Telos PESTLE Analysis

Skip the Research. Get the Strategy.

Gain competitive clarity with our PESTLE analysis of Telos—concise, actionable insights into political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists, it's ready to use and fully editable. Purchase the full report now for the complete deep-dive.

Political factors

Federal cyber budgets and procurement

DoD and civilian cyber appropriations, allocated in multi-billion-dollar federal IT and defense budgets, directly shape Telos’ pipeline and award cadence by determining program starts and task-order volumes. Multi-year appropriations and IDIQ/GWAC vehicles convert one-off buys into stable, multi-year task orders that smooth revenue and backlog. Continuing resolutions or budget delays defer contract kickoffs and elongate sales cycles, compressing near-term revenue. Securing positions on priority programs and GWAC pools mitigates award volatility and shortens capture timelines.

Zero Trust and national cyber strategy

White House Executive Order on Improving the Nation’s Cybersecurity (May 12, 2021) and OMB Memorandum M-22-09 (March 7, 2022) drive Zero Trust adoption across federal agencies. These mandates create procurement pull for identity, cloud and network security vendors and align with NIST SP 800-207 (Aug 2020) and agency reference architectures to speed deployment. Noncompliance can disqualify vendors from federal bids.

Geopolitical tensions and threat intensity

Rising nation-state activity lifts demand for hardened communications and cyber solutions as global military spending topped about $2.3 trillion in 2023 (SIPRI) and major budgets like the US FY2024 defense bill near $858 billion. Classified and cross-border work expands but increases onboarding complexity and compliance. Urgent operational needs push sole-source and rapid acquisitions. Export controls and alliance frameworks such as AUKUS and NATO shape international market access.

Government shutdown and election cycle risk

Government shutdowns pause contracting actions and payments, straining cash flow—CBO estimated the 2018–2019 shutdown cost the economy about 11 billion dollars, with federal contractors facing delayed invoices. Election turnovers can reorder program priorities and funding lines; federal contracting exceeds 600 billion dollars annually, so shifts matter. Transition periods slow decisions but can refresh budgets for new initiatives.

- Shutdowns pause awards/payments, pressuring liquidity

- 2018–19 CBO cost: 11 billion dollars

- Federal contracting >600 billion dollars/year

- Diversify beyond federal to soften shocks

Cyber workforce and industrial policy

Federal incentives for cyber talent and onshoring — anchored by the CHIPS and Science Act (about 52 billion allocated for semiconductor and related manufacturing) — can ease Telos staffing and facility siting; 2024 saw expanded CHIPS-related pilot grants and public–private cyber pilots. Buy American and tightened supply‑chain rules raise sourcing costs but favor domestic suppliers. Active participation in standards bodies shapes compliance and future procurement requirements.

- CHIPS funding: 52 billion

- 2024: expanded CHIPS/cyber pilots

- Buy American: tighter sourcing

- Standards bodies: influence future rules

Federal defense budgets, cyber mandates and CHIPS Act reshape contractor backlog and costs

DoD/federal budgets (US FY2024 ≈ $858B; federal contracting >600B/yr) and multi‑year IDIQ/GWACs drive Telos revenue visibility and backlog. Cyber mandates (Zero Trust, NIST SP 800‑207) and export controls expand addressable spend but raise compliance costs. CHIPS & Science Act ($52B) and Buy American push onshoring, easing staffing but increasing supplier costs.

| Factor | 2024–25 metric | Impact |

|---|---|---|

| Defense/Fed spend | $858B (FY2024); >$600B contracting | Smooths backlog; award timing risk |

| Cyber mandates | Zero Trust/Ongoing OMB rules | Procurement pull; compliance barrier |

| Onshoring | $52B CHIPS | Talent/facility support; higher costs |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Telos, with data-backed trends and region-specific regulatory context; designed for executives and investors, it offers forward-looking insights, actionable sub-points and clean formatting for reports, decks, and scenario planning.

A concise, visually segmented Telos PESTLE summary that relieves briefing pain by offering clear, editable insights for meetings, presentations, and cross‑team alignment—easy to drop into slides, annotate for local context, and share across devices.

Economic factors

IT spending cycles and macro conditions

Recessions compress discretionary enterprise security spend, slowing sales cycles and procurement; mission-critical federal programs remain more resilient though milestone timing can slip. Inflation-driven wage and cloud cost increases have raised input costs industrywide. Telos benefits from long-term federal contracts that provide revenue visibility; U.S. federal IT spending exceeds $100 billion annually.

Cost of capital and cash conversion

Higher policy rates (federal funds ~5.25–5.50% and 10-year Treasury ~4.2% in mid‑2025) lift borrowing costs and customer hurdle rates, slowing new deal economics. Longer federal billing DSO increases working capital strain for Telos, while fixed‑price contracts magnify execution risk amid inflation. Efficient backlog delivery and timely contract closeouts support margins and cash conversion.

Competitive pricing and consolidation

Cybersecurity remains crowded, driving intense price competition as global cybersecurity spending topped $200 billion in 2024; large platform vendors bundle services to defend share and pressure point-solutions on price. M&A activity continues reshaping the landscape, creating exit pathways or new integrated rivals. Differentiation via certifications and FedRAMP Moderate/High authorizations (several hundred approvals by 2024) helps sustain pricing power.

Cloud migration and SaaS mix

Shift to cloud security and SaaS mix improves revenue quality as enterprise cloud spend approached roughly $620B in 2024, driving higher-margin subscriptions; FedRAMP-authorized SaaS offerings can unlock sticky ARR by easing federal procurement and retention. Usage-based pricing boosts adoption but increases COGS volatility and gross-margin pressure. Partner ecosystems materially influence pipeline and deal flow, amplifying go-to-market reach.

- cloud_spend_2024: ~$620B

- subscription_stickiness: FedRAMP aids ARR retention

- pricing_risk: usage-based raises COGS variability

- partners: amplify deal flow

Dollar strength and international demand

Dollar strength (DXY ~105 in July 2025) raises Telos pricing in non-USD markets, eroding competitiveness and margins as local buyers face higher costs; multinational clients often defer security projects in economic slowdowns, while public-sector and allied governments—with global defense spending near $2.24 trillion in 2023—tend to sustain security allocations, making local partnerships crucial to manage procurement and currency/payment risk.

- Impact: weaker price competitiveness in FX-volatile markets

- Demand risk: project delays by global enterprises

- Resilience: public-sector security budgets remain a stable revenue base

- Mitigation: local partners reduce procurement and payment exposure

Federal defense budgets, cyber mandates and CHIPS Act reshape contractor backlog and costs

Recessionary pressure and higher rates (~federal funds 5.25–5.50% mid‑2025) tighten enterprise spend but federal contracts (> $100B IT spend) provide revenue stability. Inflation and cloud cost growth compress margins; shift to SaaS/cloud (cloud spend ~$620B in 2024) improves ARR quality. FX strength (DXY ~105 Jul‑2025) pressures non‑USD margins; FedRAMP and backlog execution sustain pricing power.

| Metric | Value |

|---|---|

| Federal IT spend | > $100B (annual) |

| Global cyber spend | $200B (2024) |

| Cloud spend | $620B (2024) |

| Fed funds | ~5.25–5.50% (mid‑2025) |

| DXY | ~105 (Jul‑2025) |

Preview the Actual Deliverable

Telos PESTLE Analysis

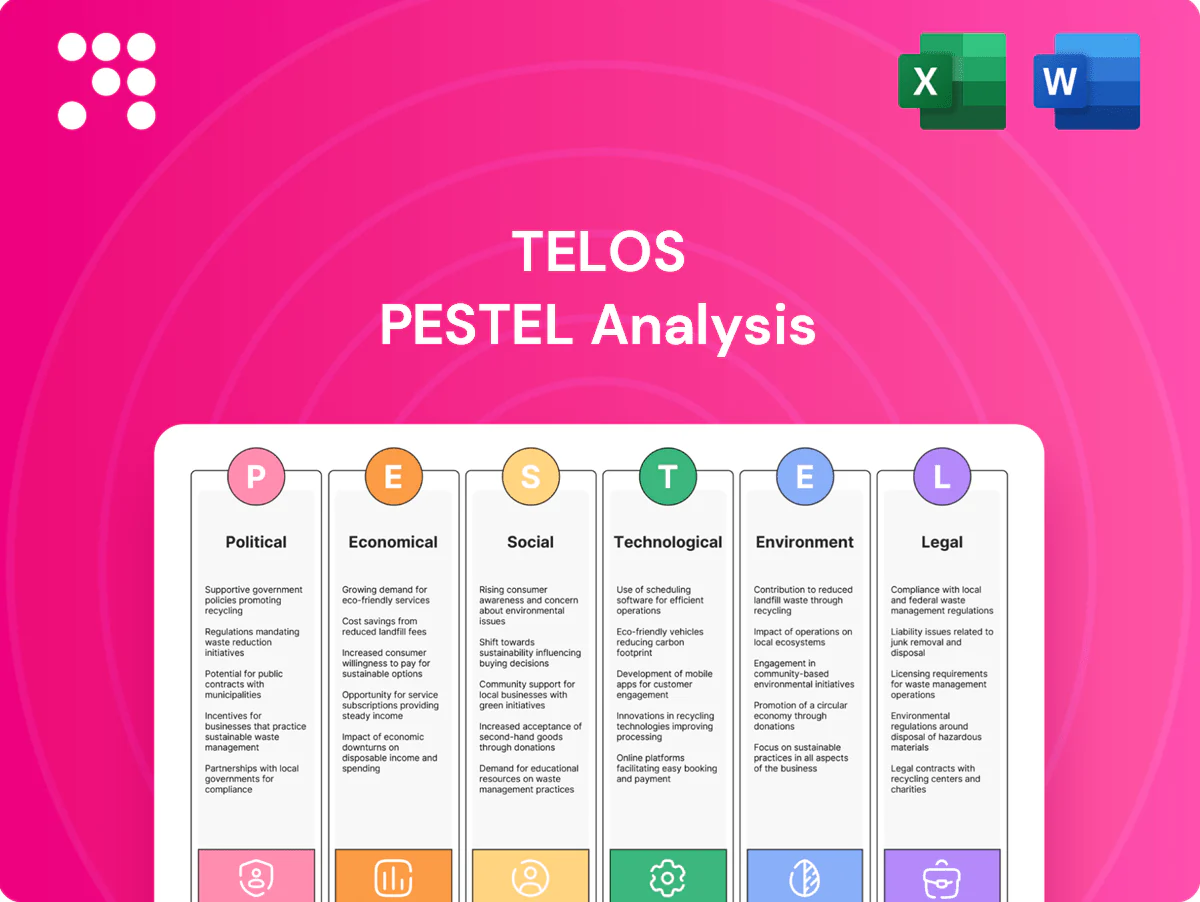

The preview shown here is the exact Telos PESTLE Analysis document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment as displayed; no placeholders or teasers. After checkout you’ll immediately be able to download this same finished file.

Skip the Research. Get the Strategy.

Gain competitive clarity with our PESTLE analysis of Telos—concise, actionable insights into political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists, it's ready to use and fully editable. Purchase the full report now for the complete deep-dive.

Political factors

Federal cyber budgets and procurement

DoD and civilian cyber appropriations, allocated in multi-billion-dollar federal IT and defense budgets, directly shape Telos’ pipeline and award cadence by determining program starts and task-order volumes. Multi-year appropriations and IDIQ/GWAC vehicles convert one-off buys into stable, multi-year task orders that smooth revenue and backlog. Continuing resolutions or budget delays defer contract kickoffs and elongate sales cycles, compressing near-term revenue. Securing positions on priority programs and GWAC pools mitigates award volatility and shortens capture timelines.

Zero Trust and national cyber strategy

White House Executive Order on Improving the Nation’s Cybersecurity (May 12, 2021) and OMB Memorandum M-22-09 (March 7, 2022) drive Zero Trust adoption across federal agencies. These mandates create procurement pull for identity, cloud and network security vendors and align with NIST SP 800-207 (Aug 2020) and agency reference architectures to speed deployment. Noncompliance can disqualify vendors from federal bids.

Geopolitical tensions and threat intensity

Rising nation-state activity lifts demand for hardened communications and cyber solutions as global military spending topped about $2.3 trillion in 2023 (SIPRI) and major budgets like the US FY2024 defense bill near $858 billion. Classified and cross-border work expands but increases onboarding complexity and compliance. Urgent operational needs push sole-source and rapid acquisitions. Export controls and alliance frameworks such as AUKUS and NATO shape international market access.

Government shutdown and election cycle risk

Government shutdowns pause contracting actions and payments, straining cash flow—CBO estimated the 2018–2019 shutdown cost the economy about 11 billion dollars, with federal contractors facing delayed invoices. Election turnovers can reorder program priorities and funding lines; federal contracting exceeds 600 billion dollars annually, so shifts matter. Transition periods slow decisions but can refresh budgets for new initiatives.

- Shutdowns pause awards/payments, pressuring liquidity

- 2018–19 CBO cost: 11 billion dollars

- Federal contracting >600 billion dollars/year

- Diversify beyond federal to soften shocks

Cyber workforce and industrial policy

Federal incentives for cyber talent and onshoring — anchored by the CHIPS and Science Act (about 52 billion allocated for semiconductor and related manufacturing) — can ease Telos staffing and facility siting; 2024 saw expanded CHIPS-related pilot grants and public–private cyber pilots. Buy American and tightened supply‑chain rules raise sourcing costs but favor domestic suppliers. Active participation in standards bodies shapes compliance and future procurement requirements.

- CHIPS funding: 52 billion

- 2024: expanded CHIPS/cyber pilots

- Buy American: tighter sourcing

- Standards bodies: influence future rules

Federal defense budgets, cyber mandates and CHIPS Act reshape contractor backlog and costs

DoD/federal budgets (US FY2024 ≈ $858B; federal contracting >600B/yr) and multi‑year IDIQ/GWACs drive Telos revenue visibility and backlog. Cyber mandates (Zero Trust, NIST SP 800‑207) and export controls expand addressable spend but raise compliance costs. CHIPS & Science Act ($52B) and Buy American push onshoring, easing staffing but increasing supplier costs.

| Factor | 2024–25 metric | Impact |

|---|---|---|

| Defense/Fed spend | $858B (FY2024); >$600B contracting | Smooths backlog; award timing risk |

| Cyber mandates | Zero Trust/Ongoing OMB rules | Procurement pull; compliance barrier |

| Onshoring | $52B CHIPS | Talent/facility support; higher costs |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Telos, with data-backed trends and region-specific regulatory context; designed for executives and investors, it offers forward-looking insights, actionable sub-points and clean formatting for reports, decks, and scenario planning.

A concise, visually segmented Telos PESTLE summary that relieves briefing pain by offering clear, editable insights for meetings, presentations, and cross‑team alignment—easy to drop into slides, annotate for local context, and share across devices.

Economic factors

IT spending cycles and macro conditions

Recessions compress discretionary enterprise security spend, slowing sales cycles and procurement; mission-critical federal programs remain more resilient though milestone timing can slip. Inflation-driven wage and cloud cost increases have raised input costs industrywide. Telos benefits from long-term federal contracts that provide revenue visibility; U.S. federal IT spending exceeds $100 billion annually.

Cost of capital and cash conversion

Higher policy rates (federal funds ~5.25–5.50% and 10-year Treasury ~4.2% in mid‑2025) lift borrowing costs and customer hurdle rates, slowing new deal economics. Longer federal billing DSO increases working capital strain for Telos, while fixed‑price contracts magnify execution risk amid inflation. Efficient backlog delivery and timely contract closeouts support margins and cash conversion.

Competitive pricing and consolidation

Cybersecurity remains crowded, driving intense price competition as global cybersecurity spending topped $200 billion in 2024; large platform vendors bundle services to defend share and pressure point-solutions on price. M&A activity continues reshaping the landscape, creating exit pathways or new integrated rivals. Differentiation via certifications and FedRAMP Moderate/High authorizations (several hundred approvals by 2024) helps sustain pricing power.

Cloud migration and SaaS mix

Shift to cloud security and SaaS mix improves revenue quality as enterprise cloud spend approached roughly $620B in 2024, driving higher-margin subscriptions; FedRAMP-authorized SaaS offerings can unlock sticky ARR by easing federal procurement and retention. Usage-based pricing boosts adoption but increases COGS volatility and gross-margin pressure. Partner ecosystems materially influence pipeline and deal flow, amplifying go-to-market reach.

- cloud_spend_2024: ~$620B

- subscription_stickiness: FedRAMP aids ARR retention

- pricing_risk: usage-based raises COGS variability

- partners: amplify deal flow

Dollar strength and international demand

Dollar strength (DXY ~105 in July 2025) raises Telos pricing in non-USD markets, eroding competitiveness and margins as local buyers face higher costs; multinational clients often defer security projects in economic slowdowns, while public-sector and allied governments—with global defense spending near $2.24 trillion in 2023—tend to sustain security allocations, making local partnerships crucial to manage procurement and currency/payment risk.

- Impact: weaker price competitiveness in FX-volatile markets

- Demand risk: project delays by global enterprises

- Resilience: public-sector security budgets remain a stable revenue base

- Mitigation: local partners reduce procurement and payment exposure

Federal defense budgets, cyber mandates and CHIPS Act reshape contractor backlog and costs

Recessionary pressure and higher rates (~federal funds 5.25–5.50% mid‑2025) tighten enterprise spend but federal contracts (> $100B IT spend) provide revenue stability. Inflation and cloud cost growth compress margins; shift to SaaS/cloud (cloud spend ~$620B in 2024) improves ARR quality. FX strength (DXY ~105 Jul‑2025) pressures non‑USD margins; FedRAMP and backlog execution sustain pricing power.

| Metric | Value |

|---|---|

| Federal IT spend | > $100B (annual) |

| Global cyber spend | $200B (2024) |

| Cloud spend | $620B (2024) |

| Fed funds | ~5.25–5.50% (mid‑2025) |

| DXY | ~105 (Jul‑2025) |

Preview the Actual Deliverable

Telos PESTLE Analysis

The preview shown here is the exact Telos PESTLE Analysis document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment as displayed; no placeholders or teasers. After checkout you’ll immediately be able to download this same finished file.

Description

Skip the Research. Get the Strategy.

Gain competitive clarity with our PESTLE analysis of Telos—concise, actionable insights into political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists, it's ready to use and fully editable. Purchase the full report now for the complete deep-dive.

Political factors

Federal cyber budgets and procurement

DoD and civilian cyber appropriations, allocated in multi-billion-dollar federal IT and defense budgets, directly shape Telos’ pipeline and award cadence by determining program starts and task-order volumes. Multi-year appropriations and IDIQ/GWAC vehicles convert one-off buys into stable, multi-year task orders that smooth revenue and backlog. Continuing resolutions or budget delays defer contract kickoffs and elongate sales cycles, compressing near-term revenue. Securing positions on priority programs and GWAC pools mitigates award volatility and shortens capture timelines.

Zero Trust and national cyber strategy

White House Executive Order on Improving the Nation’s Cybersecurity (May 12, 2021) and OMB Memorandum M-22-09 (March 7, 2022) drive Zero Trust adoption across federal agencies. These mandates create procurement pull for identity, cloud and network security vendors and align with NIST SP 800-207 (Aug 2020) and agency reference architectures to speed deployment. Noncompliance can disqualify vendors from federal bids.

Geopolitical tensions and threat intensity

Rising nation-state activity lifts demand for hardened communications and cyber solutions as global military spending topped about $2.3 trillion in 2023 (SIPRI) and major budgets like the US FY2024 defense bill near $858 billion. Classified and cross-border work expands but increases onboarding complexity and compliance. Urgent operational needs push sole-source and rapid acquisitions. Export controls and alliance frameworks such as AUKUS and NATO shape international market access.

Government shutdown and election cycle risk

Government shutdowns pause contracting actions and payments, straining cash flow—CBO estimated the 2018–2019 shutdown cost the economy about 11 billion dollars, with federal contractors facing delayed invoices. Election turnovers can reorder program priorities and funding lines; federal contracting exceeds 600 billion dollars annually, so shifts matter. Transition periods slow decisions but can refresh budgets for new initiatives.

- Shutdowns pause awards/payments, pressuring liquidity

- 2018–19 CBO cost: 11 billion dollars

- Federal contracting >600 billion dollars/year

- Diversify beyond federal to soften shocks

Cyber workforce and industrial policy

Federal incentives for cyber talent and onshoring — anchored by the CHIPS and Science Act (about 52 billion allocated for semiconductor and related manufacturing) — can ease Telos staffing and facility siting; 2024 saw expanded CHIPS-related pilot grants and public–private cyber pilots. Buy American and tightened supply‑chain rules raise sourcing costs but favor domestic suppliers. Active participation in standards bodies shapes compliance and future procurement requirements.

- CHIPS funding: 52 billion

- 2024: expanded CHIPS/cyber pilots

- Buy American: tighter sourcing

- Standards bodies: influence future rules

Federal defense budgets, cyber mandates and CHIPS Act reshape contractor backlog and costs

DoD/federal budgets (US FY2024 ≈ $858B; federal contracting >600B/yr) and multi‑year IDIQ/GWACs drive Telos revenue visibility and backlog. Cyber mandates (Zero Trust, NIST SP 800‑207) and export controls expand addressable spend but raise compliance costs. CHIPS & Science Act ($52B) and Buy American push onshoring, easing staffing but increasing supplier costs.

| Factor | 2024–25 metric | Impact |

|---|---|---|

| Defense/Fed spend | $858B (FY2024); >$600B contracting | Smooths backlog; award timing risk |

| Cyber mandates | Zero Trust/Ongoing OMB rules | Procurement pull; compliance barrier |

| Onshoring | $52B CHIPS | Talent/facility support; higher costs |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Telos, with data-backed trends and region-specific regulatory context; designed for executives and investors, it offers forward-looking insights, actionable sub-points and clean formatting for reports, decks, and scenario planning.

A concise, visually segmented Telos PESTLE summary that relieves briefing pain by offering clear, editable insights for meetings, presentations, and cross‑team alignment—easy to drop into slides, annotate for local context, and share across devices.

Economic factors

IT spending cycles and macro conditions

Recessions compress discretionary enterprise security spend, slowing sales cycles and procurement; mission-critical federal programs remain more resilient though milestone timing can slip. Inflation-driven wage and cloud cost increases have raised input costs industrywide. Telos benefits from long-term federal contracts that provide revenue visibility; U.S. federal IT spending exceeds $100 billion annually.

Cost of capital and cash conversion

Higher policy rates (federal funds ~5.25–5.50% and 10-year Treasury ~4.2% in mid‑2025) lift borrowing costs and customer hurdle rates, slowing new deal economics. Longer federal billing DSO increases working capital strain for Telos, while fixed‑price contracts magnify execution risk amid inflation. Efficient backlog delivery and timely contract closeouts support margins and cash conversion.

Competitive pricing and consolidation

Cybersecurity remains crowded, driving intense price competition as global cybersecurity spending topped $200 billion in 2024; large platform vendors bundle services to defend share and pressure point-solutions on price. M&A activity continues reshaping the landscape, creating exit pathways or new integrated rivals. Differentiation via certifications and FedRAMP Moderate/High authorizations (several hundred approvals by 2024) helps sustain pricing power.

Cloud migration and SaaS mix

Shift to cloud security and SaaS mix improves revenue quality as enterprise cloud spend approached roughly $620B in 2024, driving higher-margin subscriptions; FedRAMP-authorized SaaS offerings can unlock sticky ARR by easing federal procurement and retention. Usage-based pricing boosts adoption but increases COGS volatility and gross-margin pressure. Partner ecosystems materially influence pipeline and deal flow, amplifying go-to-market reach.

- cloud_spend_2024: ~$620B

- subscription_stickiness: FedRAMP aids ARR retention

- pricing_risk: usage-based raises COGS variability

- partners: amplify deal flow

Dollar strength and international demand

Dollar strength (DXY ~105 in July 2025) raises Telos pricing in non-USD markets, eroding competitiveness and margins as local buyers face higher costs; multinational clients often defer security projects in economic slowdowns, while public-sector and allied governments—with global defense spending near $2.24 trillion in 2023—tend to sustain security allocations, making local partnerships crucial to manage procurement and currency/payment risk.

- Impact: weaker price competitiveness in FX-volatile markets

- Demand risk: project delays by global enterprises

- Resilience: public-sector security budgets remain a stable revenue base

- Mitigation: local partners reduce procurement and payment exposure

Federal defense budgets, cyber mandates and CHIPS Act reshape contractor backlog and costs

Recessionary pressure and higher rates (~federal funds 5.25–5.50% mid‑2025) tighten enterprise spend but federal contracts (> $100B IT spend) provide revenue stability. Inflation and cloud cost growth compress margins; shift to SaaS/cloud (cloud spend ~$620B in 2024) improves ARR quality. FX strength (DXY ~105 Jul‑2025) pressures non‑USD margins; FedRAMP and backlog execution sustain pricing power.

| Metric | Value |

|---|---|

| Federal IT spend | > $100B (annual) |

| Global cyber spend | $200B (2024) |

| Cloud spend | $620B (2024) |

| Fed funds | ~5.25–5.50% (mid‑2025) |

| DXY | ~105 (Jul‑2025) |

Preview the Actual Deliverable

Telos PESTLE Analysis

The preview shown here is the exact Telos PESTLE Analysis document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment as displayed; no placeholders or teasers. After checkout you’ll immediately be able to download this same finished file.