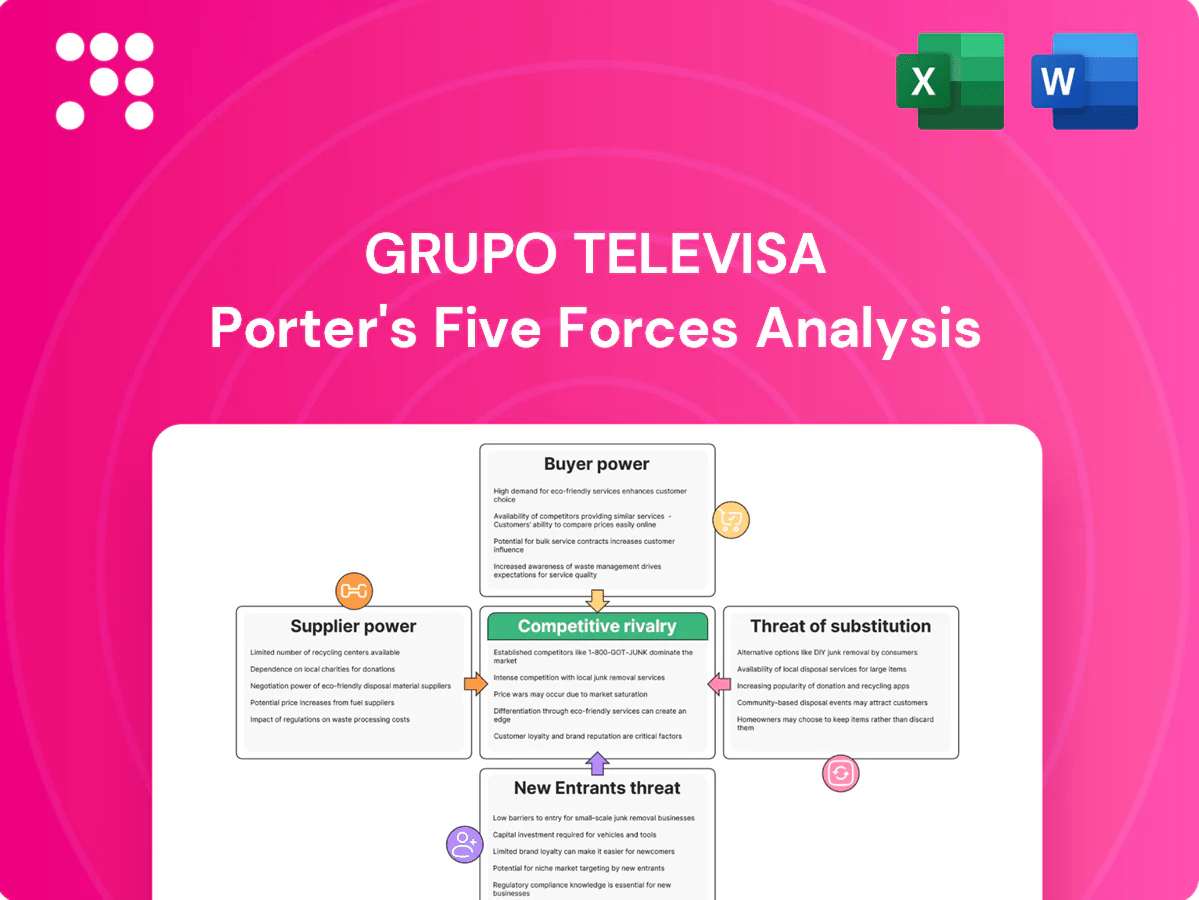

Grupo Televisa Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Grupo Televisa faces intense rivalry from streaming entrants and shifting advertiser power, while content costs and distribution partnerships shape supplier pressure. Buyer bargaining and substitute entertainment elevate strategic risk. This snapshot scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupo Televisa’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce premium content rights

Owners of sports leagues, hit formats and top franchises can demand steep fees and strict terms, and Televisa’s dependence on marquee content to sustain ratings gives these suppliers outsized leverage; global sports media rights spending topped roughly $60 billion by 2023–24, driving intense bidding. Multi-year exclusivity deals and auctions push rights prices higher, while strategic moves into owned IP and co-productions can reduce supplier power over time.

Star talent and creative guilds

High-profile actors, writers and producers drive audience draw and ad rates, and after the 2023 WGA/SAG-AFTRA agreements residuals and streaming payouts pushed top-talent costs higher in 2024, increasing fees for marquee projects by an estimated 15–25% versus pre-strike levels. Unionized labor and star scarcity sustain bargaining leverage, even as Televisa’s extensive in-house studios lower production fixed costs. Marquee titles, however, still hinge on elite talent for ratings and international sales. Long-term deals and talent-development programs implemented by Televisa reduce short-term exposure to bidding wars.

Network and tech vendors

Transmission, cloud, CDN, ad-tech and analytics vendors are highly specialized, giving key suppliers moderate leverage due to switching costs and integration complexity. In 2024 major cloud providers held ~65% of the market (AWS 32%, Azure 23%, GCP 10%), enabling competitive bidding among multiple global suppliers. Hybrid, multi-vendor deployments and open standards used by Televisa reduce vendor dependence and price pressure.

Telecom infrastructure inputs

Fiber, last-mile equipment and spectrum-dependent gear are highly capital intensive, with typical replacement cycles of 7–10 years; upfront fiber rollout and active RAN investments drive large periodic capex. Supplier concentration is high: the top 3 RAN vendors (Ericsson, Nokia, Huawei) account for over 60% of global market share, raising supplier clout. Grupo Televisa’s cross-platform scale and group purchasing across cable and telecom mitigate pricing pressure, while progressive vertical integration in network assets reduces external supplier exposure over time.

- Replacement cycles: 7–10 years

- Top-3 vendor share: >60%

- Volume purchasing: lowers unit pricing

- Vertical integration: reduces external dependency

Third-party distributors

Platform stores, device makers and smart‑TV OS partners dictate app placement and revenue shares, with Apple and Google keeping standard cuts of 30% (reduced to 15% for qualifying small developers in 2024), while carriage and syndication terms for pay‑TV remain stringent. Televisa’s strong brand and content scale improve placement and fee negotiation, and expansion of ViX and other direct‑to‑consumer channels reduces reliance on these gatekeepers.

Sports rights $60B, talent +15-25% raise costs; vertical integration curbs supplier power

Suppliers hold moderate-to-high power: sports rights (global spend ~$60B in 2023–24) and top talent (post‑2023 strikes talent costs +15–25%) drive content costs, while cloud/CDN and device gatekeepers (app cuts 30%/15%) exert pricing pressure. Televisa’s scale, vertical integration and D2C pushback reduce net supplier leverage.

| Metric | 2024 |

|---|---|

| Sports rights spend | $60B |

| Talent cost rise | +15–25% |

| Cloud share (AWS/Azure/GCP) | 32/23/10% |

| Top‑3 RAN share | >60% |

| App store cuts | 30% / 15% |

What is included in the product

Comprehensive Porter's Five Forces assessment of Grupo Televisa that uncovers competitive intensity, buyer and supplier leverage, entry barriers, and substitute threats shaping profitability. Identifies disruptive digital rivals and strategic levers to defend market share; fully editable for reports and presentations.

One-sheet Porter’s Five Forces for Grupo Televisa—quickly visualize competitive pressure with an editable spider chart and clear force scores for boardroom decisions. Clean, slide-ready layout lets you swap in current data, duplicate scenarios (regulation, streaming entrants) and integrate into broader reports without macros.

Customers Bargaining Power

Advertisers and agencies

Large advertisers and buying groups aggregate spend and negotiate CPMs and integrations, controlling a dominant share of major TV and digital buys and able to reallocate budgets across TV, digital and social within weeks. Measurement demands and brand-safety clauses—now standard in ~80% of agency contracts—add further leverage. Televisa counters with cross‑media reach (100m+ monthly viewers across its platforms), granular audience segments and bundled packages to protect yields.

Viewers and subscribers

Audiences face low switching costs across OTT, social, gaming and FTA rivals, and by 2024 global paid-streaming subscriptions exceeded 1 billion, amplifying churn risk for Grupo Televisa’s pay-TV and streaming businesses. Churn pressure makes content freshness, UX and competitive pricing decisive; personalization and tiered plans (ad-supported and premium) are key levers to retain users and reduce monthly attrition.

Wholesale carriage partners

Other pay-TV operators and ISPs negotiating channel placement and fees can wield leverage, but Televisa’s free-to-air and pay channels reach over 90% of Mexican households, limiting buyer power. Blackout risks and IFT regulatory scrutiny constrain abrupt fee hikes or delistings. Televisa’s must-have sports and entertainment line-up preserves pricing power. Reciprocal distribution via Televisa’s VOD/platforms strengthens its hand.

Enterprises and SMEs (telecom)

Enterprises and SMEs push for robust SLAs, security and competitive bundles; multisourcing trends lower reliance on a single operator. Mexico had ≈112 mobile subscriptions per 100 inhabitants in 2024, intensifying buyer leverage. Televisa’s convergent izzi offers can trade lower headline price for higher stickiness while value-added services reduce pure price sensitivity.

- SLAs & security pressure

- Multisourcing lowers switching costs

- Convergent offers increase retention

- Value-added services cut price sensitivity

International buyers of content

Global streamers and broadcasters in 2024 (Netflix, Amazon, Disney+) face many sourcing options and exert pressure on licensing fees and windowing, compressing margins. Televisa’s Spanish-language scale and deep catalog sustain negotiating power across Latin America and the US Hispanic market. Strategic co-productions and exclusivity deals continue to command licensing premiums.

- High buyer options → price pressure

- Televisa scale → stronger bargaining

- Co-pro/exclusivity → premium pricing

Global streamers compress CPMs; huge local reach and bundling protect ad yields

Large ad buyers and global streamers (≈1bn paid streaming subs in 2024) compress CPMs; agency measurement/brand‑safety clauses (~80% of contracts) and high mobile penetration (~112 subs/100 in Mexico, 2024) increase buyer leverage. Televisa counters with 100m+ monthly viewers, >90% Mexican household reach and deep Spanish catalog; izzi bundles raise stickiness and reduce pure price sensitivity.

| Metric | 2024 value | Impact |

|---|---|---|

| Monthly reach | 100m+ | Protects ad yields |

| Mexican household reach | >90% | Limits buyer power |

| Global paid subs | ≈1bn | Raises churn risk |

| Mobile penetration | ≈112/100 | Increases bargaining |

| Agency clauses | ~80% | Enhances buyer leverage |

Preview Before You Purchase

Grupo Televisa Porter's Five Forces Analysis

This preview shows the exact Grupo Televisa Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file displayed is the fully formatted, professionally written document ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this identical file upon payment.

A Must-Have Tool for Decision-Makers

Grupo Televisa faces intense rivalry from streaming entrants and shifting advertiser power, while content costs and distribution partnerships shape supplier pressure. Buyer bargaining and substitute entertainment elevate strategic risk. This snapshot scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupo Televisa’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce premium content rights

Owners of sports leagues, hit formats and top franchises can demand steep fees and strict terms, and Televisa’s dependence on marquee content to sustain ratings gives these suppliers outsized leverage; global sports media rights spending topped roughly $60 billion by 2023–24, driving intense bidding. Multi-year exclusivity deals and auctions push rights prices higher, while strategic moves into owned IP and co-productions can reduce supplier power over time.

Star talent and creative guilds

High-profile actors, writers and producers drive audience draw and ad rates, and after the 2023 WGA/SAG-AFTRA agreements residuals and streaming payouts pushed top-talent costs higher in 2024, increasing fees for marquee projects by an estimated 15–25% versus pre-strike levels. Unionized labor and star scarcity sustain bargaining leverage, even as Televisa’s extensive in-house studios lower production fixed costs. Marquee titles, however, still hinge on elite talent for ratings and international sales. Long-term deals and talent-development programs implemented by Televisa reduce short-term exposure to bidding wars.

Network and tech vendors

Transmission, cloud, CDN, ad-tech and analytics vendors are highly specialized, giving key suppliers moderate leverage due to switching costs and integration complexity. In 2024 major cloud providers held ~65% of the market (AWS 32%, Azure 23%, GCP 10%), enabling competitive bidding among multiple global suppliers. Hybrid, multi-vendor deployments and open standards used by Televisa reduce vendor dependence and price pressure.

Telecom infrastructure inputs

Fiber, last-mile equipment and spectrum-dependent gear are highly capital intensive, with typical replacement cycles of 7–10 years; upfront fiber rollout and active RAN investments drive large periodic capex. Supplier concentration is high: the top 3 RAN vendors (Ericsson, Nokia, Huawei) account for over 60% of global market share, raising supplier clout. Grupo Televisa’s cross-platform scale and group purchasing across cable and telecom mitigate pricing pressure, while progressive vertical integration in network assets reduces external supplier exposure over time.

- Replacement cycles: 7–10 years

- Top-3 vendor share: >60%

- Volume purchasing: lowers unit pricing

- Vertical integration: reduces external dependency

Third-party distributors

Platform stores, device makers and smart‑TV OS partners dictate app placement and revenue shares, with Apple and Google keeping standard cuts of 30% (reduced to 15% for qualifying small developers in 2024), while carriage and syndication terms for pay‑TV remain stringent. Televisa’s strong brand and content scale improve placement and fee negotiation, and expansion of ViX and other direct‑to‑consumer channels reduces reliance on these gatekeepers.

Sports rights $60B, talent +15-25% raise costs; vertical integration curbs supplier power

Suppliers hold moderate-to-high power: sports rights (global spend ~$60B in 2023–24) and top talent (post‑2023 strikes talent costs +15–25%) drive content costs, while cloud/CDN and device gatekeepers (app cuts 30%/15%) exert pricing pressure. Televisa’s scale, vertical integration and D2C pushback reduce net supplier leverage.

| Metric | 2024 |

|---|---|

| Sports rights spend | $60B |

| Talent cost rise | +15–25% |

| Cloud share (AWS/Azure/GCP) | 32/23/10% |

| Top‑3 RAN share | >60% |

| App store cuts | 30% / 15% |

What is included in the product

Comprehensive Porter's Five Forces assessment of Grupo Televisa that uncovers competitive intensity, buyer and supplier leverage, entry barriers, and substitute threats shaping profitability. Identifies disruptive digital rivals and strategic levers to defend market share; fully editable for reports and presentations.

One-sheet Porter’s Five Forces for Grupo Televisa—quickly visualize competitive pressure with an editable spider chart and clear force scores for boardroom decisions. Clean, slide-ready layout lets you swap in current data, duplicate scenarios (regulation, streaming entrants) and integrate into broader reports without macros.

Customers Bargaining Power

Advertisers and agencies

Large advertisers and buying groups aggregate spend and negotiate CPMs and integrations, controlling a dominant share of major TV and digital buys and able to reallocate budgets across TV, digital and social within weeks. Measurement demands and brand-safety clauses—now standard in ~80% of agency contracts—add further leverage. Televisa counters with cross‑media reach (100m+ monthly viewers across its platforms), granular audience segments and bundled packages to protect yields.

Viewers and subscribers

Audiences face low switching costs across OTT, social, gaming and FTA rivals, and by 2024 global paid-streaming subscriptions exceeded 1 billion, amplifying churn risk for Grupo Televisa’s pay-TV and streaming businesses. Churn pressure makes content freshness, UX and competitive pricing decisive; personalization and tiered plans (ad-supported and premium) are key levers to retain users and reduce monthly attrition.

Wholesale carriage partners

Other pay-TV operators and ISPs negotiating channel placement and fees can wield leverage, but Televisa’s free-to-air and pay channels reach over 90% of Mexican households, limiting buyer power. Blackout risks and IFT regulatory scrutiny constrain abrupt fee hikes or delistings. Televisa’s must-have sports and entertainment line-up preserves pricing power. Reciprocal distribution via Televisa’s VOD/platforms strengthens its hand.

Enterprises and SMEs (telecom)

Enterprises and SMEs push for robust SLAs, security and competitive bundles; multisourcing trends lower reliance on a single operator. Mexico had ≈112 mobile subscriptions per 100 inhabitants in 2024, intensifying buyer leverage. Televisa’s convergent izzi offers can trade lower headline price for higher stickiness while value-added services reduce pure price sensitivity.

- SLAs & security pressure

- Multisourcing lowers switching costs

- Convergent offers increase retention

- Value-added services cut price sensitivity

International buyers of content

Global streamers and broadcasters in 2024 (Netflix, Amazon, Disney+) face many sourcing options and exert pressure on licensing fees and windowing, compressing margins. Televisa’s Spanish-language scale and deep catalog sustain negotiating power across Latin America and the US Hispanic market. Strategic co-productions and exclusivity deals continue to command licensing premiums.

- High buyer options → price pressure

- Televisa scale → stronger bargaining

- Co-pro/exclusivity → premium pricing

Global streamers compress CPMs; huge local reach and bundling protect ad yields

Large ad buyers and global streamers (≈1bn paid streaming subs in 2024) compress CPMs; agency measurement/brand‑safety clauses (~80% of contracts) and high mobile penetration (~112 subs/100 in Mexico, 2024) increase buyer leverage. Televisa counters with 100m+ monthly viewers, >90% Mexican household reach and deep Spanish catalog; izzi bundles raise stickiness and reduce pure price sensitivity.

| Metric | 2024 value | Impact |

|---|---|---|

| Monthly reach | 100m+ | Protects ad yields |

| Mexican household reach | >90% | Limits buyer power |

| Global paid subs | ≈1bn | Raises churn risk |

| Mobile penetration | ≈112/100 | Increases bargaining |

| Agency clauses | ~80% | Enhances buyer leverage |

Preview Before You Purchase

Grupo Televisa Porter's Five Forces Analysis

This preview shows the exact Grupo Televisa Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file displayed is the fully formatted, professionally written document ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this identical file upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Grupo Televisa faces intense rivalry from streaming entrants and shifting advertiser power, while content costs and distribution partnerships shape supplier pressure. Buyer bargaining and substitute entertainment elevate strategic risk. This snapshot scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupo Televisa’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce premium content rights

Owners of sports leagues, hit formats and top franchises can demand steep fees and strict terms, and Televisa’s dependence on marquee content to sustain ratings gives these suppliers outsized leverage; global sports media rights spending topped roughly $60 billion by 2023–24, driving intense bidding. Multi-year exclusivity deals and auctions push rights prices higher, while strategic moves into owned IP and co-productions can reduce supplier power over time.

Star talent and creative guilds

High-profile actors, writers and producers drive audience draw and ad rates, and after the 2023 WGA/SAG-AFTRA agreements residuals and streaming payouts pushed top-talent costs higher in 2024, increasing fees for marquee projects by an estimated 15–25% versus pre-strike levels. Unionized labor and star scarcity sustain bargaining leverage, even as Televisa’s extensive in-house studios lower production fixed costs. Marquee titles, however, still hinge on elite talent for ratings and international sales. Long-term deals and talent-development programs implemented by Televisa reduce short-term exposure to bidding wars.

Network and tech vendors

Transmission, cloud, CDN, ad-tech and analytics vendors are highly specialized, giving key suppliers moderate leverage due to switching costs and integration complexity. In 2024 major cloud providers held ~65% of the market (AWS 32%, Azure 23%, GCP 10%), enabling competitive bidding among multiple global suppliers. Hybrid, multi-vendor deployments and open standards used by Televisa reduce vendor dependence and price pressure.

Telecom infrastructure inputs

Fiber, last-mile equipment and spectrum-dependent gear are highly capital intensive, with typical replacement cycles of 7–10 years; upfront fiber rollout and active RAN investments drive large periodic capex. Supplier concentration is high: the top 3 RAN vendors (Ericsson, Nokia, Huawei) account for over 60% of global market share, raising supplier clout. Grupo Televisa’s cross-platform scale and group purchasing across cable and telecom mitigate pricing pressure, while progressive vertical integration in network assets reduces external supplier exposure over time.

- Replacement cycles: 7–10 years

- Top-3 vendor share: >60%

- Volume purchasing: lowers unit pricing

- Vertical integration: reduces external dependency

Third-party distributors

Platform stores, device makers and smart‑TV OS partners dictate app placement and revenue shares, with Apple and Google keeping standard cuts of 30% (reduced to 15% for qualifying small developers in 2024), while carriage and syndication terms for pay‑TV remain stringent. Televisa’s strong brand and content scale improve placement and fee negotiation, and expansion of ViX and other direct‑to‑consumer channels reduces reliance on these gatekeepers.

Sports rights $60B, talent +15-25% raise costs; vertical integration curbs supplier power

Suppliers hold moderate-to-high power: sports rights (global spend ~$60B in 2023–24) and top talent (post‑2023 strikes talent costs +15–25%) drive content costs, while cloud/CDN and device gatekeepers (app cuts 30%/15%) exert pricing pressure. Televisa’s scale, vertical integration and D2C pushback reduce net supplier leverage.

| Metric | 2024 |

|---|---|

| Sports rights spend | $60B |

| Talent cost rise | +15–25% |

| Cloud share (AWS/Azure/GCP) | 32/23/10% |

| Top‑3 RAN share | >60% |

| App store cuts | 30% / 15% |

What is included in the product

Comprehensive Porter's Five Forces assessment of Grupo Televisa that uncovers competitive intensity, buyer and supplier leverage, entry barriers, and substitute threats shaping profitability. Identifies disruptive digital rivals and strategic levers to defend market share; fully editable for reports and presentations.

One-sheet Porter’s Five Forces for Grupo Televisa—quickly visualize competitive pressure with an editable spider chart and clear force scores for boardroom decisions. Clean, slide-ready layout lets you swap in current data, duplicate scenarios (regulation, streaming entrants) and integrate into broader reports without macros.

Customers Bargaining Power

Advertisers and agencies

Large advertisers and buying groups aggregate spend and negotiate CPMs and integrations, controlling a dominant share of major TV and digital buys and able to reallocate budgets across TV, digital and social within weeks. Measurement demands and brand-safety clauses—now standard in ~80% of agency contracts—add further leverage. Televisa counters with cross‑media reach (100m+ monthly viewers across its platforms), granular audience segments and bundled packages to protect yields.

Viewers and subscribers

Audiences face low switching costs across OTT, social, gaming and FTA rivals, and by 2024 global paid-streaming subscriptions exceeded 1 billion, amplifying churn risk for Grupo Televisa’s pay-TV and streaming businesses. Churn pressure makes content freshness, UX and competitive pricing decisive; personalization and tiered plans (ad-supported and premium) are key levers to retain users and reduce monthly attrition.

Wholesale carriage partners

Other pay-TV operators and ISPs negotiating channel placement and fees can wield leverage, but Televisa’s free-to-air and pay channels reach over 90% of Mexican households, limiting buyer power. Blackout risks and IFT regulatory scrutiny constrain abrupt fee hikes or delistings. Televisa’s must-have sports and entertainment line-up preserves pricing power. Reciprocal distribution via Televisa’s VOD/platforms strengthens its hand.

Enterprises and SMEs (telecom)

Enterprises and SMEs push for robust SLAs, security and competitive bundles; multisourcing trends lower reliance on a single operator. Mexico had ≈112 mobile subscriptions per 100 inhabitants in 2024, intensifying buyer leverage. Televisa’s convergent izzi offers can trade lower headline price for higher stickiness while value-added services reduce pure price sensitivity.

- SLAs & security pressure

- Multisourcing lowers switching costs

- Convergent offers increase retention

- Value-added services cut price sensitivity

International buyers of content

Global streamers and broadcasters in 2024 (Netflix, Amazon, Disney+) face many sourcing options and exert pressure on licensing fees and windowing, compressing margins. Televisa’s Spanish-language scale and deep catalog sustain negotiating power across Latin America and the US Hispanic market. Strategic co-productions and exclusivity deals continue to command licensing premiums.

- High buyer options → price pressure

- Televisa scale → stronger bargaining

- Co-pro/exclusivity → premium pricing

Global streamers compress CPMs; huge local reach and bundling protect ad yields

Large ad buyers and global streamers (≈1bn paid streaming subs in 2024) compress CPMs; agency measurement/brand‑safety clauses (~80% of contracts) and high mobile penetration (~112 subs/100 in Mexico, 2024) increase buyer leverage. Televisa counters with 100m+ monthly viewers, >90% Mexican household reach and deep Spanish catalog; izzi bundles raise stickiness and reduce pure price sensitivity.

| Metric | 2024 value | Impact |

|---|---|---|

| Monthly reach | 100m+ | Protects ad yields |

| Mexican household reach | >90% | Limits buyer power |

| Global paid subs | ≈1bn | Raises churn risk |

| Mobile penetration | ≈112/100 | Increases bargaining |

| Agency clauses | ~80% | Enhances buyer leverage |

Preview Before You Purchase

Grupo Televisa Porter's Five Forces Analysis

This preview shows the exact Grupo Televisa Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file displayed is the fully formatted, professionally written document ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this identical file upon payment.