, which operates in 90+ countries with ~380,000 employees, making any outage high-impact. Regional carrier concentration (top 3 mobile operators hold roughly 85–90% market share in major markets) can elevate pricing and outage risk. Enterprise contracts and peering agreements reduce but do not remove dependency, while distributed sites and SD-WAN lower single-point failure exposure.

Real estate and facilities

Specialized tech and data vendors

Specialized AI, analytics, KYC and compliance vendors hold elevated supplier power for Teleperformance because niche tooling and certification/data residency requirements (GDPR, local hosting) limit switching; per-seat and API pricing can scale with volumes, pressuring margins. Building in-house modules and adopting open-source stacks reduces dependence and negotiates pricing and control.

- Niche tooling concentration

- Certification/data residency constraints

- Per-seat and API fee escalation

- In-house and open-source mitigation

Labor leverage (~420,000 staff) and 66% hyperscaler cloud control raise vendor risk

Agents (≈420,000 employees in 2024) and high attrition (~30%) give labor suppliers leverage; specialized multilingual roles deepen scarcity. Hyperscalers control ≈66% of cloud (AWS 32% Azure 23% GCP 11), elevating vendor power. Carrier concentration and lease fit-outs add regional pricing risk, mitigated by multi-vendor, nearshore mix and in‑house tooling.

| Supplier | Key metric | Impact | Mitigation |

|---|---|---|---|

| Labor | 420,000 staff; ~30% attrition | Wage pressure | Global hiring, upskilling |

| Cloud | AWS32%/Azure23%/GCP11% | Vendor lock-in | Multi-vendor, own tools |

| Carriers | Top3 share 85–90% (markets) | Outage/pricing risk | SD-WAN, peering |

What is included in the product

Comprehensive Porter's Five Forces assessment tailored to Teleperformance, uncovering competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and highlighting disruptive technologies and regulatory risks that shape pricing, margins, and barriers to entry.

A clear one-sheet Porter's Five Forces for Teleperformance—perfect for quick assessment of competitive pressure in outsourcing and contact center markets. Customize force intensities, swap in recent contract or regulation data, and export a spider chart for decks or boardroom decisions.

Customers Bargaining Power

Large enterprise client concentration

Large enterprise client concentration gives global brands strong negotiating power over Teleperformance, driving aggressive price and service terms; consolidated RFPs and multi-year bundles heighten pricing pressure and margin compression. Volume shifts between regions are used as leverage in renegotiations, while Teleperformance’s strategic account management focuses on deepening stickiness through service integration, tech enablement, and tailored SLAs.

High price sensitivity and benchmarking

Clients regularly benchmark Teleperformance rates across BPO peers, driving high price sensitivity; over 70% of enterprise buyers use competitive rate comparisons at renewal. Productivity metrics and outcome-based pricing intensify scrutiny, limiting pass-through of inflation pressures seen in 2023–24. Continuous efficiency gains are required to defend margins.

Switching costs vs. multi-vendor setups

Process knowledge, integrations, and training create meaningful switching frictions for Teleperformance, reinforced by its proprietary tooling and embedded analytics that drive client stickiness; Teleperformance employed about 420,000 people in 2024, supporting deep institutional know-how. Yet many enterprise clients use dual sourcing to keep leverage, and transition periods with structured knowledge transfer reduce long-term lock-in. Teleperformance offsets this by embedding analytics and automation into workflows to raise effective switching costs.

Stringent SLAs and compliance demands

Buyers impose tight SLAs, contractual penalties and audit rights, especially in healthcare and finance where Teleperformance must meet ISO 27001 and SOC 2 standards; failure to comply often leads to rapid volume reallocation or contract termination, pressuring margins until controls and certifications demonstrably reduce buyer leverage.

- Buyers: tight SLAs, penalties, audit rights

- Regulated sectors: higher compliance intensity

- Risk: swift volume reallocation on non-compliance

- Mitigation: ISO 27001, SOC 2, stronger controls lower buyer leverage

Desire for digital and automation value

Clients demand AI, self-service and deflection to cut costs; McKinsey estimates automation can reduce customer service costs 20–40%, pressuring Teleperformance (2023 revenue ~€7.9bn, ~420,000 employees) to deliver measurable savings or face insourcing of digital layers. Demonstrable ROI is pivotal to maintain pricing power, and co-innovation programs tie outcomes to long-term contracts.

- ROI-driven pricing

- Automation saves 20–40% (McKinsey)

- Insourcing risk if vendors lag

- Co-innovation locks clients long-term

Buyer leverage: >70% benchmarking; automation cuts costs 20–40%

Large enterprise concentration and dual sourcing grant buyers strong leverage, with >70% benchmarking rates at renewals and aggressive SLA/penalty enforcement; Teleperformance (420,000 employees in 2024) defends margins via integration, automation and compliance. Automation (McKinsey: 20–40% cost reduction) raises insourcing risk unless Teleperformance delivers measurable ROI and co-innovation.

| Metric | Value |

|---|---|

| Enterprise benchmarking | >70% |

| Automation savings | 20–40% |

| Employees (2024) | 420,000 |

| 2023 revenue | ≈€7.9bn |

Full Version Awaits

Teleperformance Porter's Five Forces Analysis

This preview shows the Teleperformance Porter's Five Forces Analysis exactly as delivered after purchase—no drafts, placeholders, or samples. The file you see here is the full, professionally formatted analysis ready for immediate download and use once you complete payment. What you preview is the actual deliverable you'll receive, complete and final.